Summary: The debate over Section 87A continues even after Budget 2025, as tax professionals and authorities remain divided on its interpretation. The key change introduced in the Finance Bill, 2025, is the increase in the rebate limit from ₹7 lakh to ₹12 lakh under the New Tax Regime. However, a crucial restriction has been added: the rebate no longer applies to tax on special rate income, including capital gains and lottery winnings. Previously, Section 87A allowed a rebate for resident individuals with income up to ₹7 lakh, without restrictions on special rate income (except long-term equity gains under Section 112A). The new amendment explicitly limits the rebate to tax calculated under regular slab rates as per Section 115BAC, which excludes special rate income. This means individuals earning capital gains or other special incomes may not benefit from the rebate, even if their total income is under ₹12 lakh. Misconceptions remain, with many assuming the rebate applies broadly. However, only resident individuals qualify, and the rebate is only applicable to normal slab-rate income. Those with significant special rate income might consider tax planning strategies, including evaluating the Old Regime’s benefits. While the changes aim to streamline tax provisions, they have introduced new complexities, leaving taxpayers and advisors seeking further clarity.

The debate over Section 87A has been ongoing since last year’s ITR filings, and even after the 2025 Budget, the confusion remains. Despite inquiries to Big 4 firms and government authorities, there is still no clear or uniform response.

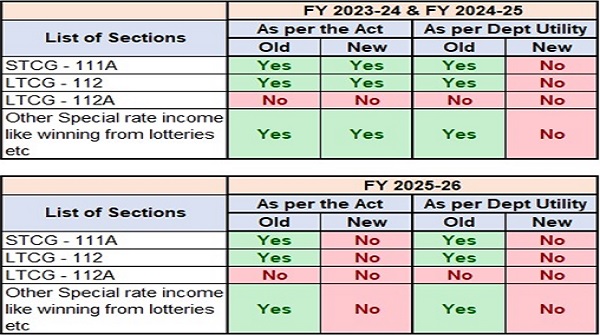

After thoroughly examining the new Finance Bill and its key provisions, a chart has been prepared explaining the issue in detail.

Page Contents

- What Has Changed?

- Key Changes:

- Common Misconceptions and Clarifications

- Q.1 Does this rebate provisions applies to everyone?

- Q.2 Does the ₹12 lakh limit include capital gains and special rate income?

- Q.3 If my normal income is below ₹12 lakh but total income (including capital gains) exceeds ₹12 lakh, will I still get the rebate?

- Q.4 Will I get a rebate on special rate income tax if my total income is less than ₹12 lakh?

- Q.5 Under the Old Regime, can I get a rebate on capital gains?

- Q.6 Is there a way to reduce tax liability under the new rules?

- Q.7 Instead of simplifying, why is it getting more complicated?

What Has Changed?

The Finance Bill, 2025, has raised the rebate limit under Section 87A to ₹12 lakh under the New Tax Regime. However, a crucial restriction has been introduced—rebate will no longer apply to tax on special rate income, such as capital gains and lottery winnings.

Before diving into the details, let’s examine the old and revised provisions.

I. Before Amendment (Up to FY 2024-25)

Before the amendment made in Budget 2025, Section 87A allowed resident individuals with a total income of up to ₹7 lakh (under the New Regime) to claim a rebate equal to the total tax payable or ₹25,000, whichever was lower.

There was no restriction on claiming the rebate against special rate income, except under Section 112A, which explicitly stated that the rebate would not apply to tax on long-term capital gains from equity investments.

II. After Amendment in Budget 2025 (Applicable from FY 2025-26 onwards)

Key Changes:

- The rebate threshold under Section 87A has been increased from ₹7 lakh to ₹12 lakh.

- A new proviso has been inserted, restricting the rebate on special rate income which was not there in the Act earlier, which is as follows:

“Provided further that the deduction under the first proviso, shall not exceed the amount of income-tax payable as per the rates provided in sub-section (1A) of section 115BAC.”

From above you can easily point out the following:

1. Section 87A considers total income, which includes all sources, including special rate incomee. Capital Gains.

2. Section 112A(6) already restricted rebate on long-term equity gains.

These provisions were in place until March 2025, so everyone figured the rebate would still apply to short-term gains, other long-term gains, and special rate income. But with all the chaos surrounding it, let’s not go down that road again—I’d hate to be the one to spoil your mood!

3. The newly inserted proviso explicitly restricts rebate eligibility on special rate income, ensuring that the rebate applies only to tax on regular slab-rate income.

As per Section 87A, the rebate cannot exceed the tax calculated under Section 115BAC, which specifically outlines the slab rates applicable under the New Tax Regime. Since Section 115BA defines tax rates only for normal income and does not cover special rate income (such as capital gains or lottery winnings), the rebate is now effectively limited to tax computed on income taxed at regular slab rates.

Common Misconceptions and Clarifications

Q.1 Does this rebate provisions applies to everyone?

Ans. It only applies to Resident Individuals. So, NRIs and HUFs are out of the picture.

Q.2 Does the ₹12 lakh limit include capital gains and special rate income?

Ans. Yes, total income includes all heads of income, including capital gains, dividends, and special rate income.

Q.3 If my normal income is below ₹12 lakh but total income (including capital gains) exceeds ₹12 lakh, will I still get the rebate?

Ans. Because your total income is exceeding Rs.12 Lac.

Q.4 Will I get a rebate on special rate income tax if my total income is less than ₹12 lakh?

Ans. The rebate only applies to normal slab rate income and not on capital gains or any special rate income.

Q.5 Under the Old Regime, can I get a rebate on capital gains?

Ans. Yes, except for long-term capital gains on listed equity (112A).

Q.6 Is there a way to reduce tax liability under the new rules?

Ans. Proper tax planning is necessary. If you have significant capital gains or other special rate incomes and income is less than ₹5 lakh, the Old Regime might be more beneficial in some cases.

Q.7 Instead of simplifying, why is it getting more complicated?

Ans. Because the government knows that Indians just can’t handle things being too simple! Jokes aside, the intention is always to simplify tax laws, but, as they say, too many cooks spoil the broth—or in this case, too many amendments turn a simple rule into a puzzle. In the quest to make things easier, they sometimes end up making them even more confusing. But hey, at least they’re keeping tax consultants in business!

Author Bio