1. Introduction Paragraph :-

The main issue arising is that the payment to the supplier is made beyond 180 days from the date of issue of invoice in cases where retention is made for more than 180 days. Such kind of retentions are common in the construction and infrastructure related industry and in contracts involving supply of goods as well as services.

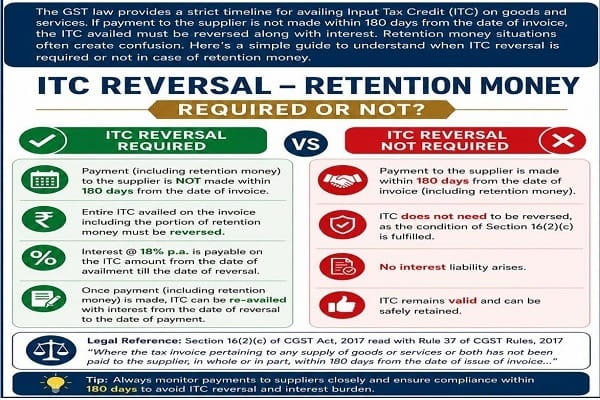

Treatment of retention under GST Act is going to be very crucial for construction industry. Work process of construction industry is always complex & continuous supply of service. The outcome of said contract is measurable only after completion of certain activities/project. Due to its long term nature, retention withheld is inevitable and part & parcel of construction industry. ITC on retention money is required to be reversed in the case of non-payment of consideration within 180 days as per sec 16(2) of CGST Act, 2017.

2. Purpose of Retention Money :-

Retention money in real estate refers to a portion of the payment withheld by the buyer, developer, or contractee from the contractor/vendor until satisfactory completion of the project or defect liability period.

Its main purposes are:

(I) Ensures Quality of Work

(II) Security Against Defects

(III) Gurantees Completion of Pending Works

(IV) Protection Against Breach of Contracts

(V) Defect Liability Assurance

3. Legal Disputes on ITC reversal on Retention Money :-

The issue lies in a specifically in second proviso to Section 16(2) of the CGST Act, 2017 read with Rule 37 of CGST Rules, 2017. This part of the GST law comes into play when a tax payer fails to pay a supplier within 180 days from the date of invoice issued by the supplier.

Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of 180 days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed:

While third proviso to Section 16(2) of CGST Act, 2017 as stated below-

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Below is the bare text of Rule 37 of CGST Rules, 2017

Rule 37. Reversal of input tax credit in the case of non-payment of consideration.-

(1) A registered person, who has availed of input tax credit on any inward supply of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, but fails to pay to the supplier thereof, the amount towards the value of such supply whether wholly or partly, along with the tax payable thereon, within the time limit specified in the second proviso to sub-section(2) of section 16, shall pay or reverse an amount equal to the input tax credit availed in respect of such supply , proportionate to the amount not paid to the supplier, along with interest payable thereon under section 50, while furnishing the return in FORM GSTR-3B for the tax period immediately following the period of 180 days from the date of the issue of the invoice:

Provided that the value of supplies made without consideration as specified in Schedule I of the said Act shall be deemed to have been paid for the purposes of the second proviso to sub-section (2) of section 16:

Provided further that the value of supplies on account of any amount added in accordance with the provisions of clause (b) of sub-section (2) of section 15 shall be deemed to have been paid for the purposes of the second proviso to sub-section (2) of section 16.

(2) Where the said registered person subsequently makes the payment of the amount towards the value of such supply along with tax payable thereon to the supplier thereof, he shall be entitled to re-avail the input tax credit referred to in sub-rule (1)..

(4) The time limit specified in sub-section (4) of section 16 shall not apply to a claim for re-availing of any credit, in accordance with the provisions of the Act or the provisions of this Chapter, that had been reversed earlier.

4. Legal Aspects and View :-

On plain reading of Second Proviso to Section 16(2) read with Rule 37, it is to be highlighted that the both said proviso & rule uses the term- “fails to pay” rather than “does not pay”.

In this context, the argument put forth is that the provision for the reversal of credit becomes applicable specifically when the recipient fails to pay. This term “fails to pay” is linked to a specific incident where a payment was expected due to a contractualobligation.

