“The existing system of scrutiny assessment in the IT department involves a high level of personal interaction between tax payer and the department which leads to certain undesirable practices and on the part of tax officials. To eliminate such instances, scheme of faceless assessment in electronic mode involving no human interface is being launched this year in phased manner”. – Current Finance minister Nirmala Sitharaman.

INTRODUCTION

This is the world of digitalization, with accessible internet, tech savvy citizens, and keeping in mind the perks of it, administrative departments in the country are on a pathway of digitalization. Physically operated administration practices are continously being upgraded to computerized version to improve efficiency and resource utilization. CBDT too, plays active role in the same. Time to time department keeps upgrading it services to make its functioning more effective and efficient. Lately, it has incorporated Income Tax Business Application (ITBA) project for electronic conduct of various functions/proceedings including e-assessment. Adding a feather to this cap, union budget 2019 proposed to introduce E-Assessment scheme, 2019.

HISTORY TRAILS AND RUDIMENTARY STEPS

Details of income is to be furnished by taxpayer by filling a return of income. Post filling, now the department processes the information for assuring its correctness. This process of examination return is called Assessment. Summary assessment u/s 143(1), Scrutiny assessment u/s 143(3), best judgment assessment u/s 144 or income escaping assessment u/s 147 are major assessments under IT act.

If history trails could be summarised, traditionally proceedings of assessment, right from selection and serving notice to completion of assessment were carried in physical manner. Digitalization swept in and e assessment was thought of in year 2015 which was on a pilot basis. Further, in the year 2017, ITBA project was rolled in and assesses were made to comply, first voluntarily and then necessarily for scrutiny u/s 143(3) after instructions published in 2018, through e-proceedings tab at designated portal.

From hardcopy submissions and physical representations, department now eyes to make assessments completely faceless, nameless and jurisdiction less. To add feathers of legality to this dream following steps were taken:

Through Finance Act 2018, Section 143 was amended to insert three new sub-sections (3A), (3B) and (3C). Section 143(3A) provides that CG may make scheme by notification in official gazette. 143(3B) enabled govt. to apply provisions of IT act, with such exception, adaptations and modifications as may be specified to give effect to scheme prescribed u/s 143(3A). 143(3C) provides that every notification issued under subsection 3A and 3B be laid before each of parliament as soon as issued.

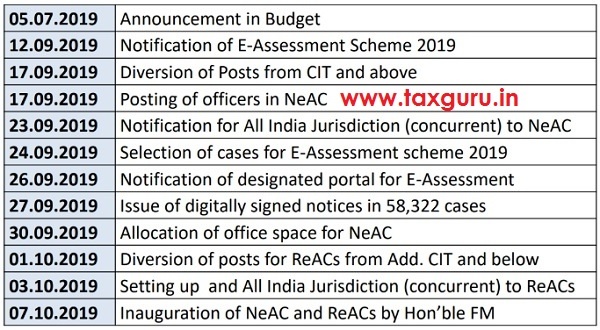

Later on, in budget speech on 5th July 2019 Finance minister made announcement of the faceless assessment scheme. Creation of dedicated assessment hierarchy for scheme followed.

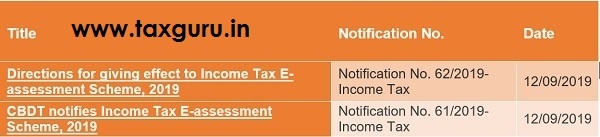

Finally, on 12th September 2019 notifications were issued by CBDT regarding e-assessment scheme 2019, which is to be launched in phased manner.

E-ASSESSMENT SCHEME, 2019

In the interest of revenue and to facilitate bonafide and hassle free assessment proceedings both on the part of assesse and department, CBDT has introduced E-Assessment scheme, 2019. let’s look at the backdrop and framework of the scheme as issued through notification no. 61/2019 and 62/2019.

IMPORTANT TERMINOLOGIES

“assessment” – assessment of total income or loss of the assessee u/s 143(3) of the Act

“automated allocation system” – algorithm for randomised allocation of cases, by using suitable technological tools

“automated examination tool” – algorithm for standardised examination of draft orders, with a view to reduce the scope of discretion

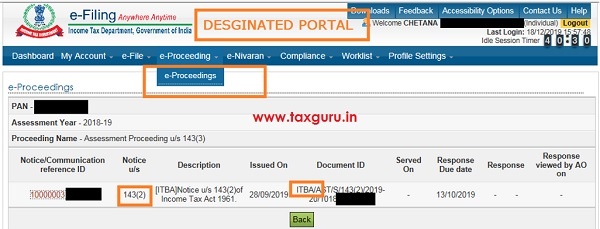

“e-assessment” – assessment proceedings conducted electronically in ‘e-Proceeding’ facility through assessee’s registered account in designated portal

“registered account” of the assessee – electronic filing account registered by the assessee in designated portal

“registered e-mail address” – e-mail address at which an electronic communication may be delivered or transmitted to the addressee, including- email address available at account in designated portal or in the last income-tax return furnished or in PAN database and further as specified in scheme.

