Introduction:

Overseas Direct Investments (ODI) in the Indian Context means, any capital outflows / investments made by Indian residents in a foreign country but does not include portfolio investment.

As more companies involve themselves with foreign investments, the importance of the Foreign Exchange Management Act (FEMA) regulations and their compliance becomes a major part of the company’s operations. ODI can be made either by an Individual or by any other Indian entity. Originally when Liberalized Remittance Scheme was announced there was no restriction on setting up overseas entities by Individuals. However, RBI interpreted provisions differently. According to RBI the general permission under LRS was restricted to overseas portfolio investment and not for overseas direct investment. However 5th August 2013, individuals are allowed to make ODI under the Liberalized Remittance Scheme (LRS) up to USD 2,50,000/- per financial year. Two other primary condition that need to be met are

(i) Investor should invest his own money, meaning thereby he cannot borrow and invest and

(ii) The overseas company where investment is made will not be allowed to have step down subsidiary.

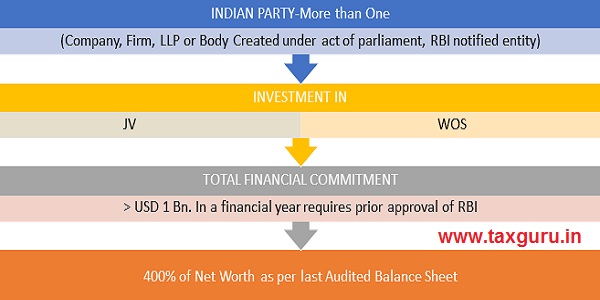

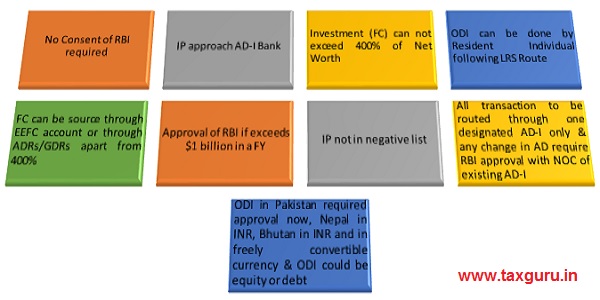

There are two routes through which a person resident in India may invest overseas viz. Automatic Route and Approval Route. Under the Automatic Route, there is no need to take prior approval of the RBI while investing abroad. However, under the Approval route, a person investing abroad needs to obtain prior approval from the RBI. In case the investment exceeds USD One billion or 400% of net worth in a financial year, approval of RBI is compulsory.

FORMS TO FILED IN RESPECT OF ODI:

| Name of the Form | Purpose | Time of Filling |

| ODI Part I | Intimation of Investment | At the time of initial remittance |

| ODI Part II | Details of all remittances /repatriation of income from overseas venture in terms of dividends, interest, royalties, fees for technical services…etc. | Known as Annual Performance Report (APR) to be submitted before 31st December every year. |

| ODI Part III | Details of divestments | At the time of divestments |

| FLA Return | Annual Return on Foreign Liabilities and Assets containing details of foreign assets and liabilities as on the 31st March of the immediately preceding financial year. | On or before 15th July every year. |

INDEX GENERAL PART- I

1. LEGAL BOUNDARIES TO BE REFERRED

2. Financial Commitment or Overseas Direct Investment

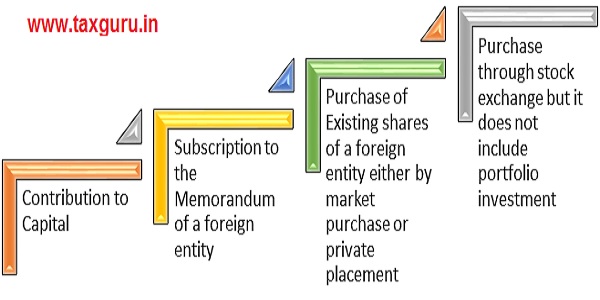

3. METHODS OF INVESTING

4. NET WORTH OF INDIAN PARTY-EXAMPLE

5. NET WORTH OF INDIAN PARTY

Net worth of its holding company (which holds at least 51% stake in the Indian Party)

or its subsidiary company (in which the Indian party holds at least 51% stake)

May be taken into account to the extent not availed of by the holding company or the subsidiary independently and has furnished letter of disclaimer in the favor of the Indian Party.