- Since the right to claim payment in case of retention arises at the time of satisfaction of the condition as per the contract and not from the date of raising of the invoices, therefore the period of 180 days shall be calculated from the date when the payment of retention money becomes due and not from the date of invoice.

- Retention money has been withheld with the consent of the supplier and amount paid by recipient to the supplier is more than the entire tax amount of the entire invoice, therefore it should be treated that recipient has complied with the provision of payment to the supplier within 180 days of the issue of the invoice.

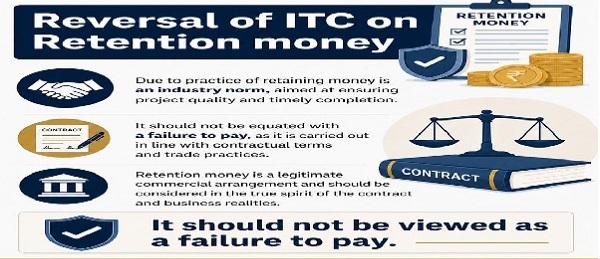

The core argument is that retention money, being a common practice in various industries, should not fall under the definition of “fails to pay.” This is because retention money is withheld in accordance with mutually agreed terms within the contract. Therefore, when a tax payer is not under any obligation to make a payment for retention money within the contractually stipulated 180-day period, it cannot be claimed that they failed to make a payment to the supplier.

Furthermore, it is emphasized that the second proviso to Section 16(2) of the CGST Act primarily serves as an anti-evasion measure within the law. The legislative intention behind introducing this provision was to ensure that suppliers, particularly those from the Micro, Small, and Medium Enterprises (MSME) sector, are paid in a prompt and timely manner.

Henceforth, the argument is that the language of the law and its intent do not align with the application of the second proviso to retention money situations where no obligation to pay exists. This argument seeks to clarify that the provision should be reserved for instances where there is a clear obligation to pay, as intended by the legislation, and not for cases involving retention money.

In support of above, Judgement of erstwhile laws can also relied upon which are squarely applicable in GST regime as well.

Anantnath Developers Vs. Commissioner of Central Tax 2018 ACR 83 CESTAT Mumbai wherein it is held that- “He also submitted that the retention of amount out of bill amount was for specific performance of contract. They are placing purchase order on their sub-contractors and take corresponding guarantee from the sub-contractors. The purchase order provides for 5% of retention of bill amount. That service tax amount is paid by them in full to the sub-contractors and only retention amount is retained. Further entire service tax was paid by the contractors to the government. Thus when service tax was paid in full, credit cannot be denied.”

The amount being retained be treated as deposit as once retained it loses the character of amount being retained for an invoice.

- Once an amount is retained, it is not for the particular invoice but as a deposit with the consent of the supplier wherein he has treated that the amount due towards the individual invoice has been paid but the deposit has been kept for the successful completion of the contract. That further when a claim is made by the supplier for payment of retention money, it is not with respect to the individual invoice but with respect to entire amount retained.

Second Proviso to Section 16(2) is illegal and ultra vires as it forces the buyer to reverse the credit for non-payment of consideration to supplier and government itself get unjustly enriched when both the parties have agreed to defer the payment and the supplier by exercising the right as vested under Section 63 of the Indian Contract Act, 1872 has waived off the right to receive the payment until a future date.

5. Concluding Remarks :-

Applicability of reversal of Input Tax Credit on retention money is not at all correct and the fact that right to receive has been waived off by the supplier should be treated as payment of consideration and recipient cannot be asked to do the impossible. In the alternative, it can be considered that the period of 180 days should start from the day when the retention money becomes due.

The practice of retaining money is an industry norm, aimed at ensuring project quality and timely completion. It should not be equated with a failure to pay, as it is carried out in line with contractual terms and trade practices.

*****

The author can be contacted at calokeshaggarwal52@gmail.com His mobile number is +91-8368353016.

DISCLAIMER : This publication serves as a general guide for informational purposes only. The references and content provided are for educational purposes and should not be considered as legal advice.

Author Bio

The interest issue covered very intelligently with legal footings .

Very much helpful in my case.

thanks

Thanks vimal ji.