Case Law Details

In re Metro Brands Limited (CAAR Mumbai)

M/s Metro Brands Limited filed an application before the Customs Authority for Advance Rulings (CAAR), Mumbai seeking an advance ruling on whether imports of footwear from Vietnam and Bangladesh under eligible Free Trade Agreement (FTA) notifications qualify for the benefit of NIL Agriculture Infrastructure and Development Cess (AIDC) under Serial No. 19 of Notification No. 11/2021-Customs dated 01.02.2021 where the importer claims and is allowed a concessional rate of Basic Customs Duty (BCD), and not necessarily a NIL rate. The applicant imports footwear under CTH 6402, 6403 and 6404 from Vietnam, Bangladesh, Brazil, Cambodia and China, and avails preferential BCD under Notification No. 46/2011-Customs (AIFTA) and Notification No. 99/2011-Customs (SAFTA) supported by valid Certificates of Origin and compliance with the Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR). Effective from 02.02.2025, BCD on footwear was reduced from 35% to 20%, Social Welfare Surcharge was exempted, and AIDC at 18.5% became applicable, while Notification No. 11/2021-Customs provided a NIL AIDC rate under Serial No. 19 for goods where exemption from BCD is claimed and allowed under specified notifications listed in its Annexure.

The applicant contended that Notification Nos. 46/2011-Customs and 99/2011-Customs are expressly included in the Annexure to Notification No. 11/2021-Customs. It argued that Section 25(1) of the Customs Act, 1962 empowers the Government to exempt goods from the whole or any part of customs duty, meaning that both complete and partial exemptions constitute “exemption” for the purposes of Serial No. 19. The applicant further relied on Annexure C of the Union Budget, 2021, stating that imports under FTAs were intended to remain exempt from AIDC, and submitted that nothing in Notification No. 11/2021-Customs restricts the benefit only to cases where BCD becomes NIL. According to the applicant, once concessional BCD under an eligible FTA notification is claimed and allowed, the conditions of Serial No. 19 stand fulfilled.

Before examining the merits, CAAR considered whether the application was barred under Section 28I of the Customs Act, 1962 on the ground that the Directorate of Revenue Intelligence (DRI) was investigating alleged AIDC issues. The jurisdictional Commissionerate argued that the matter was under investigation and therefore the application should not be entertained. The Authority examined the facts and found that only query letters, audit correspondence, representations and investigation were pending, while no consultative letter or show cause notice had been issued on the question raised in the application. It observed that no adjudication proceedings had been initiated before any authority, tribunal or court. Referring to the legal position emerging from earlier decisions, the Authority held that mere investigation or information gathering does not amount to a “pending” question under Section 28I(2). The statutory bar is attracted only where formal proceedings requiring adjudication have commenced. Consequently, the objection to maintainability was rejected and the application was held admissible.

On the substantive issue, the Authority analysed the statutory framework governing AIDC and the exemption notification. It noted that AIDC is levied under Section 124 of the Finance Act, 2021 and that Notification No. 11/2021-Customs grants exemptions in specified circumstances under Section 25(1) of the Customs Act. Footwear falling under CTH 6402, 6403 and 6404 ordinarily attracts AIDC at 18.5% under Serial No. 14A. However, Serial No. 19 grants a NIL rate where exemption from BCD is claimed and allowed under notifications specified in the Annexure. Notification Nos. 46/2011-Customs and 99/2011-Customs are included in that Annexure, and the applicant’s imports from Vietnam and Bangladesh fall within their scope. Notification No. 46/2011-Customs provides both concessional and NIL BCD rates depending on tariff classification, while Notification No. 99/2011-Customs grants full exemption from BCD to eligible imports from Bangladesh, subject to its conditions. The Authority concluded that the applicant’s imports are covered by the relevant FTA notifications, subject to production of a valid Certificate of Origin, fulfilment of the respective notification conditions and compliance with CAROTAR, 2020 to the satisfaction of the proper officer.

The Authority then interpreted the expression “exemption from basic customs duty is claimed and allowed” appearing in Serial No. 19. It held that Section 25(1) expressly recognises exemption from the whole or any part of customs duty, thereby covering both absolute and partial exemptions. Since Serial No. 19 contains no words restricting its application only to cases where BCD becomes NIL, importing such a limitation into the notification would be impermissible. Accordingly, the expression “exemption from BCD” includes both complete and concessional exemptions granted under notifications issued under Section 25. The Authority further held that the applicant satisfies the conditions of Serial No. 19 by claiming and being allowed exemption under Notification Nos. 46/2011-Customs and 99/2011-Customs, subject to compliance with the applicable conditions, Certificates of Origin and CAROTAR requirements. It also noted that Annexure C to the Union Budget, 2021 reflects the legislative intent that imports under FTAs should remain outside the ambit of AIDC, and that Notification No. 11/2021-Customs contains no restriction on simultaneous availment of FTA-based concessional BCD and AIDC exemption.

The Authority concluded that the application was maintainable under Section 28I of the Customs Act, 1962, as no formal proceedings on the question raised were pending. On merits, it held that the expression “exemption from Basic Customs Duty is claimed and allowed” in Serial No. 19 of Notification No. 11/2021-Customs includes both full and partial BCD exemptions under Section 25(1) of the Customs Act. Consequently, goods imported under Notification No. 46/2011-Customs (AIFTA) and Notification No. 99/2011-Customs (SAFTA) are eligible for the NIL rate of AIDC under Serial No. 19 even where BCD is allowed at a concessional rate, subject to fulfilment of the prescribed conditions, including production of a valid Certificate of Origin and compliance with CAROTAR, 2020 to the satisfaction of the proper officer at the time of import. The Authority ruled accordingly.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, MUMBAI

M/s Metro Brands Limited (having IEC No. 0303084448) and (hereinafter referred to as ‘the applicant’, in short) filed application (CAAR-1) for advance ruling before the Customs Authority for Advance Rulings, Mumbai (CAAR in short). The said application was received in the secretariat of the CAAR, Mumbai on 03.12.2025 along with enclosures in terms of Section 2811 (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Act’ also).

2. The applicant has sought an advance ruling to obtain clarity regarding the applicability of NIL Agriculture Infrastructure and Development Cess (AIDC) under Serial No. 19 of AIDC Exemption Notification No. 11/2021-Customs dated 1st February 2021 (hereinafter referred to as ‘ AIDC Exemption Notification ‘, in short). The said benefit is available in respect of imports made under the Free Trade Agreement (FTA) notifications specified in the Annexure to the notification, subject to the condition that the importer claims and is granted a concessional rate of Basic Customs Duty (BCD) under the relevant FTA notification.

3. Submission by Applicant-

3.1. M/s Metro Brands Limited is one of India’s largest and oldest footwear and accessories specialty retailers, headquartered in Mumbai, having commenced operations in 1955 and currently operating an extensive network of 928 retail stores across 206 cities in 31 States and Union Territories and is therefore a well-established importer of footwear products sourced from multiple international manufacturing hubs such as Vietnam, Bangladesh, Brazil, Cambodia and China. As part of their operations, the Company imports specified footwears from Vietnam, Bangladesh, Brazil, Cambodia and China.

3.2. The Applicant is engaged in importing under various categories of footwear falling under I ISN 6402, 6403 and 6404. The Applicant is engaged in the import of footwear under these I leadings from Vietnam, Bangladesh, Brazil, Bangladesh and Cambodia.

3.3. The imports are undertaken through major ports including Nhava Sheva, ACC Mumbai and Land Customs Station Petrapolc (West Bengal) from Vietnam, Bangladesh and Brazil. On imports from Vietnam and Bangladesh, the applicant avails benefit of relevant Free Trade Agreements (FTAs) viz India ASEAN FTA (AIFTA) and South Asian Free Trade Agreement (SAFTA) duly backed by a Certificate of Origin (COO) as prescribed in the said FTAs in terms of Rules of Origin (RoO).

3.4. Up till 1st February 2025, the customs duty applicable to footwear under Customs Tariff Head (CTH) 6402, 6403 and 6404 was as per the First Schedule to the Customs Tariff Act, 1975 (Customs Tariff Act) i.e., Basic Customs Duty (BCD) of 35%.

3.5. Effective from 2nd February 2025, the following changes were brought in relation to the import of footwear classified under I-ISN 6401 to 6405 —

- BCD rate reduced from 35% to 20%

- Social Welfare Surcharge (SWS) earlier levied @10% of BCD exempted on all footwear classified under CTH 6401 to 6405.

