The Government of Rajasthan, Commercial Taxes Department, has issued a circular superseding Circular No. F.17(151)ACCT/GST/2017/7602 dated 07.01.2022 and prescribing revised guidelines for scrutiny of returns under Section 61 of the RGST Act, 2017, read with Rule 99 of the RGST Rules, 2017. The circular standardises the procedure for selection and scrutiny of returns, including analysis of specified risk parameters such as mismatches in GSTR-1, GSTR-3B, GSTR-9, GSTR-2A/2B, TDS, TCS, e-way bills, ITC, RCM liability, cancelled registrations, delayed returns and interest payment. It provides for preparation and approval of scrutiny lists by the Business Intelligence Unit, allocation of cases through the Integrated Tax Management System for faceless or jurisdictional scrutiny, issuance of Form GST ASMT-10, consideration of replies in ASMT-11, closure through ASMT-12 where appropriate, and transfer of unresolved cases for action under Sections 73, 74 or 74A. The circular also requires prior approval for adjudication where tax not paid, short paid or ITC wrongly availed or utilised exceeds ₹5 crore, prescribes monitoring responsibilities, and includes a manual for scrutiny of returns outside jurisdiction.

Government of Rajasthan

Commercial Taxes Department

Circular No: F.17 (134) ACCT/GST/2017 PART-II-01613

Date: 07/07/2026

CIRCULAR

All Additional Commissioner (Adm.),

Commercial Taxes Department,

Rajasthan.

Sub.:- Guidelines to be followed regarding scrutiny of returns under section 61 of the RGST Act, 2017.

Section 61 of the RGST Act, 2017 stipulates that the proper officer may scrutinize the returns and particulars furnished by a registered person with a view to verify the correctness of the return/returns filed. Further, rule 99 of the RGST Rules, 2017 mandates that the discrepancies, if any, observed shall be communicated to the taxpayer to seek his explanation.

Vide Circular no. F.17(151)ACCT/GST/2017/7602 dated 07.01.2022, guidelines to be followed regarding scrutiny of returns under section 61 of the RGST Act, 2017 were laid down. Now, in supersession of the same, the following guidelines are hereby issued so as to ensure the uniformity and to standardize the procedure for the forthcoming years and pending scrutiny proceedings as per Section 61 of the RGST Act along with the subsequent action as per section 73, section 74 or section 74A, as the case may be, of the RGST Act, 2017 if required to be initiated for the purpose of demand and recovery.

1. The Business Intelligence Unit (here in after referred to as BIU), from time to time, shall undertake the analysis of data submitted by the registered taxpayer (hereinafter referred to as RTP) available on GSTN Portal based on the parameters given below:-

PARAMETERS

(i) Excess Outward Tax in GSTR-1 compared to GSTR-9/GSTR-3B.

(ii) Less Turnover shown in GSTR-3B compared to GSTR-7(TDS).

(iii) Less Turnover shown in GSTR-1 compared to GSTR-8 (TCS).

(iv) Less RCM Liability disclosed in GSTR-9 than shown by suppliers in GSTR-1.

(v) Excess Outward liability in E-way Bills compared to GSTR-3B.

(vi) Excess ITC claimed in GSTR- 3B/9 which is not confirmed in GSTR-2A/2B or GSTR- 9.

(vii) Excess ISD ITC availed in GSTR-9 v/s GSTR- 2A/2B.

(viii) ITC claimed from suppliers who have not filed GSTR- 3B.

(ix) ITC claimed from suppliers whose RC have been cancelled.

(x) ITC claims after the last date of availment of ITC as per section 16(4) of the RGST Act, 2017.

(xi) GSTR-3B filed after due date and interest paid/Short paid/ not paid.

In the exercise of analyzing, two sets of treatments are to be accorded to the aforesaid parameters, namely:-

(a) Serial number (i), (v) and (ix) shall be mandatorily given for scrutiny;

(b) Suitable weightage may be allocated for the remaining parameters for preparation of the list.

In addition to above, other parameters if any, may be included with the prior approval of Chief Commissioner, State Tax.

2. The list of RTPs based on the parameter(s) for selection of returns for scrutiny shall be prepared by the Special Commissioner (BIU). The list of RTP shall be prepared mentioning all the parameters on the basis of which the returns is being selected for scrutiny. In both cases, the draft list shall be cross-referenced with cases selected for audit so as to remove duplication.