6. PROHIBITIONS

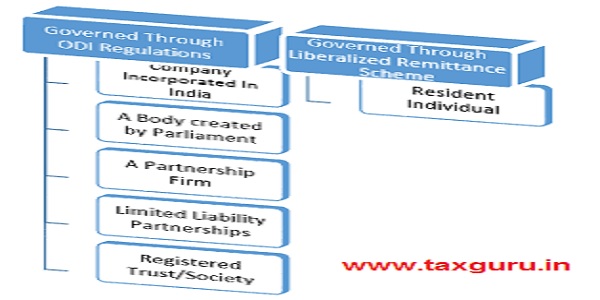

7. Entities allowed for ODI & Its Governance

8. Permissible Sources of Funding

9. General Permission (Regulation 4)

10. ODI under Automatic Route

11. ODI UNDER AUTOMATIC ROUTE

12. ODI-AUTOMATIC ROUTE (AR)-PARAMETER

13. ODI-Automatic Route -1 Eligible Limit

14. ODI-Automatic Route –2 Procedure

15. ODI-Automatic Route –3 Total FC “Comprise of” and Limit Prescribed

16. ODI-Automatic Route –3 Total FC “Comprise of” and Limit Prescribed-2nd Page

17. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

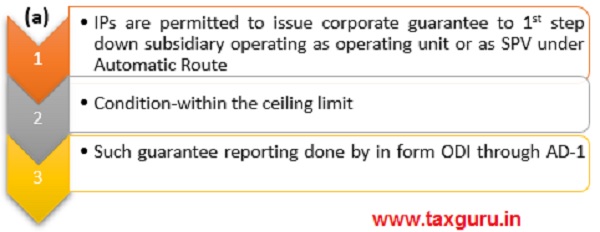

18. ODI-Automatic Route –4 Conditions for Indian Entity may offer Guarantee-Corporate or personal

19. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

20. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

21. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

22. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

23. ODI-Automatic Route –4 Conditions for Investment or Financial Commitment

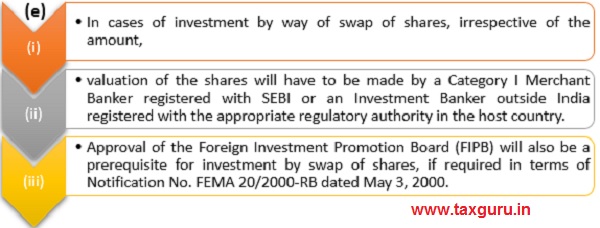

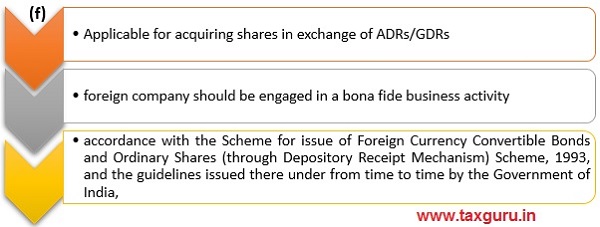

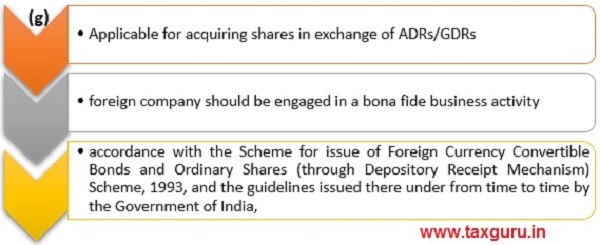

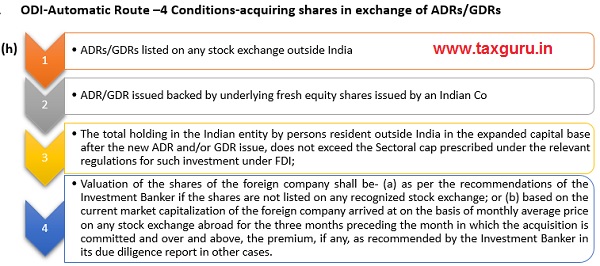

24. ODI-Automatic Route –4 Conditions-acquiring shares in exchange of ADRs/GDRs

25. ODI-Automatic Route –4 Conditions-acquiring shares in exchange of ADRs/GDRs

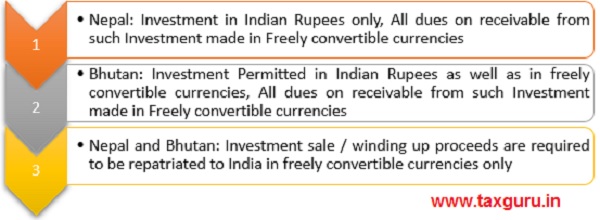

26. ODI-Automatic Route –5 Investment or FC in Nepal and Bhutan

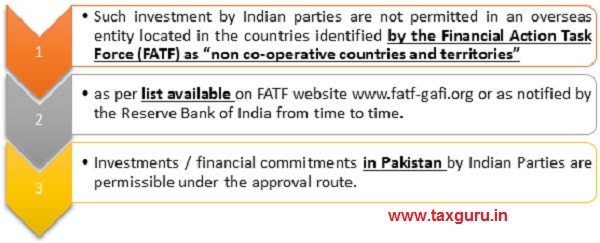

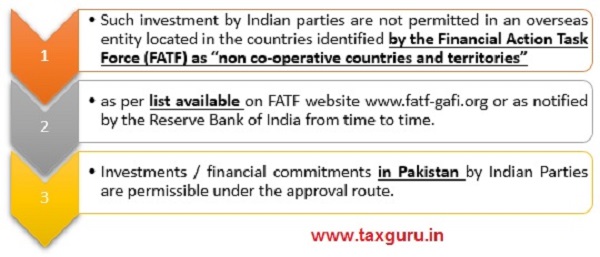

27. ODI-Automatic Route –6 FAFT Countries

