1. Introduction :-

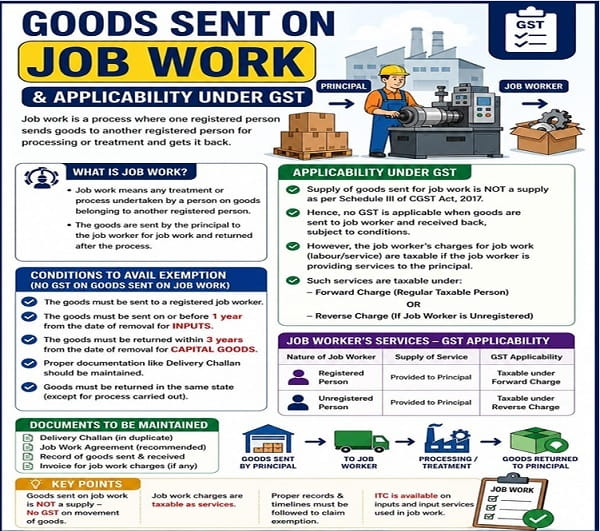

The definition of Job-work under GST is covered under section 2(68) of the CGST Act, 2017 states “Any treatment or process undertaken by a person on goods belonging to another registered person”. Therefore, a job worker is a person (registered or unregistered) who is processing or treating the goods of another registered person, and the owner of the goods is called the Principal in this respect. The GST ITC-04, one of the most significant compliance forms, is essential for tracking the flow of goods to and from job workers. Proper filing allows businesses to achieve supply chain transparency, reclaim Input Tax Credit (ITC) effortlessly, and avoid audit conflicts.

Form GST ITC-04 is a statement required to be filed by a Principal (registered person) who sends inputs or capital goods to a job worker without payment of GST under Section 143 of the CGST Act, 2017. It enables the GST department to track the movement of goods sent for job work and ensures compliance with the prescribed time limits.

2. Main Features of Job Work :-

The goods i.e inputs, semi-finished goods, or capital goods. Job work is a supply of service under GST.

The principal can supply goods to the job worker without charging GST by delivering a delivery challan.

3. Turnover-based filing frequency of ITC-04 :-

Annual Turnover Frequency Due Dates

- Above ₹5 crore- half-yearly (April to September, October–March) 25th October, 25th April

- Up to ₹5 crore annually, 25th April

4. Relevant Legal Provision :-

- Section 143 of the CGST Act, 2017 – Job work procedure.

- Section 19 of the CGST Act, 2017 – ITC on inputs and capital goods sent for job work.

- Rule 45 of the CGST Rules, 2017 – Conditions and filing of ITC-04.

5. Who is Responsible to file a ITC-04 form :-

The responsibility to file Form GST ITC-04 lies solely with the Principal (the registered person who sends goods for job work). The job worker is not required to file ITC-04, whether the job worker is registered under GST or not.

- A registered manufacturer sending raw materials or semi-finished goods to a job worker.

- A registered trader sending goods for activities such as packing, labeling, testing, or processing.

- Any registered person sending capital goods for repair, refurbishment, or other job work.

- A principal who sends goods directly from the supplier’s premises to the job worker.

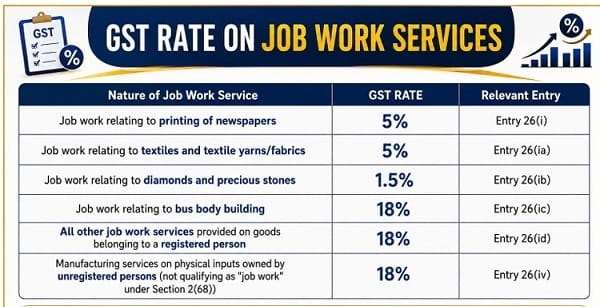

6. GST rate on Job work services :-

Under GST, the rate applicable to job work services depends on the nature of the job work and the type of goods on which the job work is performed. The rates are prescribed under Notification No. 11/2017-Central Tax (Rate), as amended.

| Nature of Job Work Service | GST RATE | Relevant Entry |

| Job work relating to printing of newspapers | 5% | Entry 26(i) |

| Job work relating to textiles and textile yarns/fabrics | 5% | Entry 26(ia) |

| Job work relating to diamonds and precious stones | 1.5% | Entry 26(ib) |

| Job work relating to bus body building | 18% | Entry 26(ic) |

| All other job work services provided on goods belonging to a registered person | 18% | Entry 26(id) |

| Manufacturing services on physical inputs owned by unregistered persons (not qualifying as “job work” under Section 2(68)) | 18% | Entry 26(iv) |

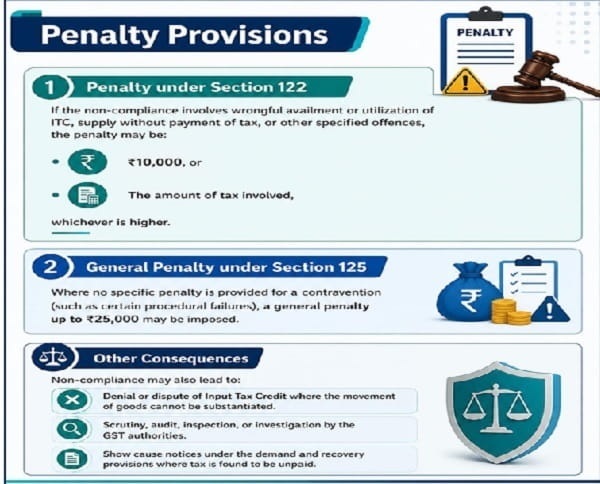

7. Consequences of Non-Compliance with Job Work Provisions :-

There is no separate penalty specifically prescribed for non-compliance with the job work provisions under Section 143 of the CGST Act. However, failure to comply with the job work procedure can result in GST liability, interest, ITC reversal, and penalties under various provisions of the CGST Act.

8. Concluding remarks over compliance tips under Job work process :-

To ensure smooth compliance with the GST provisions relating to job work under Section 143 of the CGST Act, 2017 and Rule 45 of the CGST Rules, 2017, businesses should follow the best practices below:

- Keep a job work register for the movement of goods.

- Match challans of delivery with ITC-04 data.

- File within the due date to escape penalties.

- Utilize accounting software automation for reminders.

*****

The author can be contacted at calokeshaggarwal52@gmail.com His mobile number is +91 836-835-3016.

DISCLAIMER : This publication serves as a general guide for informational purposes only. The references and content provided are for educational purposes and should not be considered as legal advice.

Author Bio