Case Law Details

Sanjay Ramchandra Gawande Vs ACIT (ITAT Pune)

Pune ITAT Upholds Denial of TDS Credit in Rectification; Wrong Deductor Details Cannot Be Corrected U/s 154

Summary: The Pune ITAT dismissed the assessee’s appeal and upheld the rejection of a rectification application under Section 154 of the Income-tax Act relating to denial of TDS credit. The assessee admitted that while filing the return for AY 2015-16, the name of the deductor was incorrectly entered as “SMC Infrastructure Pvt. Ltd.” instead of “Municipal Council, Kamtee, Nagpur,” resulting in a mismatch and restriction of TDS credit to ₹3,87,988 instead of the claimed ₹14,27,420 in the Section 143(1) processing. The assessee sought rectification under Section 154, which was rejected by the Centralized Processing Center and confirmed by the CIT(A). The Tribunal observed that the incorrect deductor details were entered by the assessee, the Section 143(1) processing was computer-generated without manual intervention, and allowing the additional TDS credit would require detailed verification of TDS documents, including Form 26AS and other records. It held that such verification falls outside the scope of Section 154, as the issue was not a mistake apparent from the record. Accordingly, it upheld the orders of the CPC and the CIT(A) and dismissed the appeal.

The Pune ITAT dismissed the assessee’s appeal and upheld the rejection of a rectification application u/s 154 seeking grant of TDS credit of ₹10.39 lakh. The assessee had correctly disclosed the income in the return but had inadvertently mentioned the wrong name of the deductor, resulting in a mismatch during CPC processing. Consequently, while processing the return u/s 143(1), the CPC restricted the TDS credit to ₹3.87 lakh instead of the claimed ₹14.27 lakh.

The Tribunal observed that the mistake originated from the assessee’s own incorrect data entry in the return of income. Since the CPC processes returns through an automated system without manual intervention, the mismatch could not be treated as a mistake apparent from the record. The Tribunal held that allowing the additional TDS credit would require verification of running bills, Form 26AS and other supporting documents, which involves detailed factual examination beyond the limited scope of section 154.

Holding that such verification cannot be undertaken in rectification proceedings, the ITAT ruled that the CPC was justified in rejecting the rectification application, and the CIT(A) had rightly confirmed the same. Accordingly, the assessee’s appeal was dismissed.

Cases Discussed:

- Sanjay Ramchandra Gawande Vs ACIT (ITAT Pune)

FULL TEXT OF THE ORDER OF ITAT PUNE

This is an appeal filed by the assessee against the order of the Learned Additional/Joint Commissioner of Income Tax (Appeals)-2, Bengaluru [Ld. Addl./JCIT(A)], passed u/s. 250 of the Income Tax Act, 1961 (‘the Act’) for AY 2015-16 on 23.02.2026.

2. Submission of Ld. AR:

The Ld. AR filed a paper book containing 120 pages including decisions of the Hon’ble High Court and the ITAT. The Ld. AR admitted that there was a mistake by the assessee in typing the name of the deductor in the return of income. The facts mentioned by the assessee are as under :

“1. The appellant is an individual engaged in the business of civil construction contracting.

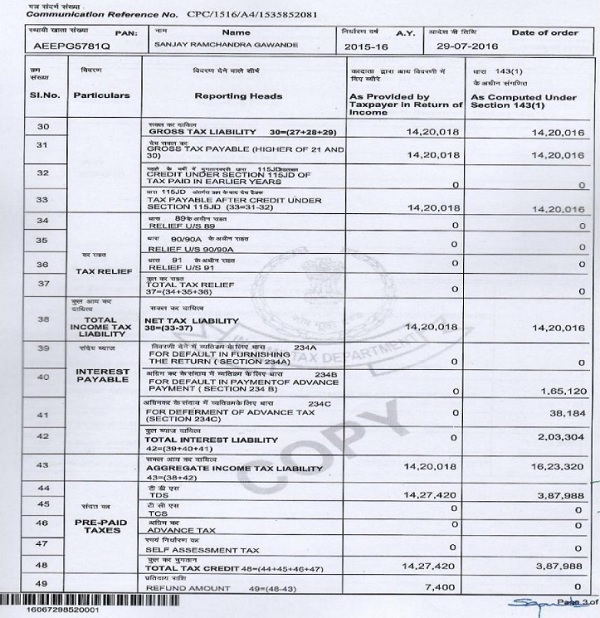

2. The appellant filed the return of income for Assessment Year 2015-16 on 31.10.2015 declaring turnover of Rs.7,41,98,149 and total income of Rs.48,87,650 and claiming credit of TDS amounting to Rs.14,27,420.

3. The return was processed under section 143(1) wherein the returned income was accepted. However, TDS credit was restricted to Rs.3,87,988 and TDS amounting to Rs.10,39,432 was not granted.

