Case Law Details

Mohammed Kamran Vs Senior Intelligence Officer (Karnataka High Court)

Conclusion: Where State GST authorities have already initiated investigation into the same transactions, commencement of parallel proceedings by DGGI on identical allegations was impermissible and liable to be quashed.

Held: State GST authorities initiated proceedings against assessee by issuing summons under section 70 of the CGST/KGST Act alleging discrepancies in GST compliance and calling for production of books of account and other records. Assessee responded to the summons and furnished substantial documentary evidence during the ongoing investigation. While the State investigation was still pending, the Directorate General of GST Intelligence (DGGI) commenced an independent investigation on the basis of intelligence alleging fraudulent availment and passing of fake Input Tax Credit (ITC), conducted simultaneous searches and thereafter initiated criminal proceedings culminating in the assessee’s arrest. Assessee contended that once the State GST authorities had assumed jurisdiction and commenced investigation into the very same transactions, initiation of another investigation by DGGI on identical allegations amounted to parallel proceedings prohibited by the statutory scheme of the GST enactments. Such simultaneous investigations resulted in overlapping jurisdiction, abuse of process and violation of the principle embodied in section 6 of the CGST Act regulating exercise of concurrent jurisdiction by Central and State tax authorities. Revenue submitted that DGGI received independent intelligence indicating a large-scale fake ITC racket involving several interconnected entities. The investigation undertaken by DGGI was based upon independent material generated through Business Intelligence and Fraud Analytics, analysis of GST returns, common IP addresses, e-way bills and cancelled registrations revealing an organised syndicate involving fraudulent availment and passing of fake ITC exceeding ₹100 crore. Therefore, DGGI was fully competent to investigate offences under sections 69 and 132 of the CGST Act. High Court held that the statutory framework did not contemplate simultaneous investigations by two different authorities into the same cause of action once jurisdiction had already been assumed by one competent authority. Section 6 of the CGST Act seeks to avoid multiplicity of proceedings and conflicting investigations. Since the State authorities had already initiated proceedings and the subject matter substantially overlapped with the investigation commenced by DGGI, initiation of parallel criminal proceedings without any statutory justification was unsustainable.

Recent Cases

- G.K. Trading v. Union of India, 2020 SCC OnLine All 1907.

- Kuppan Gounder P.G. Natarajan v. Directorate General of GST Intelligence (DGGI), 2021 SCC OnLine Mad 17053.

- Anurag Suri v. Directorate General of GST Intelligence (DGGSTI), 2021 SCC OnLine Ori 2510.

- Indo International Tobacco Ltd. v. Vivek Prasad, 2022 SCC OnLine Del 90.

- Vivek Narsaria v. State of Jharkhand, 2024 SCC OnLine Jhar 50.

- Prabir Purkayastha v. State (NCT of Delhi), 2024 SCC OnLine SC 3229.

- M/s Armour Security (India) Ltd. v. Commissioner, CGST, Delhi East Commissionerate & Anr., 2025 INSC 982 (SLP (C) No. 6092 of 2025, decided on 14.08.2025).

- Radhika Agarwal v. Union of India, (2025) 9 SCC 329.

- Vihaan Kumar v. State of Haryana, (2025) 5 SCC 799.

FULL TEXT OF THE JUDGMENT/ORDER OF KARNATAKA HIGH COURT

The petitioner is before the Court seeking the following prayer:

1. “To issue a writ of certiorari or a writ or order or direction of appropriate in nature and quash the entire proceedings (as per Annexure-F) and complaint dated 12-11-2025 (as per Annexure-H) filed by respondent No.1 in Crime No.34/2025 in File No.DGGI/INV/125/ 2025-Gr-C-01 O/o Pr-ADG-DGGI-ZU – Bangalore which is pending on the file of Hon’ble Special Court for Economic Offences, Bangalore City as abuse of process of law insofar as petitioner is concerned.

2. To issue a writ of certiorari or writ or order or direction of appropriate writ in nature and quash the arrest of petitioner dated 16-09-2025 and consequent order of remand order dated 16-09-2025 (as per Annexure-‘F’) passed by Hon’ble Special Court for Economic Offences, Bangalore in Crime No.34/2025 in File No. DGGI/INV/125/ 2025-Gr-C-01 O/o Pr-ADG-DGGI-ZU – Bangalore as illegal and consequently release the petitioner forthwith insofar as petitioner is concerned.

3. To issue a writ of certiorari or a writ or order of direction of appropriate in nature and quash the order of cognizance dated 25-11-2025 (as per Annexure-F) passed in PCR No.280 of 2025 on the file of Hon’ble Special Court for Economic Offences, Bangalore which is in Crime No.34/2025 in File No. DGGI/INV/125/ 2025-Gr-C-01 O/o Pr-ADG-DGGI-ZU – Bangalore (as per Annexure-H), as illegal and abuse of process of law insofar as petitioner is concerned.

4. To pass such other order or orders as this Hon’ble Court deems fit to grant in the facts and circumstances of the case, in the interest of justice.”

2. Heard Sri Hashmath Pasha, learned senior counsel appearing for the petitioner, Sri Madhu N.Rao, learned counsel appearing for respondent Nos.1 and 2 and Sri B.N. Jagadeesha, learned Additional State Public Prosecutor appearing for respondent Nos.3 and 4.

3. The facts, in brief, germane are as follows: –

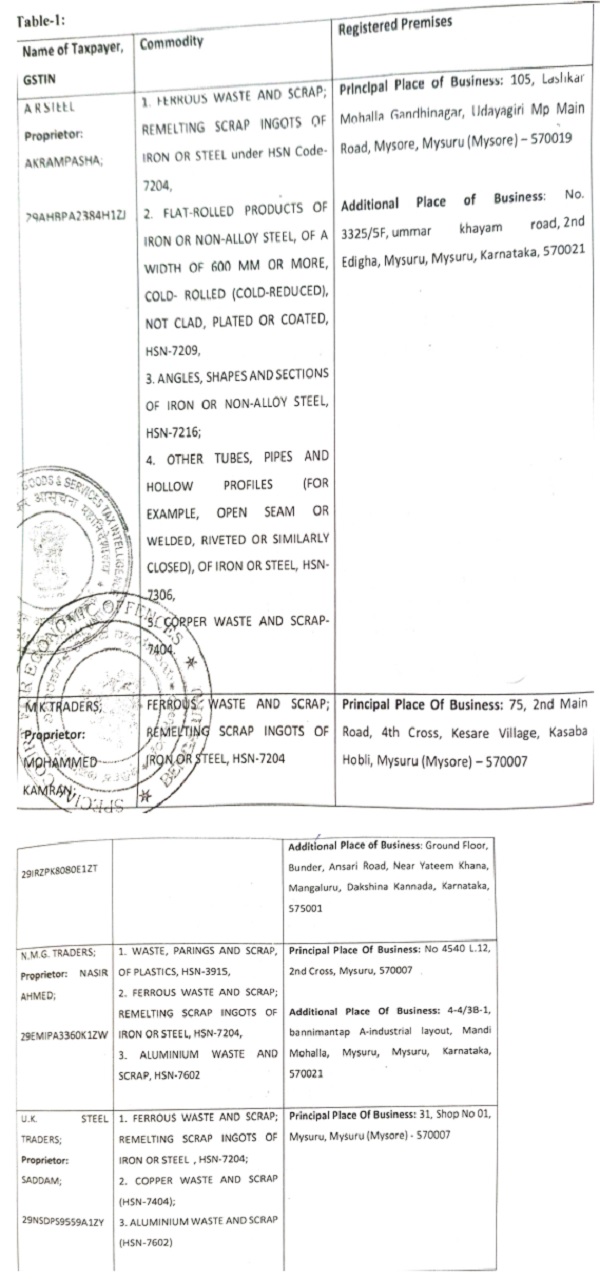

3.1. The petitioner is the proprietor of one M/s M.K. Traders engaged in the business of iron and steel waste scrap. The petitioner is said to have obtained Goods and Service Tax (‘GST’ for short) registration and used to buy scrap materials from different suppliers and sell them to registered manufacturers of steel and allied products.

3.2. On 14-05-2025, the 3rd respondent/Commercial Tax Officer and the 4th respondent/Joint Commissioner of Commercial Taxes commence investigation with respect to business transactions between the petitioner and one M/s A.R. Steels and two others –M/s N.M.G. Traders and M/s U.K. Steel Traders. On 17-06-2025, the 3rd and 4th respondents conduct inspection of the business spot where the accused runs his business. Thereafter, a notice is issued for commencement of formal investigation against the petitioner. The 4th respondent/Joint Commissioner of Commercial Taxes issues a notice alleging gross discrepancies in payment of GST and demanded production of invoices/documents concerning the business. Three months thereafter, in reply, the accused is said to have produced invoices and bills and other accounts pertaining to the payment of GST before the 3rd respondent.

3.3. When things stood thus, another notice is issued, now by the Central GST authorities/respondent Nos.1 and 2 on specific intelligence input indicating that the petitioner and his associate firms were involved in receiving fake invoices without actual receipt of goods or services from fictitious and non-existent suppliers. Based on the said intelligence input received, a report was generated through the Business Intelligence and Fraud Analytics platform under an early warning category. This results in conduct of a search of the premises, both residential and business premises of the petitioner/accused and his father under Section 67 of the Central Goods and Services Act, 2017 (‘the Act’ for short) leading to certain seizures. A case is registered in Crime No.162 of 2025 against the accused and his family by the Directorate General of GST Intelligence (‘DGGI’) for showing complete non-cooperation and obstructing the proceedings.

