Case Law Details

Kamlesh Pramod Gandhi Vs ITO (ITAT Pune)

Pune ITAT Quashes Reassessment for Failure to Issue Mandatory Notice under Section 143(2) Despite Return Filed in Response to Section 148

Summary: The ITAT Pune held that a reassessment completed without issuing a mandatory notice under Section 143(2) of the Income-tax Act, 1961 after the assessee filed a return in response to a notice under Section 148 was invalid. The Tribunal found that although the Assessing Officer and CIT(A)/NFAC treated the return as invalid, the record showed that it had been e-verified and therefore could not be regarded as invalid. Since the return filed pursuant to Section 148 was valid, issuance of notice under Section 143(2) was mandatory even if the return was filed belatedly. Relying on earlier judicial precedents and its coordinate bench decisions, the Tribunal held that non-issuance of notice under Section 143(2) constituted a jurisdictional defect rendering the reassessment proceedings a nullity. Accordingly, it set aside the order of the CIT(A)/NFAC, held the reassessment invalid, and allowed the assessee’s appeal. As the appeal succeeded on the legal issue, the Tribunal did not adjudicate the grounds challenging the additions on merits.

The Pune Bench of the Income Tax Appellate Tribunal held that issuance of a notice under section 143(2) is mandatory where an assessee files a return in response to a notice under section 148, even if such return is filed belatedly. Since the Assessing Officer completed the reassessment without issuing the mandatory notice under section 143(2), the Tribunal declared the reassessment invalid in law and quashed the assessment.

The assessee’s case was reopened on the basis of information regarding cash deposits of ₹30.70 lakh in a bank account. In response to the notice under section 148, the assessee filed a return declaring a lower income and explained that the cash deposits represented business receipts from the sale of automobile spare parts. The Assessing Officer, however, rejected the explanation for want of supporting evidence and added the entire cash deposits as unexplained income besides making another addition on account of reduction in returned income.

Before the CIT(A), the assessee specifically challenged the reassessment on the ground that no notice under section 143(2) had been issued after filing the return in response to section 148. The CIT(A) rejected the contention by holding that the return was treated as invalid by the system, and therefore issuance of notice under section 143(2) was unnecessary.

The Tribunal found this reasoning to be factually incorrect. Examining the material placed on record, including the screenshot from the income-tax portal, it noted that the return had in fact been successfully e-verified and was reflected on the portal as a valid return filed in response to section 148. The Tribunal also observed that the Assessing Officer himself had computed the reassessed income by taking the income declared in that return as the starting point, thereby treating it as a valid return for assessment purposes.

Relying on its earlier decisions in Bharat Kantilal Chengede and Bababhai Sadarbhai Shaikh, as well as the judgments of the Patna High Court in CIT v. Nagendra Prasad, the Delhi High Court in PCIT v. Draft Infrabuild (P.) Ltd., and other judicial precedents, the Tribunal reiterated that non-issuance of notice under section 143(2) after receipt of a return in response to section 148 is a jurisdictional defect, which renders the reassessment proceedings void. The Tribunal further held that this mandatory requirement cannot be dispensed with merely because the return was filed beyond the time stipulated in the notice under section 148.

Accordingly, the Tribunal held that the reassessment order suffered from a fatal jurisdictional defect, set aside the orders of the lower authorities, and quashed the reassessment itself. Having allowed the appeal on the legal issue, the Tribunal did not consider the additions on merits.

Author’s Comments:

This ruling further strengthens the growing line of judicial precedents holding that issuance of notice under section 143(2) is an indispensable jurisdictional requirement in reassessment proceedings whenever a return is filed in response to section 148. The Tribunal has also made an important factual observation that where the Income-tax portal reflects a return as successfully e-verified, the Revenue cannot subsequently contend that it was an invalid return merely to justify the omission of issuing a notice under section 143(2). The decision is likely to be of considerable significance in reassessment cases where the Department seeks to sustain assessments despite non-compliance with this mandatory procedural safeguard.

Cases Discussed

- Kamlesh Pramod Gandhi Vs ITO (ITAT Pune)

- Bharat Kantilal Chengede vs. ITO, ITA No. 1902/PUN/2025, order dated 13.01.2026, Assessment Year 2012-13.