4. The appellant had raised bills aggregating to Rs.4,51,92,674 in respect of contractual work executed in the name of Municipal Council, Kamtee, Nagpur TAN NGPM02853E.

Out of this:

-

- 3,99,35,548 was received subsequently and TDS of Rs.6,84,310 was deducted.

- 52,57,126 pertained to balance income on which TDS of Rs.3,55,122 was deducted but not deposited by the deductor.

5. The entire income of Rs.4,51,92,674 was duly accounted for and offered to tax in Financial Year 2014-15 relevant to Assessment Year 2015-16.

6. The TDS of Rs.6,84,310 deducted under TAN NGPM02853E (Municipal Council, Kamtee, Nagpur) is reflected in Form 26AS for Assessment Year 2016-17 since the payment and deduction occurred in Financial Year 2015-16. However, the corresponding income had already been assessed in Assessment Year 2015-16.

7. The TDS of Rs.3,55,122 was deducted from the appellant’s income but was not deposited by the deductor and therefore does not appear in Form 26AS.

8. While filing the return of income for Assessment Year 2015-16, the appellant correctly mentioned TAN NGPM02853E. However, due to an inadvertent clerical error, the name of the deductor was mentioned as “SMC Infrastructure Pvt. Ltd.” instead of “Municipal Council, Kamtee, Nagpur.”

9. The appellant filed an application under section 154 seeking rectification and grant of TDS credit of Rs.10,39,432. The CPC rejected the rectification application.”

2.1 The Ld. AR submitted that the assessee is entitled for tax credit.

3. Submission of Ld. DR:

The Ld. DR submitted that the assessee in the return of income had incorrectly mentioned name of the deductor, therefore, there was mismatch and accordingly in the order u/s 143(1) of the Act which was computer generated the TDS was not allowed. The assessee filed rectification application with the Centralized Processing Center against the order u/s 143(1) of the Act which was rejected as there was no apparent mistake in the order u/s 143(1) of the Act. The Ld. DR supported the order of the Assessing Officer (AO) and the Ld. CIT(A) and requested to dismissed the appeal of the assessee.

4. Findings and analysis:

We have heard both the parties and perused the record. In this case, the assessee had filed return of income for AY 2015-16 on 31.10.2015. The due date for filing return of income for AY 2015-16 was 31.10.2015. The return of income of the assessee was processed by the Centralized Processing Center and order u/s 143(1) of the Act was passed on 29.07.2016. The Centralized Processing Center has restricted the assessee’s claim for TDS to Rs.3,87,988/- instead of Rs.14,27,420/-. The relevant part of the order u/s 143(1) of the Act which is at page Nos. 59 to 70 of the paper book is scanned and reproduced as under :

4.1 The assessee filed rectification application before the Centralized Processing Center against the order u/s 143(1) of the Act dated 29.07.2016. The Centralized Processing Center rejected assessee’s application. Aggrieved by the rectification order passed by the Centralized Processing Center, the assessee filed an appeal before the Ld. CIT(A) who confirmed the rectification order.

4.2 In this case, admittedly, the assessee had entered incorrect name in the Income Tax return while claiming tax deducted at source. The Centralized Processing Center processed Income Tax Return with the help of computer and there is no manual intervention and after that order u/s 143(1) of the Act is passed. Since, the assessee himself has entered incorrect details, there was mismatch and accordingly the Centralized Processing Center has restricted TDS credit of the assessee to Rs.3,87,988/-. The assessee filed rectification application before the Centralized Processing Center. In this case, admittedly, there was a mistake in data entered by the assessee in the return of income. Therefore, it is not an apparent mistake for the Centralized Processing Center to correct it. It is outside purview of section 154 of the Act as an elaborate verification of TDS documents is required before allowing any claim of excess TDS to the assessee. Therefore, this is outside the purview of section 154 of the Act. Hence, the Centralized Processing Center had rightly rejected the assessee’s claim of rectification and the Ld. CIT(A) had rightly confirmed the order u/s 154 of the Act.

4.3 The Ld. AR filed paper book which contains Working of TDS claimed at page No. 33, Running Bills issued by the Municipal Council, Kamtee at page Nos. 34 to 58, Copy of Form 26AS at page Nos.26 to 29 of the paper book. The Ld. AR submitted that as per R A Bill issued by the Municipal Council, TDS has been deducted. However, verification of all these documents which has been filed in the paper book is outside the purview of section 154 of the Act and these documents itself explains that there was no mistake apparent from record as far as order u/s 143(1) of the Act is concerned. In these facts and circumstances of the case, we do not find any merit in the appeal of the assessee. Accordingly, appeal of the assessee is dismissed.

5. In the result, the appeal of the assessee is dismissed.

Order pronounced in the open Court on 10th July, 2026

Author Bio