EL-Equalisation Levy, Assessee-Any Person Resident or Non-Resident with Permanent Establishment

1. EMERGENCE OF EL

Can you imagine the life without Technology? Certainly not. It is very appealing to the case with Digital Economy too. Today the way of doing business has changed drastically and dramatically. All tangible and intangible goods are being bought and sold on space. Practically concept of permanent establishment (fixed place of business) though looked comprehensive arrangement for taxing on business transactions initially but with the arena of digital economy has made it ineffective and non-comprehensive to bring business transactions into tax bracket.

Advent of Digital Economy has been very facilitative at the same time been a great pain for any country for not taxing business transactions based on source rule principle. Rapid growth of information and communication technology has resulted in substantial expansion of the supply and procurement of digital goods and services globally, including India. The Digital Economy is growing at approximately 10% per annum, significantly faster than the global economy as a whole. At present the digital domain, business may be conducted without regard to national boundaries and may dissolve the link between an income producing activity and a specific location. Persons carrying business in digital domain could be located anywhere in the world. Entrepreneurs across the world have been quick to evolve their business to take advantages of these changes.

The new business models have created new challenges:

(i) The difficulty in characterizing the nature of payment and establishing a nexus or link between taxable transaction, activity and taxing jurisdiction,

(ii) The difficulty of locating the transaction, activity and identifying the taxpayer for income tax purposes.

The digital business, thus, challenges physical presence based permanent establishment rules. If permanent establishment principles are to remain effective in the new digital world, the fundamental PE concept for the outpaced economy i.e. place of business, location and permanency must be reconciled with the new digital reality.The tax challenges arising from the digital economy have been addressed by the Organisation for Economic Cooperation and Development (OECD) in its report on Action plan 1 of the Base Erosion & Profit Shifting (BEPS) project. The report has identified three options viz a new nexus based on significant economic presence, a withholding tax on digital transactions and equalization levy, to address the broader direct tax challenges of the digital economy.

In the Indian context, the Central Board of Direct Taxes (CBDT), recognizing the significance of issues relating to the digital economy and the need to have a simple way to resolve them and bring greater clarity and predictability in the tax regime, directed that a Committee be constituted for the same. After examining the three options stated in Action plan 1 of the BEPS project, the Committee in its proposal for equalization levy on specified transactions of February 2016 noted that the two options i.e. new nexus based on significant economic presence and a withholding tax on digital transactions would require changes in number of tax treaties. Accordingly, the Committee noted that the third option of equalization levy provided a simpler option that could be adopted under the domestic law without needing amendment to a large number of tax treaties. As per the Committee, the equalization levy imposed on payment for digital transactions would not be a tax on income and hence would not be covered by the tax treaties.

The Committee proposed that the said levy may be imposed on specified digital services and facilities including online marketing and advertisement; cloud computing; website designing, hosting and maintenance; digital space.

2. EQUALISATION LEVY INCEPTION:

Taking note of Action plan 1 of the BEPS project and in line with the above Committee proposal , the Finance Act 2016 has inserted a new chapter VIII titled ‘Equalization Levy’ which has come into force from 1 June 2016. The same is not a part of the Income-tax Act, 1961.

3. RATE:

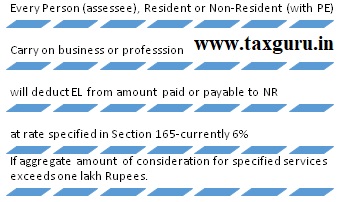

EL is to be charged at the rate of six per cent of the amount of consideration received or receivable by a non-resident.

4. SOME IMPORTANT DEFINITIONS;

Section 164 (d): “equalisation levy” means the tax leviable on consideration received or receivable for any specified service under the provisions of this Chapter;

Section 164 (g): “permanent establishment” includes a fixed place of business through which the business of the enterprise is wholly or partly carried on;

Section 164 (i): “specified service” means online advertisement, any provision for digital advertising space or any other facility or service for the purpose of online advertisement and includes any other service as may be notified by the Central Government in this behalf;

Section 164 (j): words and expressions used but not defined in this Chapter and defined in the Income-tax Act, or the rules made thereunder, shall have the meanings respectively assigned to them in that Act.

5. COVERAGE:

Section 163 (1): This Chapter extends to the whole of India except the State of Jammu and Kashmir.

6. APPLICABILITY:

Amount of consideration for any specified service received or receivable by a person, being a non-resident from––

(i) a person resident in India

(ii) and carrying on business or profession; or

(iii) a non-resident having a permanent establishment in India& business activity connected to said PE..

