Meaning of Residential Status

Residential status for income tax refers to the status of an individual or an entity based on their presence or stay in India during a financial year. It determines the extent to which their income will be taxed in India. The residential status is determined based on the number of days an individual or an entity has spent in India during the relevant financial year and the preceding financial years.

Types of Residential Status –

The Income Tax Act classifies taxpayers into three categories based on their residential status, which are:

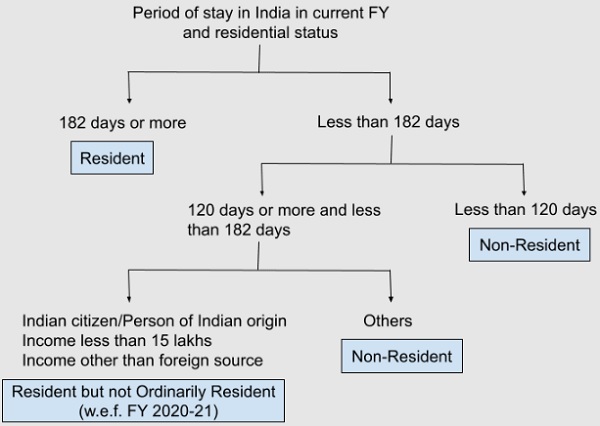

1. Resident and Ordinary Resident (ROR): An individual is considered a resident of India if he/she meets any of the following conditions:

- Stayed in India for 182 days or more during the financial year OR

- Stayed in India for 60 days or more during the financial year and 365 days or more during the four years immediately preceding the financial year.

If an individual meets either of these conditions, he/she is considered a resident of India. If the individual meets both these conditions, then he/she is a Resident and Ordinary Resident (ROR). The period is reduced to 120 days or more instead of 182 days for such an individual whose total income other than foreign sources exceeds Rs 15 lakh.

2. Resident but Not Ordinary Resident (RNOR): An individual if he consider to be as resident than the next step is to determine whether is a ordinary or non-ordinary resident. He will be a ROR if he meets both of the following conditions:

1. Has been a resident of India in at least 2 out of 10 years immediately previous years and

2. Has stayed in India for at least 730 days in 7 immediately preceding years

3. Non-Resident (NR): An individual who does not meet any of the above conditions is considered a Non-Resident (NR). This status is applicable to individuals who have stayed outside India for the entire financial year or who do not have a residential status in India.

Taxability under residential status

The taxability under residential status depends on the residential status of the individual as per the Income Tax Act. Here’s how the taxability differs based on the residential status:

1. Resident and Ordinary Resident (ROR): An individual who is a resident and ordinary resident (ROR) is taxable on their global income, which includes income earned both in India and abroad. Such individuals are required to file their income tax returns in India and pay tax on their global income.

2. Resident but Not Ordinary Resident (RNOR): An individual who is a resident but not an ordinary resident (RNOR) is taxable only on the income earned or received in India. Such individuals are generally exempt from tax on income earned outside India, except in cases where the income is received in India or arises from a business or profession set up in India.

3. Non-Resident (NR): An individual who is a non-resident (NR) is taxable only on the income earned or received in India. Non-residents are generally not required to file their income tax returns in India, except in cases where their income earned in India exceeds the prescribed threshold limit.

In addition to the above, there are various tax deductions and exemptions available to residents and non-residents. The taxability under residential status may also differ based on the double taxation avoidance agreement (DTAA) between India and the country of residence of the individual. Therefore, it is important for individuals to determine their residential status correctly to ensure proper tax compliance and minimize their tax liability.

*****

The author is an Income Tax and GST Practitioner and can be contacted at 9024915488.

Author Bio

I have been an NRI for the past 30+ years and am now planning to return to India for good. As I have a business overseas and also income from my overseas investments, how much will I be taxed on my return to India. Over here income from company dividends and ULIPs are not taxable.

Hi Madhav, for resident of India income earned outside India is also taxable, but you would get benefit tax paid outside India for same income under Double Taxation Avoidance Agreement (DTAA) to discuss in detail please whatsap us at 9024915488. thanks