Case Law Details

CAPT Vs Spicejet Private Limited (NCLT Delhi)

The National Company Law Tribunal (NCLT), Delhi, dismissed a Section 9 application filed by an employee seeking initiation of the Corporate Insolvency Resolution Process (CIRP) against SpiceJet Limited for alleged unpaid employment dues of ₹1,13,56,444 along with interest of ₹56,78,222, aggregating to ₹1,70,34,666.

The Operational Creditor submitted that he was appointed as a Trainee Captain in April 2019 and claimed that substantial salary dues for the period from April 2020 to August 2022 remained unpaid despite repeated requests and a demand notice issued under the Insolvency and Bankruptcy Code (IBC).

The Corporate Debtor challenged the maintainability of the application. It contended that a substantial portion of the claim related to the period from April 2020 to March 2021, which fell within the period protected under Section 10A of the IBC. Excluding that amount reduced the alleged default below the statutory threshold of ₹1 crore. It also argued that there was no agreement for payment of interest, that the employment contract had been replaced by revised terms accepted by the employee in 2020, and that the claim was subject to a pre-existing dispute regarding salary calculations and full and final settlement.

The Tribunal first held that employment dues fall within the definition of “operational debt” under Section 5(21) of the IBC and can form the basis of a petition under Section 9.

However, it found that the amount claimed for the period from April 2020 to March 2021 could not be considered because Section 10A bars initiation of CIRP for defaults arising during the specified COVID-19 suspension period. Consequently, the claim of ₹47,52,918 for that period was excluded while computing the threshold under Section 4 of the IBC.

The Tribunal also rejected the claim for interest of ₹56,78,222, observing that no agreement providing for payment of interest had been produced. Relying on decisions of the National Company Law Appellate Tribunal (NCLAT), it held that, in the absence of an agreement or acknowledgment, interest could not be added for the purpose of meeting the statutory threshold under the IBC.

On the issue of maintainability, the Tribunal found that a pre-existing dispute existed between the parties regarding the quantum of employment dues. It noted that the Corporate Debtor had consistently disputed the amount claimed, relied on revised employment terms accepted by the employee, referred to a full and final settlement proposal, and denied any further liability. Email exchanges placed on record also demonstrated disagreement regarding the amount payable. The Tribunal observed that such disputes concerning employment dues could not be adjudicated in insolvency proceedings and referred to the Supreme Court’s decision in GLS Films Industries Private Limited v. Chemical Suppliers India Private Limited, which reiterated that the adjudicating authority only needs to determine the existence of a plausible pre-existing dispute.

The Tribunal concluded that: (i) the claim relating to the Section 10A period could not be counted for the threshold requirement; (ii) the interest claim could not be included in the absence of any agreement; and (iii) a pre-existing dispute regarding the employment dues existed before issuance of the Section 8 demand notice. As a result, the alleged default fell below the threshold prescribed under Section 4 of the IBC, and the application was also barred by the existence of a pre-existing dispute. Accordingly, the Section 9 application seeking initiation of CIRP was dismissed.

FULL TEXT OF THE NCLT JUDGMENT/ORDER

1. The present application is filed on 24.02.2025 by Capt. Devesh Bbyan (herein-after referred as Corporate Applicant) against the Respondent M/s Spicejet Limited (hereinafter referred to as Corporate Debtor”) under Section 9 of the Insolvency and Bankruptcy Code, 2016 (hereinafter referred to as “IBC 2016”) read with Rule 6 of the Insolvency and Bankruptcy (Application to Adjudicating Authority) Rules, 2016 (hereinafter referred to as “IB (AAA) Rules, 2016”) for initiation of Corporate Insolvency Resolution Process (CIRP).