7. NOT CONVERED:

Section 165(2): EL not charged when:

(a) NR has PE in India and specified services connected with such PE

(b) Aggregate amount of consideration not exceed one lakh rupees

(c) Not for business or profession i.e. for personal purpose

8. COLLECTION AND RECOVERY OF EQUALISATION LEVY:

Section 161(1) Collection of EL:

Section 166 (2): Recovery of Equalisation Levy:

> EL So deducted in a month to be paid by assesse

> To the credit of CG

> By the seventh day of the month immediately following calendar month (Just like TDS-withholding provisions)e.g. EL deducted on 5th May, 2020 is supposed to be credited by 7th June, 2020.

Section 166 (3): Liable to pay EL even though EL not deducted

9. FURNISHING OF STATEMENTS(SECTION 167):

(1) Every assessee shall, within the prescribed time after the end of each financial year, prepare and deliver or cause to be delivered to the Assessing Officer or to any other authority or agency authorised by the Board in this behalf, a statement in such form, verified in such manner and setting forth such particulars as may be prescribed, in respect of all specified services during such financial year.

(2) An assessee who has not furnished the statement within the time prescribed under sub-section (1) or having furnished a statement under sub-section (1), notices any omission or wrong particular therein, may furnish a statement or a revised statement, as the case may be, at any time before the expiry of two years from the end of the financial year in which the specified service was provided.

(3) Where any assessee fails to furnish the statement under sub-section (1) within the prescribed time, the Assessing Officer may serve a notice upon such assessee requiring him to furnish the statement in the prescribed form, verified in the prescribed manner and setting forth such Particulars, within such time, as may be prescribed.

10. PROCESSING OF STATEMENT(SECTION 168):

(1) Where a statement has been made under section 167 by the assessee, such statement shall be processed in the following manner, namely:––

(a) the equalisation levy shall be computed after making the adjustment for any arithmetical error in the statement;

(b) the interest, if any, shall be computed on the basis of sum deductible as computed in the statement;

(c) the sum payable by, or the amount of refund due to, the assessee shall be determined after adjustment of the amount computed under clause (b) against any amount paid under sub-section (2) of section 166 or section 170 and any amount paid otherwise by way of tax or interest;

(d) an intimation shall be prepared or generated and sent to the assessee specifying the sum determined to be payable by, or the amount of refund due to, him under clause (c); and

(e) the amount of refund due to the assessee in pursuance of the determination under clause (c) shall be granted to him:

Provided that no intimation under this sub-section shall be sent after the expiry of one year from the end of the financial year in which the statement is furnished.

(2) For the purposes of processing of statements under sub-section (1), the Board may make a scheme for centralised processing of such statements to expeditiously determine the tax payable by, or the refund due to, the assessee as required under that sub-section.

11. INTEREST ON DELAYED PAYMENT OF EQUALISATION LEVY:

Every assessee, who fails to credit the equalisation levy or any part thereof as required under section 166 to the account of the Central Government within the period specified in that section, shall pay simple interest at the rate of one per cent. of such levy for every month or part of a month by which such crediting of the tax or any part thereof is delayed.

12. PENALTY FOR FAILURE TO DEDUCT OR PAY EQUALISATION LEVY:

Any assessee who––

(a) fails to deduct the whole or any part of the equalisation levy as required under section 166; or(b) having deducted the equalisation levy, fails to pay such levy to the credit of the Central Government in accordance with the provisions of sub-section (2) of that section, shall be liable to pay,—

(i) in the case referred to in clause (a), in addition to paying the levy in accordance with the provisions of sub-section (3) of that section, or interest, ifany, in accordance with the provisions of section 170, a penalty equal to the amount of equalisation levy that he failed to deduct; and

(ii) in the case referred to in clause (b), in addition to paying the levy in accordance with the provisions of sub-section (2) of that section and interest in accordance with the provisions of section 170, a penalty of one thousand rupees for every day during which the failure continues, so, however, that the penalty under this clause shall not exceed the amount of equalisation levy that he failed to pay.

13. PENALTY FOR FAILURE TO FURNISH STATEMENT-SECTION 172

> Penalty Rs. 100/- for each day till default continue

> Payment within prescribed period

14. PENALTY NOT TO BE IMPOSED IN CERTAIN CASES-SECTION 173

> Section 173 (1) If assessee prove to the satisfaction of assessing officer about reasonable cause of failure

> Section 173 (2) if assessee not given opportunity being heard

Author Bio

Very Good article in Equalization levy covering all aspects