Date : Feb 02, 2016

Sixth Bi-monthly Monetary Policy Statement, 2015-16

By Dr. Raghuram G. Rajan,

Governor

Monetary and Liquidity Measures

On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.75 per cent;

- keep the cash reserve ratio (CRR) of scheduled banks unchanged at 4.0 per cent of net demand and time liability (NDTL);

- continue to provide liquidity under overnight repos at 0.25 per cent of bank-wise NDTL at the LAF repo rate and liquidity under 14-day term repos as well as longer term repos of up to 0.75 per cent of NDTL of the banking system through auctions; and

- continue with daily variable rate repos and reverse repos to smooth liquidity.

Consequently, the reverse repo rate under the LAF will remain unchanged at 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 7.75 per cent.

Assessment

2. Since the fifth bi-monthly statement of December 2015, global growth has slowed, with the ongoing weakening of activity in major emerging market economies (EMEs) outweighing the recovery in some advanced economies (AEs). World trade has remained subdued, held down by anaemic demand, new lows in commodity prices and currency realignments. In the United States, an improving labour market continues to support a consumption-led recovery. Manufacturing activity is sluggish, however, reflecting retrenchment in oil and gas drilling activity and declining exports. In the Euro area, improving labour market and financing conditions are supporting consumer spending and business investment. Although core inflation and wage growth are subdued, deflation risks appear to be receding. In Japan, the combination of exceptional monetary accommodation and fiscal stimulus has failed to spur sustainable domestic demand so far. In China, growth in Q4 of 2015 was the slowest since 2009, pulled down by manufacturing, residential investment and exports. EME commodity exporters confront recessionary conditions, falling currencies, sluggish exports and still high inflation relative to their recent histories.

3. The December calm in global financial markets – suggesting that the normalisation of US monetary policy was fully anticipated – was dispelled in January 2016 by fears of further weakening of the Chinese economy and the depreciation of the Renminbi. Capital outflows from China triggered sell-offs across AEs and EMEs, exacerbating currency declines and heightening volatility. Crude oil prices fell below US $ 30 per barrel – a 12-year low –on expectations of Iran adding to the supply glut. Prices of gold prices and US Treasuries hardened on safe haven demand. Financial markets remain vulnerable to bouts of volatility and capital outflows from EMEs as an asset class. Bearish commodity price dynamics are also likely to impact investor sentiment.

4. On the domestic front, economic activity lost momentum in Q3 of 2015-16, pulled down by slackening agricultural and industrial growth. The north-east monsoon season ended in December with a deficiency of 23 per cent relative to the long period average (LPA). By end-January, rabi sowing was mildly deficient relative to a year ago, as well as to the quinquennial average in respect of all crops, except coarse cereals. Rural incomes will continue to be supported by allied activities such as dairy and horticulture, which now contribute as much to GDP as food grains.

5. In the first two months of Q3 of 2015-16, industrial activity slowed in relation to the preceding quarter. This mainly reflects weak investment demand with some deceleration of capital goods production. Stalled projects continue to remain high, and there is a decline in new investment intentions, perhaps on the back of low capacity utilization. While revenue growth in manufacturing has been modest, the fall in costs, partly because of a decline in commodity prices, and partly because of improvements in manufacturing efficiency, have resulted in relatively stronger profitability. The Reserve Bank’s industrial outlook survey suggests a modest expansion of activity likely in Q4. In January 2016, the manufacturing purchasing managers’ index (PMI) expanded to a four-month high on, inter alia, resumption of output by firms affected by the December floods as well as on new domestic and export orders.

6. Lead indicators of the services sector are mixed. Construction activity is still tepid, as evidenced by weak growth in cement production, though the pick-up in road construction bodes well for future activity, especially if supported by construction in the major proposed industrial corridors. Railway freight growth is still weak, though it may reflect lower transport needs for inputs like coal, and competition from roadways. However, the services PMI rose to a ten-month high in December on improvement in new business orders and upbeat expectations.

7. Retail inflation measured by the consumer price index (CPI) rose for the fifth month in December across all constituent categories. While the upturn in December essentially reflected unfavourable base effects, the ongoing seasonal decline in prices of fruits and vegetables could temper headline inflation in the near-term. Prices of cereals recorded modest increases despite the adverse monsoon, indicative of effective supply management. On the other hand, pulses inflation continued to remain elevated, reflecting structural mismatches.

8. CPI inflation excluding food and fuel rose for the fourth successive month. Excluding petrol and diesel from this category, inflation remained flat. A breakdown into goods and services categories shows that while goods inflation declined, services inflation has been sticky since September 2015 across housing, transport and communication, medical and other services. Household inflation expectations remain elevated and the rate of increase in corporate staff costs picked up. On the other hand, rural wage growth has been muted.