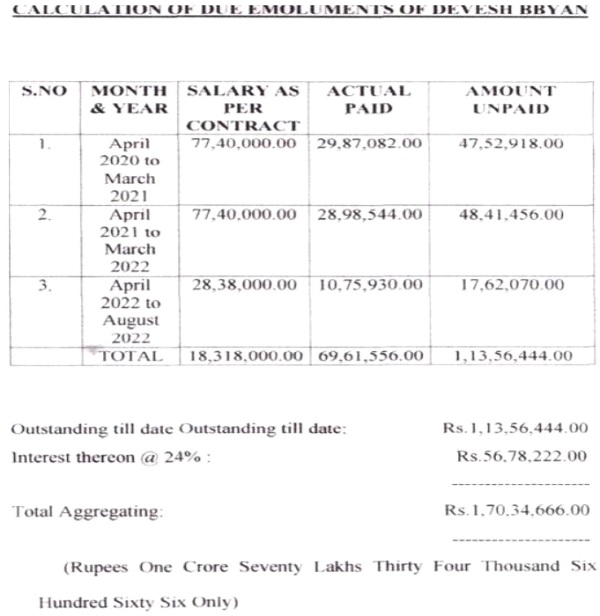

2. It is the submissions of the Petitioner(s), that the present Petition has been filed with respect to the ‘default’ committed by the Corporate Debtor in paying the ’employment dues’ amounting to Rs. 1,13,56,444.00 (Rupees One Crore Thirteen Lakhs Fifty Six Thousand Four Hundred Forty Four only) plus Interest thereon @ 24% per annum (Rs. 56,78,222/- + 1,13,56,444/-), total aggregating to Rs.1,70,34,666.00 (hereinafter referred to as “Operational Debt’).

3. Advocate Mr. Amit Punj appeared on behalf of Corporate Debtor on the basis of advance service of the Petition and raised issue of maintainability of the present Petition. During the course of hearing on 06.03.2025, Ld. Counsel for the Petitioner sought time to examine the issue specifically in respect of applicability of Section 10A in respect of certain claim amount and also to the limitation issue. The arguments of both sides on maintainability of the Petition were heard on 09.09.2025. Both the sides were directed to file their written submissions on the issue of maintainability. Although, written submissions on behalf of Corporate Debtor have been placed on record, however, no written submissions have been filed by the Operational Creditor.

Submissions of the Operational Creditor –

4. In brief the facts of the matter and law as submitted by the Operational Creditor in the Company Petition and Oral arguments are as under: –

4.1 The Operational Creditor was offered the position of Trainee Captain Q400 in the Flight Operations Department in the Corporate Debtor Company as per Offer letter dated 19.04.2019 which position was offered at an annual compensation of Rs.7,740,000.00 (Rupees Seventy-Seven Lakhs Fourty Thousand Only) per annum i.e. Rs.6,45,000.00 (Rupees Six Lakhs Fourty Five Thousand Only) per month. Upon the acceptance of the said offer, the Operational Creditor was appointed on the said position as per the letter of appointment dated 23.04.2019.

4.2 The Operational Creditor had joined the employment/services of the Corporate Debtor and for his due services so rendered to the Corporate Debtor during the period April 2020 to March 2021, April 2021 to March 2022, April 2022 to August 2022. An aggregate sum of Rs. 1,83,18,000.00 (Rupees One Crore Eighty Three Lakhs Eighteen Thousand Only) falls due out of which the Corporate Debtor had paid only Rs.69,61,556.00 (Rupees Sixty Nine Lakhs Sixty One Thousand Five Hundred Fifty Six Only) to the Operational Creditor leaving a balance due of Rs.1,13,56,444.00 (Rupees One Crore Thirteen Lakhs Fifty Six Thousand Four Hundred Fourty Four Only) which was not being paid by the Operational Creditor in spite of repeated requests and demands.

4.3 Since the Corporate Debtor did not pay the abovesaid dues so claimed time and again in spite of e-mail correspondence so exchanged between the parties. The Corporate Debtor had even tried to force their own settlement upon the Operational Creditor by suppressing and withholding the legitimate dues of the Operational Creditor. Thereafter, the Operational creditor also issued the notice of demand dated 03.10.2024 under Rule 5 of Insolvency and Bankruptcy Code to the Corporate Debtor. The Corporate Debtor rather honouring the said demand so made by the Operational Creditor had got issued a false and baseless reply to the said notice of demand without any basis.

Submissions of the Corporate Debtor –

5. The Corporate Debtor has filed Brief Synopsis and Written Submissions on the maintainability of the Petition. In brief its submissions are as under:

5.1 As per the Offer letter dated 19.04.2019, the Petitioners was entitled to compensation as per attached Annexure-1 with the said letter. The said Annexure show that except basic salary of Rs. 1,30,000/- per month, all the components are variables.

