Case Law Details

Canara Bank (Erstwhile Syndicate Bank) Vs KGOC Terminals Private Limited (NCLT Amaravati)

The National Company Law Tribunal (NCLT), Amaravati Bench, admitted a Section 7 application under the Insolvency and Bankruptcy Code, 2016 (IBC) filed by the financial creditor against the corporate debtor for initiation of the Corporate Insolvency Resolution Process (CIRP). The Tribunal also appointed an Interim Resolution Professional (IRP) and declared a moratorium under Section 14 of the IBC.

The financial creditor filed the petition seeking initiation of CIRP for default in repayment of ₹64,69,67,541.47 as on 01.12.2020. The corporate debtor, incorporated on 28.06.2012, had approached the bank for financial assistance. A term loan of ₹44.21 crore was sanctioned on 27.07.2017 for setting up 23 bulk liquid terminals for storage of petroleum and petrochemical products, secured through mortgage of immovable properties. Subsequently, the corporate debtor defaulted in repayment of principal and interest, and the loan account was classified as a Non-Performing Asset (NPA) on 01.12.2020.

Following the default, the financial creditor initiated proceedings under the SARFAESI Act. It issued a demand notice under Section 13(2) on 08.04.2021, took symbolic possession of the secured assets under Section 13(4), published possession notices, issued a redemption notice, and conducted two e-auctions. Despite these measures, an outstanding amount of ₹61.19 crore remained as on 11.01.2023. Although the corporate debtor submitted a One Time Settlement (OTS) proposal, it was initially not accepted.

The corporate debtor opposed the petition primarily on the ground that the alleged default occurred during the suspension period under Section 10A of the IBC. It argued that the date of default was 01.12.2020, which fell within the period protected by Section 10A, and therefore no CIRP could be initiated. It also disputed the existence and computation of the financial debt, contending that the petition failed to satisfy the requirements of Section 7 and was filed as a debt recovery mechanism.

The financial creditor, in its rejoinder, stated that the repayment schedule had been revised at the corporate debtor’s request. The project completion date was extended from 15.11.2018 to 15.11.2020, shifting the first repayment instalment from 15.02.2019 to 15.02.2020. It asserted that the corporate debtor had defaulted in servicing interest from 31.05.2019 and defaulted in repayment of principal from 15.02.2020, which was prior to the Section 10A suspension period. The creditor also relied upon the corporate debtor’s OTS proposal dated 23.11.2022 as an acknowledgment of debt.

During the proceedings, an OTS sanctioned on 28.04.2025 led to withdrawal of the company petition with liberty to revive it if the settlement terms were breached. The corporate debtor paid an upfront amount of ₹4.5 crore, but subsequently failed to comply with the OTS conditions. The financial creditor therefore filed a restoration application, which was allowed on 28.04.2026, restoring the original petition.

The Tribunal first examined whether the petition was filed within the limitation period. Although the petition had been filed beyond three years from the date of default, it observed that the OTS proposal dated 23.11.2022 constituted a clear acknowledgment of financial debt, thereby giving rise to a fresh period of limitation. The Tribunal further held that the subsequent OTS sanctioned on 28.04.2025, accepted by the corporate debtor, also amounted to acknowledgment of debt. Since the corporate debtor failed to comply with the OTS and the restoration application was filed after cancellation of the settlement, both the original petition and the restoration application were held to be within limitation.

On the issue of Section 10A, the Tribunal rejected the corporate debtor’s objection. It found that, although the NPA date was 01.12.2020, the repayment obligations had become due much earlier. The first instalment became payable on 15.02.2020, and the corporate debtor had also defaulted in payment of interest from 31.05.2019. Therefore, the defaults had commenced before the commencement of the suspension period under Section 10A. Relying on the decisions of the Supreme Court in Laxmi Pat Surana v. Union Bank of India and Ramesh Kymal v. Siemens Gamesa Renewable Power Pvt. Ltd., the Tribunal held that Section 10A bars CIRP only for defaults occurring during the protected period and does not apply where defaults had already occurred before that period.

The Tribunal also concluded that the financial debt and default were established. It noted that the financial creditor had produced the sanction letter, statements of account, certificates under the Bankers’ Books Evidence Act, and the CRILC report. The Tribunal further observed that the corporate debtor’s own OTS proposal offering ₹43 crore and depositing 15% thereof amounted to a clear acknowledgment of liability. The corporate debtor also failed to produce any proof of payment of the balance OTS amount. Consequently, the Tribunal held that there was a financial debt, a default in repayment, and that the default exceeded the statutory threshold under Section 4 of the IBC.

Finding the petition complete and noting that no disciplinary proceedings were pending against the proposed IRP, the Tribunal admitted the Section 7 application, declared a moratorium under Section 14 of the IBC, appointed the proposed IRP, directed the financial creditor to deposit ₹5 lakh towards CIRP expenses, and ordered communication of the admission order to all concerned parties.