- Agriculture Infrastructure and Development Cess (AIDC) is levied (4), 5% on import of footwear classified under CTI1 6401 to 6405. However, despite the reduction in 13CD and elimination of SWS, balanced by the insertion of AIDC, overall, there was no change in the effective rate of customs duty applicable on imports of footwear.

3.6. Further, in case of AIDC, specific exemption is extended from the levy, on specified goods as listed and notified in Notification No 11/2021-Customs dated 1st February 2021 as amended (AIDC Exemption Notification).

3.7. Serial No. 19 of AIDC Exemption Notification specifically extends exemption from AIDC against specific exemption notification as listed in Annexure to the notification wherein the importer is allowed to claim exemption from BCD. The relevant portion of Serial No. 19 is reproduced below for case of reference.

…… “all goods on which exemption from basic customs duty is claimed and allowed under the notifications, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (0, mentioned in the ANNEXURE.” ….”

3.8. The Annexure to the AIDC exemption notification lists specified exemption notifications including those under specific FTAs for grant of exemption from AIDC on imports.

3.9. On perusal of the Annexure of the AIDC exemption notification vis-a-vis the details as mentioned in the background earlier, the following can be summarized vis-à-vis eligibility of exemption from AIDC in relation to goods imported by the Company.

| Countries | Coverage | FTA | AIDC Exemption Notification (Annexure Reference) |

| Bangladesh | Yes | SAE IA | Notification No. 99/2011-Customs dated 9 November 2011 at Serial No 9 |

| Vietnam | Yes | ASEAN | Notification No. 46/2011-Customs dated 1 June 2011 at Serial No 4 |

3.10. To explain further,, the preferential duty benefit under the AIFTA is affected vide Notification No. 46/2011 — Customs dated 01.06.2011 issued by the Central Government under Section 25 (1) of the Customs Act, 1962 (Customs Act). Serial number 904, 905, 906, 909 and 910 exempts goods falling under Customs Tariff Sub-heading 64029990, 64031990, 6403990 and 64041990 respectively.

3.11. In respect of the above listed classification, Sr. No. 903, 904, 905, 906, 907, 908, 909 and 910 of the said notification provides for complete as well as partial exemption from payment of duty with respect to goods covered under Tariff heading 6402 to 6404. The relevant portion of the Notification has been extracted below for reference.

| Sr. No. |

Chapter Heading, subheading and Tariff Item | Description | Rate (in percentage unless otherwise specified) |

|

| 903 | 640110 to640212 | All Goods | 5.00 | 5.00 |

| 904 | 640220 to 640299 | All Goods | 5.00 | 5.00 |

| 905 | 640312 | All Goods | 0.00 | 0.00 |

| 906 | 640319 to 640391 | All Goods, other than Footwear made on a base or platform of wood, not having an inner sole or a protective metal toe-cap | 5.00 | 5.00 |

| 907 | 64039190 | Footwear made on a base or platform of wood not having aninner sole or a protective metal toe-cap | 0.00 | |

| 908 | 640399 | All Goods, other than Footwear made on a base or platform of wood not having an inner sole or a protective metal. toe-cap .and not covering ankle | 5.00 | 5.00 |

| 909 | 64039990 | Footwear made on a base or . platform of wood not having an inner sole or a protective metal toe-cap and not covering ankle | 0.00 | 0.00 |

| 910 | 6404 | All Goods | 5.00 | 5.00 |

3.12. Similarly, preferential duty benefit under the SAFTA is affected vide Notification No. 99/2011 — Customs dated 09.11.2011, (SAFTA Notification) issued by the Central Government under Section 25 (1) of the Customs Act. The said notification exempts all goods other than those mentioned in the ANNEXURE to this notification (i.e., 2203 to 2206, 220710, 2208, Chapter 24), from the whole of the duty of customs leviable thereon under the First Schedule to the Customs Tariff Act, when imported into India from a country listed in APPENDIX to this notification (i.e., People’s Republic of Bangladesh, Kingdom of Bhutan, Republic of Maldives, Nepal and Islamic Republic of Afghanistan.

3.13. Thus, it can be inferred that the goods falling under CTH 6402 to 6404 too are exempt from BCD when imported from Bangladesh into India under SAFTA against a valid COO.

3.14. In simpler words. AIDC is generally leviable on the subject goods. However, for imports made under specified FTAs, the AIDC is effectively reduced to nil by virtue of Serial No. 19 read with the relevant Annexure of AIDC exemption notification.

3.15. The Applicant proposes to import these goods under an eligible FTA. While AIDC is otherwise leviable under Serial No. 14A, an exemption is concurrently available under Serial No. 19 read with the Annexure.

3.16. In other words, imports under FTAs against the aforementioned exemption notifications are covered and eligible for exemption from AIDC.

3.17. In view of the above, the Applicant seeks an Advance Ruling from the I Hon’ble Authority to confirm the eligibility to claim the nil AIDC benefit under Serial No. 19 for such FTA-based imports.

3.18. The Advance Ruling application at Serial No. 11 seeks the following information from the application

“Whether the question(s) raised is pending in the applicant’s case before any officer of Customs, Appellate Tribunal or any Court of Law? If so, provide relevant details.”

3.19 The Applicant in response to above submitted that the question of appropriate classification of the Subject Goods under Customs Tariff and the applicability of a notification issued under sub-section (1) of section 25 of the Customs Act is not pending in the Applicant’s case before any officer of Customs, Appellate Tribunal or any Court of Law.

3.20. In October 2025 Applicant was issued a letter by Directorate of Revenue Intelligence (DRI) seeking information on imports made from February 2025 till date. Further, there was a consultative letter issued by Commissioner, Customs (Audit), Mumbai in relation to 1 Bill of Entry (130E) wherein incorrect exemption was claimed which was explained as well.

3.21. The relevant extract of the applicable provisions and jurisprudence on the subject is as below. Section 28 I of the Customs Act lays down the procedure to be followed on receipt of an application for an Advance Ruling. Amongst others, the said Section provides the’ list of scenario’s where an advance ruling application may not be accepted. The said list is as follows:

- Where the question raised in the application is already pending in the Applicant’s case before any officer of customs, the Appellate Tribunal or any Court; and

- Where the same as in a matter already decided by the Appellate Tribunal or any Court.

3.22. An extract of the applicable provision is as under —

Section 281 Procedure on receipt of application. —

(1) …

(2) The Authority may, after examining the application and the records called for, by order, either allow or reject the application:

Provided that the Authority shall not allow the application 3 */ where the question raised in the

application is –

(a) already pending in the applicant’s case before any officer of customs,. the Appellate Tribunal or any Court;

(b) the same as in a matter already decided by the Appellate Tribunal or any Court:.

Provided further that no application shall be rejected under this sub-section, unless an opportunity has been given to the applicant of being heard:

Provided also that where the application is rejected, reasons for such rejection shall be given in the order.

(3)

3.23. A bare perusal of the above relevant provisions provides that ,the question raised in the application has to be already pending before any officer of Customs, the Appellate Tribunal or any Court. In this regard reliance can be placed on the case of DRI versus Mis Spray-tee India. Ltd , wherein an appeal was filed by the DRI against an Advance Ruling issued on classification of actuator and aerosol valves meant for perfumes and toilet sprays. The DRI appealed to declare the said Advance Ruling as void ab initio on grounds that the fact of DRI investigation was not disclosed by the applicant and such an action amounted to misrepresentation of facts and fraud. The Hon’ble Delhi High Court held that the DRI had not issued any pre-consultation notice or show cause notice which would indicate that the question regarding classification of any goods was pending. In order for a question to be considered as pending before any officer of customs, it would be necessary for the question to be raised in any notice enabling the assessee to respond to the said issue. It is only after this stage that it would be necessary for the officer of customs to render its decision on the question. Merely because an officer of customs contemplates that a question may arise, does, not mean that the question is pending consideration. For a question to be stated to be pending, the concerned officer must formally set forth the same for the assessee to contest the same.

3.24. Further, in re: HQ Lamps Manufacturing Co. Pvt Ltd, the Hon’ble Customs Authority for Advance Rulings (CAAR.) has examined the ambit of the expression “where the question raised in the application is already pending in the Applicant’s case before any officer of customs.,” in detail. It was held that the said proviso gets attracted only in certain scenarios.. An illustrative list of such scenarios is as follows:

- Wherein a Show Cause Notice has been issued

- ROE has been provisionally assessed under section 18 of the Customs Act

- The matter is pending before the Special Valuation Branch of the Customs Commissionerate for the purpose of valuation of the goods in question

- The proper officer has held the pre-notice consultation with the applicant in terms of the proviso of subsection (a) of Section 28(1) of the Customs Act.