3. The Special Commissioner (BIU) shall get the list approved by the Chief Commissioner State Tax. The cases so generated will be allocated through the Integrated Tax Management System (ITMS) to the officers across the State for faceless scrutiny or to the proper officers having territorial jurisdiction over such RTPs, as may be decided from time to time.

4. While the cases for scrutiny shall be allocated by the HQ on the basis of the given parameters, it is expected of the tax officer to apply due diligence so as to make a complete and holistic scrutiny of the taxpayers. Where any discrepancy in return(s) already selected for scrutiny comes to the notice of proper officer in addition to the discrepancies already identified, he shall include the same in ASMT-10.

5. Where any discrepancy in returns pertaining to the same taxpayer for tax-period(s) other than that selected for scrutiny or pertaining to taxpayers other than those selected by HQ for scrutiny come to knowledge of the officer, he shall update the details thereof on the ITMS portal and proceed for scrutiny in the matter.

6. If any discrepancy comes to the notice after due scrutiny and review of data, the proper officer shall generate an intimation in Form GST-ASMT-10 from the ITMS portal as per the provisions of section 61(1) RGST Act 2017 read with rule 99 (1) of the RGST Rules clearly indicating all the discrepancies noticed during the scrutiny of the returns. The intimation so generated shall be duly uploaded on the Boweb portal.

7. Where the RTP furnishes explanation for the discrepancies in ASMT-11 and if such explanation is acceptable, the proper officer shall drop the proceeding and inform him accordingly in ASMT-12.

8. Where the RTP submits ASMT-11 within thirty days from the date of service of intimation in Form ASMT-10 or such further period as may be permitted by the proper officer and –

(i) furnishes explanation for the discrepancies in ASMT-11 and if such explanation is acceptable; or

(ii) accepts the findings so communicated and pays the tax along with the interest and any other amount arising from such discrepancy mentioned in the said intimation by filing the required DRC-03,

then, the proper officer shall accept the said reply/payment and drop the said proceedings and inform him accordingly in ASMT-12.

9. In case no satisfactory explanation is furnished within the stipulated time or where the registered person, after accepting the discrepancies, fails to take the corrective measure(s) in his return(s) for the month(s) in which the discrepancy is accepted, the case shall be transferred by the Scrutiny Officer (who has carried out the faceless scrutiny) to the Jurisdictional proper officer through the Boweb Portal in accordance with the Manual for Scrutiny of Returns of Taxpayers (Outside Jurisdiction) issued by GSTN (herewith attached). The scrutiny officer shall also attach his ‘finding/scrutiny report’ along with comments/reasons for recommending to proper jurisdictional officer through Boweb portal.

10. The Jurisdictional Proper Officer shall initiate appropriate action and proceed to determine the tax and other dues under section 73, 74 or 74A. In cases which result in detection of tax not paid or short paid or input tax credit wrongly availed or utilized more than Rs. Five Crore , adjudication proceedings shall be initiated only after the prior approval of the concerned jurisdictional Additional Commissioner (Adm.) of State Tax.

11. In case, the scrutiny has been initiated by the Jurisdictional Proper Officer only, he shall proceed accordingly. All such cases pertaining to 2022-23 shall be transferred to the Jurisdictional proper officer latest by the 25th of August, 2026.

12. Where no discrepancy exists after scrutiny of return(s), the proper officer shall report the facts along with reasons, on the feedback functionality provided on the ITMS portal in due time.

13. The concerned Additional Commissioner (Adm.) shall ensure proper monitoring of the work done by the officers under their jurisdictions in light of the legal provisions and the stipulated time frame.

The instructions contained in this circular are restricted for official use only.

(Anandhi)

Chief Commissioner

State Tax,

Rajasthan, Jaipur

F.17 (134) ACCT/GST/2017 PART-II-01613

Date:

Copy to following for information and necessary action:

1. Chief Commissioner, CGST & Central Excise, Jaipur Zone, Jaipur.

2. PS to Commissioner, State Tax, Rajasthan.

3. Joint Secretary, Finance (Tax) Department, Jaipur.

4. All Special Commissioners, CTD, Headquarter, Jaipur.

5. Additional Commissioner (IT) for uploading it on Department’s website rajtax.gov.in and on the web portal RAJVISTA/TCS, CTD, Jaipur.

6. Director, Public Relations, CTD, Jaipur for publicity.

7. Guard file.

Chief Commissioner

State Tax,

Rajasthan, Jaipur

Manual > Scrutiny of Returns of Taxpayers (Outside Jurisdiction) by a Scrutiny Officer

This manual is applicable only to state officers for the time being

A. Role of Scrutiny Officer

1. Scrutiny Officer is a new role which can be assigned in addition to the role of “Adjudicating Authority” if the State Administration desires that the officer should be able initiate scrutiny of taxpayers across the State without jurisdictional restrictions.

2. If required, this role can also be assigned independently.

3. Sub-state admins cannot assign the role of Scrutiny Officer.

B. Assignment of Role of Scrutiny Officer

To assign the Scrutiny Officer role to a Tax Official, perform the following steps:

1. Access the GST Portal. The GST Home page is displayed.

2. Using your valid credentials, login to the GST Portal.

3. Navigate to Jurisdictional Admin and click on User Role & Jurisdiction Administration.

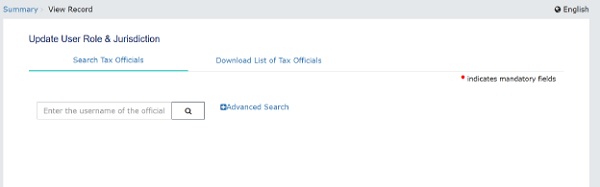

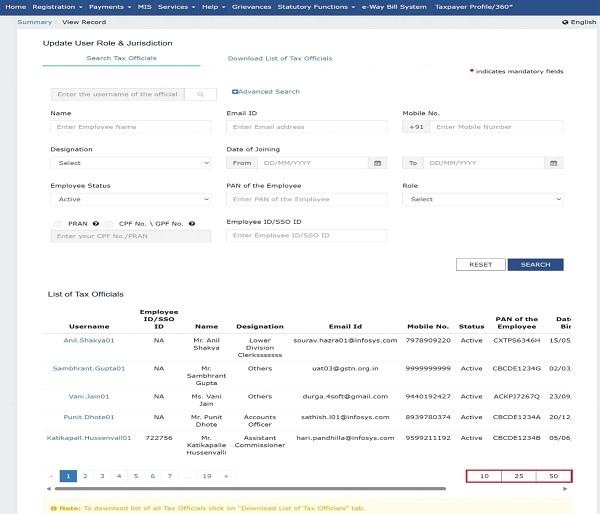

4. The View Record page will be displayed on the screen. Search Tax Officials tab will be selected by default.

5. To search for a particular tax officer:

a. Admin can enter the Officer’s exact username in Search Tax Officials tab, or

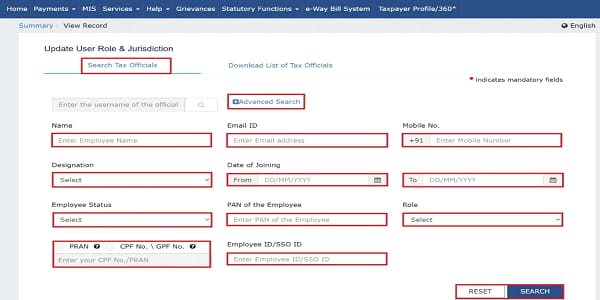

b. Admin can click on the Advanced Search hyperlink under Search Tax Officials Here user can enter any one field or multiple fields to search the list of tax officials.

Tax Officer can search using at least one of these fields Name, Email ID, Mobile No., Date of Joining (From and To), Employee Status, PAN or Employee ID/SSO ID, Designation or Role (from the respective drop-down list), PRAN or CPF No./GPF No. After entering the details click on the SEARCH button to proceed further or click on the RESET button to enter the details again.

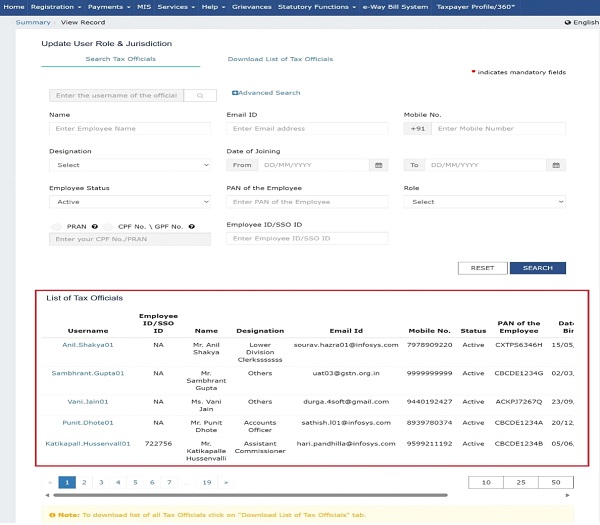

6. List of Tax Officials will be displayed on the screen.

Note: If the user search by Employe Status field alone, the user will get maximum 100 records only. To get a complete list, the user needs to navigate the Download List of Tax Officials tab.

Note: Tax officer can view the desired number of records per page by clicking on the Pagination Option provided at the bottom of List (10/25/50).

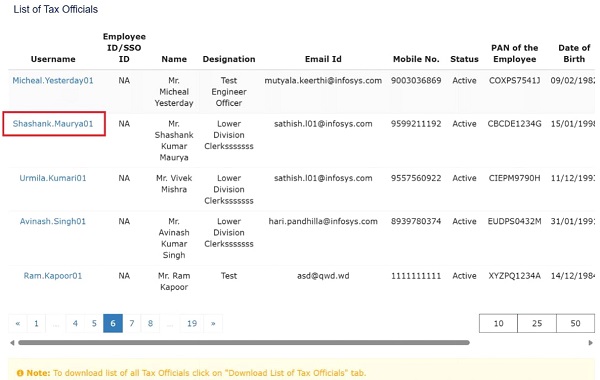

7. Click on the hyperlink under the Username column.

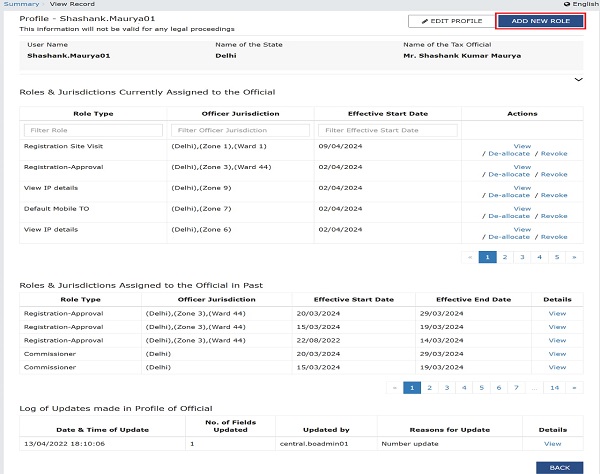

8. View Record page will be displayed on the screen. Click on the ADD NEW ROLE button to assign Scrutiny officer role to the official.