- Bababhai Sadarbhai Shaikh vs. ITO, ITA No. 144/PUN/2025, order dated 23.10.2025, Assessment Year 2015-16.

- CIT vs. Nagendra Prasad, (2023) 156 com19 (Patna).

- Chand Bihari Agrawal v. Commissioner of Income Tax, Central, Patna, M.A. No. 239 of 2011, decided on 25-7-2023.

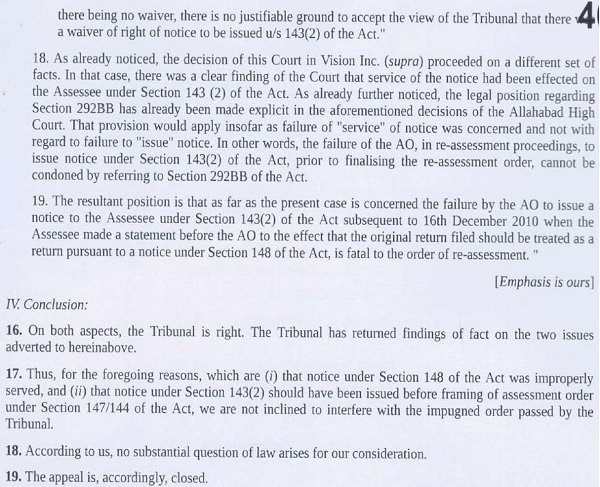

- PCIT vs. Draft Infrabuild (P.) Ltd.

- PCIT vs. Shri Jai Shiv Shankar Traders (P.) Ltd., [2015] 64 taxmann.com 220/383 ITR 448 (Delhi).

- DIT v. Society for Worldwide Interbank Financial Telecommunications, [2010] 323 ITR 249 (Delhi).

- CIT v. Rajeev Sharma, [2010] 192 Taxman 197/336 ITR 678 (Allahabad).

- CIT v. Salarpur Cold Storage (P.) Ltd., [2014] 50 taxmann.com 105/228 Taxman 48 (Allahabad).

- Hotel Blue Moon.

- Sapthagiri Finance & Investments v. ITO, [2012] 25 taxmann.com 341/210 Taxman 78 (Madras) (Mag.).

FULL TEXT OF THE ORDER OF ITAT PUNE

This appeal filed by the assessee is directed against the order dated 15.01.2026 of the Ld. CIT(A) / NFAC, Delhi relating to assessment year 2014-15.

2. Although a number of grounds have been raised by the assessee, however, the Ld. Counsel for the assessee confined his argument to only one issue i.e. the validity of the re-assessment order in absence of issue of notice u/s 143(2) of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’).

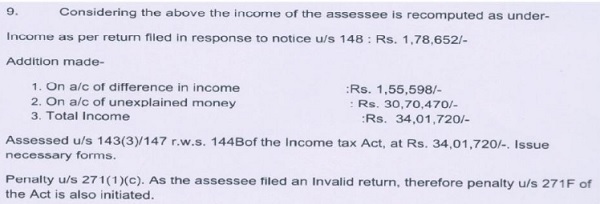

3. Facts of the case, in brief, are that the assessee filed his return of income on 12.02.2015 declaring total income of Rs.3,34,250/-. Information was received by the department regarding substantial cash deposit of Rs.30,70,470/- in the bank account maintained with Shri Renukamata Multi State Urban Co-operative Society Limited. Based on such information the Assessing Officer formed reason to believe that the income chargeable to tax has escaped assessment. Accordingly, he issued a notice u/s 148 of the Act on 31.03.2021 in response to which the assessee filed his return of income on 27.01.2022 declaring total income of Rs.1,78,652/-after claiming deduction of Rs.75,012/- under Chapter VI-A. This return was treated as invalid by the CPC. The Assessing Officer noted that the assessee in the return filed in response to the notice issued u/s 148 of the Act has reduced his income. He specifically asked the assessee to explain the reason for reducing his income. However, no explanation was furnished by the assessee. In absence of any satisfactory explanation and material available on record, the Assessing Officer added the difference amount of Rs.1,55,598/- as unexplained income.

4. The Assessing Officer further noted that there are certain cash deposits made by the assessee in his bank account. He, therefore, asked the assessee to explain the same. The assessee in response to the same submitted that he is engaged in the business of automobile spare parts under the name and style of M/s. Gandhi Tempo and the cash so deposited was out of cash sales made over the counter. Apart from this he also used to send spare parts by transport to different buyers at the given address and after receiving the goods buyers deposit the cash in his account. It was submitted that sometimes he used to collect the sale value in advance and thereafter send the goods. The deposits are received in bank through RTGS and cheques transfer and cash deposited by the buyers from their home town in his bank account. The assessee also submitted the bank statement and other related documents / details. However, in absence of any supporting documents, the Assessing Officer rejected the explanation given by the assessee and made addition of the entire amount of cash deposited of Rs.30,70,470/- to the total income of the assessee. The Assessing Officer accordingly determined the total income of the assessee at Rs.34,01,720/-.

5. Before the Ld. CIT(A) / NFAC, the assessee apart from challenging the addition on merit, challenged the validity of the re-assessment order in absence of notice issued u/s 143(2) of the Act. However, the Ld. CIT(A) / NFAC dismissed both the grounds.

6. So far as the validity of the order in absence of issue of notice u/s 143(2) is concerned, he held that the return in response to the notice u/s 148 has been treated as invalid return by the system. Therefore, once the return itself is treated as invalid, the Assessing Officer was justified in proceeding with the re-assessment by issuing notice u/s 142(1) of the Act. He held that the issuance of notice u/s 143(2) pre-supposes a valid return which was absent in the present case. Therefore, non-issue of notice u/s 143(2) of the Act does not vitiate the re-assessment proceedings.

7. So far as the merit of the case is concerned, he held that the assessee was unable to discharge the burden cast on him. The assessee in the instant case failed to produce the primary evidences such as sale bills, vouchers, stock registers or VAT returns to substantiate the sales corresponding to the specific dates and amounts of the cash deposits. Without a verifiable trail linking the cash deposits to specific commercial transactions, the claim of business sales remains a bald assertion. He accordingly upheld the addition on merit also.

8. Aggrieved with such order of the Ld. CIT(A) / NFAC the assessee is in appeal before the Tribunal.

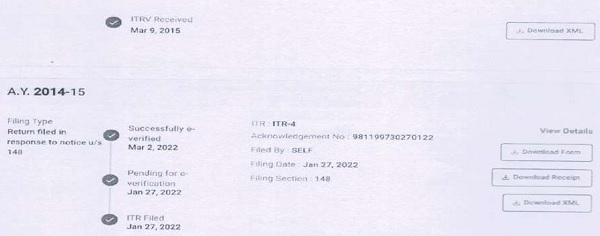

9. The Ld. Counsel for the assessee at the outset submitted that the assessee in response to the notice u/s 148 of the Act dated 31.03.2021 filed its return of income on 27.01.2022 which was subsequently e-verified on 02.03.2022 which is evident from the screenshot of the return filed on income tax portal, copy of which is placed at pages 5 to 8 of the paper book. Therefore, the finding of the Ld. CIT(A) / NFAC that the return was treated as invalid by the system is incorrect. He submitted that a return which has been e-verified and is appearing as filed return on the income tax portal cannot be characterized as invalid return. He submitted that it is an undisputed fact that no notice u/s 143(2) of the Act was ever issued by the Assessing Officer after filing of the return in response to the notice u/s 148 of the Act. He has only issued notice u/s 142(1) of the Act. Relying on the decision of the Hon’ble Patna High Court in the case of CIT vs. Nagendra Prasad reported in (2023) 156 com19 (Patna), he submitted that the Hon’ble High Court in the said decision has held that where notice was issued by the Assessing Officer under section 148 requiring the assessee to file a return within thirty days but return was filed after eight and a half months, since return was filed by the assessee in response to the said notice though delayed, there should have been a notice issued under section 143(2) as requirement to issue notice could not be dispensed with.

10. Referring to the decision of the Co-ordinate Bench of the Tribunal in the case of Bababhai Sadarbhai Shaikh vs. ITO vide ITA No. 144/PUN/2025 order dated 23.10.2025 for assessment year 2015-16, he submitted that in that case also notice u/s 148 of the Act was issued on 31.03.2021 and the assessee vide letter dated 14.03.2022 requested the Assessing Officer to consider the original return as return filed in response to notice u/s 148. Since no notice u/s 143(2) of the Act was issued, the Tribunal, following the decision of the Hon’ble Patna High Court in the case of CIT vs. Nagendra Prasad (supra), held that there should have been a notice issued u/s 143(2) which is a requirement and which cannot be dispensed with.

11. Referring to the decision of the Co-ordinate Bench of the Tribunal in the case of Bharat Kantilal Chengede vs. ITO vide ITA No.1902/PUN/2025 order dated 13.01.2026 for assessment year 2012-13, he submitted that in that case also notice u/s 148 was issued on 25.03.2019 and the assessee filed his return in response to the said notice on 11.12.2019 which is after the statutory period of 30 days given by the Assessing Officer. The notice u/s 143(2) was not issued and the assessment order was passed on 20.12.2019. When the assessee challenged the assessment in absence of notice u/s 143(2), the Tribunal, following various decisions held that the failure by the Assessing Officer to issue notice to the assessee u/s 143(2) after the assessee filed his return in response to the notice u/s 148 is fatal to the order of re-assessment. Relying on various other decisions, he submitted that since admittedly the Assessing Officer has not issued notice u/s 143(2) after the assessee filed return in response to the notice u/s 148, though, belatedly, such assessment order is invalid being not in accordance with law.

12. The Ld. DR on the other hand submitted that the assessment record and assessment order clearly indicate that the return filed in response to the notice u/s 148 was not accepted by the system as a valid return and was reflected as an invalid return. The Assessing Officer has specified this fact in the assessment order. Therefore, there is no requirement of issue of notice u/s 143(2).

13. So far as the contention of the assessee that the return subsequently stood e-verified on 02.03.2022 is concerned, he submitted that the matter requirs verification from the assessment record. He submitted that mere production of a screenshot at the appellate stage cannot automatically displace the contemporaneous record relied upon by the Assessing Officer while framing the assessment. He submitted that this screenshot or the fact that the return subsequently stood e-verified was not on the record of the file of the Ld. DR.

14. So far as the various decisions relied on by the Ld. Counsel for the assessee are concerned, he submitted that these decisions are distinguishable and not applicable to the facts of the present case. In all these cases, there existed a valid return on record and the Hon’ble Courts found complete absence of notice u/s 143(2) despite such valid return. However, in the present case, the assessment order itself records that the return filed in response to notice u/s 148 was treated as invalid by the system and the re-assessment proceedings were continued through statutory notices u/s 142(1).

15. Without prejudice to the above, the Ld. DR submitted that the matter may be restored to the file of the Assessing Officer for examination of the assessment records and portal records regarding the exact status, date of validation and processing of the return purportedly filed in response to the notice u/s 148 of the Act. Further, the assessee has not challenged the validity of reopening on merits before the Tribunal. He submitted that the reopening was based on specific information relating to substantial cash deposits and therefore, re-assessment proceedings were initiated on a valid foundation. He accordingly submitted that the order of the Ld. CIT(A) / NFAC be upheld and the grounds raised by the assessee be dismissed.

16. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and the Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. The only issue to be decided in the instant appeal is regarding the validity of assessment in absence of issue of notice u/s 143(2) of the Act. It is an admitted fact that the Assessing Officer in the instant case issued notice u/s 148 on 31.03.2021. It is also an admitted fact that the assessee filed its return of income in response to the notice u/s 148 of the Act on 27.01.2022. It is also an admitted fact that no notice u/s 143(2) was issued to the assessee. It is also an admitted fact that the Assessing Officer passed the order on 25.03.2022 u/s 147 r.w.s. 144B of the Act. Under these circumstances, we have to see as to whether the assessment order can be held as null and void in absence of any notice u/s 143(2).

