1) New Income Tax Act- A Step Towards Simplification:- In a landmark move, the Finance Minister is set to introduce a new Income Tax Bill in Parliament next week, aimed at overhauling the existing tax framework. The new legislation will be guided by the principle of ‘Nyay’ (justice), ensuring a fair, transparent, and simplified tax system for all taxpayers. By addressing complexities and ambiguities in the current law, the proposed reforms seek to enhance ease of compliance, reduce litigation, and promote economic growth. This long-awaited tax code is expected to modernize India’s direct tax structure, making it more equitable and efficient.

2) Personal Income- tax Reforms with special focus on middle class: –The Budget 2025 announced that there will be no income tax payable upto income of Rs 12 lakh (i.e. average income of Rs. 1 lakh per month other than special rate income such as capital gains) under the new regime. This limit will be Rs. 12.75 lakh for salaried taxpayers, due to standard deduction of Rs. 75,000.

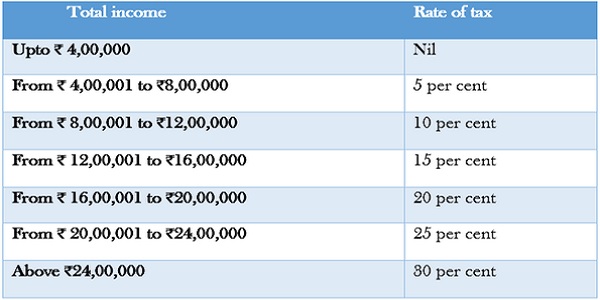

The Slabs and rates are being changed across the board to benefit all taxpayers. The new structure will substantially reduce the taxes of the middle class and leave more money in their hands, boosting household consumption, savings and investment. In the new tax regime, FM proposed to revise tax rate structure as follows:

Under the new tax regime, a resident individual with a total income of up to ₹7,00,000 currently does not have to pay any tax due to the rebate benefit. It is now proposed to enhance this rebate so that individuals earning up to ₹12,00,000 will also not be required to pay any tax. This effectively ensures that taxpayers in this income bracket receive complete tax relief.

For salaried individuals, the effective tax-free limit is even higher. With the inclusion of the standard deduction of ₹75,000, salaried taxpayers can have an income of up to ₹12.75 lakh without any tax liability under the new regime.

For instance, as per the revised tax structure, an individual earning ₹12,00,000 would have been liable to pay ₹80,000 in tax under the previous system. However, with the new rebate provisions, their tax liability becomes zero, providing them with a full benefit of ₹80,000. Similarly, taxpayers earning slightly above ₹12,00,000 will still receive marginal relief, ensuring they do not face a sharp increase in tax liability.

To illustrate, an individual with an income of ₹18,00,000 will receive a tax benefit of ₹70,000, amounting to 30% of their previously payable tax. Likewise, a taxpayer earning ₹25,00,000 will benefit by ₹1,10,000, which is 25% of their previous tax liability.

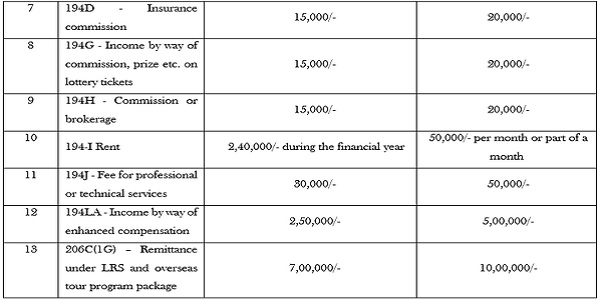

The Budget 2025 introduces key reforms in Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) to ease compliance, reduce tax burdens, and support taxpayers.

Major changes include higher exemption limits for senior citizens and rental income, removal of TCS on education-related remittances, and simplification of TDS/TCS provisions to avoid duplicate taxation and compliance difficulties. Additionally, the relaxation granted for TDS payment delays in July 2024 has now been extended to TCS payments, further easing tax administration.

Key Budget 2025 Announcements on TDS & TCS:

- TDS on Interest for Senior Citizens (Section 194A): The tax deduction limit on interest for senior citizens has been doubled from ₹50,000 to ₹1,00,000, providing greater financial relief.

- TDS on Rent (Section 194I): The annual threshold for TDS deduction on rent has been raised from ₹2.40 lakh to ₹6 lakh, benefiting landlords and tenants.

- TCS on Remittances (LRS): The threshold for collecting tax at source (TCS) on foreign remittances under RBI’s Liberalized Remittance Scheme (LRS) has been increased from ₹7 lakh to ₹10 lakh. Additionally, TCS on remittances for education purposes (where the funds come from a loan taken from a specified financial institution) has been removed.

- Simplification of TDS & TCS Compliance: To prevent compliance difficulties, the TCS on the sale of goods has been omitted, ensuring smoother transactions. Furthermore, the higher TDS deduction provisions will now apply only in non-PAN cases, reducing the burden on compliant taxpayers.

- Relaxation in TCS Payment Delays: Following the July 2024 decriminalization of TDS payment delays, similar relaxation is now proposed for TCS payment delays, allowing more flexibility in tax compliance.

- Higher TDS/TCS Removal for Non-Filers: The provisions mandating higher TDS/TCS rates for non-filers of tax returns under Sections 206AB and 206CCA have been omitted to ease compliance burdens.

- Decriminalization of Delays in TDS/TCS Payments: The relief provided in July 2024 for delayed TDS payments up to the due date of filing the statement has now been extended to TCS payments.

- Removal of TCS on Sale of Specified Goods: No TCS will be applicable on sales exceeding Rs. 50 lakh for specified goods, reducing compliance burdens for businesses

The summary of TDS Threshold Table is as below :

–

4) Exemption on NSS Withdrawals:

Withdrawals made from the National Savings Scheme (NSS) by individuals on or after August 29, 2024, will be exempt from taxation. Additionally, similar tax treatment will be extended to NPS Vatsalya accounts, akin to standard NPS accounts, subject to overall limits.

5) Updated Return Time Limit Extension:

The time limit for filing an updated income tax return (ITR-U) has been extended from 2 years to 4 years. The additional tax payable for filing an updated return:

- 60% of the aggregate tax and interest for returns filed between 24-36 months.

- 70% of the aggregate tax and interest for returns filed between 36-48 months.

6) Self-Occupied Property Valuation: Taxpayers can now claim an annual value of ‘nil’ for up to two self-occupied properties without any conditions, simplifying compliance for homeowners.

It is proposed to provide that the annual value of the property consisting of a house or any part thereof shall be taken as nil, if the owner occupies it for his own residence or cannot actually occupy it due to any reason!

7) Obligation to furnish information in respect of crypto-asset: It is proposed to bring amendment in the Act to provide for that a prescribed reporting entity in respect of a crypto-asset shall furnish information in respect of a transaction in such crypto asset, in a statement as prescribed. It is also proposed to align the definition of virtual digital asset accordingly.

8) Extension of time limit of Validity of Registration for small charitable trusts/institutions

Extended Registration Period: The validity of registration for smaller charitable trusts has been increased from 5 years to 10 years, reducing administrative burdens.

Rationalization of Violations: Minor defaults, such as incomplete applications, will not lead to disproportionate penalties or cancellation of trust registrations.

Definition of Substantial Contribution: Amendments will clarify who qualifies as a substantial contributor to a trust or institution for determining exemption eligibility.

9) Ease of Doing Business & Compliance

- Extension of Tax Benefits for Startups: The eligibility period for Section 80-IAC tax benefits for startups has been extended for another 5 years, covering startups incorporated up to April 1, 2030.

- Capital Gains Tax Parity for Non-Residents: The tax treatment of long-term capital gains on securities for Foreign Institutional Investors (FIIs) will now be aligned with that of resident taxpayers.

- Simplified Taxation for Business Trusts: Business trusts will now be taxed under Section 112A, in addition to the existing provisions under Sections 111A and 112.

- Significant Economic Presence (SEP) Rules: Transactions or activities confined to purchasing goods in India for export will be excluded from the Significant Economic Presence (SEP) definition, ensuring clarity in taxation.

- Unit Linked Insurance Policies (ULIPs): Gains from the redemption of ULIPs not covered under Section 10(10D) will be taxed as capital gains.

- Amendment in Capital Asset Definition: To clarify the tax treatment of securities held by investment funds under Section 115UB, the definition of capital assets will be revised.

- Transfer Pricing Rationalization: The arm’s length price determination for similar transactions will now apply for 3 years, simplifying transfer pricing regulations.

10) Compliance & Administrative Reforms

- Extended Prosecution Exemption for TCS Delays: Taxpayers failing to deposit TCS on time will be exempted from prosecution if payments are made before the due date for filing quarterly TCS statements.

- Time Limit for Penalty Orders Rationalized: Penalty orders must now be passed within six months from the end of the quarter in which related proceedings are completed.

- Time Limit for Retaining Seized Books & Documents: Seized documents must be retained only for one month from the end of the quarter in which assessment or reassessment orders are made.

- Extension of Exemption for Specified Undertaking of UTI (SUUTI): The exemption for SUUTI under the Unit Trust of India (Transfer of Undertaking and Repeal) Act, 2002, is extended to March 31, 2027.

- Faceless Scheme Extension: The deadline for notifying faceless tax schemes will be removed, allowing the government to extend such initiatives beyond March 31, 2025.

- Updated Block Assessment for Digital Assets: The term “virtual digital asset” will now be included in the definition of undisclosed income for block assessments.

- Carry Forward of Losses in Amalgamation Cases: Losses accumulated by predecessor entities will now be carried forward for a maximum of 8 years.

Conclusion

In conclusion, Budget 2025 has made significant strides in providing relief to individual taxpayers and fostering a more business-friendly environment. By increasing the threshold for TDS and offering tax relief to individuals, the government has alleviated financial burdens, particularly for middle and lower-income groups. This relief is expected to boost consumer spending, stimulate demand, and increase savings, further driving economic growth. Additionally, the focus on enhancing the ease of doing business through simplified compliance and tax incentives is a positive step toward promoting growth and investment. These measures reflect a commitment to economic stability, improved financial inclusion, and a more dynamic business landscape, positioning the country for sustainable development in the coming years.

*****

For any tax related query you can contact the author at 9024915488.

Author Bio