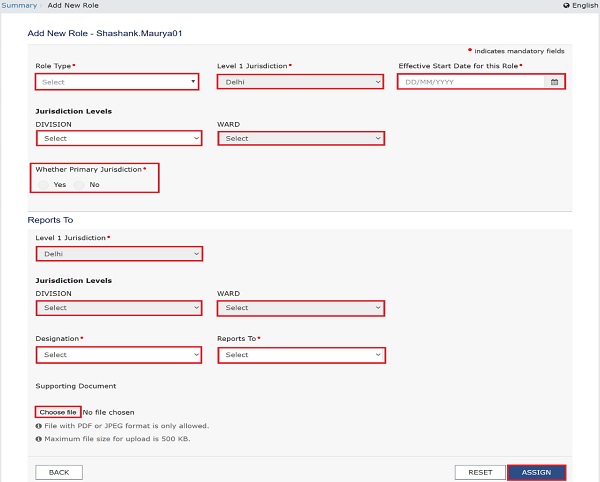

9. The Add New Role page is displayed for the selected profile. Add all the mandatory fields.

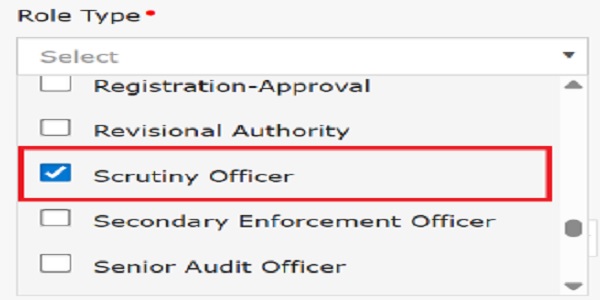

10. Select the Scrutiny Officer role from the Role Type dropdown list.

11. Once all the mandatory fields are filled, click on the ASSIGN button to add the Scrutiny Officer role.

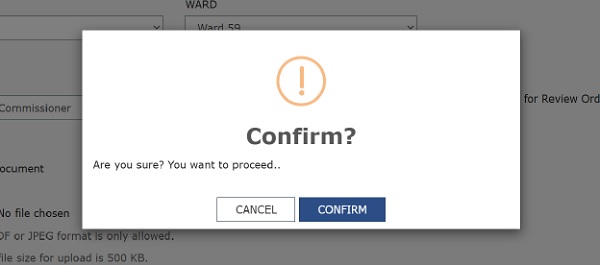

12. Click on the CONFIRM button to save the Scrutiny Officer role details.

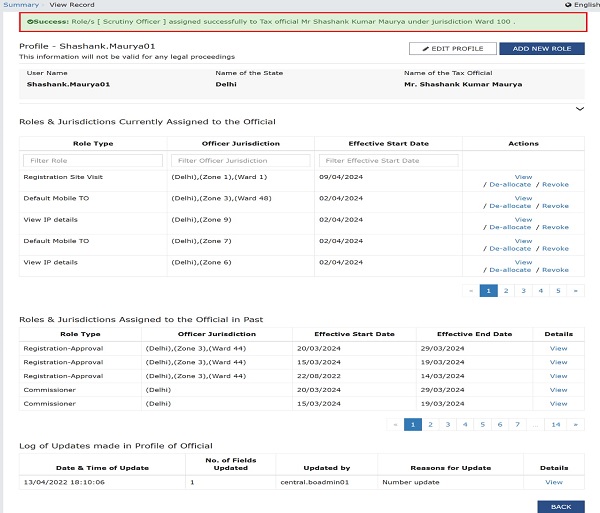

13. A success message is displayed for the assignment of the Scrutiny Officer role.

C. Initiate Suo-Moto Proceedings for Scrutiny of Returns

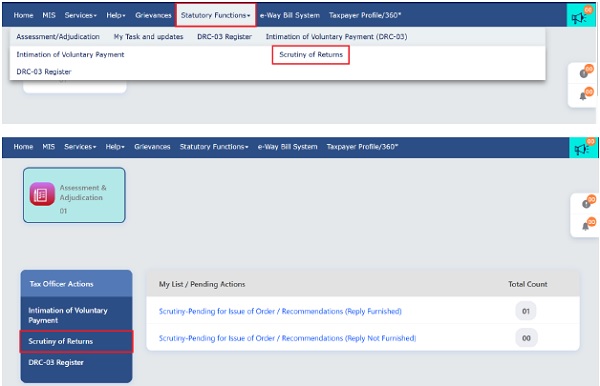

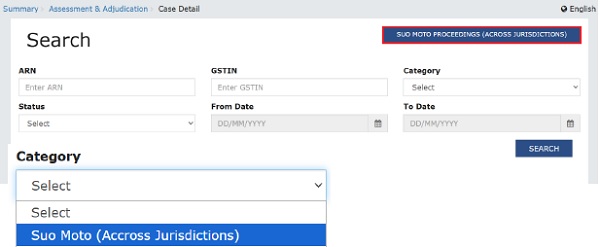

1. Navigate to Statutory Functions > Scrutiny of Returns or Navigate to Assessment & Adjudication > Scrutiny of Returns option

2. For Scrutiny Officer role, Suo Moto Proceedings (Across Jurisdictions) button will be displayed. This option will also appear in the Category dropdown list.

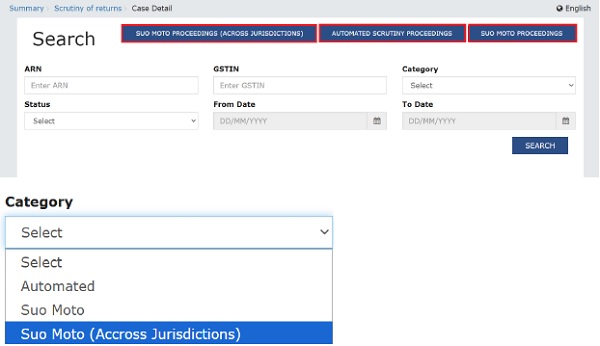

3. If the Officer has both Adjudicating Authority and Scrutiny Officer role, the following three buttons will be displayed.

- Suo Moto Proceedings (Across Jurisdictions)

- Automated Scrutiny Proceedings

- Suo Moto Proceedings

Identical options will also appear in the Category dropdown list.

4. For officers with only Adjudicating Authority role, Suo Moto Proceedings and Automated Scrutiny Proceedings buttons will be displayed.

