Sir, in the past our Government has taken several measures to reduce tax litigations. In the last budget, Sabka Vishwas Scheme was brought in to reduce litigation in indirect taxes. It resulted in settling over 1,89,000 cases. Currently, there are 4,83,000 direct tax cases pending in various appellate forums i.e. Commissioner (Appeals), ITAT, High Court and Supreme Court. This year, I propose to bring a scheme similar to the indirect tax sabkaVishwas for reducing litigations even in the direct taxes. – FM Nirmala sitharaman

What is Vivad se Vishwas scheme?

The Direct Tax Vivad Se Vishwas Bill, 2020 tabled on lok sabha on Wednesday is introduced to provide complete waiver of interest and penalty to the taxpayers whose liabilities are in dispute.

A bill to provide for resolution of disputed tax and for matters connected therewith or incidental thereto.

What are the benefits to economy by this?

The number of appeals that are filed is much higher than the number of appeals that are disposed. As a result, a huge amount of disputed tax arrears is locked-up in these appeals. This scheme will pave a way for tax collection by providing an inducement to the taxpayers.

It shall also act as the name suggests on trust building rather than seeing it as mere tax resolution.

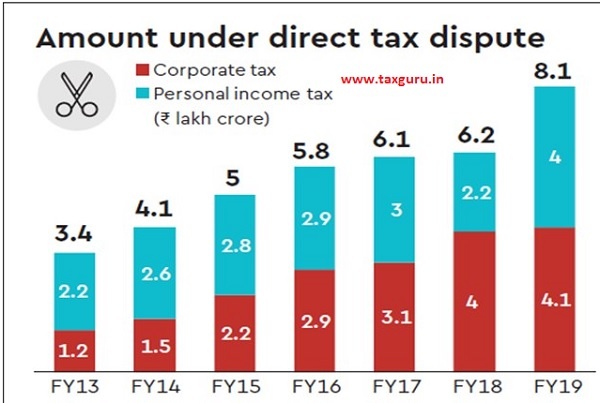

Nearly five lakh cases of tax disputes are pending in various tribunals. It seeks to cut down on nearly 4.8 lakh tax disputes, a huge amount of disputed tax arrears is locked-up in these appeals. As on the 30th November, 2019, the amount of disputed direct tax arrears is Rs. 9.32 lakh crores.

What are benefits to assesses opting for this?

The taxpayers will be able to deploy the time, energy and resources saved by opting for such dispute resolution towards their business activities.

An added incentive to escape safely when you have uncertain appeal hanging by your side.

Am I eligible to it?

Yes, if you are a person or the income-tax authority who has filed appeal before the appellate forum and such appeal is pending on 31st day of January, 2020.

Appellate forum means the Supreme Court or the High Court or the Income Tax Appellate Tribunal or the Commissioner (Appeals).

The provisions of the scheme shall be applicable to appeals filed by taxpayers or the Government, which are pending with the Commissioner (Appeals), Income tax Appellate Tribunal, High Court or Supreme Court as on the 31st day of January, 2020 irrespective of whether demand in such cases is pending or has been paid.

What comes under the “ineligibility” class?

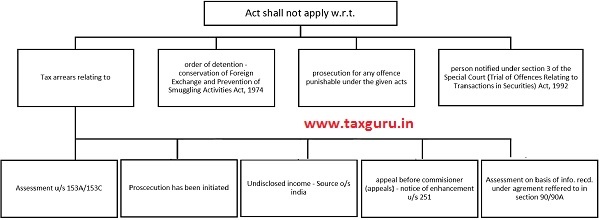

The provisions of this Act shall not apply:

A) in respect of tax arrear,

1. relating to an assessment year in respect of which an assessment has been made under section 153A or section 153C.

2. relating to an assessment year in respect of which prosecution has been instituted on or before the date of filing of declaration;

3. relating to any undisclosed income from a source located outside India or undisclosed asset located outside India;

4. relating to an assessment or reassessment made on the basis of information received under an agreement referred to in section 90 or section 90A of the Income-tax Act, if it relates to any tax arrear;

5. relating to an appeal before the Commissioner (Appeals) in respect of which notice of enhancement u/s 251 of the Income-tax Act has been issued on or before the specified date;

B) To any person in respect of whom an order of detention has been made under the provisions of the Conservation of Foreign Exchange and Prevention of Smuggling Activities Act, 1974 on or before the filing of declaration.