3.25. In light of the applicable provisions and prevalent jurisprudence, it can be concluded that for an Advance Ruling application to be barred under the provisions of the Section 281 of the Customs Act, issuance of a Show-Cause Notice (SCN) is a pre-condition. Further, mere investigation or letters issued by Revenue authorities seeking information cannot be understood to be covered under the purview of “question pending before any officer of Customs, Appellate Tribunal or any Court of Law”.

3.26. Hence, it is submitted by the Applicant that the Hon’ble CAAR has jurisdiction to entertain the instant application as no SCN has been issued by the DRI against the Applicant concerning the claim of exemption the applicability of Exemption notification.

3.27. Since the. DRI or the Customs authorities have not issued any SCN as yet, it is humbly subrhitted that the question of law in this application is not pending before any officer of customs, the Appellate Tribunal or any Court and that the Hon’ble CAAR has jurisdiction to accept this application as the same is not barred under the provisions of the Section 281 of the Customs Act. Further, the objective of the ruling is to seek certainty on availability of exemption going forward.

3.28. The importer complies with the requirement of COO and also undertakes compliances as required under Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR) as per the direction of the Customs authorities.

4. Whether the benefit of NIL AIDC under Serial No. 19 of AIDC Exemption Notification shall be available on imports made under the FTA notifications listed in its Annexure, in eases where the importer claims and is allowed a concessional rate of 13C1) under such FTA notifications

4.1 The Applicant submitted that the question raised before this Hon’ble Authority must be answered by reading together all the relevant legal provisions, namely Section 25 of the Customs Act, the policy explanation contained in Annexure C of the Union Budget 2021, the structure and wording of AIDC Exemption Notification and the FTA notifications listed in its Annexure. When these provisions arc seen together, and when they are applied to the Applicant’s actual manner of import under AIFTA and SAFTA, it becomes clear that the Applicant’s goods fully meet the conditions for exemption from AIDC under Serial No. 19 of AIDC Exemption Notification.

4.2 AIDC Exemption Notification forms the basis for the levy and exemption of the AIDC on imported goods, and its language is central to the present application.

4.3 The said Notification contains a schedule in which various tariff items attract AIDC at prescribed rates. Footwear falling under CTI 16402 to 6405 is covered under Serial No. 14A of this schedule and is ordinarily subject to AIDC at the rate of 18.5 percent. However, it also contains Serial No. 19, which provides that AIDC shall be levied at the rate of NIL on goods for which exemption from BCD is “claimed and allowed” under the notifications listed in the Annexure to the AIDC Notification.

4.4 The Annexure to the notification expressly includes Notification No. 46/2011-Customs relating to AIFTA and Notification No. 99/2011-Customs relating to SAFTA, both of which govern the Applicant’s imports. A close and careful reading of Serial No. 19 shows that it is framed in broad, unconditional terms. The exemption becomes applicable once two objective conditions are met: first, the importer must claim exemption from Basic Customs Duty under one of the notifications listed in the Annexure; and second, such exemption must be allowed by the proper officer upon verification.

4.5 The structure of AIDC Exemption Notification, thus establishes a clear legal framework: goods that are otherwise liable to AIDC under the tariff entries set out in the Notification may nonetheless become eligible for a complete waiver of AIDC if they satisfy the limited conditions prescribed in Serial No..19. The Applicant would like to highlight that since the Applicant imports footwear from FTA partner countries under notifications specifically included in the Annexure and since such imports would be assessed to a concessional BCD rate upon verification of the COO and compliance with CAROTAR requirements, the conditions of Serial No. 19 would stand fulfilled.

4.6 It is imperative to note that the wording of the AMC Exemption Notification supports the position that goods imported under the FTA notifications listed in the Annexure arc eligible for nil AIDC once the claim for BCI) exemption under such notifications is admitted. The Notification does not incorporate any further qualifications or exclusions that would limit the benefit based on the extent of I3CD reduction.

4.7 Thus, it can he said that the Notification does not draw any distinction between full and partial exemptions, nor does it require that the I3CD be reduced to zero.

4.8 The Applicant would now like to put some light on the operative expression “exemption from BCD” that must therefore be understood in the sense in which the term “exemption” is used under Section 25 of the Customs Act i.e., the parent provision under which all the relevant notifications have been issued.

4.9 Section 25 of the Customs Act, which is the parent statutory power enabling the Government to issue exemption notifications in the “public interest.” Section 25(1) explicitly provides that the Government may exempt goods “from the whole or any part of the duty of customs leviable thereon,” and this formulation is unambiguously deliberate, because it not only recognizes but legally equates partial duty relief with full duty relief.

4.10 In other words, the statute itself instructs that any reduction in the quantum of duty whether the rate is reduced by 5%, 50% or 100% is nonetheless an “exemption.” It follows necessarily that whenever a subsequent notification, such as Notification No. 11/2021-Customs, predicates a benefit upon the presence of an “exemption from BCD,” that phrase, being used in delegated legislation issued under Section 25, must inherit the full statutory meaning conferred by the parent statute.

4.11 Any narrower interpretation would effectively read down the statutory language of Section 25 and impose an artificial and unwarranted distinction that the Legislature itself did not intend.

4.12 The Applicant would like to bring to your attention that the intention of the legislature regarding AIDC and its interaction with concessional duty schemes becomes clearer when we refer to Annexure C of the Union Budget 2021 discussed in detail below.

4.13 The Applicant submitted that Annexure C of the Union Budget 2021 provides essential context for understanding the scheme under which the AIDC was introduced and the manner in which AIDC interacts with existing concessional duty structures such as FTAs. Annexure C forms part of the official budget documents and therefore serves as a contemporaneous source explaining the policy framework within which AIDC Exemption Notification was issued.

4.14 Accordingly, this annexure is a valuable interpretative aid for appreciating the scope and purpose of the exemptions embedded in Serial No. 19 of the AIDC Notification.

4.15 On a careful reading of Annexure C, it shows that AIDC was conceived as a customs duty-type impost introduced under Clause 115 of the Finance Bill, 2021. The Annexure clarifies that, simultaneously with the imposition of AIDC, the Government had lowered the BCD rates on the very goods on which AIDC was being imposed. This parallel reduction in BCD reflects a calibrated approach, designed to ensure that the overall import duty burden remained broadly neutral even after the introduction of AIDC.

4.16 Within this policy backdrop, paragraph (4) of Annexure C assumes particular importance for the present matter. It explicitly states that goods imported under customs duty exemptions available under F’I’As, EOUs and Advance Authorisation schemes are being exempted from AIDC. Although the Annexure does not elaborate on the mechanics of this exemption, it clearly conveys that the introduction of AIDC was not intended to disturb or dilute the existing concessional duty frame Works provided under India’s FTAs. This is especially relevant because F’I’As are commitments entered into by India under international treaties and the tariff concessions offered under such treaties constitute preferential rates that are expected to operate without being offset by additional imposts such as AIDC.

4.17 For the purposes of the present application, the Applicant submitted that paragraph (4) of Annexure C provides important guidance when interpreting Serial No. 19 of A1DC Exemption Notification. Although the notification itself must be applied strictly in accordance with its language. the Budget Annexure provides insight into the fiscal setting within which the notification was issued. The Annexure indicates that imports benefiting from ETA-based duty concessions were envisaged to remain outside the burden of AIDC, which supports a reading of Serial No. 19 that is consistent with this framework. Since Serial No. 19 exempts goods on which “exemption from 13CD is claimed and allowed” under the notifications listed in its Annexure and since the Al ETA and SAFTA notifications applicable to the Applicant’s imports are included in that list, the Applicant’s interpretation that AIDC should not apply once such concessional BCD is allowed is aligned with the policy position reflected in Annexure C.

4.18 Further, nothing in Annexure C suggests that the exemption from AIDC was intended to apply only where the BCD become zero. Instead; the Annexure refers in general terms to goods imported “under Customs duty exemptions available under ETA… schemes.” In the context of Seetion25 of the’ Customs Act, which treats both full and partial duty relief .as “exemption”, this language reasonably supports the view that any- concessional BCD granted under ETA notifications, once allowed-by the proper officer, should attract the nil AIDC treatment under Serial No. 19.–Ilus, the Budget Annexure reinforces the broader understanding that AIDC was not crafted to neutralize or undermine VIA-based preferential tariff benefits but was instead introduced in a -manna that preserves the intended effect of those benefits.