FULL TEXT OF THE NCLT JUDGMENT/ORDER

Order pronounced and recorded vide separate sheets. The Petition bearing RCP (IBC)/1/7/AMR/2026 (Old Case CP (IB)/16/7/AMR/ 2023 filed by the Financial Creditor under Section 7 of the IBC, 2016 is admitted, and the IRP is appointed.

The Petition bearing CP (IB)/16/7/AMR/2023 (hereinafter referred to as the “CP 16/2023” or “Petition”) has been e-filed on 24.02.2023 and physically filed vide Diary No.1901 dated 14.03.2023, by the Canara Bank (erstwhile Syndicate Bank) (hereinafter referred to as the “Financial Creditor”) under Section 7 the Insolvency and Bankruptcy Code, 2016 (hereinafter referred to as the “IBC” or “Code”) read with Rule 4 of the Insolvency and Bankruptcy (Application to Adjudicating Authority) Rules, 2016 (hereinafter referred to as the “IB Rules”) with a prayer to initiate the Corporate Insolvency Resolution Process (hereinafter referred to as the “CIRP”) against KGOC Terminals Private Limited (hereinafter referred to as the “Corporate Debtor”) for default in payment of dues of Rs.64,69,67,541.47 as on 01.12.2020.

2. The Corporate Debtor is a Company incorporated on 28.06.2012 under the Companies Act, 1956 with CIN: U63030AP2012PTC081699 having its registered office at D.No.70-15-15, Chunduru Govindaraju Street, Road No.2, Suresh Nagar, Kakinada-533033, Andhra Pradesh. Hence, the territorial jurisdiction lies with this Adjudicating Authority.

FACTS OF THE CASE:

3. The facts of the case, as stated in the Petition filed by the Financial Creditor, are summarized below:

(i) The Canara Bank (erstwhile Syndicate Bank), having its branch office at Kakinada Main-II Branch, Kakinada, is the Financial Creditor. This Petition has been instituted through its Authorized Signatory, Ms. K. Sunita, who is duly empowered to represent the Financial Creditor.

(ii) The Corporate Debtor is a private limited company duly registered with the Registrar of Companies, Vijayawada. It is engaged in supporting and auxiliary transport activities, including travel agency-related services.

(iii) The Corporate Debtor approached the Financial Creditor for financial assistance and submitted a loan application dated 07.04.2017 seeking a term loan facility.

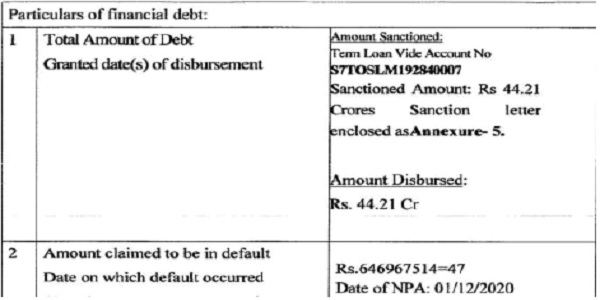

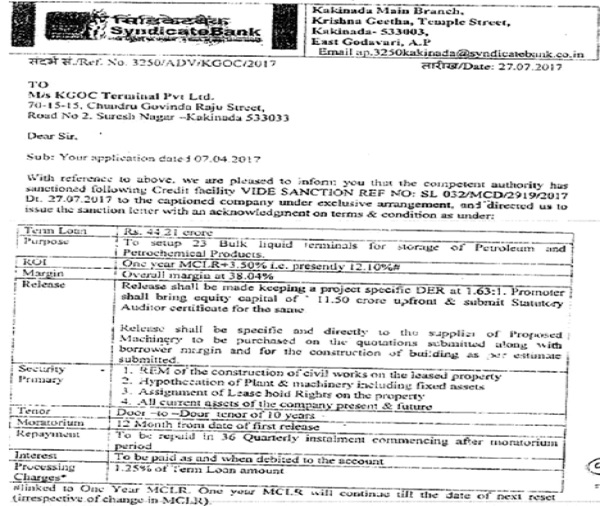

(iv) Upon consideration of the request, the Financial Creditor vide sanction letter dated 27.07.2017, sanctioned a term loan of Rs.44.21 crores for the purpose of setting up 23 bulk liquid terminals for storage of petroleum and petrochemical products under A/c No. S7TOSLM192840007. To secure the credit facilities, the mortgagor deposited title deeds relating to immovable properties, and created mortgage in favour of the Financial Creditor.

(v) Subsequently, the Corporate Debtor committed defaults in servicing the loan by failing to make timely repayment of principal and interest. Owing to default, the loan account of the Corporate Debtor was classified as a Non-Performing Asset (hereinafter referred to as the “NPA”) on 01.12.2020 in accordance with the guidelines issued by the Reserve Bank of India (hereinafter referred to as the “RBI”). As on the date of NPA classification, the outstanding liability stood at Rs.64,69,67,514.47.