9. Liquidity conditions tightened in the second half of December with advance tax outflows. Tightness spilled over into January 2016 on the back of a seasonal pick-up in demand for currency, restrained spending by the government and a pick-up in bank credit growth, in relation to deposit mobilisation. In order to mitigate these conditions, the Reserve Bank injected liquidity through variable rate term repos of varying tenors ranging from overnight to 56 days, besides provision through the regular liquidity windows. The average daily liquidity injection (including variable rate overnight and term repos) increased from ₹ 1,200 billion in December to about ₹ 1,345 billion in January. In addition, the Reserve Bank also injected ₹ 200 billion through open market purchase operations on December 7 and January 20. In response, money market rates remained close to the policy rate with a marginal downside bias. Bank credit in the form of personal loans and non-bank flows from both domestic and foreign sources grew strongly.

10. India’s exports remained in contraction mode for the thirteenth successive month in December, although there are indications of a sequential bottoming out. In volume terms too, the rate of decline appears to be moderating. While softer petroleum, oil and lubricants (POL) and commodity prices helped to contain the trade deficit, these benign effects were offset by a spike in the quantum of gold and POL imports. As a consequence, the trade deficit widened during December in relation to preceding months, though the overall current account deficit is likely to remain well contained and easily financed. Net foreign direct investment (FDI) and non-resident deposits have remained robust in relation to last year. The persisting decline in oil prices may, however, impact the flow of remittances from the Gulf region where fiscal positions are deteriorating rapidly. Portfolio investment also recorded some outflows since November. Nevertheless, as on January 22, 2016, foreign exchange reserves stood at US$ 347.6 billion – an accretion of US$ 5.9 billion during the current financial year so far.

Policy Stance and Rationale

11. Inflation has evolved closely along the trajectory set by the monetary policy stance. With unfavourable base effects on the ebb and benign prices of fruits and vegetables and crude oil, the January 2016 target of 6 per cent should be met. Going forward, under the assumption of a normal monsoon and the current level of international crude oil prices and exchange rates, inflation is expected to be inertial and be around 5 per cent by the end of fiscal 2016-17 (Chart 1). However, the implementation of the VII Central Pay Commission award, which has not been factored into these projections, will impart upward momentum to this trajectory for a period of one to two years. The Reserve Bank will adjust the forecast path as and when more clarity emerges on the timing of implementation. Vagaries in the spatial and temporal distribution of the monsoon and the impact of adverse geo-political events on commodity prices and financial markets add additional uncertainty to the baseline.

12. Prospects for the rabi harvest are improving slowly. The near-term outlook for industrial activity may be constrained by adverse base effects in Q4 and still weak exports, although the pick-up in corporate profitability on the back of declining input costs may provide an offset. Some categories of services are likely to gain momentum on expectations of higher activity in coming months, though the aggregate state of activity remains muted. On balance, therefore, GVA growth for 2015-16 is kept unchanged at 7.4 per cent with a downside bias.

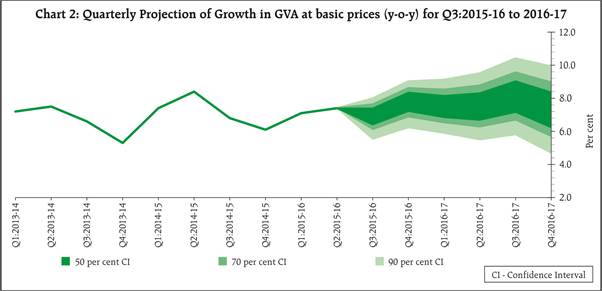

13. For 2016-17, growth is expected to strengthen gradually, notwithstanding significant headwinds. Expectations of a normal monsoon after two consecutive years of rainfall deficiency, the large positive terms of trade gain, improving real incomes of households and lower input costs of firms should contribute to strengthening the growth momentum. Yet, still weak domestic private investment demand in a phase of balance sheet adjustments, re-emergence of concerns relating to stalled projects, excess capacity in industry, sluggish external demand conditions dampening export growth could act as headwinds. Based on an assessment of the balance of risks, GVA growth for 2016-17 is projected at 7.6 per cent (Chart 2).

14. In keeping with the Government’s Start-up India initiative, the Reserve Bank will take steps to ease doing business and contribute to an ecosystem that is conducive for growth of start-ups. These measures will create an enabling framework for receiving foreign venture capital, differing contractual structures embedded in investment instruments, deferring receipt of considerations for transfer of ownership, facilities for escrow arrangements and simplification of documentation and reporting procedures. A detailed statement is being issued separately.

15. The current momentum of growth is reasonable, though below what should be expected over the medium term. Underlying growth drivers need to be rekindled to place the economy durably on a higher growth trajectory. The revival of private investment, in particular, has a crucial role, especially as the climate for business improves and fiscal policy continues to consolidate. The Indian economy is currently being viewed as a beacon of stability because of the steady disinflation, a modest current account deficit and commitment to fiscal rectitude. This needs to be maintained so that the foundations of stable and sustainable growth are strengthened. The Reserve Bank continues to be accommodative even as it leaves the policy rate unchanged in this review, while awaiting further data on the development of inflation. Structural reforms in the forthcoming Union Budget that boost growth while controlling spending will create more space for monetary policy to support growth, while also ensuring that inflation remains on the projected path of 5 per cent by the end of 2016-17.

16. The first bi-monthly monetary policy statement for 2016-17 will be announced on Tuesday, April 5, 2016.

Alpana Killawala

Principal Adviser

Press Release : 2015-2016/1807