4.19 In order to conclude, the Applicant states that Annexure C of the Union Budget 2021 when read in conjunction with Notification No. 11/2021-Customs and the statutory meaning of “exemption” under Section 25 of the Customs Act, supports the Applicant’s position that imports effected under SAFTA and SAFTA, where the claimed concessional BCD is admitted upon verification, should qualify for the NIL AIDC rate under Serial No. 19 of the AIDC Notification. Annexure indicates that. ETA imports were envisioned to be exempt from /UDC, and the language of the Notification implements this principle without restricting the exemption only to cases of full BCD relief.

4.20 In simpler words. Annexure C makes it clear that AIDC was, introduced along with a reduction in certain I3CD rates so that the overall tax burden remains broadly neutral, and. importantly, it also states that imports made under ETAs, Advance Authorisation and similar concessional mechanisms should not be subjected to. AIDC.

4.21 As discussed earlier, Section 25 of the Customs Act empowers the Central Government to issue exemption notifications “if satisfied that it is necessary in the public interest so to do.” The text of sub-section (1) states that the Government may, by notification in the Official Gazette, exempt goods “from the whole or any part of the duty of customs leviable thereon.” The language used in the section is important, because it makes it clear that the expression “exempt”. is- not restricted :to situations where the entire duty is remitted. The statute expressly recognizes that an exemption may relate either to _the whole of the duty or to any part of it. In other words, partial and full exemptions are both contemplated expressly within the statutory definition of an exemption. There is. no qualification or hierarchy in the section that places. a full exemption on a different footing from a partial exemption, nor is there any requirement that an exemption must reduce the duty to zero.

4.22 Since Section 25 is the enabling provision under which Notification No. 11/2021-Customs (AIDC Exemption Notification), Notification No. 46/2011-Customs (AIFTA), Notification No. 99/2011-Customs (SAFTA) and other ETA notifications have been issued, the meaning of the ward “exemption” contained in Section 25 applies to all notifications issued under it, unless the notification itself contains language that alters or restricts the meaning for the purpose of that particular notification. AIDC Exemption Notification, and specifically Serial No. 19 therein, uses the. phrase “exemption from I3CD is claimed and allowed” without adding any further qualifier regarding the extent or quantum of the exemption. The notification does not specify that the exemption must reduce the I3CD to nil, nor does it distinguish between a complete exemption and a concessional rate. Therefore, when Serial No. 19 refers to an exemption from BCD, it must be understood in the same manner that Section 25 uses the term: an exemption may relate to the whole of the duty or any part of it.

4.23 Thus, the Applicant states that Section 25 provides the foundation for interpreting Serial No. 19 of the AIDC Exemption Notification. It confirms that the term “exemption from BCD,” as used in the Notification, naturally includes both full and partial exemptions granted under notifications issued under the same provision. Accordingly, where an importer claims and is allowed a concessional rate of BCD under a listed ETA notification, such exemption falls within the scope of Serial No. 19, and the nil rate of AIDC becomes applicable as prescribed,

4.24 This position is further reinforced when the AIDC notification is viewed in the wider context of Section 25 of the Customs Act and the pattern of exemptions reflected in the other notifications listed in the Annexure. Section 25 does not impose any requirement that an exemption may be granted only where the underlying duty becomes nil; on the contrary, it expressly contemplates both absolute and partial exemptions, thereby permitting the Government to extend relief even in cases where a concessional rate of duty continues to apply. This statutory structure is mirrored in the notifications included in the Annexure to Notification No. 11/2021-Customs, many of which grant exemption from specified duties notwithstanding the fact that the corresponding BCD under those notifications is not reduced to zero. The presence of such notifications, where the exemption is unquestionably available despite the continuance of a positive BCD rate confirms that neither the statute nor the delegated legislation treats a nil BCD rate as a precondition for availing an exemption under Section 25 notification. Consequently, the exemption from AIDC under Serial No. 19 cannot be interpreted as being contingent upon the BCD being reduced to nil, particularly when the notification itself contains no such stipulation. The consistent legislative pattern, the language of Section 25, and the manner in which exemptions operate across the accompanying notifications collectively demonstrate that the AMC exemption is triggered solely when the importer claims and is allowed exemption from BCD under any of the listed notifications, irrespective of whether such exemption is full or partial.

4.25 The Applicant would now like to bring to the attention of this Hon’ble Authority that the above interpretation gains further support when the wording of AIDC Exemption Notification is examined alongside the manner in which restrictions are expressly drafted in other exemption notifications, such as Notification No. 21/2012-Customs , which deals with the ley and exemption of Special Additional Duty (SAD) under Section 3(5) of the Customs Tariff Act. Notification 21/2012 contains an explicit paragraph stating that its exemption shall not apply to goods in respect of which duty exemption is claimed based on country of origin. This explicit exclusion is extremely significant for interpretative purposes because it demonstrates that when the Central .Government intends to prevent the concurrent enjoyment of two benefits particularly in situations involving origin-based exemptions, it uses clear, firm and unmistakable exclusionary words. The restriction is explicit, unambiguous, and forms an integral part of the notification. This drafting approach demonstrates that such limitations, when intended, are expressly set out in the text of the notification.

4.26 Notification No. 12/2012-Customs, also issued under Section 25(1) of the Customs Act, is a general exemption notification covering a broad range of goods and prescribing reduced or nil rates of BCD for the goods listed in its table.

4.27 Unlike Notification No. 12/2012, AIDC Exemption Notification (Notification No. 11/2021-Customs) does not contain any clause that denies, curtails or limits the availability of its exemptions when an’ importer simultaneously claims benefits under a country-of-origin-based concessional duty notification. The notification applies according to its own terms, and the conditions for each serial number arc confined to those expressly mentioned therein. In simpler words, it can be inferred that the absence of such language in AIDC Exemption Notification must therefore be treated as intentional. Under established principles of delegated legislation, where the Government has shown in one notification how it expresses the intention to exclude concurrency and then omits that expression in another similarly-situated notification issued under the same statutory authority, the omission is a conscious legislative choice.

4.28 Accordingly, when Notification No. 21/2012-Customs is read alongside AIDC Exemption Notification (Notification No. 11/2021-Customs), a consistent principle becomes evident from the plain language of the notifications. Wherever the Central Government. intends to restrict the simultaneous availability of two different exemptions, such as the exemption from SAD under Serial No. 1 of Notification No. 21/2012 vis-à-vis a country-of-origin-based BCD exemption, the restriction is expressly articulated within the text of the notification itself. The limitation is not left to inference; it is clearly and deliberately stated. In contrast, AIDC Exemption Notification (Notification No. 11/2021-Customs) contains no such express prohibition or qualifying condition that would bar the AIDC exemption under Serial No. 19 when a concessional rate of. BCD is availed under an FTA notification. Therefore, the availability of the AIDC exemption cannot be considered displaced merely because the importer simultaneously claims a country-of-origin-based concession,

4.29 Thus, the applicant would like to highlight that when these statutory principles, policy declarations, and drafting comparisons arc applied to the Applicant’s factual situation, the legal conclusion becomes inevitable.

4.30 In the totality of these circumstances, the Applicant submitted that the statutory architecture governing the AIDC, the contemporaneous policy exposition in Annexure C of the Union Budget 2021 and the unambiguous wording of AIDC Exemption Notification together yield a singular and consistent conclusion. Serial No. 19 employs the expression “exemption from BCI)” without qualification, and, by virtue of Section 25 of the Customs Act, that expression necessarily extends to all forms of duty relief, whether full or partial granted under the FTA notifications issued under the same enabling power. The absence of any exclusionary clause in AIDC Exemption Notification, especially when contrasted with the deliberate restrictive drafting adopted in Notification No. 21/2012-Customs, confirms that the Legislature did not intend to curtail the concurrent operation of AIDC exemption with preferential BCD schemes. This interpretation is further fortified by Annexure C, which expressly records that imports under FTAs were envisaged to remain outside the incidence of AIDC. Accordingly, once the concessional BCD claim under AIFTA SAFTA is verified and allowed, the conditions prescribed in Serial No. 19 stand fully satisfied, and the Applicant’s imports are, by operation of law, entitled to the NIL rate of AIDC.