17. It is the submission of the Ld. DR that since the return was treated as invalid by the system, therefore, there was no valid return filed and therefore, there was no requirement of issuing any notice u/s 143(2). However, a perusal of the assessment order shows that the Assessing Officer has proceeded to compute the income on the basis of the return filed in response to the notice u/s 148 by observing as under:

18. A perusal of the paper book shows that the return filed by the assessee has been e-verified by the system and the same reads as under:

19. Once the system shows that the return has been e-verified, therefore, merely because the Assessing Officer mentions in the order that the return was treated as invalid return by the system, the same in our opinion cannot be accepted. We, therefore, hold that the return filed by the assessee is not an invalid return.

20. Once the return is treated as a valid return, the next question that arises for our consideration is as to whether the assessment order can be held as valid in absence of any notice issued u/s 143(2) when the assessee files the return in response to the notice u/s 148, though, belatedly.

21. We find an identical issue had come up before the Co-ordinate Bench of the Tribunal in the case of Bharat Kantilal Chengede vs. ITO (supra). In that case, notice u/s 148 of the Act was issued to the assessee on 25.03.2019 and the assessee filed his return of income in response to the same on 11.12.2019 which was after the statutory period of 30 days given by the Assessing Officer. No notice u/s 143(2) of the Act was issued by the Assessing Officer before completion of the assessment. The Tribunal relying on various decision quashed the assessment order by observing as under:

“14. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and the Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the Assessing Officer in the instant case issued notice u/s 148 of the Act on 25.03.2019. We find the assessee in the instant case filed his return of income on 11.12.2019 which is after the statutory period of 30 days given by the Assessing Officer. It is also an admitted fact that the assessment order was passed on 20.12.2019 and no notice u/s 143(2) of the Act has been issued and served on the assessee before completion of the assessment. Under these circumstances, we have to see as to whether non-issue of notice u/s 143(2) of the Act renders the assessment proceedings invalid when the assessee filed the return in response to the notice issued u/s 148 of the Act belatedly.

15. We find an identical issue had come up before the Hon’ble Delhi High Court in the case of PCIT vs. Draft Infrabuild (P.) Ltd. (supra). We find the Hon’ble High Court, following its earlier order in the case of PCIT vs. Shri Jai Shiv Shankar Traders (P.) Ltd. (supra) and various other decisions, has held that the failure by the Assessing Officer to issue a notice to the assessee u/s 143(2) of the Act after the assessee files his return of income in response to the notice u/s 148 of the Act is fatal to the order of re-assessment proceedings. The relevant observations of Hon’ble High Court read as under:

15. This brings us to the second aspect of the matter, i.e., the consequences of the failure of the appellant/revenue to issue notice under Section 143(2) of the Act before framing the assessment order. Concededly, the appellant/revenue did not issue a notice under Section 143(2) of the Act, although it had on record the ROI filed by the respondent/assessee for the AY in issue, i.e., 2010-11. The return was, concededly, filed on 04.12.2015. This return was considered while framing the assessment under Section 147/144 of the Act. The only reason furnished for not issuing a notice under Section 143(2) of the Act is that the ROI was not filed within the thirty (30) days provided via the notice dated 30.03.2015 issued under Section 148. This argument does not impress us because if we were to hold [as we have], that the said notice was directed towards the wrong address, the respondent/assessee could have not adhered to the timeline provided in the said notice.

15.1 The respondent/assessee became aware of the Section 148 notice being issued after it received the notice dated 12.06.2015 under Section 142(1) of the Act. The fact that the respondent/assessee had filed an ROI on 04.12.2015 is not disputed. The fact that this ROI, as noticed above, was taken into account is also not in dispute. Therefore, in our opinion, before framing an assessment order, the AO ought to have issued a notice under Section 143(2) of the Act. The submission advanced on behalf of the appellant/revenue that, while it could consider the invalid return while framing the assessment order, it was not obliged to issue a notice under Section 143(2) of the Act because it was not filed within the timeframe given in the Section 148 notice is untenable in law, since the ROI, which was belated, was considered by the AO while carrying out the assessment.