Designated Portal – web portal designated by Pr. Chief Commissioner or Pr. Director General in-charge of NeAC.

SCOPE OF SCHEME

The assessment under this Scheme shall be made in respect of such territorial area, or persons or incomes or cases as may be specified by the Board.

E-assessment is not a special type of assessment; just that current assessments are being made electronic to enjoy perks of digitalization.

Reassessment u/s 147 is not covered and is still to be proceeded through offline mode.

Recently, it has been announced that over 58,322 cases have been picked under this scheme and e-notices for the AY18-19 have been served before 30/09/2019.

STRUCTURE

Board i.e. Central Board of Direct Taxes shall constitute for the purpose of this scheme: –

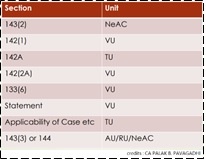

i. NATIONAL E-ASSESSMENT CENTRE (NEAC)

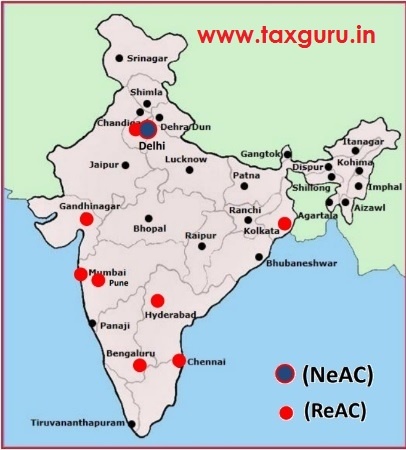

Constituted as a principal body to facilitate the means to and shall have jurisdiction to conduct assessment proceedings in an electronic mode. It shall be headed by Pr. CCIT and is located in Delhi. It shall specify format, mode, pjnal communication amongst them shall be mandatorily through NeAC and be exclusively through electronic mode.

ii. REGIONAL E-ASSESSMENT CENTRES (REAC)

Constituted (as it may deem necessary) to facilitate the means to and shall have jurisdiction to conduct assessment proceedings in the cadre controlling region of a Principal Chief Commissioner. It shall be headed by CCIT and there are 8 ReAC across country.

iii. ASSESSMENT UNITS

Constituted (as it may deem necessary) to perform functions of making assessment which includes:

- determination of any liability (including refund)

- seeking information or clarification from assessee on points or issues so identified

- analysis of material furnished by the assessee or any other person

- such other functions as may be required

iv. VERIFICATION UNITS

Constituted (as it may deem necessary) to perform functions of verification which includes:

- enquiry, cross verification, examination of books of accounts

- examination of witnesses and recording of statements

- such other functions as may be required

v. TECHNICAL UNITS

Constituted (as it may deem necessary) to perform functions of providing technical assistance which includes any assistance or advice on legal, accounting, forensic, information technology, valuation, transfer pricing, data analytics, management or any other technical matter.

vi. REVIEW UNITS

Constituted (as it may deem necessary) to perform functions of review of the draft assessment order, which includes:

- checking whether material evidence has been brought on record

- relevant points of fact and law, issues on which addition or disallowance should be made and applicable judicial decisions have been duly incorporated in the draft order

- checking for arithmetical correctness of modifications proposed

- such other functions as may be required

PROCEDURE

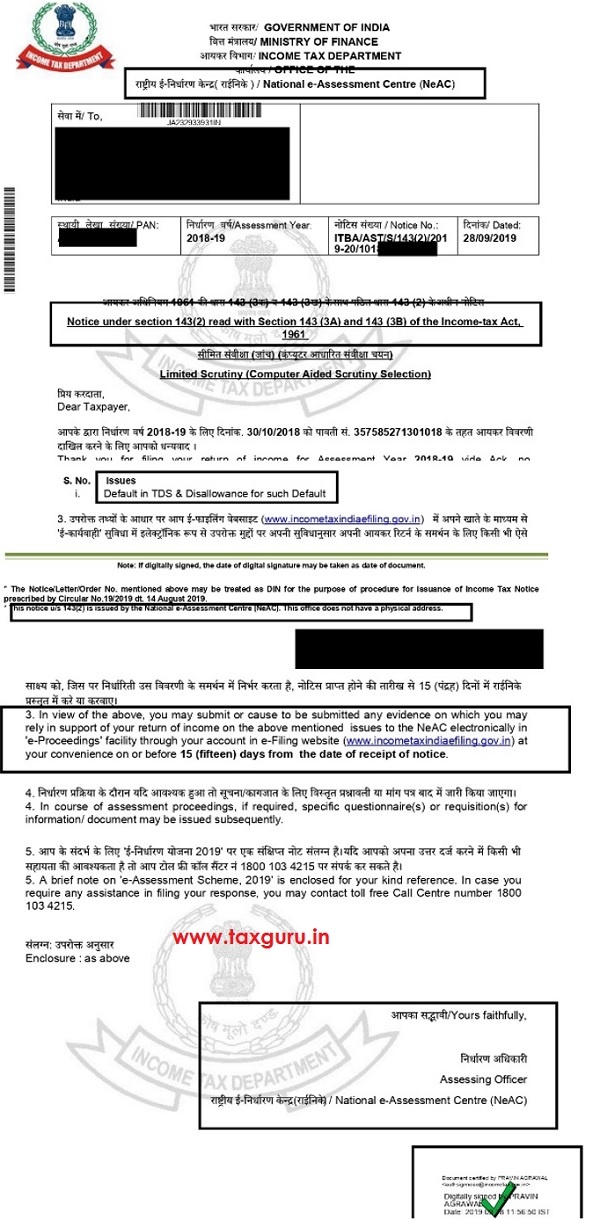

1. Once case is selected for assessment, NeAC shall serve notice u/s 143(2) with issues mentioned therein to the assessee.

Note: Every notice/ order/ other communication shall be delivered to assessee by placing it on assessee’s registered account or sending to his/AR’s registered email address or uploading on assessee’s mobile app followed by a real time alert in all cases.

2. Assessee shall file response within 15 days from the date of receipt of notice.

Note: The time and place of dispatch and receipt of electronic record shall be determined in accordance with the provisions of section 13 of the Information Technology Act, 2000.

Note: Assessee shall submit response through his registered account and upon generation of acknowledgement it shall be deemed to be authenticated.

3. Now, NeAC shall assign respective case through an automated system (randomised allocation of cases) to a specific assessment unit in any one ReAC.

4. Post assignment, Assessment unit shall request NeAC for

– Obtaining further information/ documents/ evidence from assessee.

Then NeAC shall issue appropriate notice or requisition to assessee for obtaining the information.

– Conducting enquiry or verification by verification unit.

NeAC shall assign function to a specific verification unit in any one ReAC through an automated system

– Seeking technical assistance from technical unit.

NeAC shall assign function to a specific technical unit in any one ReAC through an automated system

5. After examining all materials gathered, Assessment unit shall prepare a draft assessment order along with details of penalty proceedings to be initiated mentioned therein, either accepting or modifying the returned income of the assessee and shall send a copy to NeAC.

6. NeAC shall examine draft assessment order in accordance with the risk management strategy specified by the Board whereupon

a) It may finalise the assessment as per draft received, and serve copy of such order and notice for initiating penalty proceedings to the assessee along with demand notice or specifying refund if any; or

b) If modification is proposed, issue SCN to assessee as to why assessment shouldn’t be completed as per draft assessment order; or

c) Conduct review of order by assigning function to a specific review unit in any one ReAC through an automated system

7. Review unit shall either concur or propose modification to draft and send its decision to NeAC.

8. If NeAC receives concurrence, it shall follow procedure laid down in 6(a) or 6(b) above.

If NeAC receives suggestions for modifications it shall communicate the same to assessment unit, which then shall after considering modification prepare final draft order and send it NeAC. NeAC shall now follow procedure laid down in 6(a) or 6(b) above.

9. If SCN is issued to assessee as per 6(b) it shall respond to NeAC on or before the date and time specified in the notice

10. NeAC shall where no response is received from assessee, finalise assessment as per draft as per 6(a) or

in any other case, send the response received to assessment unit.

11. Assessment unit shall thereafter, considering response furnished, prepare revised draft assessment order and send it to NeAC

12. Upon receiving revised draft, NeAC shall finalise assessment as per 6(a) if modification is not prejudicial to interest of assessee or

if prejudicial it shall provide opportunity as per 6(b) and response furnished by assessee shall be dealt as per point 9, 10 and 11.

13. NeAC shall after completion of assessment transfer electronic record to assessing officer having jurisdiction over such case for:

14. NeAC may at any stage, if necessary transfer the case to respective AO having jurisdiction.

PENALTY PROCEEDINGS

Penalty proceedings can be initiated by any unit through NeAC for non-compliance of any notice, direction or order.