C) To any person in respect of whom prosecution for any offence punishable under the provisions of the Indian Penal Code, the Unlawful Activities (Prevention) Act, 1967, the Narcotic Drugs and Psychotropic Substances Act, 1985, the Prevention of Corruption Act, 1988, the Prevention of Money Laundering Act, 2002, the Prohibition of Benami Property Transactions Act, 1988 or for the purpose of enforcement of any civil liability has been instituted on or before the filing of the declaration or such person has been convicted of any such offence punishable under any of those Acts.

D) To any person notified under section 3 of the Special Court (Trial of Offences Relating to Transactions in Securities) Act, 1992 on or before the filing of declaration.

Are there any specific dates to be remembered?

1. You’re eligible if your appeal is pending on 31st day of January, 2020.

2. Amount determined under this act has to be paid before 31st march 2020 to avail full benefit. After 31st march 2020 there comes an additional burden up to the not yet notified “last date”. it will not be an open-ended scheme but shall have a specific time frame. Referring to press releases it provides a deadline of 30th June, 2020

Post opting into the scheme how much do I have to pay?

| Nature of tax arrear | Amount payable till 31st March 2020 | Amount payable on or after 1st April 2020 |

| Aggregate amount of disputed tax, interest and penalty. | Amount of the disputed tax | Amount of disputed tax + 10% of disputed tax (subject to a maximum of actual interest and penalty) |

| Disputed interest or disputed penalty or disputed fee. | 25% of disputed interest or disputed penalty or disputed fee. | 30% of disputed interest or disputed penalty or disputed fee. |

How do I opt for the scheme?

Declaration including details mentioned in question above (as the case may be) shall be filed by the declarant before the designated authority in such form and verified in such manner as may be prescribed.

Designated authority means an officer not below the rank of a Commissioner of Income-tax notified by the Principal Chief Commissioner for the purposes of this Act.

Declaration shall be presumed never to have been made if:

(a) any material particular furnished in the declaration is found to be false at any stage;

(b) the declarant violates any of the conditions referred to in this Act;

(c) the declarant acts in any manner which is not in accordance with the undertaking (referred below)

What do I do of the existing ongoing dispute?

If appeal is pending before the Income Tax Appellate Tribunal or Commissioner (Appeals)

Appeal shall be deemed to have been withdrawn from the date on which certificate mentioning particulars of the tax arrear and the amount payable after final determination is issued by the designated authority.

If declarant has filed any appeal before the appellate forum or any writ petition before the High court or the Supreme Court against any order in respect of tax arrear

He shall withdraw such appeal or writ petition with the leave of the Court wherever required and furnish proof of such withdrawal along with the declaration.

Where the declarant has initiated any proceeding for arbitration, conciliation or mediation, or has given any notice thereof under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India whether for protection of investment or otherwise

He shall withdraw the claim, if any, in such proceedings or notice prior to making the declaration and furnish proof thereof along with the declaration.

Do I have to sacrifice any right?

Yes, you have to file an undertaking waving your right, whether direct or indirect, to seek or pursue any remedy or any claim in relation to the tax arrear which may otherwise be available to you under any law for the time being in force, in equity, under statute or under any agreement.

What is the time and manner of payment?

Within a period of 15 days from the date of receipt of the declaration, the designated authority shall by order, determine the amount payable by the declarant. They shall grant a certificate to the declarant containing particulars of the tax arrear and the amount payable after such determination.

No appellate forum or arbitrator, conciliator or mediator shall proceed to decide any issue relating to the tax arrear mentioned in the declaration in respect of which an order has been made.

No matter covered by such order shall be reopened in any other proceeding under the Income-tax Act or under any other law for the time being in force or under any agreement

Declarant has 15 days from receipt of certificate to pay the amount determined.

Whether amount paid above will be refunded in any circumstances?

No.

Author Bio