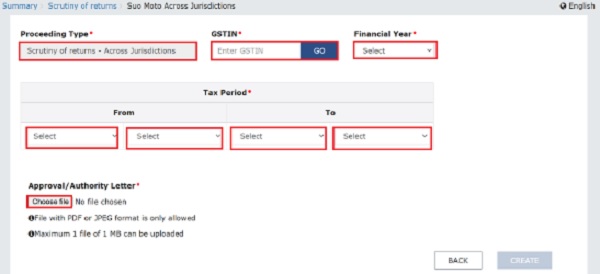

5. When the Scrutiny officer opens the Suo Moto (Across Jurisdictions) page, the Proceeding Type field is auto populated. All other fields are similar to suo-moto proceedings functionality. However, an additional step – to upload the Approval/Authority Letter by clicking on ‘Choose File’ is mandatory for the Scrutiny Officer.

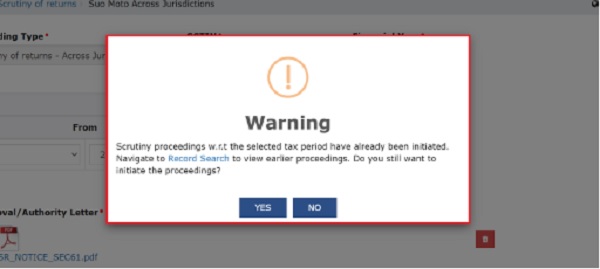

6. If a Case ID for any type of scrutiny proceedings already exists with the same GSTIN and financial year (created either by Adjudicating Authority or Scrutiny Officer), a warning message will be displayed.

On click of “YES”, Case ID will be created and on click of “NO”, warning message will disappear, and data filled in all the fields will disappear.

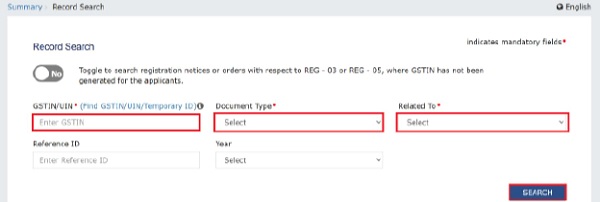

Click on the “Record Search” to view earlier proceedings.

7. After clicking on Record Search, Scrutiny Officer will be redirected to the Record Search Add relevant details in the mandatory fields.

8. When a Scrutiny Officer creates a Case ID, an email/SMS will also be sent to the Adjudicating Authorities mapped to the taxpayer’s jurisdiction.

D. References

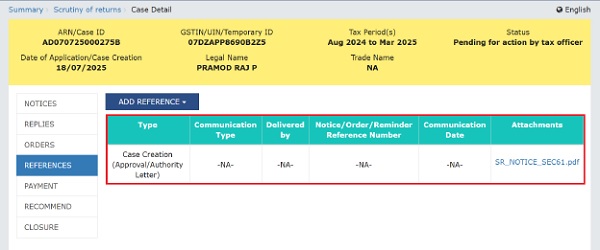

1. Once the Scrutiny Officer creates a Case ID, Approval/Authority letter will appear in the References Folder along with the uploaded document.

E. Add Recommendation

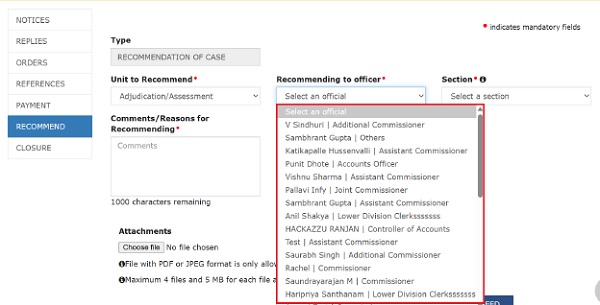

1. For Suo Moto Proceedings (Across Jurisdictions), Recommending to officer list will be populated based on taxpayer’s current jurisdiction. This means, the case can only be recommended to an officer for action under section 73, 74, 74A who holds a role within the taxpayer’s jurisdictional hierarchy.

Note: The entire process of scrutiny of returns, including issuing Notice in Form GST ASMT-10, filing of response to the same by the taxpayer in Form GST ASMT-11 and issuance of an order of acceptance of reply by Tax Officer, wherever applicable, in Form GST ASMT-12, shall continue to be the same as applicable for the officers assigned the “Adjudicating Authority” role.

To view the detailed manual for Scrutiny of Returns, click the below given link: https://botutorial.internal.gst.gov.in/userguide/taxofficial1/index.html#t=Scrutiny_of_Retur ns_fAQ.htm