5.2 The Operational Creditor has filed calculation of amount dues as Annexure-4 with the Petition. A bare perusal of Annexure-4 reveals that the Petitioner has also claimed a sum of Rs. 47,52,918/- payable from April, 2020 to March, 2021 i.e. for the period covered under Section 10A. If this amount is excluded from the total purportedly payable amount of Rs. 1,13,56,444.00, the alleged payable amount is reduced to Rs. 66,03,526/-, which is much below the threshold limit of Rs. 1.00 Crores. Further, there was no contract of payment of any interest by the Respondent/CD to the Petitioner on the purported deferred salaries and as such, the Petitioner cannot levy any interest on the purported payments.

5.3 No acknowledgement of debt and “Operational Debt” exists under IBC. There is not even a single document, filed by the Petitioners, which even prima facie shows that the alleged amount claimed by the Petitioners was ever acknowledged by the Respondent at any point of time. No Salary Slips/Invoices for the claimed amount were ever issued to the Petitioner. Rather, salary slips were issued for the amounts payable to them, post novation of contract and entire salary had been remitted as per the same.

5.4 Even in the reply to the statutory notice, the Respondent has denied payment of the said amounts and has raised substantial and disputed questions of facts, which cannot be adjudicated in the summary proceedings before this Tribunal.

5.5 The original employment contracts were replaced by new “Transitionary

Terms” introduced in 2020. The petitioners accepted the new compensation structure by signing the Google form in June 2020. As per the request of the Petitioner, Full and Final settlement of the Petitioner was done and he was informed of the FnF amount of Rs. 3,95,613/ – vide e-mail dated 10.11.2023. Vide email dated 12.01.2024, the Petitioner raised certain concerns and demanded some additional amount, not as per the old salary but as per the new novated contract. If the said alleged claims are calculated in toto, the amount would be less than Rs. 40.00 lacs.

5.6 Claims are rooted in a pre-existing dispute regarding salary calculations, which makes the initiation of insolvency proceedings inappropriate under the IBC. The Petitioners have accepted the revised salary regime and they have been working with the CD, without any protest and demur. The same is clear and apparent by the e-mails exchanged between the parties.

ANALYSIS

6. We have considered the submissions made by Ld. Counsel on behalf of the Operational Creditor and Ld. Counsel on behalf of Respondent/ Corporate Debtor. We have perused the pleadings and documents filed by both the sides and also considered Written Submissions filed by the Corporate Debtor.

Whether Employment dues can be considered as ‘Operational Debt’?

7. The Corporate Debtor has raised an issue that employment dues are not ‘Operational Debt’, and one Petition cannot be filed by two employees therefore, present Petition is not maintainable.

8. Operational debt is defined under Section 5(21) of the IBC, which is as follows:

“5. In this Part, unless the context otherwise requires,—

(21) “operational debt” means a claim in respect of the provision of goods or services including employment or a debt in respect of the payment] of dues arising under any law for the time being in force and payable to the Central Government, any State Government or any local authority;”

Thus, as per the definition of ‘Operational Debt’ claim in respect of employment dues fall within the category of ‘Operational Debt’, therefore Petition under Section 9 IBC can be filed for employment dues.

Claim for Section 10A IBC period-

9. The Corporate Debtor in their written submissions has referred to the Annexure-4 filed by the Petitioner which is stated to be calculation of due emoluments. The Corporate Debtor has submitted that the same reveals that the Petitioner has also claimed a sum of Rs. 47,52,918/- payable from April, 2020 to March, 2021 i.e. for the period covered under Section 10A. If this amount is excluded from the total purportedly payable amount of Rs. 1,13,56,444.00, the alleged payable amount is reduced to Rs. 66,03,526/-, which is much below the threshold limit of Rs. 1.00 Crores. We may extract Annexure-4:

10. On perusal of the above calculation sheet, as filed by the Petitioner, it emerges that the Petitioner has claimed default of Rs. 47,52,918/- for the period April 2020 to March 2021. The Section 10A of the IBC, bars initiation of CIRP for the default arising during 25.03.2020 to 24.03.2021. The Section 10A reads as follows:

“10A. Suspension of initiation of corporate insolvency resolution process.— Notwithstanding anything contained in sections 7,9 and 10, no application for initiation of corporate insolvency resolution process of a corporate debtor shall be filed, for any default arising on or after 25th March, 2020 for a period of six months or such further period, not exceeding one year from such date, as may be notified in this behalf: Provided that no application shall ever be filed for initiation of corporate insolvency resolution process of a corporate debtor for the said default occurring during the said period. Explanation – For the removal of doubts, it is hereby clarified that the provisions of this section shall not apply to any default committed under the said sections before 25th March, 2020.”