NeAC shall upon recommendation, serve SCN to assessee. And upon response, respective unit may wither draft order for penalty or drop penalty after recording reasons for same.

PROCEDURE FOR APPEAL

Appeal made against the assessment made by NeAC under this scheme shall be filled before the commissioner (appeals) having the jurisdiction over jurisdictional assessing officer.

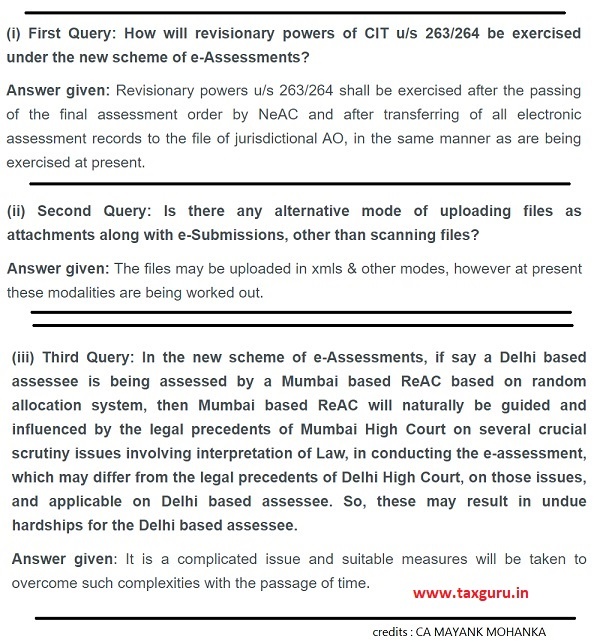

QUESTIONS ASKED IN WEBCAST CONDUCTED BY ICAI & NEAC

PERKS OF SCHEME 2019

a. Elimination of interaction between Assessing officer and Assessee to the extent technologically feasible – reduction of personal bias, harassment by tax officials, elimination of possibility of unauthorized practices such as corruption. Thus ensuring a greater transparency.

b. Reduction of red-tapism during the assessment proceedings.

c. Upgrading from traditional modes of administration, provides significant reduction in resource consumption. For both assessee and department, time is saved, resources used for physical storage, documentation, communication is significantly reduced. Thus providing ease of administration to department and ease of compliance to tax payer.

d. Unwanted personal bias, over pitched assessment, differences, resulting litigation cost is saved.

e. 24×7 accessibility and dedicated online cloud server make it hassle free to the assessee to comply from any part of country at any time.

f. Standardization as a result of digitalization, of reports, orders and proceedings provides for expeditious disposal of cases. Also providing economies of scale to the department.

g. Team based assessment with dynamic jurisdiction.

h. Significant potential to improve revenue collection by automation of processes.

i. Since submission is electronic, proof of submission remains with the assessee.

j. online system, which will use artificial intelligence, machine learning and technology tools to randomly and automatically allocate cases for assessment within the Income Tax Department.

k. Time gap between issue of notice or order and receipt by assesse in pre-electronic era can be mitigated.

DRAWBACK OF SCHEME 2019

a. Foundation of scheme is digitalisation of proceedings and records, but that comes with possibilities of technical glitches (file size limitations, emails becoming spams etc.) and issues for assesses not having sound technical knowledge. Unintended technical glitches may initiate unwanted penalty proceedings.

b. Differences in understanding may arise w.r.t. allocation of case to random assessment unit located in another part of country. Jurisdictional officer is much aware of trade practices, other administrative procedures and market of respective jurisdiction.

c. Issues may also arise in cases where frequency of one-to-one communication between officer and assessee is volatile in nature.

d. Submissions which are critical and extremely technical and confidential can be at risk of authenticity and genuineness. There may also arise a minute possibility of exposure of confidential documents to persons not known to assessee.

e. Bandwidth issues may also arise at remote areas of the country. Uneducated assesses which may prefer personal hearings over digitalisation. It also gives video conferencing option, but it still lacks a personal touch to proceedings.

f. Assesses shall be required to continously keep follow up and update their profile on designated portal.

g. Broad aspects of physical communication such as expressions, haptics, body language, gestures etc. are absent.

Faceless assessment is a great initial step towards making assessment procedure transparent and void of undesirable practices. Paying more attention to better technological setup and addressing the minutest issues by measures such as standardisation in calling data from assessee etc. shouldn’t be a big deal to department if proceed towards it at an early stage. Overall, E-assessment scheme 2019 or call it faceless assessment is a boon for the country. Income tax administration shall surely a revolution by ITBA project and now through great initiative of faceless assessment.

Author Bio

Under the E Assessment scheme, how many years books of account do we have to keep?