The Securities and Exchange Board of India issued a circular dated April 24, 2026 introducing a framework permitting net settlement of funds for Foreign Portfolio Investors (FPIs) in the cash market. Previously, FPIs were required to settle transactions on a gross basis due to restrictions on intra-day trading, leading to higher liquidity needs, increased funding costs, and operational inefficiencies. Based on industry representations, SEBI allowed netting of funds for “outright transactions,” defined as either only purchase or only sale in a security within a settlement cycle. Transactions involving both buy and sell positions will continue to be settled on a gross basis. The circular clarifies that securities settlement remains gross between FPIs and custodians, and statutory levies like STT and stamp duty remain unchanged. Implementation standards will be developed by relevant stakeholders, and entities must update systems by December 31, 2026. The measure aims to improve efficiency and reduce funding costs.

Securities and Exchange Board of India

Circular No. HO/(1)2026-AFD-POD2/I/10157/2026 Dated: April 24, 2026

To,

1. All Registered Foreign Portfolio Investors

2. All Registered Custodians

3. All Recognised Clearing Corporations

4. All Recognised Stock Exchanges

5. All Registered Stock Brokers through Recognised Stock Exchanges

Dear Sir / Madam,

Subject: Framework for net settlement of funds for transactions done by Foreign Portfolio Investors (FPIs) in cash market

1. SEBI’s Master Circular for Stock Exchanges and Clearing Corporations dated December 30, 2024 inter-alia stipulates that no institutional investor shall be allowed to do day trading, i.e., square off their transactions intra-day. Thus, all transactions carried out by FPIs are required to be grossed at custodians’ level and obligations are fulfilled by FPIs on a gross basis. The custodians, however, settle their deliveries on a net basis with the Clearing Corporations (CCs).

2. Representations were received from market participants highlighting that the gross settlement of transactions results in additional liquidity requirements, increased funding costs due to forex slippage and operational inefficiency for FPIs, particularly during days of index rebalancing.

3. Accordingly, with an objective to enhance operational efficiency and reduce cost of funding for FPIs, it is decided to permit net settlement of funds for outright transactions undertaken by FPIs in cash market. For the purpose of this circular, ‘outright transactions’ shall mean either a purchase or a sale transaction, but not both, in a security in a settlement cycle undertaken by an FPI.

4. The framework for netting of funds for transactions undertaken by FPIs in cash market shall be as follows:

a. FPI transactions in securities with only outright sell or outright purchase shall be net settled to arrive at net fund obligation for such outright transactions. Transactions in securities having both purchase and sale transactions in a settlement cycle shall be excluded from netting. Such non-outright transactions shall continue to be settled by FPI as per the current procedure, i.e. on gross basis.

b. In case value of outright sale is less than the value of outright purchase, the residual amount along with non-outright purchase obligations shall be funded by the FPI. However, if value of outright sale exceeds the value of outright purchase, the excess outright sale shall not be adjusted towards non-outright purchase obligations.

c. An illustration of the FPI obligations as per current practice and new mechanism is placed at Annexure A.

5. Further, it is clarified that settlement of securities shall continue to be carried out on gross basis between FPI and custodian. Also, Securities Transaction Tax (STT) and stamp duty shall continue to be charged on delivery basis.

6. Accordingly, the provisions stated at Para 4 of Annexure 3 of Chapter 1 (Trading) of SEBI’s Master Circular for Stock Exchanges and Clearing Corporations dated December 30, 2024 shall stand modified to the extent specified herein.

7. The implementation standards shall be formulated by the Custodians and Designated Depository Participants Standards Setting Forum (CDSSF), after consulting the relevant stakeholders.

8. Custodians, FPIs and all relevant stakeholders are advised to make necessary changes in their systems to effect the changes specified above.

9. The provisions of this circular shall be implemented on or before December 31, 2026.

10. This Circular is issued in exercise of the powers conferred under Section 11(1) of the Securities and Exchange Board of India Act, 1992 read with Regulation 44 of SEBI (Foreign Portfolio Investors) Regulations, 2019 to protect the interest of investors in securities and to promote the development of, and to regulate the securities market.