(vi) Consequent upon the default, the Financial Creditor initiated recovery proceedings under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (hereinafter referred to as the “SARFAESI Act”) and issued a demand notice under Section 13(2) on 08.04.2021, which was duly acknowledged by the Corporate Debtor. Thereafter, symbolic possession of the secured assets was taken on 01.09.2021 and the possession notice under Section 13(4) of SARFAESI Act was published in newspapers on 05.09.2021. A redemption notice under Section 13(8) of the SARFAESI Act was subsequently issued on 28.09.2021. The Financial Creditor also initiated sale proceedings by issuing auction notices dated 02.07.2022 and 07.09.2022, pursuant to which e-auctions were conducted on 11.08.2022 and 26.09.2022 respectively.

(vii) Despite the above, the outstanding amount payable by the Corporate Debtor was Rs.61,19,67,514.47 as on 11.01.2023. Though one of the Directors of the Corporate Debtor informed the Financial Creditor regarding submission of a One Time Settlement (hereinafter referred to as the “OTS”) proposal, the same was not accepted by the Financial Creditor. The Corporate Debtor has failed to discharge its admitted financial obligations and is unable to repay the outstanding debt.

(viii) As per Part-IV of Form 1 enclosed with the Petition, the details of total amount of debt sanctioned/ disbursed, the amount claimed to be in default and the date on which the default occurred are reproduced below:

(ix) In support of Petition, the Financial Creditor has enclosed the following documents:

(a) Copy of Master Data of the Corporate Debtor as Annexures-2 & 3 at pages 31-33 of the Petition.

(b) Sanction letter dated 27.07.2017 issued by the Financial Creditor as Annexure-5 at pages 36-41 of the Petition.

(c) Composite Hypothecation Agreement dated 10.11.2017 as Annexure-6(a) at pages 42-57 of the Petition.

(d) Memorandum of Deposit of Title Deeds as Annexure-6(b) at pages 58-88 of the Petition.

(e) Guarantee Agreements dated 10.11.2017 as Annexure-6(c) at pages 89-127 of the Petition.

(f) Modification of terms and conditions of sanction vide letter dated 06.11.2017 issued by the Financial Creditor as Annexure-7 at pages 128-129 of the Petition.

(g) Statement of Account maintained by the Financial Creditor in respect of the Corporate Debtor for the period from 01.08.2017 to 11.01.2023 as Annexure-8 at pages 130-140 of the Petition.

(h) Certificates under Section 2(A)(a), Section 2(A)(b) and Section 2(A)(c) of the Bankers’ Books of Evidence Act, 1891 (as amended) as Annexure-8(a), 8(b) and 8(c) at pages 141-145 of the Petition.

(i) Certificate for Notional Interest as Annexure-8(d) at page 147 of the Petition.

(j) Demand Notice under Section 13(2) of SARFAESI Act dated 08.04.2021 as Annexure-9(i) at pages 147-152 of the Petition.

(k) Acknowledgement of Demand Notice under Section 13(2) of SARFAESI Act dated 08.04.2021 as Annexure-9(ii) at pages 153-157 of the Petition.

(l) Symbolic Possession Notice under Section 13(4) of SARFAESI Act dated 01.09.2021 as Annexure-9(iii) at pages 158-163 of the Petition.

(m) Possession Notice publication in newspapers dated 05.09.2021 as Annexure-9(iv) at pages 164-165 of the Petition.

(n) Redemption Notice dated 28.09.2021 under Section 13(8) of the SARFAESI Act as Annexure-9(v) at pages 166-169 of the Petition.

(o) Sale Notice for first e-auction dated 02.07.2022 as Annexure-9(vi) at pages 170-173 of the Petition.

(p) First e-auction dated 11.08.2022 as Annexure-9(vii) at pages 174-175 of the Petition.

(q) Sale Notice for second e-auction dated 07.09.2022 as Annexure-9(viii) at pages 176-178 of the Petition.

(r) Second e-auction dated 26.09.2022 as Annexure-9(ix) at pages 179-183 of the Petition.

(s) Central Repository of Information on Large Credits (hereinafter referred to as the “CRILC”) Report dated 20.02.2023 as Annexure-10 at pages 184-185 of the Petition.

(t) Valuation Report dated 28.11.2022 in respect of Plant & Machinery of the Corporate Debtor as Annexure-11 at pages 186-198 of the Petition.

PRELIMINARY COUNTER FILED BY THE CORPORATE DEBTOR:

4. The Corporate Debtor vide Diary No.6137 dated 09.08.2023, filed the Preliminary Counter denying the submissions made in the Petition and prayed to dismiss the Petition. It has been stated in the Preliminary Counter that:

(i) The Financial Creditor sanctioned a term loan of Rs.44.21 crores to the Corporate Debtor for establishment of 23 bulk liquid terminals for storage of petroleum and petroleum products. As per the loan sanction letter dated 27.07.2017, the loan was to be repaid in 36 quarterly installments, which commences after the moratorium period.

(ii) As per the averments in the Petition itself, the alleged default occurred on 01.12.2020, being the date on which its loan account was classified as NPA. Even assuming, without admitting, that 01.12.2020 is the date of default, the Financial Creditor cannot invoke the provisions of the IBC for initiation of CIRP, since the default falls within the period protected under Section 10A of the Code.

(iii) In support of the above contention, the Corporate Debtor relied upon Section 10A of the Code, which was introduced in view of the economic distress caused by the Covid-19 pandemic and prohibits initiation of insolvency proceedings in respect of defaults arising during the specified suspension period. It was submitted that the operation of Section 10A of the Code, initially introduced with effect from 25.03.2020, was subsequently extended by notification dated 24.09.2020, thereby covering defaults arising up to 25.03.2021. Therefore, the exclusion period under Section 10A of the Code extends from 25.03.2020 to 25.03.2021, whereas the alleged date of default pleaded in this Petition is 01.12.2020. Since the alleged default squarely falls within the protected period, no Petition for initiation of the CIRP can ever be maintained in respect of such default, and this Petition is barred by Section 10A of the Code.

(iv) The Corporate Debtor categorically denies the alleged financial debt of Rs.64,69,67,514.47 and any interest claimed thereon. Further, the purported debt, its computation, and the interest calculation are hypothetical, erroneous and baseless.

(v) It is contended that neither there was any financial debt nor any admitted liability exists in relation to the alleged transactions. Consequently, the Petition cannot be treated as a valid Petition under Section 7 of the Code and is liable to be rejected under Section 7(5)(b) of the Code. The Financial Creditor failed to establish the essential ingredients required under Section 7 of the Code read with Rule 4 of the IB Rules. The Petition is founded on concocted facts and has been filed as a debt recovery mechanism with mala fide intent to damage the reputation of the Corporate Debtor.

(vi) The Corporate Debtor has made all efforts towards execution of the project and bears no liability towards the Financial Creditor.

5. During the course of hearing dated 13.09.2023, it was noted that the Proxy Counsel appearing for the Corporate Debtor submitted that the Preliminary Counter can be treated as the Main Counter. By recording the aforesaid submission, the matter was posted to 11.10.2023, for filing the rejoinder, if any.

IA (IBC)/1/2024 FILED BY THE FINANCIAL CREDITOR:

6. Subsequently, the Financial Creditor vide Diary No. 8 dated 02.01.2024, filed the IA (IBC)/1/2024 (hereinafter referred to as the “IA 1/2024”) under Section 60(5) of the IBC, 2016 praying to take on record the additional documents enclosed with the IA as Annexure-A (Letters dated 27.07.2017, 28.03.2019 and 19.07.2019 of the Financial Creditor), Annexure-B (Statement of Account of the Corporate Debtor from 16.11.2017 to 30.09.2023) and Annexure-C (OTS letter dated 23.11.2022 sent by the Corporate Debtor). The aforesaid additional documents were taken on record and the IA was allowed and disposed of by this Adjudicating Authority vide its Order dated 02.02.2024.

REJOINDER FILED BY THE FINANCIAL CREDITOR

7. The Financial Creditor vide Diary No. 8 dated 02.01.2024, also filed the rejoinder dated 27.12.2023, which was also taken on record vide this Adjudicating Authority Order dated 02.02.2024. The submissions made in the rejoinder by the Financial Creditor are summarised below:

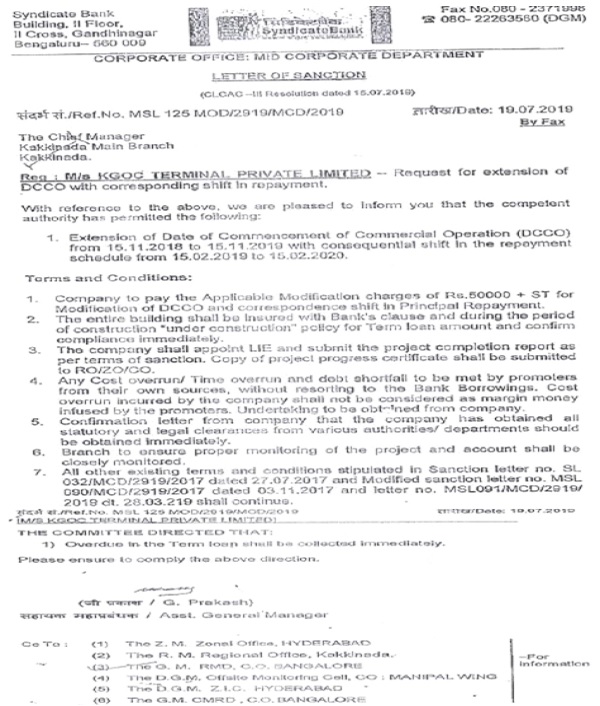

(i) The project was required to achieve date of commencement of commercial operation (hereinafter referred to as the “DCCO”) by 15.11.2018. However, at the request of Corporate Debtor vide letter No. MSL 124 MOD/2919/MCD/2019 dated 19.07.2019, the Financial Creditor vide its letter dated 19.07.2019, permitted the extension of the DCCO from 15.11.2018 to 15.11.2020 with a consequential shift in the repayment schedule from 15.02.2019 to 15.02.2020.