11. The Hon’ble Supreme Court in Ramesh Kymal Vs M/s Siemens Gamesa Renewable Power Pvt Ltd. Civil Appeal No. 4050 of 2020 in their judgment dated 09.02.2021 examined the scope of Section 10A and observed as under:

“23. Adopting the construction which has been suggested by the appellant would defeat the object and intent underlying the insertion of Section 10A. The onset of the Covid-19 pandemic is a cataclysmic event which has serious repercussions on the financial health of corporate enterprises. The Ordinance and the Amending Act enacted by Parliament, adopt 25 March 2020 as the cut-off date. The proviso to Section 10A stipulates that “no application shall ever be filed” for the initiation of the CIRP ‘for the said default occurring during the said period”. The expression “shall ever be filed” is a clear indicator that the intent of the legislature is to bar the institution of any application for the commencement of the CIRP in respect of a default which has occurred on or after 25 March 2020 for a period of six months, extendable up to one year as notified.”

12. In view of above, amount of default of Rs. 47,52,918/- for the period April 2020 to March 2021 may not be considered for the purpose of threshold of Rs 1 crore for filing Petition under IBC.

Entitlement of interest amount claimed –

13. The Operational Creditor has claimed an amount of Rs. 56,78,222/- as interest @ 24% per annum. No agreement between the Operational Creditor and Corporate Debtor for claiming interest amount has been brought on record. The Hon’ble NCLAT in the case of Rishabh Infra Vs. Sadbhav Engineering Ltd., CA (AT) (Ins.) No. 1881 of 2024 has held that the Operational Creditor cannot add interest with the principal amount on the basis of unilaterally raised invoices in the absence of any agreement for interest admission of interest by the CD or any other document. In Shitanshu Bipin Vora Vs. Sh. Haree Yarns Pvt. Ltd., CA (AT) (Ins.) No. 2204 of 2024, Hon’ble NCLAT has held that without there being any agreement for interest, obligation of payment of interest on the basis of the condition in the invoice cannot be accepted. Therefore, in absence of any agreement, Operational Creditor is not entitled to claim Interest amount of Rs. 56,78,222/- for the purpose of threshold of Rs. 1 (One) Crore as provided in Section 4 of the IBC.

Whether pre-existing dispute exists-

14. The Corporate Debtor has not disputed the relationship of employer and employee between the Operational Creditor and the Corporate Debtor. However, the Corporate Debtor has raised an issue of pre-existing dispute. The Corporate Debtor in their reply to Section 8 notice has stated as under:

“k) You, by showing the aforesaid poor and below standard performance, also breached/flouted clauses 3.1; 3.3; 16 and 16.1 of the Letter of Appointment dated 23.04.2019 which resulted in terminating the services of yours, by my client, vide Termination Letter dated 12.08.2022.

1) You were called upon to report to my client’s HR Team, for your full and final settlement and obtaining the No dues Certificate after complying with all requisite formalities. You, however never reported to my client for completing the aforesaid formalities. It is however stated that that as communicated to you, vide various e-mails, sent by my client, a sum of Rs. 3,95,613/ – (Rupees Three Lacs Ninety Five thousand Six Hundred thirteen only) was payable by my client to you as full and final settlement of dues, till the date you worked with my client and my client is ready and willing to release to you, subject, however to fulfilment of all the procedural formalities and signing of relevant documents by you, as already communicated to by my client.”

Moreover, after March 2020, when Covid-affected normalcy of life as well as commercial services worldwide, my client requested all its employees to accept the revised terms and conditions of the employment including revision in the salary Structure. You while tendering your acceptance of the google form, clearly indicated that you are ready and willing to work in conformity with the revised terms and conditions and are also agreeable to take the revised salary. You confirmed that “I refer to the Revised Pilot Contract sent to me vide e-mail dated 17 June 2020 and I hereby consent to the same with the request to roster me to the flight schedule in accordance with the Operational requirements of the company.” This clearly proves that there was a novation in the contract, which you expressly agreed. It is also a matter of fact that after revision of the contract, you were paid the salary in terms of the fresh/ new contract. There is no amount, due and/or payable by my client to you, on any account, whatsoever. As such, no amount as alleged in your legal notice, or otherwise, is due or payable by my client to you on any account, whatsoever. Without prejudice to the aforesaid contentions of my client that no amount, on any account, whatsoever, is due or payable by my client to you, it is stated that most of the claims, as put forth by you by way of your legal notice under reply, are barred by limitation.”

15. The Operational Creditor in their Petition has not refuted the contentions raised by the Corporate Debtor in their reply to Section 8 notice. No separate affidavit in terms of Section 9(3)(b) of the Code has been placed on record. The email exchanges between the parties, as filed by the Petitioner indicate that there was an issue of total amount due. The Corporate Debtor vide email dated 08.11.2022 has informed the Operational Creditor as under:

“Dear Capt. Bbyan,

Please find attached the full and final settlement sheet. You are requested to send accepted undertaking which is attached. Post that we will release the amount’

Thanks and Regards’

Ashok Samanta

Human Resources

Email: ashok.samanta@gpleeiet.com“

16. On 10.11.2023, the Corporate Debtor send an email to the Operational Creditor

Dear Capt. Bbyan,

Request to send the filled and signed attached undertaking.

Total amount is 395613.

F&F amount is 213133 and OT is 182480.

Thanks and Regards,

Ashok Samanta

17. These emails indicate that there is dispute between Operational Creditor and Corporate Debtor in respect of quantum of employment dues. These disputes about employment dues amount cannot be adjudicated in the IBC proceedings.

18. Recently, Hon’ble Supreme Court in the case of GLS Films Industries Private Limited vs Chemical Suppliers India Private Limited, Civil Appeal No. 4019 of 2025 decided on 09.04.2026 has considered the issue of pre-existing dispute in Section 9 IBC Petition in the light of law laid down in Mobilox Innovations Private Limited vs. Kirusa Software Private Limited (2018) 1 SCC 353, S.S. Engineers vs. Hindustan Petroleum Corporation Limited and others (2022) 234 COMP CAS 95, and Sabarmati Gas Limited vs. Shah Alloys Limited (2023) 3 SCC 229 has observed as under:

“21. Given the obtaining facts and the aforestated settled legal position, it was not for the NCLAT to delve into the appellant’s dispute to decide whether it had actual merit. All that is required is for the adjudicating authority to satisfy itself as to the existence of a plausible pre-existing dispute, which was not spurious, hypothetical or illusory. Whether the party raising that dispute would succeed on the strength thereof is not within the ken of such inquiry. That being so, we are of the opinion that the NCLT was correct in concluding that the application filed by the respondent under Section 9 of the Code did not merit consideration, owing to pre-existing disputes. The NCLAT was not justified in reversing the said decision. There was clearly no consensus between the parties as to who was liable to pay to the other and the amount that was payable.”

19. In view of above discussion, we have found that (i) amount of default of Rs. 47,52,918/- for the period April 2020 to March 2021 may not be considered for the purpose of threshold of Rs 1 crore for filing Petition under IBC (ii) Operational Creditor is not entitled to claim Interest amount of Rs. 56,78,222/- for the purpose of threshold of Rs. one crore as provided in Section 4 IBC. Therefore alleged defaulted amount is below threshold of Rs One crore as provided in Section 4 of the IBC, (iii) there exists pre-existing dispute between the Operational Creditor and the Corporate Debtor in respect of amount of employment dues. These dispute exists prior to Section 8 notice. Therefore, the present Section 9 application is not admissible on the ground of lack of threshold under Section 4 IBC and also on existence of pre-existing dispute between the parties.

20. In the light of the above, the instant application bearing CP (IB) No. 148/ND/2025 filed by, Capt. Devesh Bbyan (Operational Creditor), under Section 9 of the Code read with Rule 6(1) of the Insolvency 85 Bankruptcy (Application to Adjudicating Authority) Rules, 2016 for initiating CIRP against M/s Spicejet Limited is liable to be dismissed and is, accordingly dismissed.

Let a copy of the order be served to the parties.

Author Bio