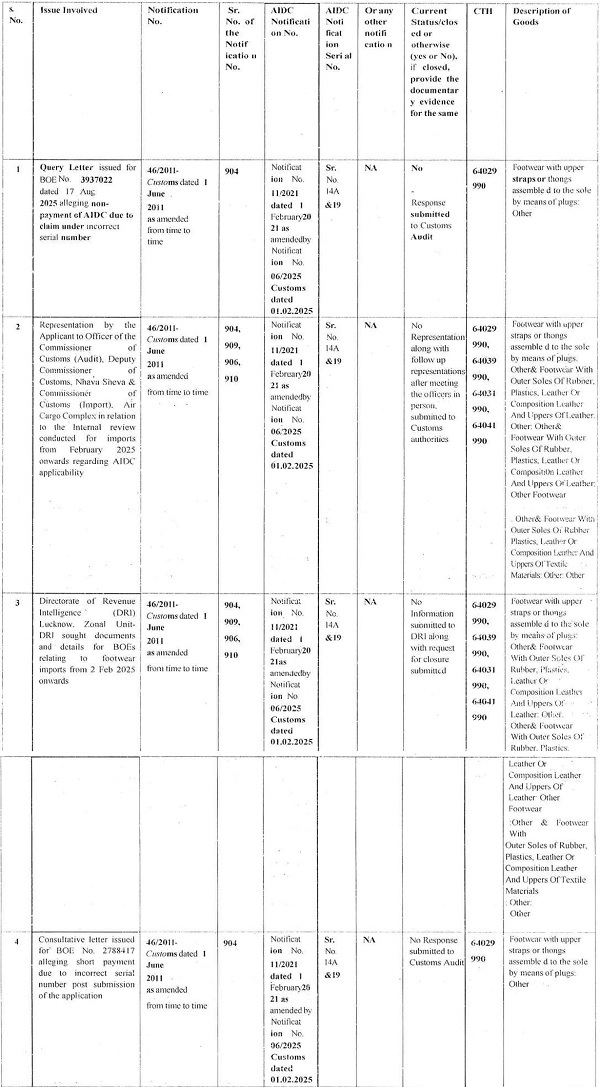

5. The applicant submitted details of all the pending matters before any officer of Customs, CESTAT, High Court, or Supreme Court regarding the “eligibility for exemption from AIDC on specified footwear imported under FTAs” vide letter dated 30.03.2026. The said details submitted by the applicant are in table below:

5.1 Further, the applicant; in the above table at Sr. No. 4, has stated that the issue raised in the consultative letter issued for BOE No. 2788417 by JNCH Audit AIDC pertains to Sr. Nos. 14A and 19. However, upon perusal of the copy of the said consultative letter submitted by the applicant, it is observed that the issue raised therein relates to Sr. Nos. 14A and 17, and riot 14A and 19. Accordingly, clarification in this regard was sought from the applicant.

The applicant, vide letter dated 17.06.2024, clarified and categorically submitted that the aspect of Sr. No. 19 vis-a-vis Sr. No. 14A has never been raised by any authority

6. Applicants’ interpretation of Law:-

6.1. ISSUE FOR DETERMINATION:

6.1.1 The issues before the Hon’ble Authority of Advance Ruling are:

Whether the benefit of NIL AIDC under Serial No. 19 of AlDC Exemption Notification shall be available on imports made under the FT4 notifications listed in its Annexure, in cases where the importer claims and is allowed a concessional rate of BCD under such FT4 notifications

6.1.2 The issue placed for determination has to be appreciated in light of the following legal submissions and their applicability to the transaction undertaken by the Applicant. In this context, the Applicant would like to refer to the following legal provisions:

6.2 RELEVANT LEGAL PROVISIONS

6.2.1 Section 25 of the Customs Act holds power to grant exemption from duty as this is the statutory head under which both the FTA notifications and Notification No.11/2021 were issued and because Section 25 expressly recognizes that an exemption may be “from the whole or any part” of the duty, which is the core legal foundation of our contention that a partial 13C1) concession is still an “exemption.” The relevant extract is reproduced below for ease of reference.

(1). If the Central Government is satisfied that it is necessary in the public interest so to do, it may, by notification in the Official Gazette, exempt generally either absolutely or subject to such conditions (to be Milled before or after clearance) as may be specified in the notification goods of any specified description from the whole or any part of duty of customs leviable thereon.

(2) If the Central Government is satisfied that it is necessary in the public interest so to do, it may, by special order in each case, exempt from the payment of duty, under circumstances of an exceptional nature to be stated in such order, any goods on which duty is leviable.

(2A) The Central Government may, if it considers it necessary or expedient so to do for the

purpose of clarifying the scope or applicability of any notification issued under sub-section (1) or order issued under sub-section (2), insert an explanation in such notification or order, as the case may be, by notification in the Official Gazette, at any time within one year of issue of the notification under sub-section (1) or order under sub-section (2), and every such explanation shall have effect as if it had always been the part of the first such notification or order, as the case may be.]

(3) An exemption under sub-section (1) or sub-section (2) in respect of any goods from any part of the duty of customs leviable thereon (the duty of customs leviable thereon being hereinafter referred to as the statutory duty) may be granted by providing for the levy of a duty on such goods at a rate expressed in a form or method different from the form or method in which the statutory duty is leviable and any exemption granted in relation to any goods in the manner provided in this sub-section shall have effect subject to the condition that the duty of customs chargeable on such goods shall in no case exceed the statutory duty.

Explanation. -“Form or method”, in relation to a rate of duty of customs, means the basis, namely valuation, weight, number, length, area, volume or other measure with reference to which the duty is leviable.] “

6.2.2 Section 124 of the Finance Act, 2021 enables AIDC, because AIDC’s legal basis and its characterization as a duty of customs follows froth the Finance Act and is referred to in AIDC Exemption Notification. The relevant extract is reproduced below for ease of reference.

(1) There shall be levied and collected, in accordance with the provisions of this section, for the purposes of the Union, a duty of customs, to be called Agriculture Infrastructure and Development Cess, on the goods specified in the First Schedule to the Customs ‘Tariff Act, 1975 (51 of 1975.) (hereinafter referred to as the Customs Tariff Act), being the goods imported into India,. at the rate not exceeding the rate of customs duty as specified in the said Schedule, for the purposes of financing the agriculture infrastructure and other development expenditure.

(2) …………………..

(3) Where the duty is leviable on the goods at any percentage of its value, then, for the purposes of calculating the Agriculture Infrastructure and Development Cess–under this section, the value of such goods shall he calculated in the same manner as the value of goods is calculated for the purpose of customs duty under section 14 of the Customs Act, 1962 (52 of 1962.).

(4) The Agriculture Infrastructure and Development Cess on imported goods shall be in addition to any other duties of customs chargeable on such goods, under the Customs Act, 1962 (52 of 1962) or any other law for the tune being in.

(5) …………………..’

6.2.3 AIDC Exemption Notification quote Serial No.I4A which levies –AIDC on the FISN codes 6402 to 6405, however, Serial No.19 which include the Annexure list (showing Notification Nos. 46/2011 and 99/2011 as included), because Serial 19 is the direct operative provision that triggers AIDC = NIL on goods where BCD exemption is claimed and allowed under listed notifications. The relevant extract is reproduced below for–ease of reference.

“In exercise of the powers conferred by sub-section (1) of section 25 of the Customs Act, 1962 (52 of 1962) read with 41section 124 .of the Finance Act, 2021 (13 of 2021)1, the Central Government, on being satisfied that it is necessary in the public interest so to do, hereby exempts goods of the description specified in column (3) of the ‘fable below and falling within the Chapter, heading or sub-heading or tariff item of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) as specified in column (2) of the said Table, from so much of the Agriculture Infrastructure and Development Cess leviable thereon under the 51–said section of the Finance Act, 2021 (13 of 2021)1, as is in excess of the amount calculated at the rate specified _in column (4) of the said Table.

| SI. No. | Chapter or heading I or subheading or tariff item of the First Schedule | Description of goods | Rate |

| 14A | 6401, 6402, 6403, 6404 or 6405 | All goods | 18.5% |

| 19 | Any Chapter | All goods on which exemption from basic customs duty is claimed and allowed under the notifications, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (z), mentioned in the ANNEXURE. | Nil, |

ANNEXURE

| S. No. | Details of the Notifications |

| 4. | Notification No. 46/2011-Customs, dated the 1st June, 2011 vide number G.S.R. 423(E), dated the 1st June, 2011. |

| 9. | Notification No. 99/2011-Customs, dated the 9th November, 2011 vide number G.S.R. 801(E), dated the 9th November, 2011. |

6.2.4 The Union Budget 2021, through Annexure C, sets out the policy rationale and legislative intent underlying the introduction of AIDC. This Budget Annexure is a contemporaneous and authoritative aid to interpret AIDC Exemption Notification because it explains that AIDC was introduced as part of a larger customs duty rationalisation exercise, where certain BCD rates were simultaneously reduced to neutralize the impact of the new levy. Importantly, Annexure C expressly states that imports under FTAs and other specified schemes would be exempt from AMC, thereby confirming that AIDC was not intended to burden goods that already enjoy concessional treatment under Section 25 notifications. This declared intent is critical for interpreting Serial No. 19 of AIDC. Exemption Notification, particularly to establish that the AIDC exemption applies even when the underlying BCD exemption under an FTA is only partial. The relevant extract is reproduced below for ease of reference.