(ii) Consequently, the first instalment of Rs.1,23,00,000/- along with interest became due on 15.02.2020. The Corporate Debtor failed to service interest regularly from 31.05.2019 and defaulted on principal repayments from 15.02.2020 onwards.

(iii) Therefore, the alleged default does not fall within the COVID-19 suspension period contemplated under Section 10A of the Code.

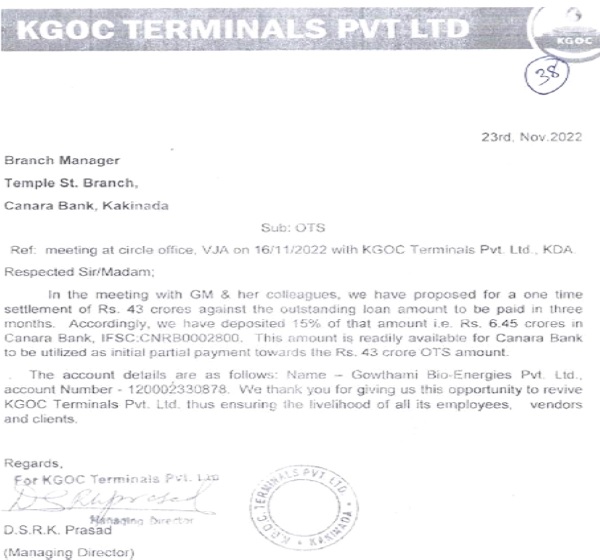

(iv) Further, an OTS proposal dated 23.11.2022 was submitted by the Corporate Debtor, which was ultimately rejected by the Financial Creditor.

(v) The aforesaid OTS proposal is a valid and legitimate acknowledgment of debt by the Corporate Debtor.

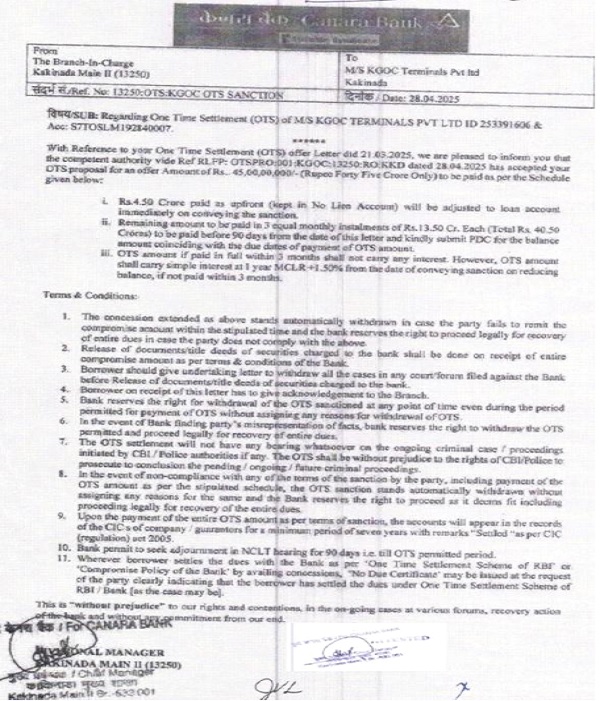

8. During the course of hearing dated 29.04.2025, the Corporate Debtor submitted that the OTS proposed by the Corporate Debtor has been accepted by the Financial Creditor vide OTS sanction letter dated 28.04.2025 and also screen shared the same. However, there was no representation on behalf of the Financial Creditor and therefore, the Corporate Debtor was directed to file the copy of the aforesaid OTS sanction letter along with the proof of payment of upfront amount made by the Corporate Debtor, with a further direction to communicate the order to the Financial Creditor for their appearance on the next date of hearing.

9. During the course of next hearing dated 07.05.2025, the Financial Creditor submitted that in view of the OTS sanctioned on 28.04.2025, the Corporate Debtor has paid an upfront amount of Rs.4.5 Crores and sought permission to withdraw the Petition with a liberty to file a fresh Petition, if the Corporate Debtor fails to comply the terms and conditions of the above OTS sanction letter. Accordingly, the CP 16/2023 was dismissed as withdrawn vide this Adjudicating Authority Order dated 07.05.2025 with the liberty to file a fresh Company Petition to the Financial Creditor, if the Corporate Debtor fails to comply the terms and conditions of the above OTS sanction letter.

