Case Law Details

Caspian Impact Investments Private Ltd Vs DCIT (ITAT Hyderabad)

Assessee, engaged in impact investment activities, originally filed ROI on 30.10.2019 declaring ₹10.76 crore under normal provisions & ₹11.28 crore u/s 115JB. After NCLT-approved demerger of debt division from Caspian Impact Investment Advisors Pvt. Ltd., a second revised ROI was filed on 30.09.2020 declaring ₹8.58 crore under normal provisions & ₹8.42 crore u/s 115JB. CPC processed return u/s 143(1)(a) on 09.03.2021, making three adjustments – ₹1.64 lakh u/s 36(1)(iii), ₹13.22 lakh u/s 37(1) & ₹10.41 lakh u/s 43B. CIT(A) confirmed all additions.

On further appeal, Tribunal found:

Section 37(1): The “loss on sale of fixed assets” of ₹13.22 lakh had already been suo motu disallowed by Assessee in computation. CPC’s action resulted in double disallowance, which was unsustainable.

Section 43B: The ₹10.41 lakh provision stood in books of demerged company as on 01.04.2018 & got transferred under NCLT demerger scheme. Since no fresh provision was created in AY 2019-20, invoking s.43B was invalid. Such carried-forward liability could not trigger addition in current year.

Tribunal thus directed deletion of both additions. On Assessee’s legal plea that CPC exceeded scope of 143(1)(a), ITAT held the issue academic after deleting additions on merits. Accordingly, the appeal was allowed in full.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal is filed by M/s. Caspian Impact Investments Private Limited, (“the assessee”), feeling aggrieved by the order passed by the Learned ADDL/JCIT (A)-1, Mumbai (“Ld. First Appellate Authority”), dated 27.02.2025 for the A.Y. 2019-20.

2. The assessee has raised the following grounds of appeal:

RE: GENERAL GROUND

1. That the impugned order is bad in law, since it is perverse, contrary to facts on record and hence, the same deserves to be set aside.

2. The Ld. Additional / Joint Commissioner of Income-tax (Appeals), ACIT JCIT(A)-1, Mumbai (‘Ld. CIT(A)’) erred in law and in fact to uphold the assessee has not furnished any documentary evidence and inertly stated the facts, which was not found to be satisfactory.

3. The Ld. CIT(A) erred in not adjudicating the Appellant’s submissions in a reasoned and judicious manner, thereby violating the principles of natural justice and resulting in a mechanical confirmation of the adjustments made in the Intimation under section 143(1) issued by the Li A DIT-CPC.

RE: GROUNDS ON MERITS

4. The Ld. ADIT-CPC erred in facts and in law by disallowing the amount of INR 13,22,458/- towards loss on sale of fixed assets, despite the fact that the same is already disallowed in the return of income in Schedule B? (Row 23). The said action by the Ld. ADIT-CPC has led to double disallowance of the same amount

5. The Ld. ADIT-CPC erred in facts and in law, by disallowing an amount of INR 10,41,545/- without appreciating that the said liability is a commercial liability taken over from the demerged entity under an approved scheme of arrangement

6. The Ld. ADIT-CPC erred in law and in facts by disallowing an amount of INR 10,41,545/-u/s 43B of the Act, towards provision for leave encashment, without appreciating the fact that the same has already been disallowed in the hands of the demerged company, thereby leading to double disallowance of the same amount

7. The above grounds are without prejudice to each other. The Appellant craves leave to add, withdraw, alter or modify, amend or vary of above grounds of the appeal before or at the time of hearing.

3. The brief facts of the case are that the assessee is a company, filed its original return of income for the Assessment Year 2019–20 on 30.10.2019, declaring total income of Rs.10,76,70,443/- under the normal provisions of the Income Tax Act, 1961 (“the Act”) and Rs.11,28,99,449/- under section 115JB of the Act. Subsequently, on 26.03.2020, the assessee revised its return of income only to modify disclosure in Schedule BP of ITR pursuant to a proposed adjustment under section 143(1)(a) of the Act. However, the income in the revised return was the same as declared in the original return. During the year, the assessee acquired the debt division of M/s. Caspian Impact Investment Advisor Pvt. Ltd. (“demerged company”) pursuant to a scheme of demerger approved by the Hon’ble NCLT vide order dated 24.10.2019. To give effect to the said demerger, the assessee again filed a second revised return of income on 30.09.2020 declaring total income of Rs.8,58,78,905/- under the normal provisions and Rs.8,42,68,147/- under section 115JB of the Act. The second revised return was processed by CPC under section 143(1)(a) of the Act on 09.03.2021. CPC made the additions of Rs.1,64,955/-under section 36(1)(iii), Rs.13,22,458/- under section 37(1) and Rs.10,41,545/- under section 43B of the Act, making a total adjustment of Rs.25,28,958/-.

4. Aggrieved with the order of the CPC the assessee filed appeal before the Ld. CIT(A). The Ld. CIT(A) confirmed all three additions made by the CPC.

5. Aggrieved with the order of the Ld. CIT(A), the assessee is now in appeal before us challenging only the addition of Rs.13,22,458/- under section 37(1) and Rs.10,41,545/- under section 43B of the Act. The Ld. Authorised Representative (Ld. AR) submitted detailed arguments both on the legal as well as on the merits of the case.

6. On the legal ground, it was submitted that the impugned adjustments made by CPC do not fall within the limited scope of adjustments permissible under section 143(1)(a) of the Act. Reliance was placed on the plain language of section 143(1)(a) to contend that disallowance of expenses debited to the profit and loss account, especially where detailed verification is required, is outside the scope of such adjustment. Therefore, the entire intimation issued by CPC under section 143(1)(a) is bad in law.

