Day: May 11, 2019

11 articlesGoods and Services Tax

Goods and Services Tax

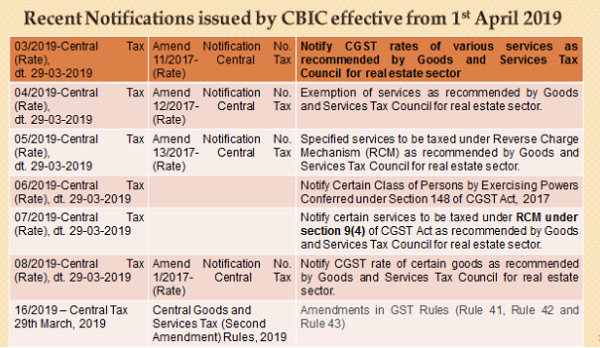

GST on Real Estate: Time for Builders & Officials to Enrich Gracefully

Goods and Services Tax

Goods and Services Tax

How to View and Download GST Accounting and Billing Software

Corporate Law

Corporate Law

Domicile and Apostille

Income Tax

Income Tax

Extension of time for Special audit by AO on Suo moto basis

Income Tax

Income Tax

Disallowance of Contribution of PF, ESIC etc u/s 36(1)(va) – A Comparative Study between Section 36(1)(va) Vs. Section 43-B

Goods and Services Tax

Goods and Services Tax

Seizure notice issued to transporter is valid despite not being supplier of goods: HC

CA, CS, CMA

CA, CS, CMA

The Power of Planning & its Execution

Goods and Services Tax

Goods and Services Tax

Examination For Confirmation of Enrollment of GST Practitioners on 14.06.2019

Income Tax

Income Tax

Employee’s contribution for PF/ESI before due date of filing return of income is allowable expense

Goods and Services Tax

Goods and Services Tax