10. Thereafter, the Financial Creditor vide Diary No. 2553 dated 26.12.2025, filed an application bearing Restoration Application (IBC)/2/2026 under Section 60(5) of the IBC read with Rule 11 of the National Company Law Tribunal Rules, 2016 (hereinafter referred to as the “NCLT Rules”) seeking to restore the CP 16/2023 on the following grounds:

(i) The Canara Bank had approved the OTS proposal of Corporate debtor on 28.4.2025 on payment of upfront amount of Rs. 4.50 crores and the balance amount accepted by the Corporate debtor amounting to Rs.40.50 crores was payable in 90 days by the Corporate debtor as per the OTS Sanction starting from 30.5.2025.

(ii) In view of the above settlement, the Financial Creditor in the hearing dated 7.5.2025 before this Adjudicating Authority informed that the Financial Creditor wanted to withdraw the CP 16/2023 against the Corporate Debtor and requested to give liberty to reopen the same in case of failure or non-compliance of terms and conditions of OTS sanction, which was recorded by this Adjudicating Authority vide Order dated 7.5.2025.

(iii) The instalment payable on 30.5.2025 was not paid by the Corporate Debtor and hence, the Financial Creditor decided to file restoration of CP 16/2023 and continue the legal process.

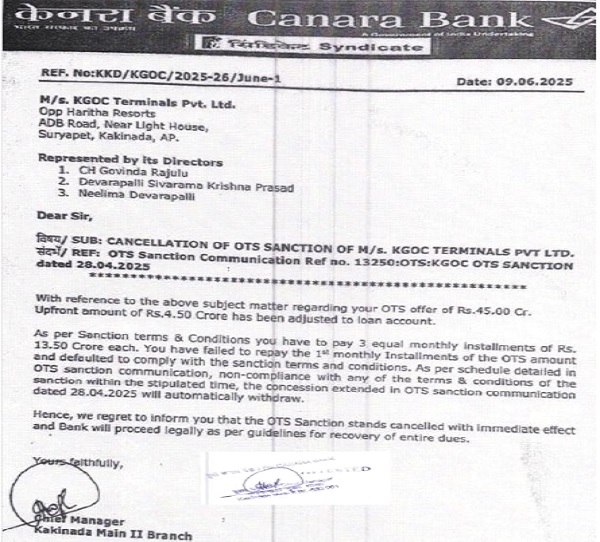

(iv) The Financial Creditor also sent mail to the Corporate Debtor regarding failure of the OTS and rejection/ cancellation of the same, but the Corporate Debtor failed to respond to the same.

11. This Adjudicating Authority vide its Order dated 28.04.2026, allowed the Restoration Application, in view of the liberty granted to the Financial Creditor in CP 16/2023 vide its Order dated 07.05.2025, and restored the CP 16/2023 to file.

12. Upon restoration of CP 16/2023, it was renumbered as Revised Company Petition (IBC)/1/7/AMR/2026 (hereinafter referred to as the “RCP 1/2026”)

13. In the first hearing dated 28.04.2026 after restoration of the CP 16/2023, the Financial Creditor submitted that the Corporate Debtor had already filed its reply in the CP 16/2023 prior to its withdrawal and Mr. Sunil Kumar, the Counsel appearing on behalf of the Corporate Debtor took notice and sought time to file Vakalat.

14. During the course of hearing dated 11.05.2026, Ms. Sowmya, Counsel appearing for the Corporate Debtor sought and was granted one week time to file the Vakalat and thereafter another one week time to file the reply and in the event, the Counsel of the Corporate Debtor fails to file the Vakalath or reply within the above time, the right to file the reply will be forfeited.

15. During the course of hearing dated 05.06.2026, the Counsels for both the Parties were heard and the RCP 1/2026 was reserved for orders.

ANALYSIS AND FINDINGS:

16. We have heard the submissions of the Counsel for the Financial Creditor and the Counsel for the Corporate Debtor and perused the records carefully.

17. The first issue for consideration before us is “Whether the Petition has been filed within the limitation period.”

(i) As per Part-IV of Form 1 enclosed with the Petition, the date of default is stated to be 01.12.2020, being the date on which the loan account of the Corporate Debtor was classified as NPA. However, in terms of the additional documents taken on record vide this Adjudicating Authority Order in IA 1/2024, the date of default works out to 15.02.2020.

(ii) On perusal of the records, it is noted that the CP 16/2023 was e-filed on 24.02.2023 and physically filed vide Diary No.1901 dated 14.03.2023, which is beyond the period of 3 years from the date of default.

(iii) However, it is noted that the Corporate Debtor acknowledging its liability towards the Financial Creditor submitted an OTS proposal dated 23.11.2022 to the Financial Creditor, which is reproduced below:

(iv) Therefore, the OTS proposal dated 23.11.2022 would amount to acknowledgement of the financial debt on 23.11.2022 and fresh limitation would again start from 23.11.2022.

(v) It is further noted that based on the Corporate Debtor’s letter dated 03.2025, the Financial Creditor vide its letter dated 28.04.2025 sanctioned the OTS, which has been accepted by the Corporate Debtor on the same date. The above OTS sanction letter is reproduced below:

(vi) Therefore, the OTS offer letter dated 21.03.2025 by the Corporate Debtor and its sanction by the Financial Creditor would amount to acknowledgement of the financial debt and fresh limitation would again start.

(vii) The Corporate Debtor failed to comply the terms and conditions of the above OTS sanction letter and the Financial Creditor cancelled the OTS vide its letter dated 09.06.2025, which is reproduced below:

(viii) Thereafter, in terms of the liberty granted by this Adjudicating Authority vide its Order dated 07.05.2025 in CP 16/2023, the Financial Creditor vide Diary No. 2553 dated 26.12.2025, filed Restoration Application, well within three years of cancellation of the OTS.

(ix) In view of the above, we are of the considered view that both CP 16/2023 as well as Restoration Application were filed within the limitation period.

18. The next issue for consideration before us “Whether the default period falls under exclusion period under Section 10A of the Code.”

(i) The main objection of the Corporate Debtor is that the date of default mentioned in the Petition is 01.12.2020, which falls within the suspension period prescribed under Section 10A of the IBC.

(ii) The material on record establishes that the Financial Creditor sanctioned a term loan of Rs.44.21 Crores vide sanction letter dated 27.07.2017. As per the sanction terms, the loan is to be repaid in 36 Quarterly instalments commencing after the moratorium period of 12 months starting from the date of first release and the interest is to be paid as and when debited to the Account. The relevant extract of sanction letter dated 27.07.2017 is reproduced below:

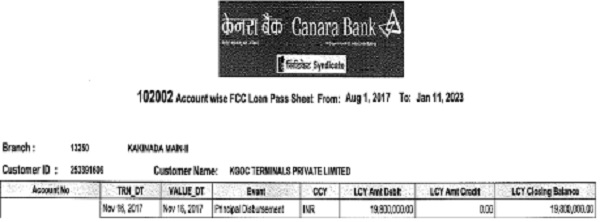

(iii) The Financial Creditor made the first disbursement amount of Rs.1,98,00,000/- to the Corporate Debtor on 16.11.2017. The Statement of Account of the Corporate Debtor for the period 01.08.2017 to 11.01.2023 reflecting the said disbursement is reproduced below:

(iv) Therefore, as per the terms of the sanction letter, the first instalment becomes due on 15.02.2019. However, at the request of the Corporate Debtor the DCCO was extended by the Financial Creditor, vide letter dated 19.07.2019, and consequently the repayment schedule stood shifted to 15.02.2020. The extract of the letter dated 19.07.2019 is reproduced below:

(v) Pursuant to the shift in repayment schedule from 15.02.2019 to 15.02.2020, the Financial Creditor in its rejoinder has clarified that the installment of Rs.1,23,00,000/- together with interest became due on 15.02.2020 and that the Corporate Debtor had failed to service the interest itself regularly from 31.05.2019 and defaulted in payment of principal installments from 15.02.2020 onwards, which is before the Section 10A period.

(vi) The Hon’ble Supreme Court in Laxmi Pat Surana vs. Union Bank of India (2021) 8 SCC 481 held that ‘default’ is non-payment of debt, when whole or any part of the debt becomes due and payable and is not paid.

(vii) Therefore, merely because the account was classified as NPA on 01.12.2020, the same cannot obliterate the earlier defaults, which had already occurred prior to the commencement of the suspension period under Section 10A. The material on record clearly demonstrates that default had commenced much prior to 25.03.2020 and continued thereafter. Consequently, the protection under Section 10A is not available to the Corporate Debtor. The Hon’ble Supreme Court in Ramesh Kymal vs. Siemens Gamesa Renewable Power Pvt. Ltd. (2021) 3 SCC 224 held that Section 10A bars initiation of CIRP only in respect of defaults occurring during the protected period. Where default had occurred prior thereto, the bar is inapplicable.

(v) Furthermore, even after OTS sanctioned by the Financial Creditor vide its letter dated 28.04.2025, the Corporate Debtor again failed to pay the instalment payable on 30.5.2025.

(viii) In view of the above, we are of the considered view that default period does not fall under exclusion period under Section 10A of the Code.

19. The next issue for consideration before us is “Whether there is a financial debt and default in repayment thereof, when it became due and payable, which meets the minimum threshold limit of Rupees One crore as required under Section 4 of the IBC, 2016?”