11. This Circular is available at sebi.gov.in under the link “Legal —Circulars”.

Yours faithfully,

Manish Kumar Jha

Deputy General Manager

Tel no. +91-22-26449219

Email: manishkj@sebi.gov.in

Annexure A

Illustration of obligations of FPI as per current practice and new mechanism

1. Consider an example wherein on a particular day, an FPI has bought 10 shares of stocks A and B worth 1000 each and sold 20 shares of stocks B and C worth 2000 each. For the sake of simplicity, it is assumed that all the transactions are on account of the said FPI, and the custodian clears the transactions of only this single FPI. All transactions are assumed to be confirmed. The example is summarised in the table given below:

| Stock | Buy Quantity | Buy Value | Sell Quantity | Sell Value |

| A | 10 | 1000 | 0 | 0 |

| B | 10 | 1000 | 20 | 2000 |

| C | 0 | 0 | 20 | 2000 |

2. The obligations of FPI under the current practice and new mechanism is as under:

2.1. Current Practice (Gross Settlement):

a. All the transactions of the FPI are settled on a gross basis with the custodian.

b. The custodian, however, settles its obligations on a net basis with the Clearing Corporation (CC).

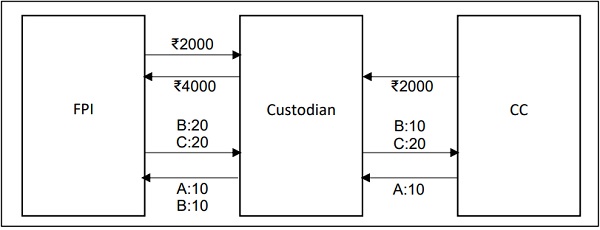

c. Accordingly, in the example given above, the pay-in and pay-out obligations of FPI towards the custodian and of custodian towards CC are given below:

i. Obligation of FPI towards custodian

| Pay-in | Pay-out | |

| Funds | 2000 | 4000 |

| Securities | Stock B: 20 Stock C: 20 | Stock A: 10 Stock B: 10 |

ii. Obligation of custodian towards CC

| Pay-in | Pay-out | |

| Funds | 0 | 2000 |

| Securities | Stock B: 10 Stock C: 20 | Stock A: 10 |

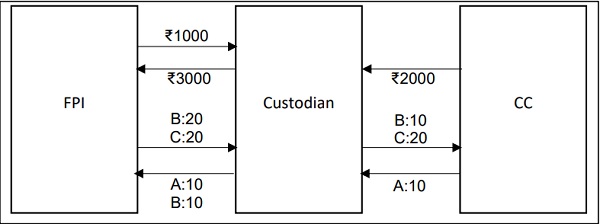

iii. Pictorial depiction of the obligations of FPI, custodian and CC is given below:

2.2. New Mechanism (Netting of funds):

a. The transactions in securities with only outright sell or outright purchase shall be netted to arrive at a net fund obligation for outright transactions.

b. In the instant example, there is an outright purchase in stock A and an outright sale in stock C, therefore, they shall be netted to arrive at a net fund obligation for outright transactions.

c. Since stock B involves both purchase and sale under the same settlement cycle, it shall be settled as per the existing practice of gross settlement.

d. The excess outright sell value (on account of netting of funds for stocks A and C) shall not be adjusted towards non-outright buy obligations.

e. Further, the manner of settlement between custodian and CC shall remain unchanged.

f. Accordingly, in the example given above, the pay-in and pay-out obligations of FPI towards the custodian and of custodian towards CC are given below:

i. Obligation of FPI towards custodian

| Pay-in | Pay-out | |

| Funds | 1000 | 3000 |

| Securities | Stock B: 20 Stock C: 20 | Stock A: 10 Stock B: 10 |

ii. Obligation of custodian towards CC

| Pay-in | Pay-out | |

| Funds | 0 | 2000 |

| Securities | Stock B: 10 Stock C: 20 | Stock A: 10 |

iii. Pictorial depiction of the obligations of FPI, custodian and CC is given below: