1. ITR-3 form is required to be filed by individual or HUF whose total income for a given assessment year includes Income from a profession or business (both audit and non-audit cases), Income earned from one or multiple house properties, Income from Other Sources, Income generated from short or long-term capital gains. A salaried person engaged in F&O or intraday trading shall use ITR 3 to file the return.

2. ITR-3 is viewed as the most complicated ITR form for taxpayers, especially for a layman. In this article, an attempt has been made to simplify the filing of ITR 3 with the help of Illustrations and relevant provisions.

3. INTRADAY TRADING Intraday trading means buying and selling stocks on the same trading day. Intraday trading is also known as Day Trading. Share prices keep fluctuating throughout the day, and intraday traders try to draw profits from these price movements by buying and selling shares during the same trading day.

Intraday equity transactions are speculative in nature and hence income gained from intraday stock trading is regarded as speculative business income. Intraday trading is done through a Demat account of the trader.

4. FUTURE AND OPTIONS ( F&O) Futures and options are stock derivatives that are traded in the share market and are a type of contract between two parties for trading stock or index at a specific price or level at a future date.

The income/loss arising from trading in F&O transactions would be treated as a Business Income / Loss for the purpose of taxation. This means that taxpayers who have made money or incurred losses in the derivatives market will have to file their income tax returns through ITR Form-3 or Form-4.

5. DEMAT ACCOUNT STATEMENT: The first step for a taxpayer towards such return filing is to download/obtain a Demat Statement.

The demat Account statement is a summary of all the shares in the demat account. The statement provides the relevant details like quantity, buy date, buy price, buy value sale date , sale price , sale value , P&L value etc. of each transaction. These inputs are needed for reporting details in ITR Schedules.

Demat Statement can be downloaded either directly from the website of the relevant national depository or through a broker with whom the taxpayer maintains a demat account.

6. PRELIMINARY STEPS :

(a) Download utility from the income tax website www.incometax.gov.in

(b) Login to the portal and download prefill data. Upload this data in the downloaded utility.

(c) Select: AY 2021-22(Current AY) >. Start New filing > Individual> Select ITR Form > ITR 3> Let’s Get Started. Tick on the reason for filing Tax. Taxable income is more than the basic exemption limit.

(d) Select Schedules: Uncheck the schedules not required / applicable for ascertaining tax on share market transactions. You may find some irrelevant schedules, not getting unchecked. Just ignore.

7. ILLUSTRATION: TRANSACTION DETAILS FOR PY 2020-21

| Sl | Particulars | Amount(Rs.) | Amount(Rs.) |

| (a) | Income From Salary | 25,00,000 | |

| Less: Professional Tax | (2,500) | ||

| Less: Standard Deduction | (50,000) | ||

| Taxable Salary (25,00,000- 52500) | 24,47,500 | ||

| (b) | F&O Business ( Sale Value ) | 12,00,000 | |

| F&O Business ( Purchase Value ) | 15,00,000 | ||

| Exp incurred for F&O | 1,25,000 | ||

| Net Profit/ Loss from F&O Business | ( 4,25,000) | ||

| F&O Turnover ** | 18,00,000 | ||

| (c ) | Intraday turnover ( Absolute) | 75,000 | |

| Profit from Intraday transactions | 6,500 | ||

| Turnover in the case of Intraday Trading or F&O transaction is Absolute Turnover, Absolute Turnover is the Sum total of absolute profits minus losses made on daily transactions.

Turnover is only to determine if a tax audit is required or not. The tax liability does not get affected by turnover. |

|||

8. REPORTING THE DETAILS IN SCHEDULES

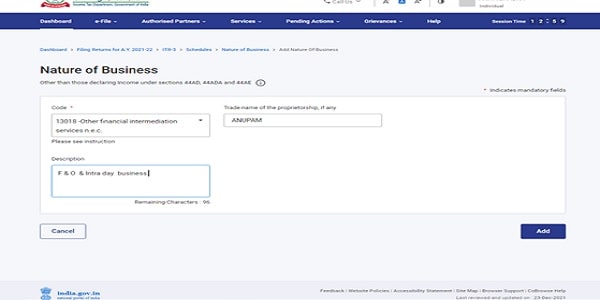

8.1 Nature of Business Select Code from the drop-down list. A trade name can be your name / Firm’s name. Enter description as F&O / Intraday business in the given box. This will give a fair idea about the nature of the business of the assessee.

There is no specific business code mentioned for F&O or intraday business. You may also select 09028 –Retail sale of other products.

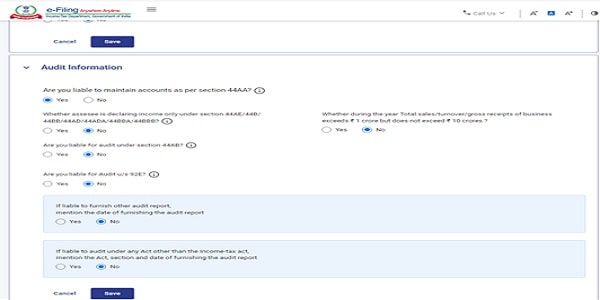

8.2 Audit Information: Are you liable to maintain accounts under section 44AA:

Statutory Provision

An individual or HUF, carrying business or profession (other than a specified profession) needs to maintain Books of Accounts if his income from business exceeds Rs. 2.50 lakhs and total turnover from business exceeds Rs 25 lakhs in any of the 3 preceding years – Section 44AA

In the Illustration above, income from the business is not exceeding Rs 2.50 lakhs or total sales in business is not exceeding Rs.25.00 lakh, Accounts are not required to be maintained under sec 44AA of Income tax Act.

However, the utility in the portal is not allowing to enter losses under the heading “No Account “. So, the option, yes need to be clicked and sales and purchase value of F&O transaction need to be reported in the schedule Part A – P&L Account.

8.3 Are you liable for Audit Under Sec 44AB

| Statutory Provision : | ||

| (a) | A person carrying on business, if his total sales in business for the year exceed or exceed Rs. 10 crores is required to get his Accounts Audited. | The threshold limit of Rs 10 crores is applicable as in the case of share trading more than 95% of the business transactions are done through banking channels. |

| (b) | Tax audit under Section 44AB also becomes mandatory for taxpayers who opt for a presumptive scheme of taxation in any of the preceding 5 years and now declare an income lower than the presumptive income and such income (after setting off F & O losses or other business losses if any) exceeds the maximum amount not chargeable to tax i.e. Rs 2.5 lakhs. | |

There is a difference of opinion amongst the experts, whether presumptive taxation scheme under section 44AD can be availed for F&O business.

In my view, F&O transactions are executed through recognized stock exchange and accounts cum records are maintained by the agencies / brokers of demat account. Hence presumptive tax scheme under sec 44AD cannot be availed in case of F&O income.

Thus, the relevant clause of audit requirement under section 44AB for presumptive tax is not applicable on a person carrying F&O business.

An individual engages in F&O business whose absolute turnover is less than Rs 10 crore and incurred loss is not required to get Tax Audit.

8.4 PART A -P&L Enter the sale value of F&O under the heading other Income Credited to P & L account and purchase value and expenditure in another expenditure debit to P & L Account

8.5 Intraday Transaction: – Part A – Profit & Loss – No Account > Speculative Activity

8.6 Schedule Salary: -Enter the relevant details in Salary Schedule

8.7 Other Schedules: Click on Schedule BP (Income from Business & profession), CYLA (Current Year Loss Adjustment), BFLA (Brought Forward Loss Adjustment) & CFL Carry Forward Losses) and confirm.

These schedules will automatically fetch the amount from the details entered. You just need to confirm.

8.8 Schedule Part II – TTI (Tax on total Income) – Provide confirmation of Tax Computation by clicking on it.

8.9 Preview Return > Proceed to preview > Proceed to Validation

9. Validation Error It is quite irritating to find the number of Validation errors after doing all the above exercises. Common validation errors and the way to rectify such errors are as follows: –

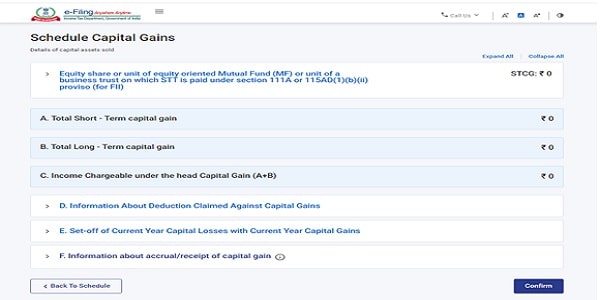

9.1 The total of all the quarter of respective CG must be equal to the final figures of schedule BFLA.” This is because you have not entered the quarter-wise details in Schedule Capital Gain.

Click on Sl. No. F ” of Schedule CG (Information about Accrual / Receipt of Capital Gain). Add details and enter the quarter-wise details of Capital Gain. Enter 0 if there is NIL CG in any quarter.