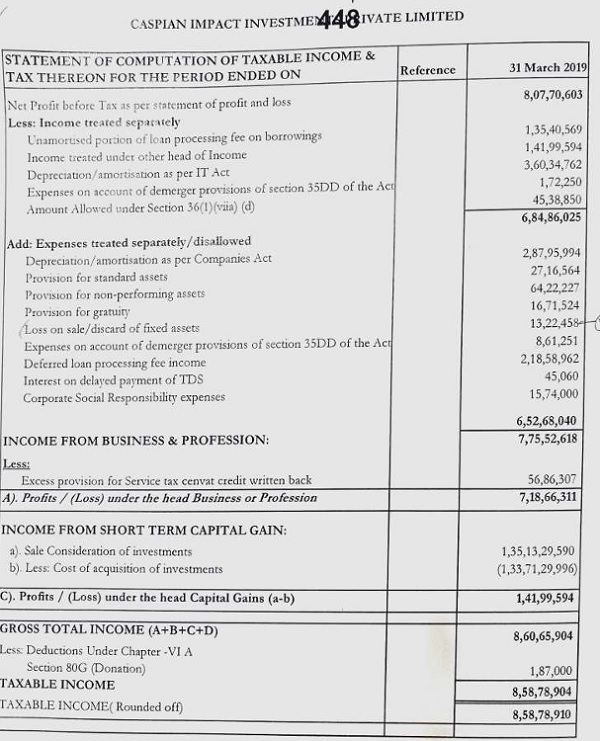

7. On the disallowance of Rs.13,22,458/- under section 37(1), the Ld. AR drew our attention to the computation of income placed at page no.448 of the paper-book. It was pointed out that the assessee had on its own already disallowed the said amount of Rs.13,22,458/- representing “loss on sale of fixed assets” while filing the return of income. However, CPC again made a disallowance of the same amount, which has resulted in double disallowance in the hands of the assessee. Since the assessee had already added back the said sum, there was no justification for CPC to make a further adjustment. Accordingly, the Ld. AR prayed before the Bench for deletion of Rs.13,22,458/- made by the CPC.

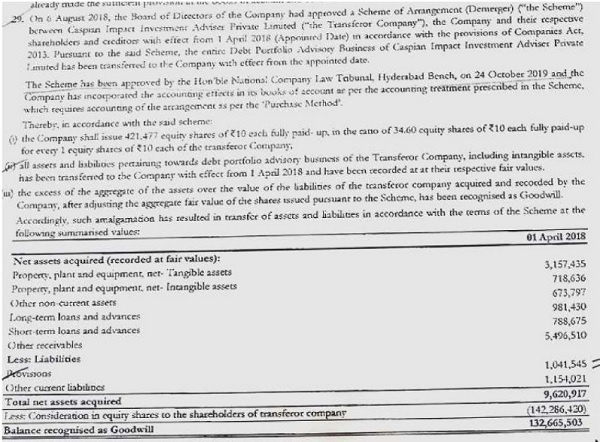

8. On the disallowance of Rs.10,41,545/- under section 43B of the Act, the Ld. AR invited our attention to Note No.29 of the audited financial statements, which records that a provision of Rs.10,41,545/- was standing in the books of the demerged company as on 01.04.2018. It was explained that pursuant to the scheme of demerger approved by the Hon’ble NCLT, the said provision got transferred to the assessee’s books. It was contended that since the provision was not created during the year under consideration, but was carried forward from earlier years of the demerged company, the provisions of section 43B could not be invoked in AY 2019–20. Accordingly, the Ld. AR prayed before the Bench for deletion of Rs.10,41,545/- made by the CPC.

9. Per contra, the Learned Departmental Representative (Ld. DR) supported the order of the Ld. CIT(A). It was submitted that before the Ld. CIT(A), the assessee could not furnish adequate evidence to substantiate its claim. The Ld. DR accordingly contended that the order of the Ld. CIT(A) deserves to be upheld. In the alternative, it was submitted that the issue raised by the assessee requires verification. Hence, the Ld. DR prayed that the issue may be remanded to the file of the Ld. AO for proper verification.

10. We have heard the rival submissions and perused the material available on record. On the disallowance of Rs.13,22,458/- under section 37(1) of the Act, we have gone through the page No.448 of the Paper Book which is to the following effect:

11. On perusal of the above, it is evident that the assessee had on its own disallowed the said sum in its computation of income while filing the return. Therefore, the adjustment made by CPC under section 143(1)(a) of the Act has led to double disallowance, which is not sustainable. Accordingly, the addition of Rs.13,22,458/- is directed to be deleted.

12. On the disallowance of Rs.10,41,545/- under section 43B of the Act, we have gone through the note No.29 of the Audited Financial Statement of the assessee, which is to the following effect:

13. On perusal of the above, we find that the assessee has adequately demonstrated through Note No.29 of the audited accounts that the provision stood in the books of the demerged company as on 01.04.2018 and was transferred pursuant to the scheme of demerger. No fresh provision was created during AY 2019–20. The adjustment under section 43B of the Act presupposes that a provision is created in the relevant year without actual payment. Since the provision in question pertains to earlier years, no addition can be sustained in the present year. We therefore hold that the disallowance of Rs.10,41,545/- under section 43B of the Act is unsustainable and the same is deleted.

14. On the scope of section 143(1)(a) of the Act, the Ld. AR raised a legal ground that the adjustments made by the CPC are beyond the scope of section 143(1)(a) of the Act. In view of our findings above, having deleted the additions on merits, the legal ground has become academic. Accordingly, we do not adjudicate on the same.

15. In the result, the appeal of the assessee is allowed.

Order pronounced in the Open Court on 3rd October, 2025.

Author Bio