15.2 The absence of notice, under Section 143(2), impregnates the proceedings with a jurisdictional defect and, hence, renders it invalid in the eyes of the law. This position is no longer res integra, as demonstrated by the observations made in Principal Commissioner of Income-tax v. Shri Jai Shiv Shankar Traders (P.) Ltd. [2015] 64 taxmann.com 220/383 ITR 448 (Delhi) :

“12. The narration of facts as noted above by the court makes it clear that no notice under section 143(2) of the Act was issued to the assessee after December 16,2010, the date on which the assessee informed the Assessing Officer that the return originally filed should be treated as the return filed pursuant to the notice under section 148 of the Act.

13. In DIT v. Society for Worldwide Interbank Financial Telecommunications [2010] 323 ITR 249 (Delhi), this court invalidated a reassessment proceeding after noting that the notice under section 143(2) of the Act was not issued to the assessee pursuant to the filing of the return. In other words, it was held mandatory to serve the notice under section 143(2) of the Act only after the return filed by the assessee is actually scrutinised by the Assessing Officer.

14. The interplay of sections 143 (2) and 148 of the Act formed the subject matter of at least two decisions of the Allahabad High Court in CIT v. Rajeev Sharma [2010] 192 Taxman 197/336 ITR 678 (Allahabad) it was held that a plain reading of section 148 of the Act reveals that within the statutory period specified therein, it shall be incumbent to send a notice under section 143(2) of the Act. It was observed (page 687):

“The provisions contained in sub-section (2) of section 143 of the Act is mandatory and the Legislature in its wisdom by using the word „reason to believe’ had cast a duly on the Assessing Officer to apply mind to the material on record and after being satisfied with regard to escaped liability, shall serve notice specifying particulars of such claim.

In view of the above, after receipt of return in response to notice under section 148, it shall be mandatory for the Assessing Officer to serve a notice under sub-section (2) of Section 143 assigning reason therein . . .

in absence of any notice issued under sub-section (2) of section 143 after receipt of fresh return submitted by the assessee in response to notice under section 148, the, entire procedure adopted for escaped assessment, shall not be valid.”

15. In a subsequent judgment in CIT v. Salarpur Cold Storage (P.) Ltd. [2014] 50 taxmann.com 105/228 Taxman 48 (Allahabad), it was held as under:

“10. Section 292BB of the Act was inserted by the Finance Act, 2008 with effect from April 1, 2008. Section 282BB of the Act provides a deeming fiction. The deeming fiction is to the effect that once the assessee has appeared in any proceeding or cooperated In any enquiry relating to an assessment or reassessment, it shall be deemed that any notice under the provisions of the Act, which is required to be served on the assessee, has been duly served upon him in time in accordance with the provisions of the Act The assessee is precluded from taking any objection in any proceeding or enquiry that the notice was (i) not served upon him ; or (ii) not served upon him in time ; or (iii) served upon him in an improper manner. IN other words, once the deeming fiction comes into operation, the assessee is precluded from raising a challenge about the service of a notice, service within time or service in an improper manner. The proviso to section 292BB of the Act, however, carves out an exception to the effect that the section shall not apply where the assessee has raised an objection before the completion of the assessment or reassessment. Section 292BB of the Act cannot obviate the requirement or complying with a jurisdictional condition. For the Assessing Officer to make an order of assessment under section 143(3) of the Act, it is necessary to issue a notice under section 143(2) of the Act and in the absence of a notice under section 143(2) of the Act, the assumption of jurisdiction itself would be invalid.”

16. In the same decision in Salarpur Cold Storage (P.) Ltd. (supra), the Allahabad High Court noticed that the decision of the Supreme Court in Hotel Blue Moon (supra) where in relation to block assessment, the Supreme Court held that the requirement to issue notice under Section 143(2) was mandatory. It was not “a procedural irregularity and the same is not curable and, therefore, the requirement of notice under Section 143(2) cannot be dispensed with.”