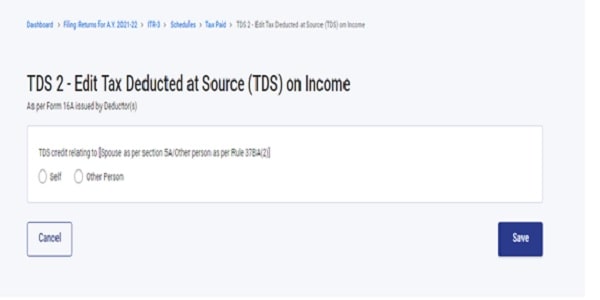

9.2 Validation error in TDS Schedule: Please select the radio button for the field TDS credit relating to Self/Other Person. Select the drop-down of the head of income for which corresponding income offered

Go to Schedule Tax Paid. Select Tax deducts at the source. There will be two options. Self and others. Click on Self

In the same schedule, scroll down and select the head of income from the drop-down menu:-

10. Frequently Asked Questions

Q.1 Is it mandatory to report F&O losses in ITR 3

Ans. Though it is not mandatory under the I tax Act but highly recommended to report losses in ITR. As not only these losses can be set off against other income but also can be carried forward for 8 subsequent years.

Q 2. What is the Business code (Nature of Business) for F&O Traders to be mentioned in ITR3 for FY 2020-21? Is it 13018 – Other financial intermediation services n.e.c (OR) 09028 – Retail sale of other products n.e.c (OR) any other appropriate code?

Ans. There is no specific code under the category, you may select “others” under Trading

Q3. Can I carry forward F&O losses without setting off in the current year’s profits.

Ans. No

Q4. An assessee, whose business turnover on options trading is Rs 20 lakhs in the year and incurred a loss of Rs 4 lakhs and did not maintain books of accounts as per sec44 AA. He has other income from Other Sources more than taxable exemption limit says Rs. 2.5lakhs. Is there any need for tax audit and to maintain books of accounts as specified?

Ans. Tax audit is not applicable if there is no cash receipts/payment involved as such, however, books may only be in form of a ledger statement, P&L given by the broker.

Disclaimer: The article is for education purposes only.

The Author can be approached at caanitabhadra@gmail.com

Author Bio

I have filled ITR form 3 last year (FY 22-23) as I had Intraday trading losses. But this year (23-24), I have no business transaction. Please suggest which ITR form I select to file to carry forward last year business losses. I have Income from Salary, from House Property and Other income this year.

Please guide

ITR 3 – for carry forward losses of previous year

Dear Ma’am,

I am a salaried individual joined the organisation last year in April. CTC between 3lac 70 to 3lac 90.

I have invested in mutual funds and shares but have not sold it. Also, I did intraday trading and incurred a loss of a small amount of below 10rs.

I don’t have Form 16 as I didn’t declare the details within the timeline needed by my employer.

Please assist, which ITR form would be applicable for me and can I file ITR without form 16?

File ITR1

In the absence of Form 16, take help from Salary Statement & cross check the same with pre-filled details in portal.

I got retired in 2019 nov. I kept Provident Fund with my employer for three years and received lump sum in 2022 afte three years . In every year interest accured on PF was considered while filing ITR.

Please convey which schedule to be refered in ITR 3 and where to report the lump sum received

Schedule EI- Exempt Income

I am salaried and have short term and long term gain. But I have only one intraday entry i.e. -192 which form i can fill for ITR.

can i fill ITR 2

You can ignore small amount of intraday and file ITR 2

I only did a little intraday trading,sum is only under 1000. delivery equities with a short-term profit of less than 100 rupees. Additionally, professional earnings.

Which schedule should I pick? Can I submit an ITR 4? Please advise.

You can file ITR 4

where we mention intrada loss in itr 3 as no account case.

Schedule P&L > No Account > Speculative activity

In FY 2022-23, i have

Income from salary-860000

Profit by selling share(LTCG)-15000

Profit by selling share(STCG)-1650

Dividend income-850

Profit by selling IPO on the first day of allotment-6000(INTRADAY)

Interest income from Saving/FD-18000

Please guide which ITR to fill, where to fill the income from share and dividends and tax calculation on share income ?

Thank you

ITR 3 ( as intraday transaction made)

THANK YOU.

BUT WHERE TO PUNCH ALL THESE(STCG,LTCG,INTRA) ENTRIES ?

Separate articles are available to explain , where to punch STCG & LTCG & Intraday transactions.

Link for the articles are :-

https://taxguru.in/income-tax/reporting-capital-gain-sale-equity-itr-2.html

https://taxguru.in/income-tax/report-fo-losses-in-itr-3-step-by-step-guidelines.html