(i) As per Part-IV of Form 1 enclosed with the Application, the amount claimed to be in default is Rs.64,69,67,514.74 as on 01.12.2020,.

(ii) At Part-V of Form-1, the Financial Creditor, as evidences of default of the financial debt, has enclosed the Sanction Letter dated 27.07.2017, Statement of Account of the Corporate Debtor showing the disbursements along with Certificates issued under Section 2(A)(a), Section 2(A)(b) and Section 2(A)(c) of the Bankers’ Books Evidence Act, 1891 (as amended) and CRILC report.

(iii) Although, the Corporate Debtor in its Counter had denied the alleged claim of Rs.64,69,57,514.47 or any interest, the OTS proposal dated 23.11.2022 submitted by the Corporate Debtor itself constitutes a clear acknowledgment of liability, wherein the Corporate Debtor had proposed a OTS of Rs.43 Crores against the outstanding loan amount to be paid in three months and also deposited 15% of that amount i.e. Rs.6.45 Crores with the Canara Bank.

(iv) Further, it is submitted by the Financial Creditor that against OTS sanction letter dated 28.04.2025, the balance amount payable is Rs.40.50 crores in 90 days starting from 30.05.2025 and even the first instalment payable on 30.05.2025 has not been paid by the Corporate Debtor.

(v) The Corporate Debtor not filed any proof with regard to the payment of remaining OTS amount.

(vi) In view of the aforesaid discussions, we are of the considered view that there is a financial debt extended by the Financial Creditor to the Corporate Debtor and there is a default in repayment thereof, when it became due and payable and the default exceeds the minimum threshold of Rupees One Crore.

20. However, before admission, this Adjudicating Authority has to satisfy that the Petition is complete and there are no disciplinary proceedings pending against the proposed IRP.

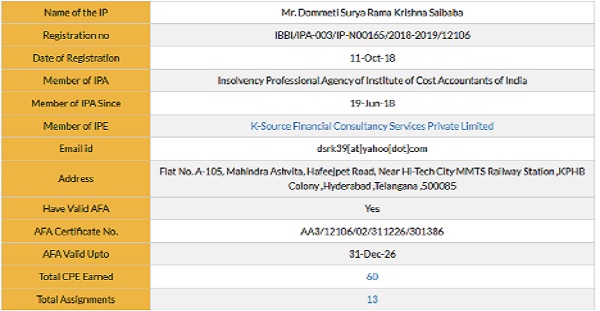

21. We have gone through the contents of the Petition filed by the Financial Creditor and found that the same is complete. The Financial Creditor has proposed the name of Mr. Dommeti Surya Rama Krishna Saibaba, having Registration No. IBBI/IPA-003/IP-N000165/2018-2019/12106 as IRP in this matter. The written consent of the proposed IRP in Form 2 dated 13.02.2023 affirming that he is eligible to be appointed as IRP in respect of the Corporate Debtor and certificate that there are no disciplinary proceedings pending against him with the Board or the Insolvency Professional Agency of Institute of Cost Accounts of India, is at page 34 & 35 of the Application. The credentials of the proposed IRP have been verified on the IBBI website, which shows that the proposed IRP holds the valid AFA up to 31.12.2026. The relevant extract of the IBBI website is given below:

22. As a sequel to the discussion above, the present Petition bearing RCP (IBC)/1/7/AMR/2026 (Old Case CP(IB)/16/7/AMR/2023) filed by the Financial Creditor under Section 7 of the IBC for initiating the CIRP against the Corporate Debtor, namely, KGOC Terminals Private Limited is hereby admitted and accordingly, the Moratorium is declared in terms of Section 14 of the Code.

23. We also appoint Mr. Dommeti Surya Rama Krishna Saibaba, having Registration No. IBBI/IPA-003/IP-N000165/2018-2019/ 12106, email ID: dsrk39@yahoo.com having registered address at Flat No.A-105, Mahindra Ashvita, Hafeejpet Road, Near Hi-Tech City MMTS Railway Station, KPHB Colony, Hyderabad-500085, Telangana, as IRP in the instant matter, who shall perform the duties in accordance with the Code, IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (hereinafter referred to as the ‘CIRP Regulations’) and other applicable laws, as amended from time to time.

24. The Financial Creditor is directed to deposit 5,00,000/- (Rupees Five Lakhs only) with the IRP to meet the expense to perform the functions assigned to him in accordance with Regulation 6 of the CIRP Regulations. The amount, however, will be subject to adjustment by the Committee of Creditors as to be duly accounted for by IRP and shall be paid back to the Financial Creditor.

25. A copy of this Order shall immediately be communicated to the Financial Creditor, the Corporate Debtor, IBBI, and the IRP named above by the Court Officer/ Registry of this Adjudicating Authority.

26. Accordingly, RCP (IBC)/1/7/AMR/2026 [Old Case CP (IB)/16/7/ AMR/2023] stands admitted.

Author Bio