3.4. On 15-09-2025, the accused is asked to be present before the 1st respondent for interrogation. The accused then travels from Mangalore to Bangalore for the purpose of personal interrogation and is taken into custody the moment he reaches the Airport at Bangalore. Before the petitioner was taken into custody, the officers conducted a search on him and recovered from him 6 mobile phones and one laptop and arrested him at 6.30 a.m. on 16-09-2025. At about 8.55 p.m. on 16-09-2025, the accused was produced before the Court of Economic Offences, Bangalore along with the remand application. On 13-11-2025, the 1st and 2nd respondents file the prosecution complaint before the jurisdictional Court under Section 223 of the BNSS for offences punishable under Sections 132(1)(b), 132(1)(c), 132(1)(f) r/w 134 and 135 of the Act. The present petition is then preferred seeking to quash the proceedings in the private complaint so registered against the petitioner and hold the arrest of the petitioner to be illegal. The challenge is on the score that there cannot be dual proceedings on the same set of facts. In the interregnum, the application filed by the petitioner seeking default bail comes to be rejected. The petitioner then approaches a co-ordinate Bench of this Court in Criminal Petition No.16884 of 2025, wherein the plea of the petitioner for regular bail comes to be allowed.

4. The learned senior counsel Sri Hashmath Pasha appearing for the petitioner would submit that the petitioner/accused is subjected to parallel investigation in violation of Section 6(2)(b) of the Act. He would submit that the Apex Court in ARMOUR SECURITY (INDIA) LIMITED v. COMMISSIONER, CGST, DELHI EAST COMMISSIONERATE reported in 2025 SCC OnLine SC 1700 holds that parallel proceedings should not be instituted by another tax administration, when one tax administration has already initiated proceedings. The petitioner was taken into custody without furnishing grounds of arrest and reasons for arrest either orally or in writing which is violative of Article 22 of the Constitution of India and Section 47 of the BNSS. The arrest of the petitioner was neither informed to any relative nor his friend before he was produced before the Magistrate. The petitioner had explained all the deposits of input tax credit from business transactions. It is his submission that filing of partial investigation report is resorted to deny statutory bail to the petitioner in violation of Section 187(3) of the BNSS and Article 21 of the Constitution of India. The offences alleged against the petitioner are the ones punishable under Section 132 of the Act, which are punishable to a maximum of 5 years imprisonment. Therefore, the petitioner ought to have been issued notice prior to taking him into custody.

5.1. Contrariwise, the learned counsel Sri Madhu N. Rao appearing for the respondent Nos.1 and 2/DGGI would vehemently contend that the arrest was necessitated on account of non-cooperation of the petitioner and since the petitioner has previously fled from the premises when search proceedings were being conducted. The petitioner was arrested as there were reasons to believe that he had committed offences under Section 132(1)(c) of the Act. The investigation is conducted on the basis of the intelligence received by the DGGI and no notice is required to be issued to the accused before causing search proceedings. The intelligence input received by the GST authorities were placed before the Competent Authority, who after going through the intelligence developed by the concerned officer, issued authorization for search, and based on the authorization, search was conducted in the premises of the petitioner and allied concerns. The accused never showed any cooperation with the investigation and had fled the premises when search and seizure proceedings were being conducted. The accused was duly served the grounds of arrest and reasons for arrest in writing, which has been acknowledged by the petitioner and the mother of the petitioner/accused was also informed of his arrest.

5.2. Learned counsel would submit that whether parallel proceedings are being conducted by the State and the Central GST authorities cannot be determined now at the stage of investigation. The State GST authorities may have been inquiring into the discrepancies in the GST payment. Respondent Nos.1 and 2 are enquiring into the larger supply chain where around 140 suppliers are involved multi-fold revenue is at stake. Therefore, the two though may arise on the same facts, but for different reasons, which will be known only on completion of investigation. The judgment of the Apex Court in ARMOUR SECURITY, on which the learned senior counsel places reliance upon itself permits such investigation to be conducted. The Apex Court in the said judgment holds that inquiry or gathering of evidence or information would not become ‘proceedings’ under Section 6(2)(b) of the Act. Learned counsel would further submit that the investigation pending before the State GST authorities was transferred to the Central GST authorities/DGGI in accordance with the judgment of the Apex Court in ARMOUR SECURITY. Therefore, he would seek dismissal of the petition.

6.The learned Additional State Public Prosecutor Sri B.N. Jagadeesha would also toe the lines of the learned counsel Sri Madhu N.Rao in seeking dismissal of the petition on the score that investigation was transferred from the hands of the State GST authorities upon the filing of the prosecution complaint by the Central GST authorities/DGGI.

7. I have given my anxious consideration to the submissions made by the respective learned senior counsel, learned counsel and learned Additional State Public Prosecutor and have perused the material on record. In the light of the aforesaid submissions, the following issues would arise for consideration:

“(i) Whether the proceedings instituted by respondent Nos.1 and 2 against the petitioner in Crime No.34 of 2025 arising out of PCR 280 of 2025 deserve to be quashed?

(ii) Whether arrest of the petitioner is in violation of law which results in obliteration of proceedings?”

ISSUE NO.1:

Whether the proceedings instituted by respondent Nos.1 and 2 against the petitioner in Crime No.34 of 2025 arising out of PCR 280 of 2025 deserve to be quashed?

8.1. A notice comes to be issued by the State GST authorities to the petitioner on 17-06-2025 alleging discrepancies in payment of GST and demanding production of certain documents. Investigation qua the petitioner commences upon the issuance of the said notice. The reply of the petitioner to the said notice is as follows:

“Dt:09.09.2025

To

The Commercial Tax Officer, (Enf)-10, MZ-11

Office of the Joint Commissioner of

Commercial Taxes (Enf) No. 487, Bidaram

Krishnappa Road, Devaraja Mohalla Mysore

570024

From

M/s M.K. Traders

GSTIN: 29IRZPK8080E1ZT

75, 2nd Main Road, 4th Cross, Kesare

Village, Kasaba Hobli, Mysuru-570007

Email: mktraderskamran@gmail.com | Contact: 9110247185

Respected Sir,

Subject: Submission of records/books evidencing in response to Summons u/s 70 of CGST/KGST Act, 2017 – RFN: MA290725018233X, dated 04.07.2025.

With respect to the subject sited above, in the process of enquiry I attended on the date 10-07-2025 scheduled and I have given all the explanations in response to the enquiry made by you. But due to short duration I couldn’t evident the documents called for by your goodself. I hereby submitting the following books of accounts/records pertaining to M/s. M K Traders, GSTIN: 29IRZPK8080E1ZT for the following periods available as on today and other related records will be submitted as soon as our auditor arrives who is out of station.

1. Inward supply invoices & E-Way bills from October-2021 to December-2021 and October-2024 to June-2025.

2. Outward supply invoices & E-Way bills from Februry-2021 to December-2021 and October-2024 to June-2025.

3. Copies of Weighment slips and LR for outward supplies from October-2024 to June-2025.

4. Bank statement: Current A/c hold by me In Axis Bank having A/c No. 921020005135334, N.R. Mohalla Branch, Mysuru in the name of M/s. M K Traders from 01-10-2024 to 30-06-2025.

Thanking you.

Yours faithfully,

Sd/-

Mohammad Kamran

Proprietor-M.K. Trader”

During the pendency of investigation at the hands of the State GST authorities, officers of the DGGI-Central GST authorities commence investigation qua the petitioner/accused and his associate firms. The reason for commencement of investigation was that the DGGI had received specific intelligence input indicating that the petitioner/accused and his associate firms were involved in receiving fake invoices without actual receipt of goods or services from fictitious/non-existent suppliers. Based on intelligence input received, a report was generated through the Business Intelligence and Fraud Analytics platform under the early warning category. Analysis was from the data of GST returns, e-way bills, registration details to identify suspicious linkages of common logins and shared contact information. The report against the accused reveals that several suppliers had filed GST returns from common IP addresses and had issued invoices to common recipients indicating close interconnection or possible collusion. The GST status showed that many of the registrations from which transactions had taken place had already been cancelled. The major identities identified were M/s U.K. Steel Traders, M/s N.M.G. Traders, M/s M.K. Traders and M/s A.R. Steels. M/s M.K. Traders belongs to the petitioner. M/s A.R. Steels belongs to the father of the petitioner. A search then is conducted in the houses and business premises of those persons. The result of search is registration of a crime in Crime No.34 of 2025 before the jurisdictional Court. The petitioner was then directed to appear for personal interrogation and when appeared he was taken into custody on an application for remand. The application for remand is as follows:

“APPLICATION FOR REMAND OF ARRESTED ACCUSED The complainant most humbly prays as follows:

INTRODUCTION:

1. The Intelligence developed by the officer of Directorate General of Goods and Services Tax Intelligence, Zonal Unit, Bengaluru indicated that several entities including M/s. M.K. Traders, M/s. A.R. Steel, M/s. U.K. Steel Trader and M/s. N.M.G. Traders are involved in availing and passing on of inadmissible Input Tax Credit (ITC) on the strength of invoices issued by fictitious entities without associated supply of goods and/or services. As per the data available in the GST portal the commodity transacted by these entities is predominantly ‘ferrous scrap’. Discreet enquiries have revealed that majority of the premises pertaining to these entities are either non-existing or non operational. The GSTINs of majority of the impugned entities are cancelled suo moto ab-ignition by the department which further consolidates the suspicion of their involvement in fictitious transactions for availing and passing on inadmissible ITC on the strength of fake invoices. Analysis of the GST returns and corresponding E-waybills filed by the entities indicates that in majority of the cases the vehicle movement details are not available. It is also observed in certain cases that the vehicle was found to be moving on a different route other than the appropriate route for the E-waybill in which the said vehicle has been used. The quantum of evasion of GST by these taxpayers cumulatively amounts to over One Hundred Crores. The investigation proceedings are elaborated in ensuing paragraphs.

INTELLIGENCE:

2. Analysis of the data available in GST portal regarding the has led to unearthing of a syndicate of fictitious entities who had reported suspicious transactions viz. issuing of invoices without actual supply of goods/services. The details of four entities operating at Mysuru, Karnataka, under investigation by this office are tabulated as under:

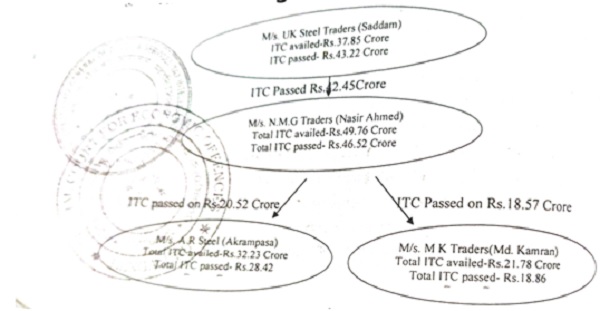

3. Intelligence gathered, indicated that the above four entities namely M/s A R STEEL, GSTIN- 29AHBPA2384H1ZJ, M/s. MK Traders, GSTIN- 29IRZPK8080E1ZT, M/s. N.M.G. Traders, GSTIN- 29EMIPA3360K1ZW and M/s. U.K. Steel Traders, GSTIN-29NSDPS9559A1ZY are registered with the department for supply of scrap. On perusal of intelligence, it appears that they are indulged in availing and passing on of fake ITC. A summary of the ITC availed and passed on by the impugned entities is tabulated as under:

Table:2

Amount in Lakh

| Name of Taxpayer | GSTIN | Status of GSTIN | Total ITC availed | Total ITC passed |

| U.K. Steel Traders | 29NSDPS9559A1ZY | Active | 3785.64 | 4,322 |

| N.M.G. Traders | 29EMIPA3360K1ZW | Active | 4976.23 | 4,652 |

| M K Traders | 29IRZPK8080E1ZT | Active | 2178.73 | 1,886 |

| A R Steel | 29AHBPA2384H1ZJ | Active | 3223.61 | 2,842 |

| Total | 14164.21 | 13,702 |

On the basis of the above intelligence and analysis, investigation was initiated, and searches were carried out at the registered premises of the above entities. The details of investigation proceedings are elaborated in the following paragraphs.

INVESTIGATION:

4. In pursuance to the outcome of analysis of the GST returns of the impugned taxpayers, searches were carried out under section 67 of the Central Goods and Services Tax Act, 2017 at the registered premises of the said taxpayers and the residential premises of the individuals related to the said taxpayers. The Taxpayer-wise discussion of their involvement in the syndicate of entities indulged in the availing and passing on of inadmissible ITC, outcomes of the searches at their premises and other evidences are discussed as under-

i. M/s. U.K. Steel Traders:

a. The TP was registered with the GST department on 09-09-2021. Their registration is active as on date. Shri Saddam is the proprietor of M/s U.K. Steel Traders.

b. GSTR2A returns of this TP indicates that they have availed input tax credit of Rs. 37,85,64,955/- from various suppliers, out of which Rs.29,76,30,325/- has been received from suppliers which are Suo-moto cancelled/ or cancelled on application of taxpayer and Rs.8,09,34,629/- has been received from the suppliers whose GSTIN is Active but most of the suppliers at Level-2 (inward supply) are found to be cancelled by the department or cancelled by the taxpayer on application within a brief period after obtaining registration.

c. It is pertinent to mention here that amongst the Active Suppliers of M/s U.K. Steel Traders, suppliers viz. 5star Traders (GSTIN-29FCZPA6147JIZU), RMS Enterprises (GSTIN-29BOFPR7678M1ZS), AHB Enterprises (GSTIN-29EWQPA9619P1ZG), Fortune Enterprises (GSTIN- 29JATPK3193N1ZI), A R Traders (GSTIN- 29FDEPA7685H1Z5), P VR Traders (GSTIN-29COBPV6331L1ZD). Junaid Enterprises (GSTIN- 29CIUPJ8764L1Z1), Blue Enterprises (GSTIN- 20 29FKXPK2789A1ZG), R S Selvam Traders (GSTIN-29CSYPV9104Q1Z7), do not have Input Tax Credit to the extent they have passed on to their recipients.

d. The entities mentioned above are into the business of sale and purchase of scrap. In the absence of adequate inward supplies at the suppliers end, the outward supplies cannot be affected and thus indicating clearly that the said supplier entities are generators of fake input tax credit in the chain. Thus, since the inward supplies as well as outward supplies of M/s UK Steel Traders appear to be dubious without actual accompanying supplies of goods (and/or services).

e. The taxpayer has passed on ITC of Rs.42,45,53,127/- to M/s. N.M.G Traders which accounts to 98% of outward supplies of M.s U.K. Steel Traders.

f/ Search of the principal place of business of M/s U.K. Steel Traders located at 31, Shop No 01, Old Kesare, Mysuru, Karnataka, 570007, was carried out on 10-09-2025 under Authorization for search bearing CBIC-DIN- 202509DS0000000D412 dated 09-09-2025 under section 67(2) of the CGST Act, 2017. During the search proceedings at the above premises was occupied by other unconnected entity and that M/s U. K. Steel Traders was not existing in the said premises. Enquiry with the owner of the said premises revealed that the said owner did not know any Saddam or his Firm and has never entered into any rental agreement to let out his premise to them. On perusal of rental agreement uploaded during request for revocation of suo-moto cancelled GSTIN, the name of owner of the premises as per the rent agreement was mentioned as Abdul Aleem whereas actual owner of the said premises was found to be ‘Shri Ramana’. The registered mobile number -7483520394 of M/s U.K. Steel Traders was found to be switched off.

g. Further, search of the residence premises of Shri Saddam, Proprietor of M/s U.K. Steel Traders located at 410 Azmatulla Bharath Nagar Sathgalli Badawane KAMYS 570019, was carried on 10-09-2025 under Authorization for Search bearing CBIC-DIN-202509DS00000722019 dated 09-09-2025. During search, it was found that the said premise was occupied by one Smt. Asma Jabin on rent from Smt. Kushter Banu. On being called by the Officer, Smt. Kushter Banu submitted that the premise has never been rented to Shri Saddam and does not have any relation to him. (MAHAZAR)

h. The above search of the principal place of business and residential premises of the proprietor of M/s U.K. Steel Traders and their availing of ITC on the strength of bogus invoices without actual supply of goods indicates dubious nature of transactions reported by them. Therefore, M/s U. K. Steel Traders appears to be a fake entity floated with sole intention of availing and passing on of inadmissible ITC on the strength of invoices without actual receipt of goods and/or services. (MAHAZAR)

ii. M/s. N.M.G.Traders (GSTIN-29EMIPA3360K1ZW)

a. The TP is registered with the department since 2022-0517. Their registration is active as on date and Shri Nasir Ahmed is the proprietor of the taxpayer.

b. As per GSTR2A registration The taxpayer has received total ITC of Rs.49,76,23,850/-from 18 suppliers (as per inward supply statement GSTR-2A). Major supplier is M/s. U.K. Steel Traders who alone have passed on ITC of Rs.42,45,53,127/- to M/s. NMG Traders. Remaining 13 suppliers are cancelled suo-moto by the department.

c. The taxpayer has passed on ITC of Rs. 46.52 Crore to various recipients and major recipients are ACTIVE.

d. The major recipient is M/s. A R Steel (GSTIN-29AHBPA2384HIZJ) who have received input tax credit of Rs.20,52,39,822/- from M/s. N.M.G Traders. The other recipient, M/s. M K Traders (GSTIN-29IRZPK8080E1ZT) has received ITC of Rs.18,57,88,319/- which is Active.

e. Search at the principal place of business of M/s N.M.G Traders located at No 4540 L.12, 2nd Cross, N.R Mohalla, Mysuru, Karnataka, 570007, was carried out on 10-09- 2025 under Authorization for search bearing CBIC-DIN-202509DS0000061186A dated 09-09-2025. During search proceeding, the said premises was found to be empty and upon enquiry from the owner of the premises, no business activity was conducted at the premises in past months. (MAHAZAR).

f. Search at the additional premises of M/s N.M.G Traders located at 4-4/3B-1, bannimantap A industrial layout, Mandi Mohalla, Mysuru, Karnataka, 570021 was carried out on 10-09-2025 under Authorization for search bearing CBIC-DIN-202509DS00000555C0E dated 09-09-2025. During search proceeding, the said premises was found to be closed and on being contacted over registered mobile number, no response was found and hence the premise was sealed in the presence of independent witness. It appeared that the no business activities were carried out on the said premises. (MAHAZAR)

g. In view of the above, it appeared that M/s N.M.G. Traders is a fictitious entity floated with sole intention to avail and pass on inadmissible ITC without actual supply of goods and/or services.

h. The search proceedings at the residential premises of proprietor of M/s N.M.G Traders is elaborated at Para-6 below.

iii. M/s. M K Traders (GSTIN-29IRZPK8080E1ZT): (Legal name-Mohammed Kamran):

a. M/s M K Traders is registered with the department since 01-02-2025 and Shri Mohammed Kamran S/o Akram Pasha.

b. The taxpayer has received total inwards supply of Rs. 21,78,73,544/- from the various suppliers, out of which Rs. 2,53,04,402/- has been availed from the suo-moto cancelled taxpayers.

c. Further, the taxpayer has received inward supply with ITC of Rs. 18,57,88,319/- from one major supplier namely M/s. N.M.G Traders.

d. Search at the registered principal place of business of premises of M/s M.K. Traders located at 75, 2nd Main Road, 4th Cross, Kesare Village, Kasaba Hobli, Mysuru, Karnataka, 570007, was carried out on 10-09-2025under Authorization for Search bearing CBIC-DIN- 202509DS0000000E37E dated 09-09-2025. During Search proceeding, the premise was found to be locked. The officer on search tried to contact the Prop. On the registered mobile number but no response was found and hence, it was sealed in the presence of independent witness. It appeared that no business activity was being carried out on the said premises. (MAHAZAR)

e. The proceedings at the residence of the proprietor of M/s M.K. Traders is elaborated at para-6 below.

5. For ease of understanding, the supply chain is illustrated in the following flow chart:

6. During investigation, simultaneous searches were carried out at the registered principal places, additional places and available residential premises of the proprietors of the above-mentioned entities. The outcome of the searches of the principal places of business and additional places has been discussed at Para-4 above while describing the nature of transactions undertaken by M/s. M.K. Traders, M/s. A.R. Steel, M/s. U.K. Steel Trader and M/s. N.M.G. Traders. The search proceeding at the residential premises of the proprietor of the said entities is elaborated as under:

i. Search at the residential premises of Shri Mohammed Kamran (Prop: M.K. Traders) and Shri Akrampasha (Prop: AR Steel).

a. As per the information available on the GST portal the residence of the proprietors of AR Steel and MK Traders is same since both are father and son viz. Akram Pasha is father of Mohammed Kamran. The declared residential address as per the GST portal is located at House No. LIG 61, 3rd Stage, Bannimantapa, Mysore, Karnataka-570015. However, discreet enquires revealed that the actual residential address of Shri Akrampasha (Prop: AR Steel) and Shri Mohammed Kamran (Prop: M.K. Traders) is located at 7, Bannimantap A Layout, Bannimantap, Mysuru, Karnataka 570015. Regardless, the search of both the premises was conducted by the officers.

b. Accordingly search at the declared residence of Shri Akrampasha (Prop: AR Steel) and Shri Mohammed Kamran (Prop: M.K. Traders) is located at LIG 61 Mysuru Banni Mantap Road KAMYS 570015, was carried out on 10-09-2025. During search, it was found that the said premises was occupied by one Shri Nadeem Ahmed and his family. During search, the forensic imaging of the mobile phone of Shri Nadeem Ahmed was done by the forensic examiner. The search was going smoothly till around 1:30 PM. However, at around 1:30 PM, two people claiming to be brothers of Shri Mohammad Kamran forcibly entered in the said premises under search and disrupted the proceeding. They forcefully pushed the officers out of the said premises. Taking advantage of the situation, Shri Nadeem Ahmed assaulted the officers present at the premises and fled the search premises. The proceedings at the premises during search are recorded in the Mahazar drawn on the spot and the same is enclosed as Document No.1 to this petition.

c. Further, search of the residential premises of Shri Akrampasa and Shri Mohammed Kamran located at 7, Bannimantap A Layout, Bannimantap, Mysuru, Karnataka 570015, was carried out 10.09.2025 under Authorization for Search bearing CBIC-DIN- 202509DS0000000DAA4 dated 09-09-2025. During search proceedings, the officer when Knocked the door for opening the premises, no response was received for about one hours. After much persuasion, the door was opened by Shri Mohammed Kamran who was shown the search authorization. After reading and acknowledging the same, he allowed the officer to search the premises. On enquiry about the family members present in the house and especially about Shri Akrampasa, they informed about the presence of Shri Mohammed Kamran, his mother, Sister, brother, Wife and one infant. With regard to Shri Parampasa, they informed that he is not in the house. The officer started looking after the recording of CCTV to find out the possible reason for delay in opening the door. From the recording, it was known that Shri Akrampasa was visible on the terrace and managed to jump to the adjacent building and escaped from there on one scooter with the help of one unidentified Aides. While officer started recording statement of the Shri Mohammed Kamran, he started showing aggression and after some time his brother and other family members took their mobile phone one after another and made calls to their accomplices. Soon thereafter, people on the bikes arrived at the premise and pretended to be from Media and started shouting over officers. Within no time many people gathered outside the premises and entered into premise under search. While the officers present were busy in calming down the mob and Shri Kamran took advantage of the mob and escaped from the premises. Meanwhile, the family members took out the segregated documents by the officer which appears to be incriminating for the evidence purpose. Later, while the forensic examiner was sealing the Hard disk of CCTV, Smt. Farzana banu, mother of Kamran, snatched the hard disk from his hand and entered into one of the room adjacent hall on the Ground floor and locked herself and attempted to destroy the said hard disc as was evident from the sound coming from the room. Thereafter, Shri Umar and his sister entered into the said room and after coming out from the room, they forcefully fled the premises with the said hard disc. Later, when police came and situation was brought to the control, they offered to search again the rooms for documents and missing DVR/Hard disk. However, the segregated documents and hard disk could not be found there which confirmed that the said documents and DVR/Hard disk were taken away by the accomplices of Shri Mohammed Kamran and Shri Akram Pasha. The i-phone of Shri Kamran could not be subjected to forensic examination as he was reluctant to open it even after much persuasion from the officer. While escaping from the house, he took the mobile with him. However, one macbook which was locked with the ID of Shri Mohammed Kamran and one Pendrive alongwith some hand written paper, unsigned Financials were seized from the premises under Mahazar drawn on the spot. Thus, the search proceeding completely disturbed and obstructed by Shri Kamran, his brother, Shri Umar and the family members. The entire proceedings were recorded under Mahazar drawn on the spot which is placed as Document No.2 to this petition.

d. Later, was learnt that the group of people headed by Shri Mohammed Umar and his brother visited the other two residential locations in synchronized manner and helped in escaping of Shri Nadeem Ahmed and Shri Nasir Ahmed from their respective premises where the search proceedings were already under progress.

ii Search at the residential premises of Shri Nasir Ahmed (Prop: N. M. G. Traders):

a. As per Search Authorization bearing CBIC-DIN-202509DS00000444A72 dated 09-09-2025, search operation was conducted at No 408 EWS Mysuru 2nd Stage KAMYS 570015 residence address of M/s. NMG Traders by the Authorized officer, Shri Randhir Kumar Singh, SIO and Team on 10-09-2025. During Search proceeding, it was found that the said premise was occupied by Shri Nasir Ahmed, Prop. Of M/s. N.M.G Traders and his family. During the search proceedings, Shri Umar and friend of Umar entered into the premises forcibly and started shouting over the officers and disturbed the search proceeding. Also, they took out Shri Nashir Ahmed out of the premises with them. During the initial enquiry with the Prop. Nashir Ahmed, it was known that the business of M/s. N.M.G Traders are dealt by Shri Mohammed Kamran, prop. Of M/s. M. K. Trader. Such submission was recorded in the video taken during the investigation but the recorded statement in writing could not be signed by Shri Nasir Ahmed due obstruction caused by Shri Mohammed Umar (the brother of Kamran) and his associates who forcibly took him with them. The proceedings at the premises during search are recorded in the Mahazar drawn on the spot which is placed as Document No.3 to this petition.

7. As elaborated above, the search proceedings at the premises were disrupted by a group of people which were apparently mobilized by Shri Akram Pasha, who had fled the premises before the search at the said premises could even begin and by his son Shri Mohammed Kamran who did not cooperated in the search proceedings and made calls during the search after which the mob intruded in the premises under search and assisted Shri Mohammed Kamran in fleeing the premises during ongoing search proceedings. Shri Mohammed Umar (brother of Shri Mohammed Kamran) and other members of family of Shri Mohammed Kamran have played pivotal role in destruction of evidence, escaping of key persons and manhandling and threatening the officers of search party. Following the above incidents two FIRs 0161/2025 and 0162/2025 were filed on 10-09-2025 at the N R Police Station for obstructing the proceedings, destroying the evidence, misbehaving with the officers on duty, manhandling and assualting of officers on duty and other offences, under section 132.121(1),122(1), 208, 210, 212, 214, 218, 221, 224, 238, 241, 351(1), 352,r/w3(5) of BNS,2023. The FIRs are placed as Document No.4&5 to this petition

8. STATEMENTS

8.1 During the search proceedings, statements were sought to be recorded under Section 70 of the Central Goods and Services Tax Act, 2017, particularly at the residential premises of Shri Mohammed Kamran and Shri Nasir (Hussain/Ahmed). Shri Mohammed Kamran, from the outset, adopted an evasive and non-cooperative stance and, during the course of the proceedings, fled his residence with the assistance of a mob. At Shri Nasir’s premises the recording initially proceeded peacefully, Shri Nasir admitted on record that he is the proprietor of M/s NMG Traders but that Shri Mohammed Kamran managed the firm’s entire operations – including the filing of returns and handling departmental queries – and paid Shri Nasir regular sums for the use of his identity in running the firm. Thereafter, persons allegedly acting on Shri Kamran’s directions reached Shri Nasir’s premises, abused the officers, obstructed the proceedings and facilitated Shri Nasir’s escape, thereby preventing continuation of the statement recording.

8.2. An Authorization for Search bearing CBIC-DIN-202509DS$000007227B9 dated 16-09-2025 was obtained under section 67(2) of the CGST Act, 2017 for causing search/seizure duly authorized by the Additional Director of DGGI, BZU. Accordingly, search proceedings were conducted at Kempegowda International Airport for searching the personal belongings of Shri Mohammed Kamran and the proceedings were recorded under Mahazar dated 16-09-2025. In accordance with the Mahazar, there was an order of seizure in Form GST-INS02 wherein 6 mobile phones and one Dell Inspiron laptop were seized.

8.3 Subsequently, a statement of Shri Mohammed Kamran was recorded under Section 70 at Kempegowda International Airport, Bengaluru on 16.09.2025; he again remained evasive and non-cooperative, though the statement was duly recorded. The said statement dated 16.09.2025 of Shri Mohammed Kamran is placed as Document No.6 to this petition.

9. EXAMINATION AND ANALYSIS OF THE EVIDENCE SEIZED DURING INVESTIGATION:

i. During the search proceedings at the residence of Shri Mohammed Kamran, located at 7, Bannimantap A Layout, Bannimantap, Mysuru, Karnataka – 570015, one MacBook, a pendrive, and certain documents were seized. Forensic imaging of these electronic devices is required to be carried out in the presence of Shri Mohammed Kamran. Among the seized documents, a handwritten account detailing date-wise payments made to various persons was found. These entries appear to reflect cash transactions routed through intermediaries, as each entry mentions the names of two individuals. In addition, unsigned trading/financial statements of M/s A.R. Steel (Prop. Akram Pasha) and M/s A.K. Steel Traders (Prop. Shri Abdul Asif) were also found at the premises.

ii. It is noteworthy that M/s A.K. Steel Traders (Prop. Abdul Asif, GSTIN 29DSQPA7479L1ZR) is a suspended entity, which also appears in the list of suppliers to M/s M.K. Traders (Prop. Mohammed Kamran). Shri Abdul Asif is part of a wider supply chain that includes suo-moto cancelled suppliers, namely M/s M.Z. Traders (GSTIN 29DPRPR6133E1ZD) and M/s Μ.Κ. Enterprises (GSTIN 29GECPM7261H1Z4). Together, these two entities have availed/passed ITC to the extent of `54 crore. The availability of unsigned financial documents of Shri Abdul Asif at the premises of Shri Akram Pasha and Shri Mohammed Kamran strongly indicates a nexus among them, which requires further investigation.

iii. With regard to the forensic imaging of data extracted from the mobile phone of Shri Nadeem Ahmed, the following facts have emerged:

-

-

-

-

- Two digital images of rubber stamps were found, one in the name of A. Traders, #161, 1st Stage, Mysore, Karnataka – 570019, GSTIN 29EAMPA0528R1Z7, and another with the impression “For N.A. Traders.”

- On verification of GSTN records, GSTIN 29EAMPA0528R1Z7 was found to be registered in the name of Shri Nadeem Ahmed with trade name M/s N.A. Traders, which is currently “Active.” However, no inward or outward supplies have been reported for the past four years, and only NIL returns have been filed.

-

-

-

iv. Further, on perusal of WhatsApp chats, it was seen that Shri Nadeem Ahmed is in regular contact with a user saved as ‘Kamran..one‘ (mobile number 9110247185), which pertains to Shri Mohammed Kamran. The chats, primarily in audio format, contain multiple instances of confirmation of payments made by Shri Nadeem Ahmed to various persons. Additionally, Shri Nadeem Ahmed was found reporting payment confirmations through audio chats to:

-

-

-

-

- “Mueez..Kamran‘ (mobile number 9110255504), believed to be Shri Mohammed Mueez Ulla Shariff, and

- “Shoiab.. Office‘ (mobile number 8660641723), believed to be Shri Mohammed Shoib Hussain.

-

-

-

v. From the evidence available, Shri Nadeem Ahmed appears to be handling cash transactions, as reflected in the audio confirmations of payments made to various persons.

10. SUMMARY OF PROCEEDINGS:

i. During the search proceedings at the residential premises in Mysuru of Shri Akram Pasha (Proprietor, M/s A.R. Steel), Shri Mohammed Kamran (Proprietor, M/s M.K. Traders), and Shri Nasir Ahmed (Proprietor, M/s N.M.G. Traders), deliberate obstruction was caused with malafide intent and attempts were made to destroy evidence. Shri Mohammed Kamran and his father, Shri Akram Pasha, managed to escape during the entry of officers for search. Shri Mohammed Umar, brother of Shri Kamran, played a key role in organizing an agitation together with Shri Kamran, which facilitated the escape of Shri Nadeem Ahmed and Shri Nasir Ahmed. The synchronized nature of the escapes clearly indicates close nexus among all the proprietors – Shri Mohammed Kamran, Shri Akram Pasha, Shri Nadeem Ahmed, and Shri Nasir Ahmed – with Shri Kamran emerging as the mastermind, as all agitation and escapes (except that of Akram Pasha) occurred after Kamran and his brother Umar absconded during the search of their premises.

ii. The principal and additional places of business of the above entities were found locked, with no signs of active business operations at multiple locations. Further, documents seized during the searches reveal that Shri Akram Pasha is also the proprietor of M/s A.R. Traders, and unsigned financial documents of M/s A.K. Steel Traders (Prop. Abdul Asif), along with handwritten records of payments, point to their nexus with multiple firms. The material collected during the searches corroborates the intelligence gathered by this office that the four entities mentioned above are engaged in passing on fake Input Tax Credit (ITC). The evidence also indicates that Shri Mohammed Kamran, is the masterminds behind the Operation of these entities.

iii. Additionally, during the search, it was found that the declared residential premises of Shri Akram Pasha and Shri Mohammed Kamran was in fact occupied by their uncle, Shri Nadeem Ahmed, who appears to be handling cash transactions for them, as evidenced from WhatsApp/audio-recordings recovered during

investigation.

iv. From the above investigation and findings, it is revealed that Shri Saddam (Prop. M/s U.K. Steel Traders) had availed Input Tax Credit (ITC) from entities which were subsequently cancelled suo-moto by the department. The ITC passed on by these entities appears to have been availed on the strength of fake invoices without any actual supply of goods. Shri Saddam further passed on such ineligible credit to M/s N.M.G. Traders. In his statement (which could not be signed due to obstruction caused by Shri Mohammed Kamran, his brother, and their aides), Shri Nasir Ahmed (Prop. M/s N.M.G. Traders) stated, in response to a query regarding the suo-moto cancelled suppliers of his firm:

“I am not aware about these suppliers of my firm M/s N.M.G. Traders and I am not in contact with any of them, as Mohammed Kamran alone handles all the sales and purchase related transactions.”

Further, WhatsApp chats of Shri Nadeem Ahmed confirm that he was reporting payments made to various persons. These chats indicate that Shri Mohammed Kamran is the mastermind in the chain, having engaged these entities for passing on fake ITC.

11.1 In view of Clause (c) of Sub-section (1) of Section 132 as above, any person “who avails input tax credit using such invoice or bill referred to in clause (b) or fraudulently avails input tax credit without any invoice or bill;” shall be punishable in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilized or the amount of refund wrongly taken exceeds five hundred lakh rupees, with imprisonment for a term which may extend to five years and with fine;

11.2 Further as per Section 132 (5) of the CGST Act, 2017, the offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) and punishable under clause(i) of that sub-section shall be cognizable and non-bailable.

11.3. Further as per Section 69(1) of the CGST Act, 2017, “Where the Commissioner has reasons to believe that a person has committed any offence specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) of section 132 which is punishable under clause (i) or (ii) of sub-section (1), or sub-section (2) of the said section, he may, by order authorize any officer of Central tax to arrest such person”.

12. Further, in view of the incidents during the search proceedings dated 10.09.2025 particularly the acts of absconding from premises and attempts to obstruct/destroy evidence is a grave apprehension that if the above-named persons are left at large, they will tamper with crucial evidence, threaten/coerce witnesses, and thereby frustrate the course of investigation. It is also pertinent that several sets of documents and digital records are yet to be recovered, examined, and verified, which are essential to quantify the full extent of tax evasion and identify – the entire beneficiary network. Their custodial interrogation is, therefore, indispensable to safeguard the integrity of the investigation.

13. The facts brought on record indicates that, Shri Mohammed Kamran, is the mastermind responsible for commission of offences under clause (c) of sub-section (1) of Section 132 of the CGST Act, 2017, which are punishable under clause (i) of the said sub-section with imprisonment up to five years and fine. The offences committed by them are cognizable and non-bailable in terms of Section 132(5) of the Act. Therefore, Shri Mohammed Kamran was clearly liable and therefore arrested under Section 69(1) of the CGST Act, 2017, in order to secure their custodial interrogation, prevent further destruction of evidence, and protect the interest of revenue.

14. The above-mentioned firms appear to be non-existent or do not carry out any active business at their registered premises, as established during the search proceedings. Further, it is evident that these firms, including M/s MK Traders, have availed Input Tax Credit (ITC) without actual supply of goods and/or services. Verification from the GSTN back office also indicates that the registrations of most of the suppliers to these entities were cancelled on account of availment and passing on of ineligible ITC or due to non-existence of business premises.

15 ROLE OF SHRI MOHAMMED KAMRAN:

i. Investigation indicates that Shri Mohammed Kamran, S/o Shri Akram Pasha, Proprietor of M/s. MK Traders (GSTIN-29IRZPK8080E1ZT) has fraudulently availed ineligible input tax credit (ITC) of ₹21.11 crores approx, without actual receipt of goods or services. Out of the same, ineligible ITC of ₹2.53 crores has been received from 19 suppliers whose registrations have been suo-moto cancelled/suspended by the Department on the grounds of being non-existent or engaged in passing on ineligible credit. Further, fake ITC of ₹18.58 crores has been availed on invoices from M/s. N.M.G. Traders, which have no active business operations and have been floated only to avail of and pass fake ITC.

ii. Evidence on record indicates that Shri. Mohammed Kamran has not only fraudulently availed fake ITC but also failed to cooperate in the ongoing investigation by this office. He misbehaved, obstructed and fled the search premises with the support of the mob. He also snatched away crucial digital evidence. Shri Mohammed Kamran raises serious apprehensions of tampering with evidence and influencing co-conspirators and crucial witnesses. He is also at risk of fleeing and furthering the scam he has orchestrated.

iii. In view of the above, and considering the grave offence committed by Mohammed Kamran, he is at risk of fleeing and evading the investigation. Furthermore, there is a high risk that Mohammed Kamran will tamper with the evidence and influence the witness in the scam. The culpable mental state of Mohanimed Kamran has already been demonstrated by his acts of fleeing the ongoing search proceedings at his residence with crucial digital evidence. It raises serious apprehensions of tampering with evidence and influencing coconspirators and vital witnesses in the case.

iv. The facts brought on record firmly establish beyond doubt that Mohammed Kamran is the mastermind who is responsible for the commission of offences under clause (c) of sub-section (1) of Section 132 of the CGST Act, 2017, which are punishable under clause (i) of the said sub-section with imprisonment up to five years and fine. The offences committed by them are cognizable and non-bailable in terms of Section 132(5) of the Act. Therefore, Mohammed Kamran is clearly liable for arrest under Section 69(1) of the CGST Act, 2017, to secure their custodial interrogation, prevent further destruction of evidence, and protect the interest of revenue.

v. In view of the above, the offences committed by Shri Mohammed Kamran are offences as per Clause (c) of Sub-section (1) of Section 132 of the Central Goods and Services Tax Act, 2017. They are punishable with imprisonment for a term which may extend to five years and with a fine in terms of clause (i) of Sub-Section (1) of Section 132 of the said Act. Further, these offences are cognizable and non-bailable in terms of sub-section (5) of Section 132 of the said Act.

vi. In view of the above, there are sufficient and reasonable grounds to believe that Shri Mohammed Kamran has committed the offences punishable under Section 132(1)(i) of the CGST Act, 2017, which are cognizable and non-bailable. Accordingly, I invoke my powers under Section 69(1) of the CGST Act, 2017, to effect his arrest to prevent further destruction of evidence, enable custodial interrogation, and safeguard the revenue.

16. LEGAL PROVISIONS AND CONTRAVENTIONS

16.1 As per Section 132(1) of the Central Goods and Services Tax Act, 2017,

“Section 132. Punishment for certain offences.-

(1) 1[Whoever commits, or causes to commit and retain the benefits arising out of, any of the following offences], namely:-

(a) supplies any goods or services or both without issue of any invoice, in violation of the provisions of this Act or the rules made thereunder, with the intention to evade tax:

(b) issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilisation of input tax credit or refund of tax:

(c)) avails input tax credit using the invoice or bill referred to in clause (b) or fraudulently avails input tax credit without any invoice or bill:

….

shall be punishable-

(i) in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds five hundred lakh rupees, with imprisonment for a term which may extend to five years and with fine:

16.2 Further super Section 132(5) of the CGST Act, 2017, the offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) and punishable under clause(i) of that sub-section shall be cognizable and non-bailable.

16.3 Further as per Section 69(1) of the CGST Act, 2017, “Where the Commissioner has reasons to believe that a person has committed any offence specified in 132(1)(a, b, c &d) of the CGST Act, 2017 which is punishable under clause (i) or (ii) of sub-section (1), or sub-section (2) of the said section, he may, by order, authorize any officer of central tax to arrest such person”.

16.4. In this case, Shri Mohammed Kamran S/o Shri Akram Pasha, aged about 24 Years (DoB: 26.12.2000), Resident of LIG-61, bannimantap road, Bannimantap, Mysore-570015, has involved himself in the evasion of GST by way of availing of ITC totally amounting to Rs.21.11 Crores without underlying supply of goods or services which is an offence under Section 132(1)(c) of Central Goods and Services Tax Act, 2017,. The same is a cognizable offence and non-bailable as per the provisions of Section 132(5) of the CGST Act, 2017. Further it appears that he is liable for arrest under Section 69(1) of the Central Goods and Services Tax Act, 2017 for offence committed under Clause (a) and Clause (b) of Subsection (1) of Section 132 of the Central Goods and Services Tax Act, 2017 which is liable for punishment with imprisonment for a term which may extend to five years and with fine in terms of Clause (i) of Sub-section (1) of Section 132 of Central Goods and Services Tax Act, 2017.

16.5 In view of the above offence, the accused Shri Mohammed Kamran was placed under arrest on 16th September 2025 at 6:30 Hours (Memorandum of arrest is attached Document No.7 to this petition), at Kempegowda International Airport, Bengaluru within the jurisdiction of this Hon’ble Court. Shri Mohammed Kamran’s arrest has been conveyed to his mother Smt. Farzana Banu telephonically on number at about 7:30 hours on 16th September 2025 in the presence of Shri Mohammed Kamran and he has made an endorsement in the arrest memo about the aforementioned telephonic conversation informing about his arrest. The Grounds of Arrest, reasons of arrest and reasons to believe have been communicated to Shri Mohammed Kamran as annexure to the Arrest Memo and the same have been read over and explained to him. A letter intimating the arrest of the accused was sent to Smt Farzana Banu on her mobile number 9611604595 by WhatsApp. However, out of inadvertence the date of arrest in the intimation letter was mentioned as 15-09-2025 instead of 16-092025. However, in the WhatsApp message which was sent to her was correctly mentioning as 16-09-2025. Accordingly, a revised intimation correcting the above date was also sent to Farzana Banu over WhatsApp. The procedure of arrest is in line with the Hon’ble Apex Court Judgements.

17 Justification of Remand:

17.1 The investigation at hand is in initial state and it has clearly outlined the role of Shri Mohammed Kamran in orchestrating the scam unearthed during the investigation. The investigation at hand involves scrutiny of humongous data and thousands of documents recovered during the investigation thus far. Several other individuals are required to be questioned, documents and details are required to be recovered and numerous information to be collected and collated. The investigation involves unearthing the network of transactions, layers of benefits drawn, evaluating quantum of evasion of GST, collecting, collating and scrutinizing thousands of records pertaining to the said entities and questioning several individuals involved in the meticulously planned scam in order to conclude the investigation into meaningful and justified outcome.

17.2 The investigation at hand has evidenced that Shri Mohammed Kamran has availed fraudulent ITC to the tune of 21.11 crores without supply of goods and/or services and availing input tax credit without actual receipt of goods and/or services. His name has figured out from every nook and corner of the investigation. It is evident from the investigation done thus far that Shri Mohammed Kamran has several other conspirators and accomplices – both small and big- in the syndicate.

17.3 As the proprietor of M/s M.K. Traders, Shri Mohammed Kamran has attempted to tamper with evidence in several ways. He initially obstructed the search by refusing to open the door of his residence for about 1.5 to 2 hours, evidently to conceal or destroy evidence. During the proceedings, he also facilitated the escape of Shri Akram Pasha (proprietor of M/s A.R. Steel) from the premises. Evidence on record indicates that Shri Kamran not only fraudulently availed fake ITC but also failed to cooperate with the investigation. He misbehaved with officers, obstructed proceedings, fled the search premises with the support of a mob, and even snatched away crucial digital evidence. Further, he directed persons to other premises to obstruct proceedings and assist co-accused in escaping. He is also not cooperating in the examination of seized digital devices by denying access and refusing to share passwords for his mobile phones and laptop. His conduct raises serious concerns regarding tampering with evidence, influencing coconspirators and witnesses, and the risk of absconding and furthering the fraudulent activities orchestrated by him.

17.4 Shri Mohammed Kamran has willfully and consciously tried to destroy the crucial evidence which would have led to investigation of other individuals involved in the above offence. His intent to destroy the evidence and misled the investigation may hamper the investigation at hand. It is submitted that the investigation is being done aspects viz. recipient of goods, receipt of proceeds, involvement of other individuals and companies etc. It is feared that Shri Mohammed Kamran may temper/destroy the evidence, influence the witness or escape. Therefore, it appears just and necessary to place Shri Mohammed Kamran under Judicial Remand so that the investigation can be concluded in a logical manner.

17.5 The investigation at hand involves unearthing the network of transactions, layers of benefits drawn, evaluating quantum of evasion of GST, collecting, collating and scrutinizing thousands of records pertaining to the said companies and questioning several individuals involved in the meticulously planned scam. The nature of investigation at hand is subtle and complex at the same time and even smallest attempt to tamper the evidence, influence the witnesses of scuttle the proceedings may hamper the recovery of evidence and in such scenario the justice envisioned at the end of the investigation and adjudication proceedings may also suffer. Therefore, it is just and essential to confine the arrested accused in Judicial Custody to enable the investigating officers to conclude the investigation in an unimpeded manner.

17.6 It is respectfully submitted that the department is pursuing further investigation in the matter and the investigations need to be conducted to quantify total GST liability and gather further evidence establishing the evasion of GST.

18. In view of the foregoing, the complainant most prays that:

PRAYER

The arrested accused, Shri Mohammed Kamran S/o Akram Pasha are hereby produced before the Hon’ble Court.

In view of the above circumstances, it is most humbly prayed that the accused Shri Mohammed Kamran, may be remanded to Judicial Custody for fifteen (15) days in the interest of further investigation and thus render justice.

Place: Bengaluru

Date: 16.09.2025

Sd/-16/09/2025

ASHOK KUMAR YADAV

SENIOR INTELLIGENCE OFFICER

DGGI BENGALURU ZONAL UNIT”

The arrest memo reads as follows:

“GSTIN-29IRZPK8080E1ZT CBIC-DIN-202509DSS0000021262E File No- DGGI/INV/125/2025-Gr C-01-0/0 Pr ADG-DGGI-ZU-BENG

ARREST MEMO

(To be prepared in duplicate)

[under Section 69 of the Central Goods and Services Tax Act, 2017]

Whereas, the principal Commissioner/Commissioner, Anwar Ali T.P. has reasons to believe that you, Mr Mohammed Kamran, Proprietor of M/s. M K Traders, age about 24 years, son/ daughter of Shri Akram Pasha and address LIG 61 Mysuru Banni Mantap Road, Mysore, Karnataka- 570015 have commited an offence specified in clause (a) or clause (b) or clause (c) or clause (d) of sub section (1) of section 132 of the Central Goods and Service Tax, 2017 which is punishable under clause (i) or (ii) of sub-section (1) or sub-section (2) of the said section.

2. I, Ashok Kumar Yadav Senior Intelligence Officer Office of the Principal Commissioner/Commissioner, CGST O/o the Pr. Additional Director General, Directorate General of GST Intelligence, Bangalore Zonal Unit, No.112, S.P.Enclave, Adjacent to Karnataka Bank, KH Road, Bangalore-560027

being duly authorized, hereby arrest you today at 6:30:AM on 2025-09-16 00:00:00.0 at Kempegowda International Airport, Bangalore under Section 69 of the said Act.

Accordingly, Shri Mohammed Kamran son / daughter of Akram Pasha has been placed under arrest and he has been explained the grounds of his arrest. He was also informed about his right to have someone informed about his arrest and Sh./Ms has been informed about his arrest.

Signature

Sd/- 16/09/2025

Name: Ashok Kumar Yadav

Designation: Superintendent /Appraiser/Senior Intelligence Officer

4. I have been explained the grounds of my arrest. The fact of my arrest have been witnessed by Shri Boddu Sreekanth, Baggage Helper, son/daughter of Duggaiah B. resident of Narayanam Peta, VTC+PO: Seetharamapuram, Dist- Nellore, AP-524310

Received copy of arrest Memo

Sd/-

Signature of the Arrestee

Sd/-

Counter Signature of Witness Wimen-2”

The grounds of arrest and reasons for arrest read as follows:

“F. No. F. No. DGGI/INV/125/2025-Gr C-01-0/0 Pr DG-DGGI-ZU-BENGALURU

Date: 16.09.2025

CBIC-DIN: 202509DSS0000021262E

Annexure to Arrest Memo issued to Shri Mohammed Kamran

I. Grounds of arrest :

1. That Shri Mohammed Kamran, has involved himself in the illicit activity of issuance of invoices without supply of goods and/or services in the name of M/s M K Traders. The grounds of arrest are as follows:

i) M/s. M K TRADERS, (hereinafter referred to as “the said taxpayer”) a proprietary firm under the proprietorship of Mohammed Kamran S/o Shri Akram Pasha, is registered with the department under GSTIN 29IRZPK8080E1ZT for supply goods viz. FERROUS WASTE AND SCRAP; REMELTING SCRAP INGOTS OF IRON OR STEEL, HSN-7204. The taxpayer has registered principal place of business at 75, 2nd Main Road, 4th Cross, Kesare Village, Kasaba Hobli, Mysuru (Mysore) – 570007 and an Additional Place of Business at Ground Floor, Bunder, ANSARI ROAD, Near Yateem Khana, Mangaluru, Dakshina Kannada, Karnataka, 575001. The taxpayer falls under the jurisdiction of Lashker Mohalla Range of Mysore CGST Commissionerate.

ii) Further, Shri Mohammed Kamran, has been found to have fraudulently availed ineligible input tax credit (ITC) of Rs.21.11 Crores on the strength of invoices without accompanying supply of goods/services. Out of the above ITC, Rs.2.53 Cr has been availed from suppliers, whose registrations have been suo-moto cancelled/suspended by the Department on the grounds of being non-existent or engaged in passing on ineligible credit. Further, he has availed ITC of Rs.18.58 Crores from M/s. N.M.G. Traders which does not have any legitimate business and is a proprietary concern of Nasir Ahmed which have emerged as major players in the fake ITC racket and are under active investigation. Though the GST Registration of M/s NMG Traders is active, they do not have actual business operations and have been floated only for availing and passing fake ITC. Search at the address of the principal place of business and additional place of business indicated no business activity. Further, the principal place of business was found to be rented premises, and the owner of the premises has submitted that there has been no business activity at the said premises. On perusal of the GSTR2A return of M/s NMG Traders, it is seen that major suppliers are either suo-moto cancelled by the department and the among the Active suppliers, several appear to be generators of fake ITC.

iii) The details of supplier wise ITC availed and status of their GST registration is tabulated below:

| Trade Name | GSTIN | Taxable Value | Total ITC Received | Reg Status |

|---|---|---|---|---|

| N.M.G. Traders | 29EMIPA3360K1ZW | 1,03,21,57,316 | 18,57,88,319 | Active (passed fake ITC) |

| A K Steel Traders | 29DSQPA7479L1ZR | 3,18,86,475 | 57,72,409 | Suspended |

| T R Traders | 29CRTPB5284M1ZX | 1,68,33,321 | 30,29,998 | Cancelled suo moto |

| A I Enterprises | 29AHTPI8019D1Z1 | 1,45,69,075 | 26,22,434 | Cancelled suo moto |

| A R Traders | 29CYCPA5269F1ZF | 1,38,31,280 | 24,89,630 | Cancelled suo moto |

| Az Trader Enterprises | 29CHIPA6100J1ZJ | 1,20,11,685 | 21,62,103 | Cancelled suo moto |

| M M Traders | 29EHOPS7644F2ZI | 1,05,52,449 | 18,99,441 | Cancelled suo moto |

| Palani Enterprises | 29GLCPP1295P1Z7 | 78,46,976 | 14,12,456 | Suspended |

| New Royal Traders | 29INLPK9785E1Z1 | 66,82,486 | 12,02,847 | Cancelled suo moto |

| Hindustan Trader | 29FCHPM1780D1ZG | 47,84,583 | 8,61,225 | Cancelled suo moto |

| Anto Steel Traders | 29DCXPA2649H1Z4 | 46,74,385 | 8,41,389 | Cancelled suo moto |

| R A Creation | 29CPRPM8989Q1Z2 | 38,28,330 | 6,89,099 | Cancelled suo moto |

| S M Steel Traders | 29FKYPS5630H1Z7 | 33,22,921 | 5,98,126 | Suspended |

| P S Traders | 29FEPPS1371E1Z1 | 24,53,889 | 4,41,700 | Cancelled suo moto |

| Barnakar Impex | 29CCSPB6025Q1ZW | 22,35,000 | 4,02,300 | Cancelled suo moto |

| Hm Traders | 29AYKPA7424L2Z2 | 21,17,409 | 3,81,134 | Cancelled suo moto |

| Raj Enterprises | 29ERLPR8805J1ZW | 10,00,245 | 1,80,044 | Cancelled suo moto |

| Elahi Traders | 29LUKPS2747H1ZR | 8,00,112 | 1,44,020 | Cancelled suo moto |

| Lido Enterprises | 29ALUPI4474M1Z5 | 7,50,000 | 1,35,000 | Cancelled suo moto |

| Sona Electronics | 29ADWPM0455G1Z4 | 1,39,453 | 39,047 | Cancelled suo moto |

| Total | 1,17,24,77,389 | 21,10,92,721 |

iv) Shri Mohammed Kamran has fraudulently availed ITC of 21.11 Crores without receipt of goods/services, solely on the strength of bogus invoices issued by non-existent/fictitious firms, including M/s. N.M.G. Traders.

v) His acts constitute offences under the CGST Act, 2017, under Section 132(1)(c): Availment/utilisation of ITC without actual receipt of goods/services;

vi) The fraudulent ITC involved, Rs.21.11 Crores, far exceeds the statutory threshold of `5 Crores. Therefore, in terms of Section 132(5) of the CGST Act, 2017, the offences are cognizable and non-bailable.

vii) In view of the above, there are sufficient and reasonable grounds that Shri Mohammed Kamran has committed the offences punishable under the CGST Act, 2017. Accordingly, in exercise of powers under Section 69(1) of the CGST Act, 2017 is warranted to effect his arrest in order to prevent further destruction of evidence, enable custodial interrogation, and safeguard the revenue

II. Reasons for Arrest:

i. To prevent Shri Mohammed Kamran from tampering with the evidence in any manner;

ii. To prevent Shri Mohammed Kamran from committing any further offence;

iii. To prevent Shri Mohammed Kamran from making inducement, threat, promise to any person acquainted with fact of the case so as to dissuade him from disclosing such facts to the court or to the investigating officer;

iv. To prevent Shri Mohammed Kamran from fleeing thereby dodging the investigation;

III. Reasons to Believe:

The competent authority has the following reasons to believe:

1. That Shri Mohammed Kamran, S/o Shri Akram Pasha, Proprietor of M/s. MK Traders (GSTIN-29IRZPK8080E1ZT) has fraudulently availed ineligible input tax credit (ITC) of ₹21.11 crores approx, without actual receipt of goods or services. Out of the same, ineligible ITC of ₹2.53 crores has been received from 19 suppliers whose registrations have been suo-moto cancelled/suspended by the Department on the grounds of being non-existent or engaged in passing on ineligible credit. Further, fake ITC of 18.58 crores has been availed on invoices from M/s. N.M.G. Traders, which have no active business operations and have been floated only to avail of and pass fake ITC.

2. That evidence on record indicates that Shri. Mohammed Kamran has not only fraudulently availed fake ITC but also failed to cooperate in the ongoing investigation by this office. He misbehaved, obstructed and fled the search premises with the support of the mob. He also snatched away crucial digital evidence. Shri Mohammed Kamran raises serious apprehensions of tampering with evidence and influencing coconspirators and crucial witnesses. He is also at risk of fleeing and furthering the scam he has orchestrated.

3. That, Shri Mohammed Kamran, is at risk of fleeing and evading the investigation and tampering with the evidence and influence the witness in the scam. The culpable mental state of Mohammed Kamran has already been demonstrated by his acts of fleeing the ongoing search proceedings at his residence with crucial digital evidence. It raises serious apprehensions of tampering with evidence and influencing co-conspirators and vital witnesses in the case.

4. That Shri Mohammed Kamran has committed the offences as per Clause (c) of Sub-section (1) of Section 132 of the Central Goods and Services Tax Act, 2017, which are punishable with imprisonment for a term which may extend to five years and with a fine, in terms of clause (i) of Sub-Section (1) of Section 132 of the said Act. Further, these alleged offences are cognizable and non-bailable in terms of sub-section (5) of Section 132 of the said Act.

7. In view of the above, there are sufficient and reasonable grounds to believe that Shri Mohammed Kamran has committed the offences punishable under Section 132(1)(i) of the CGST Act, 2017, which are cognizable and non- bailable. Accordingly, I invoke my powers under Section 69(1) of the CGST Act, 2017, to effect his arrest to prevent further destruction of evidence, enable custodial interrogation, and safeguard the revenue.

8. Hence, I have reasons to believe that Shri Mohammed Kamran, has committed offences as per Clause (c) of Sub-section (1) of Section 132 of the Central Goods and Services Tax Act, 2017, which are punishable with Section 132 of the said Act. Further, these alleged offences are cognizable and non-bailable in terms of sub-section (5) of Section 132 of the said Act.

9. Wherever the provisions of the CGST Act, 2017, have been invoked, the corresponding provisions of the Karnataka GST Act, 2017, read with Section 20 of the IGST Act, 2017, as applicable, are deemed to be invoked.

10. Accordingly, in exercise of the powers vested in me, in terms of Sub-Section (1) of Section 69 of CGST Act, 2017, I hereby authorize Shri Ashok Kumar Yadav, Senior Intelligence Officer, Directorate General of GST Intelligence, Bengaluru Zonal Unit, Bengaluru, to arrest Shri Mohammed Kamran, aged about 24 years (DOB: 26.12.2000), S/o Shri Akram Pasha residing LIG 61 Mysuru Banni Mantap Road, Mysore, Karnataka-570015(as declared in GST registration)

15/09/2025 08:10 PM

Place: BENGALURU

Date: 16.09.2025

Sd/- 16/09/20 25

अशोक कमारु यादव / Ashok Kumar Yadav

वर आसचनाू अधकार/Senior Intelligence Officer

डी. जी. जी. आई., बगल!ु जोनल इकाई/DGGI, Bengaluru Zonal Unit

To

Shri Mohammed Kamran,,

aged about 24 Years (DoB: 26-12-2000),

S/o Shri Akram Pasha

Residing at LIG 61 Mysuru Banni Mantap Road,

Mysore,Karnataka-570015(as declared in GST registration)”

(sic)

(Emphasis added at each instance)

The petitioner is before the Court on the plea that there cannot be parallel proceedings by the State GST authorities and the Central GST authorities.

8.2. Both the learned senior counsel for the petitioner and the learned counsel for respondent Nos.1 and 2 have relied on the judgment of the Apex Court in the case of ARMOUR SECURITY supra. Therefore, certain paragraphs that are relevant of the said judgment are required to be noticed. They read as follows: “

.”… …. ….

83. However, we shall now proceed to interpret the term “subject- matter” as employed in section 6(2)(b) of the Act. It is abundantly clear from the purport of the said section that “subject-matter” needs to be understood in perspective of initiation of proceedings. In other words, subject-matter of the proceedings. In the preceding paragraphs of this judgment, we have stated that proceedings stand initiated when a show-cause notice is issued with regard to a subject-matter. We say so because an issuance of a show-cause notice is the first stage whereby the Revenue for the very first time elaborately pens down various grounds and charges it is alleging against the assessee, who is invited to show cause as to why adverse action must not be taken against him on the basis of the apprehensions that the authority contemplates.

… … …

85. Primacy is given to the cogency of a show-cause notice. The subject- matter of the proceedings lies in the contents of the notice. Hence, it ought to be exhaustive, so much so that it is capable of presenting the case of the Revenue in a nutshell. In Commissioner of Central Excise, Bhubaneswar-I v. Champdany Industries Limited reported in [(2010) 1 GSTR 52 (SC); (2009) 9 SCC 466; 2009 SCC OnLine SC 1606.], while deciding upon the classification of jute carpets, this court noted that in the failure of mentioning the application of certain tests which the Revenue relied upon in the proceedings before the court, the Revenue cannot rely on such tests at a later stage. A show-cause notice must lay down the foundation of the case. Such is the importance of a show cause as a starting point in proceedings. The relevant extracts have been supplied below [ Page 64 in 1 GSTR.]:

“50. Apart from that, the point on rule 3 which has been argued by the learned counsel for the Revenue was not part of its case in the show-cause notice. It is well-settled that unless the foundation of the case is made out in the show-cause notice, Revenue cannot in court argue a case not made out in its show-cause notice. See: Commissioner of Customs, Mumbai v. Toyo Engineering India Ltd. [(2006) 7 SCC 592, paragraph 16; 2006 SCC OnLine SC 902.].

51. Similar view was expressed by this court in the case of Commissioner of Central Excise, Nagpur v. Ballarpur Industries Ltd. [(2007) 9 RC 456; (2007) 8 SCC 89; 2007 SCC OnLine SC 1076.]. In paragraph 27 of the said report, learned judges made it clear that if there is no invocation of the concerned rules in the show-cause notice, it would not be open to the Commissioner to invoke the said rule.” (emphasis supplied)

86. From the above exposition of law, we can safely conclude that a show-cause notice delineates the scope of the proceedings in the expression of subject-matter with which the authority would be dealing. It would be impermissible for an authority to invoke such rules, claims or grounds at a later stage which do not figure in the show-cause notice. That is to say, any ground, reasoning or claim which does not figure out in the show-cause notice cannot be permitted to adversely affect the noticee. Such recognition has even been made statutorily, as per sub-section (7) of section 75 of the Act, which reads as thus:

“75. General provisions relating to determination of tax.—(1) to (6)…

(7) The amount of tax, interest and penalty demanded in the order shall not be in excess of the amount specified in the notice and no demand shall be confirmed on the grounds other than the grounds specified in the notice.”

87. The expression “subject-matter” contemplates proceedings directed towards determining the taxpayer’s liability or contravention, encompassing the alleged offence or non-compliance together with the relief or demand sought by the Revenue, as articulated in the show-cause notice through its charges, grounds, and quantification of demand. Accordingly, the bar on the “same subject-matter” is attracted only where both proceedings seek to assess or recover an identical liability, or even where there is the slightest overlap in the tax liability or obligation.

88. In other words, under section 6(2)(b), the “subject-matter” is intrinsically tied to the determination of the specific violation under scrutiny or the liability alleged to be unpaid. The statutory bar is triggered only when the two proceedings against the same taxpayer are, in substance, directed towards the very same or overlapping deficiency in tax discharge or the identical contravention alleged. Where the proceedings concern distinct infractions, each Department is entitled to proceed within its respective statutory remit without infringing the prohibition. Where the proceedings concern distinct infractions, each Department is entitled to proceed within its respective statutory remit without infringing the prohibition.