“These changes would .become effective on 02.02.2021, 00:00 hours owing to the declaration made under Provisional Collection of Taxes Act, 1931.

I. Customs:

(1) An Agriculture Infrastructure and Development Cess (AMC), as duty of customs has been proposed /Clause 115 of the Finance Bill, 2021 refers” Enabling provisions has been made for levy of this cess on all imported goods at the rate not exceeding the rate specified in the First Schedule to the Customs TariffAct, 1975. However, it would be levied only on specified goods as detailed below. All other items are being exempted from this Cess…AA

… ….

… ….

… ….

(4) Further, goods imported under customs duty exemptions available under F7A and EMI as well as under advance authorization schemes are being exempted from AIDC.

7. Port of Import and reply from jurisdictional Commissionerate:

The applicant in their CAAR-1 indicated that they intend to import the subject goods from Olo The Commissioner of Customs (NSTIII), Nhava Sheva. The application was forwarded to the jurisdiction of 0/o .The Commissioner of Customs, NS-III, JNGI I, Nhava Sheva for comments on 22.12.2025, 08.01.2026 and 28.01.2026. •

7.1 The said jurisdictional authority vide letter dated 30.01.2026 forwarded comments in the said matter and submitted that the issue relating to alleged evasion of Agriculture Infrastructure and Development Cess (AIDC) on the goods imported by M/s Metro Brands Limited is presently under investigation by the Directorate of Revenue Intelligence (DRI), Lucknow. They further submitted that in terms of Section 28-l(2)(a) of the .Customs Act, 1962, the Authority shall not allow an application where the question raised therein is already pending in the applicant’s case before any officer of customs, the Appellate Tribunal, or any court i.e. any case pending with any officer of customs has been specifically excluded from the scope of advance ruling in terms of Section 281 clause (a) to 1st proviso.

7.2 In view of the change in the CHAR Authority, a personal hearing (PI I) was held again on 03.06.2026 at 11:30 AM, in accordance with the principles of natural justice. The authorized representative of the applicant attended the PH in the matter and reiterated the arguments mentioned in the written submissions. He submitted copies of few Bills of Entry stating the that Customs is not objecting to their claim of AIDC exemption. They also produced Customs, JNPT letter w.r.t earlier issue of AIDC payment & liability which emanated, from wrong filing of the AIDC entry Sr. No.

8. Details of Personal Hearing:

Shri Rahul Shukla and Ms. Surbhi. both authorised representatives appeared for PH in the matter on behalf of the applicant. They reiterated the contention filed with the application that the importer Metro Brands imparts various categories of Footwear under CTII 6402,6403 and 6404 from different countries. It was submitted that from 02.02.2025 BCD is reduced from 35%.to 20% ; SWS is exempted and AIDC is levied @18.5%. Although despite the reduction in BCD and elimination of SWS, there is no changes in effective rate of customs duty on import of Footwear. As per Notification No. 11/2021 dated 01.02.2021; Sr. NO. 14A with effect 02.02.2025 covering all goods of CTI-I 6401 to 6405; 18.5% AIDC was chargeable but as per Sr. No. 19 of the same Notification all goods of any chapter on which I3CD is exempted in the Notifications Annexed to the “Annexure” to the AIDC exemption Notification attract NIL AIDC. Sr. No.”4″ and .“9” of the Annexure of the Notification pertains to the applicant case which represent Notification 46/2011 dated 01.06.2011 and Notification 99/2011 dated 06.11.2011. As their import goods (from Vietnam and Bangladesh) are exempted from payment of BCD; No AIDC ‘is applicable. In support of their claim they also rely upon JS(TRU) letter dated 01.02.2021 which at Clause (4) 61Annex ‘C’ classifies that goods imported under customs duty exemption available under VIA and LOU as well as under Advance Authorisation Scheme are being exempted from AIDC.

Nobody appeared from the department side for PH.

DISCUSSION AND FINDINGS

9. I have carefully considered the application filed by M/s Metro Brands Limited, the submissions made in the application and during the course of personal hearing, as well as the comments furnished by the jurisdictional Commissionerate. The issue raised in the present application pertains to the eligibility of exemption from Agriculture Infrastructure and Development Cess (AIDC) under Serial No. 19 of Notification No. 11/2021-Customs dated 01.02.2021, as amended, in respect of imports made under Free Trade Agreement (FTA) notifications where concessional rates of Basic Customs Duty (BCD) are claimed and allowed.

10. Admissibility of the Application under Section 281 of the Customs Act, 1962

10.1 At the outset, it is necessary to examine the admissibility of the present application in terms of Section 281 of the Customs Act, 1962. The jurisdictional Commissionerate has contended that the issue relating ‘to alleged non-payment of AIDC is presently under investigation by the Directorate of Revenue Intelligence (DRI), and therefore, the application ought not to be entertained.

10.2 In this regard, reference is made to the provisions of Section 281(2) of the Customs Act, 1962, which reads as under:

“The Authority may, after examining the application and the records called /or, by order, either allow or reject the application:

Provided that the Authority shall not allow the application where the question raised in the application is-

(a) already pending in the applicant’s case before any officer of customs, the Appellate Tribunal or any Court; or

(b) the same as in a matter already decided by the Appellate Tribunal or any Court.”

10.3 A plain reading of the above provision makes it clear that an application is liable to be rejected in the cases where the question raised is already pending before any officer of Customs the Appellate Tribunal or any Court, or where the same issue has already been decided by a judicial forum. The expression “pending” necessarily implies the existence of a formally instituted proceeding wherein the issue has been specifically raised for determination.

10.4 From the facts placed on record, it is observed that the following actions are pending before the Department in relation to the applicant’s imports:

- A Query letter has been issued in respect of a specific Bill of Entry alleging non-payment of AlDC; however; no consultative letter or show cause notice has been issued in the said ‘matter.

- A Consultative letter has been issued by the Customs (Audit), JNCI I Commissionerate alleging short payment of AIDC due to incorrect availment under Serial No. 17 instead of Serial No.14A of Notification No. 11/2021-Customs. It is noted that the said issue pertains to the correctness of the exemption entry claimed in a particular transaction and is factually distinguishable from the broader legal question raised in the present application re aiding general eligibility to NIL AJDC under Serial 19.

- Representations and correspondence have been made by the applicant before audit and assessing authorities regarding the applicability of AIDC. Such representations, being in the nature of replies or voluntary submissions. do not constitute proceedings wherein an issue is pending for adjudication

- The Directorate of Revenue Intelligence (DRI), Lucknow has sought information and documents relating to imports made from February 2025 onwards. The said action is in the nature of investigation and. fact-finding.

10.5 From the above, it is evident that no Consultative letter or Show cause notice has been issued by any officer of Customs, nor has any adjudication proceeding been initiated before any authority, Tribunal, or Court on the question raised in the present application. The actions undertaken by the Department are limited to preliminary inquiry, audit verification, and investigation.

10.6 In this context, the reliance placed by the applicant on judicial precedent is apposite. In DRI vs. M/s Spray-Tec India Ltd., the Hon’ble High Court has categorically held that mere investigation or departmental inquiry does not render a question as “pending” for the purposes of bar on advance ruling. It was clarified that pendency can be said to arise only when the issue is formally articulated in a notice—such as a pre-consultation notice or show cause notice—thereby enabling the assessee to respond and contest the same. The Court further observed that a question attains the status of “pending” only when it stands crystallised into a proceeding capable of adjudication, and not merely when it is under contemplation by–the Department.

10.7 Further, in Re: HQ Lamps Manufacturing Co. Pvt. Ltd, the Authority for Advance Rulings has clarified that the bar under Section 281 is .attracted only in situations where formal proceedings have been initiated, such as issuance of a show cause notice, provisional assessment, or commencement of pre-notice consultation(CL). It was specifically observed that general correspondence, audit scrutiny, or information gathering would not amount to pendency of a question.

10.8 Applying the above legal position to the present facts, it is evident that the actions relied upon by the Department regarding pending DRI investigation do not amount to “pendency” within the meaning of Section 28I(2), in the absence of a formally instituted proceeding requiring adjudication.

10.9 Accordingly, I find that the objection raised by the jurisdictional Commissionerate on the ground of ongoing investigation is not sustainable in law. In the absence of any formal proceedings wherein the question raised in the present application is pending for determination, the statutory bar under Section 28I(2) is not attracted. Therefore, I proceed to examine the question raised in the application on merit:

11. Eligibility for Exemption from AIDC under Serial No. 19 of Notification No. 11/2021-Customs dated 01.02.2021

11.1 The precise issue that arises for determination in the present application is:

“Whether the benefit of NIL rate of Agriculture Infrastructure and Development Cess (AIDC) under Serial No. 19 of Notification No. 11/2021-Customs dated 01.02.2021 is available in respect of goods imported under Free Trade Agreement (FTA) notifications specified in the Annexure thereto, in cases where the importer claims and is allowed a concessional (including partial) rate of Basic Customs Duty (BCD) under such notifications.”

11.2 Statutory Scheme Governing Levy and Exemption of AIDC:

11.2.1 Agriculture Infrastructure and Development Cess (AIDC) is levied under Section 124 of the Finance Act, 2021 as a duty of customs on imported goods. This levy is in addition to other duties of customs chargeable under the Customs Act, 1962 and the Customs Tariff Act, 1975.

11.2.2 The Central Government, in exercise of the powers conferred under Section 25(1) of the Customs Act, 1962, read with Section 124 of the Finance Act, 2021, has issued Notification No. 11/2021-Customs dated 01.02.2021 (as amended), granting exemption from AIDC in specified circumstances.

11.2.3 It is pertinent to note that Section 25(1), being the parent provision, empowers the Government to exempt goods from the “whole or any part” of the duty of customs. This statutory formulation is of fundamental significance in interpreting the scope and extent of exemptions granted under notifications issued thereunder.

11.3 Relevant Entries of Notification No. 11/2021-Customs

The Applicant is engaged in importing under various categories of footwear falling under FISN 6402, 6403 and 6404. The Applicant is engaged in the import of footwear falling under I ISN 6402, 6403 and 6404 from Vietnam, Bangladesh, Brazil and Cambodia.

11.3.1. The relevant entries of Notification No.. 11/2021-Customs are reproduced -below: “In exercise of the powers conferred by sub-section (I) of section 25 of the Customs Act, 1962 (52 of 1962) read with 4 [section 124 of the Finance Act, 2021 (13 of 2021)1, the Central Government, on being satisfied that it is necessary in the public interest so to do, hereby exempts goods of the description specified in column (3) of the Table below and ‘idling within the Chapter, heading or sub-heading or tariff item of the First Schedule to the Customs TariffAct, 1975 (51 of 1975) as specified in column (2) of the said Table, from so much of the Agriculture Infrastructure and Development Cess leviable thereon under the 5[said section of the Finance Act, 2021 (13 of 2021)J, as is in excess of the amount calculated at the rate specified in column (4) of the said Table.

| Sl. No. | Chapter or heading or subheading or tariff item of the First Schedule | Description of goods | Rate |

| 14A | 6401, 6402, 6403, 6404 or 6405 | All goods | 18.5% |

| 19 | Any Chapter | All goods on which exemption from basic customs duty is claimed and allowed under the notifications published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), mentioned in the ANNEXURE. | NIL |

11.3.2 A conjoint reading of the above entries indicates that Footwear falling under CTI 16402, 6403 and 6404, as imported by the applicant, is ordinarily liable to Agriculture Infrastructure and Development Cess (AIDC) at the rate of 18.5% in terms of Serial No. 14A of the said notification. however, Serial No. 19 provides for a specific exemption mechanism whereby such goods become eligible for a NIL rate of AIDC, provided that exemption from Basic Customs Duty (BCD) is claimed and allowed under the specified notifications listed in the Annexure, subject to fulfillment of the prescribed conditions.

11.4 Coverage of Applicant’s Imports under Annexure to the AIDC Notification Relevant Entries in the Annexure to the Notification

11.4.1 The Annexure to Notification No. 11/2021-Customs specifies certain notifications under which, if BCD exemption is claimed and allowed, the benefit of NIL AIDC becomes available.

11.4.2 The relevant entries in the Annexure to the AMC Notification, as applicable to the present case, are as follows:

ANNEXURE –

| S.No. – | Details of the Notifications |

| 4. | Notification No. 46/2011-Customs, dated the 1st June, 2011 vide number. G.S.R.423(E), dated the 1st June, 2011. |

| 9. | Notification No. 99/2011-Customs,, dated the 9th November: 2011 vide number G.S.R. 801(E), dated the 9th November, 2011 |

11.5 Examination of the Factual Matrix and Applicable Tariff Entries

From the facts placed on record, it is observed that:

- The applicant imports footwear falling under CTH 6402, 6403 and 6404 from Vietnam and Bangladesh.

- In respect of the above classifications, Serial Nos. 903 to 910 of Notification No. 46/2011-Customs (AIFTA) specifically provide for complete as well as partial exemption from payment of I3asic Customs Duty (BCD) for goods falling under tariff headings 6402 to 6404. The relevant portion of the notification is reproduced below:

| Sr. No. | Chapter Heading / Tariff Item | Description | Rate (%) |

| 903 | 640110 to 640212 | All goods | 5% |

| 904 | 640220 to 640299 | All goods | 5% |

| 905 | 640312 | All goods | NIL |

| 906 | 640319 to 640391 | All goods (other than specified footwear) | 5% |

| 907 | 64039190 | Specified footwear | NIL |

| 908 | 640399 | All goods (other than specified footwear) | 5% |

| 909 | 64039990 | Specified footwear | NIL |

| 910 | 6404 | All goods | 5% |

- Thus, under the AIFTA notification, the applicable rate of I3CD ranges from NIL to 5%, depending upon the specific tariff classification of the imported footwear.

- Similarly, preferential duty benefit under SAF’I’A is extended vide Notification No. 99/2011-Customs dated 09.11.2011, issued under Section 25(1) of the Customs Act, 1962. The said notification provides that all goods, other than those specified in the Annexure thereto (i.e., goods falling under tariff items 2203 to 2206, 220710, 2208 and Chapter 24), when imported into India from countries listed in the Appendix (including the People’s Republic of Bangladesh), are exempt from the whole of the Basic Customs Duty leviable thereon.

- Accordingly, goods imported from Bangladesh, being covered under the said notification and not falling within the excluded categories, are eligible for full exemption from BCD.

11.6 Conclusion

Thus, it is evident that the subject goods imported by the applicant are clearly covered under the relevant Free Trade Agreement (FTA) notifications listed in the Annexure, namely Notification No. 46/2011-Customs (AIFTA) and Notification No: 99/2011-Customs (SAFTA), read with the, applicable serial numbers (903 to 910) in respect of footwear falling under CTI I 6402 to 6404.

Accordingly, the applicant is eligible for exemption from Basic Customs Duty (either lull or concessional, as applicable), subject to:

- production of a Valid Certificate of Origin (Cob);

- fulfilment of all conditions prescribed under the respective FTA notifications; and

- compliance with the provisions of the Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR, 2020),

to the satisfaction of the proper officer at the time of importation.

12. Interpretation of the Expression “Exemption from BCD is Claimed and Allowed”

12.1 The issue that requires consideration is the correct interpretation of the expression “exemption from basic customs duty is claimed and allowed” appearing in Serial No. 19 of the relevant notification. The question that arises is whether such exemption must necessarily result in a NIL rate of BCD, or whether it would also encompass cases where BCD is reduced to a concessional rate.

12.2 Statutory Meaning of “Exemption” under Section 25 of the Customs Act, 1962

12.2.1 Section 25(1) of the Customs Act, 1962, being the enabling provision for grant of exemption, is reproduced below:

“If the Central Government is satisfied that it is necessary in the public interest so to do,. it may, by notification in the Official Gazette, exempt generally either absolutely or subject to such conditions (to be fulfilled before or after clearance) as maybe specified in the notification goods of any specified description from the whole or any part of duty of customs leviable thereon.”

12.2.2 A plain reading of the above provision makes it abundantly clear that exemption is not confined to total waiver of duty, but extends to situations where duty is reduced in part.

12.2.3 In effect, the statute recognizes two forms of exemption:

(i) Absolute exemption, where the duty is entirely waived (i.e., NIL rate); and

(ii) Conditional or partial exemption, where the duty is reduced, wholly or in part, subject to prescribed conditions.

12.2.4 Thus, the statutory framework unequivocally establishes that exemption from duty includes both inn exemption and partial (concessional) exemption; without drawing any distinction in their legal character. The phrase “whole or any part of duty” used in Section 25(1) clearly’ reinforces this position.

13. Application of the Above Principle to Serial No. 19 of Notification No. 11/2021-Customs

13.1 The description of goods specified at Serial No. 19 of the relevant notification reads as follows:

“All goods on which exemption from basic customs duty is claimed and allowed under the notifications, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), mentioned in the ANNEXURE..”

13.2 A plain reading of the above description indicates that the scope of the entry is broadly worded and covers all goods in respect of which exemption from Basic Customs Duty (13CD) is both claimed by the importer and allowed by the proper officer under any of the notifications specified in the Annexure.

13.3 A careful reading of the above entry indicates that the expression “exemption from basic customs duty is claimed and allowed” has been used in a bread and unqualified manner, without incorporating any words of limitation. The provision does not prescribe that the exemption must necessarily result in a NIL rate of BCD, nor does it draw any distinction between complete exemption and concessional or partial exemption. Further, there is no stipulation regarding .any minimum extent or threshold of exemption that must be achieved for the benefit to apply.

13.4 In the absence of any such restrictive language, the expression “exemption from BCD” must be interpreted in its statutory sense, as understood under Section 25(1) of the Customs Act, 1962, which expressly provides for exemption from ‘the whole or any part” of the duty of customs. The legal position, therefore, is that exemption–encompasses both full and partial relief from duty. Any interpretation restricting Serial No. 19 only to cases where BCD is reduced to NIL would amount to reading into the notification a limitation not borne out from its text, which is impermissible in law.

13.5 Accordingly, it is held that the expression “exemption from BCD” appearing in Serial No. 19 includes both complete exemption as well as partial or concessional exemption, and is applicable in all cases where duty relief is granted under a notification issued under Section 25 of the Customs Act.

14. Satisfaction of Conditions Prescribed under Serial No. 19

14.1 Serial No. 19 operates upon the fulfilment of two essential conditions, namely that the importer must claim exemption from BCD under a notification specified in the Annexure, and that such exemption must be allowed by the proper officer. In the present case, it is observed that the applicant imports the subject goods under Notification No. 46/2011-Customs dated 01.06.2011 (AIFTA) and Notification No. 99/2011-Customs dated 09.11.2011 (SAFTA), which are specifically covered under SI. Nos. 4 and 9 of the Annexure to Notification No. 11/2021-Customs,

14.2 The subject goods, namely footwear falling under CTI-1,6402, 6403 and 6404, are covered under the aforesaid notifications. Under Notification No. 46/201 I -Customs, the relevant tariff entries (Sr. Nos. 903 to 910) provide for concessional as well as NIL rates of 13CD depending upon the specific classification of goods. Similarly, Notification No. 99/2011-Customs grants exemption from the whole of BCD to eligible goods imported from Bangladesh, except, for certain excluded items, which do not cover the subject goods.

14.3 It is further noted that the availment of such exemption is subject to production of a valid Certificate of Origin (COO) and fulfilment of all prescribed conditions under the respective FTA notifications, including compliance with the Rules of Origin under CAROTAR, 2020, to the satisfaction of the proper officer at the time of import. Upon such verification, the applicable BCI), whether concessional or NIL, is duly allowed by the proper officer.

14.4 In view of the above, it is evident that the requirement of “exemption from BCD being claimed and allowed” stands fully satisfied in the present case. The applicability of Serial No. 19 is not dependent upon the exemption resulting in a NIL rate of BCI) alone, but extends equally to cases where concessional rates arc applied. Consequently, the benefit of NIL AIDC under Serial No. 19 is attracted once the prescribed conditions are fulfilled.

15. Legislative Intent and Policy Context

15.1 The Applicant has placed reliance upon Annexure C to the Union Budget, 2021 in support of the interpretation adopted above. The said Annexure constitutes a contemporaneous exposition of legislative intent and clearly elucidates the policy rationale underlying the introduction of the Agriculture Infrastructure and Development Cess (AIDC). It indicates that AIDC was introduced as part of a calibrated customs duty rationalisation exercise, wherein corresponding reductions in Basic Customs Duty (I3CD1were effected so as to preserve the overall duty incidence and maintain revenue neutrality. Crucially, the Annexure further clarifies that imports availing benefits under Free Trade Agreements (FTAs), Export Oriented Unit (EOU) schemes, and Advance Authorisation schemes were consciously kept outside the ambit of AIDC. This evidences a clear legislative intent that AIDC was not meant to burden imports already enjoying concessional or preferential treatment under exemption notifications issued under Section 25 of the Customs Act, 1962.

15.2 In this regard, the relevant extract of Paragraph 4 of Annexure C is reproduced below for ready reference:

“These changes would become effective on 02.02.2021, 00:00 hours owing to the declaration made under Provisional Collection of Taxes Act, 1931.

I. Customs:

(1) An Agriculture Infrastructure and Development Cess (AIDC), as duty of customs, has been proposed [Clause 115 of the Finance Bill, 2021 refers]. Enabling provisions has been made for levy of this cess on all imported goods at the rate not exceeding the rate specified in the First Schedule to the Customs Tariff Act, 1975. However, it would be levied only on specified goods as detailed below. All other items are being exempted from this Cess…’…………………

(4) Further, goods imported under customs duty exemptions available under FTA and EOU as well as under advance authorization schemes are being exempted from AIDC”

15.3 Although budgetary documents do not override or control the express language of statutory provisions, it is a settled principle of interpretation that such contemporaneous policy documents constitute a valuable external aid in discerning legislative intent. The above extract lends strong support to a purposive construction of the relevant exemption notification; particularly Serial No. 19 thereof, by affirming that AIDC exemption is intended to extend to imports availing 11’A-based BCD concessions, irrespective of whether such exemption is absolute or partial.

16. Absence of Restrictive Provision:

6.1 It is significant that Notification No.- 11/2021-Customs does not contain any provision restricting the simultaneous availment of concessional Basic Customs Duty (BCD) under Free Trade Agreements (PTAs) and exemption from AIDC under Serial No. 19.

16.2 It is a settled principle. that where the legislature intends to impose conditions or restrictions on the availment of exemptions, it does so through clear and express terms in the notification itself.

16.3 In the present case, the absence of any such restrictive provision clearly indicates that no limitation was intended on the concurrent availment of ETA-based BCD concession and AIDC exemption.

17. To sum up:

17.1 In view of the foregoing discussion and findings, it is concluded that the present application is admissible under Section 281 of the Customs Act, 1962, as no formal proceedings on the question raised are pending before any adjudicating authority, Tribunal, or Court.

17.2 On merits, it is established that the expression “exemption from Basic Customs Duty (BCD) is claimed and allowed” appearing in Serial No. 19 of Notification No. 11/2021-Customs is to be interpreted in its statutory sense under Section 25(1) of the Customs Act, 1962, which encompasses both full (NIL) and partial (concessional) exemptions.

17.3 The subject goods imported by the applicant under the relevant Free Trade Agreement (ETA) notifications, namely Notification No. 46/2011-Customs (AIFTA) and Notification No. 99/2011-Customs (SAFTA), are covered under the Annexure to the said notification. The condition of “exemption from BCD being claimed and allowed” thus stands satisfied, subject to compliance with prescribed conditions, including production of a valid Certificate of Origin and adherence to CAROTAR, 2020, to the satisfaction of the proper officer.

17.4 Accordingly, the benefit of NiL rate of AIDC under Serial No. 19 is available even where BCD is levied at a concessional (partial) rate under FTA notifications, and is not confined solely to cases of absolute exemption.

17.5 This interpretation is further supported by the legislative intent reflected in Annexure C to the Union Budget, 2021, as well as by the absence of any restrictive provision in the notification, thereby affirming that AIDC exemption extends to imports availing FTA-based BCI) concessions.

18. On the basis of the facts and circumstances of the case, the foregoing discussions and observations, I reach the following conclusions:

18.1 The applicant is eligible for exemption and NIL rate of Agriculture Infrastructure and Development Cess (AIDC) under Serial No. 19 of Notification No. 11/2021-Customs dated 01.02.2021 in respect of goods imported under Free Trade Agreement notifications, namely Notification No. 46/2011-Customs and Notification No. 99/2011-Customs, covering imports under ASEAN and SAFTA arrangements, subject to satisfaction of the prescribed conditions under the respective notifications to the satisfaction of the proper officer at the time of actual import.

I rule accordingly.

Author Bio