17. The Madras High Court held likewise in Sapthagiri Finance & Investments v. ITO [2012] 25 taxmann.com 341/210 Taxman 78 (Madras) (Mag.). The facts of that case were that a notice under Section 148 of the Act was issued to the Assessee seeking to reopen the assessment for AY 2000-01. However, the Assessee did not file a return and therefore a notice was issued to it under Section 142 (1) of the Act. Pursuant thereto, the Assessee appeared before the AO and stated that the original return filed should be treated as a return filed in response to the notice under Section 148 of the Act. The High Court observed that if thereafter, the AO found that there were problems with the return which required explanation by the Assessee then the AO ought to have followed up with a notice under Section 143(2) of the Act. It was observed that:

“Merely because the matter was discussed with the Assessee and the signature is affixed it does not mean the rest of the procedure of notice under Section 143(2) of the Act was complied with or that on placing the objection the Assessee had waived the notice for further processing of the reassessment proceedings. The fact that on the notice issued u/s 143(2) of the Act, the assessee had placed its objection and reiterated its earlier return filed as one filed in response to the notice issued u/s 148 of the Act and the Officer had also noted that the same would be considered for completing of assessment, would show that the AO has the duty of issuing the notice under Section 143(3) to lead on to the passing of the assessment. In the ‘circumstances, with no notice issued u/s 143(3) and

16. We find Hon’ble Patna High Court in the case of CIT vs. Nagendra Prasad (supra) has held that where notice was issued by the Assessing Officer under Section 148 requiring the assessee to file a return within thirty days but return was filed after eight and a half months, since return was filed by the assessee in response to said notice though delayed, there should have been a notice issued under section 143(2) as requirement to issue notice could not be dispensed with. The relevant observations of Hon’ble High Court read as under:

“4. The only question of law arising in the facts and circumstances of the case is whether notice should have been issued under section 143(2) of the Income-tax Act?

5. Admittedly, the notice was issued by the Assessing Officer under section 148 of the Act on 14-7-2008 requiring the assessee to file a return within thirty days. A return was filed much later on 31-3-2009, after eight and a half months.

6. On identical facts, in M.A. No. 239 of 2011 titled as Chand Bihari Agrawal v. Commissioner of Income Tax, Central, Patna decided on 25-7-2023, this Court considered the issue and held against the revenue.

7. We find that the question of law has to be answered in favour of the assesee and against the revenue. Hotel Blue Moon (supra) governs the issue which has been followed in Chand Bihari Agrawal (supra).

8. The Miscellaneous Appeal stands dismissed.”

17. The various other decisions relied on by the Ld. Counsel for the assessee also supports his case to the proposition that when the assessee files return in response to the notice u/s 148 of the Act, though, belatedly, non-issue of notice u/s 143(2) of the Act makes the re-assessment proceeding a nullity.

18. So far as the decision relied on by the Ld. DR is concerned, no doubt, the Hon’ble Delhi High Court on an earlier occasion has taken a view that non-issue of notice u/s 143(2) of the Act does not make the re-assessment proceedings invalid where the assessee files the return in response to the notice u/s 148 of the Act. However, it is to be noted that subsequent to this decision, the Hon’ble High Court recently in three other decisions has held that when the assessee files return in response to the notice u/s 148 of the Act, though, belatedly, the issue of notice u/s 143(2) of the Act is a mandatory requirement and non-issue of the same makes the re-assessment proceedings invalid. In any case, it is the settled position of law that when two views are possible on an issue, the view which is favourable to the assessee has to be adopted. Since the Assessing Officer in the instant case has admittedly not issued any notice u/s 143(2) of the Act after the assessee filed the return in response to the notice u/s 148 of the Act, though, belatedly, therefore, respectfully following the decisions cited (supra), we hold that the order passed by the Assessing Officer without following the mandatory requirement of issue of notice u/s 143(2) of the Act makes such re-assessment order a nullity. Since the assessee succeeds on this legal ground, the grounds challenging the addition on merit are not being adjudicated.”

22. Since the facts of the in the instant case are identical to the facts of the case already decided by the Co-ordinate Bench of the Tribunal cited (supra), therefore, we hold that the order passed by the Assessing Officer without following the mandatory requirement of issue of notice u/s 143(2) makes the re-assessment order an invalid assessment. We, therefore, set aside the order of the Ld. CIT(A) / NFAC and the grounds raised by the assessee on this issue are allowed.

23. In the result, the appeal filed by the assessee is allowed.

Order pronounced in the open Court on 7th July, 2026.

Author Bio