28. ODI-Automatic Route –Investment through Special Purpose Vehicle (SPV)

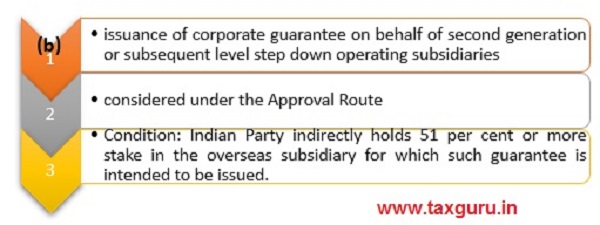

29. Issue of guarantee by an Indian Party to step down subsidiary of JV / WOS-AUTOMATIC ROUTE (AR)

30. Issue of guarantee by an Indian Party to step down subsidiary of JV / WOS-AUTOMATIC ROUTE (AR)

31. Issue of guarantee by an Indian Party to step down subsidiary of JV / WOS-AUTOMATIC ROUTE (AR)

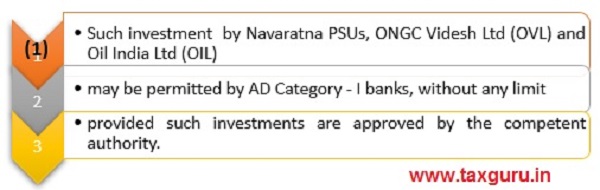

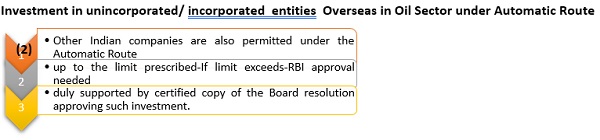

32. Investment in unincorporated/ incorporated entities Overseas in Oil Sector under Automatic Route

33. Investment in unincorporated/ incorporated entities Overseas in Oil Sector under Automatic Route

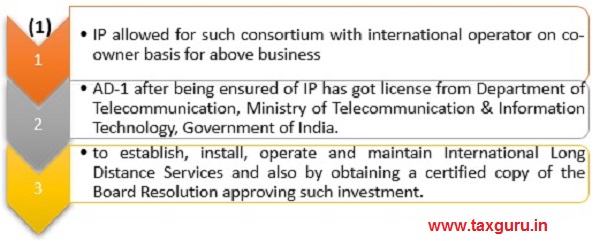

34. Construction and maintenance of submarine cable systems under the Automatic Route

35. Construction and maintenance of submarine cable systems under the Automatic Route

36. METHOD OF FUNDING-Out of One or More sources

37. METHOD OF FUNDING-General Permission for Person Resident in India for such Investment

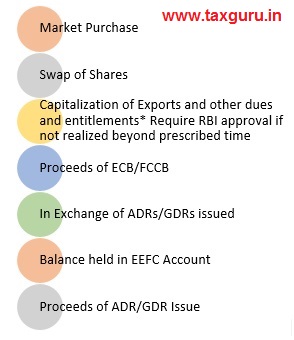

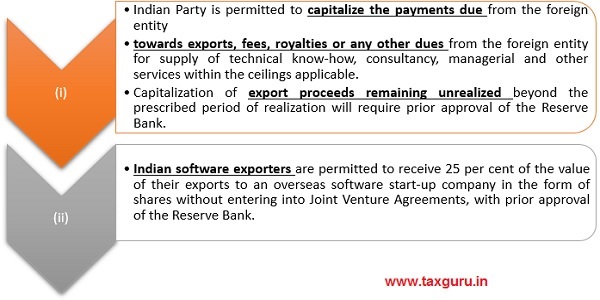

38. Capitalization of Exports and Other Dues

39. Investments (or financial commitment) engaged in Financial Services Sector-Additional Condition

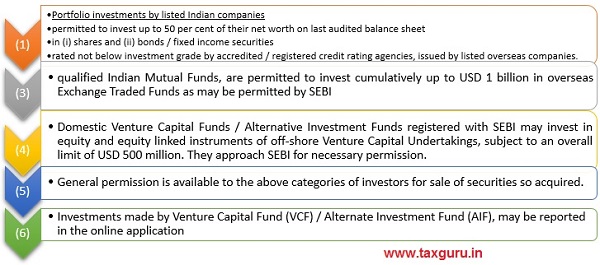

40. Investment in equity of companies registered overseas / rated debt Instruments

41. Investment in equity of companies registered overseas / rated debt Instruments (Cont.)

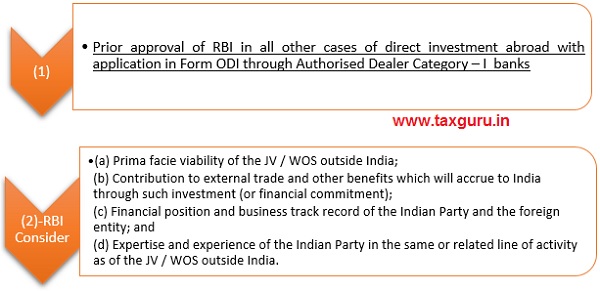

42. Approval of the Reserve Bank

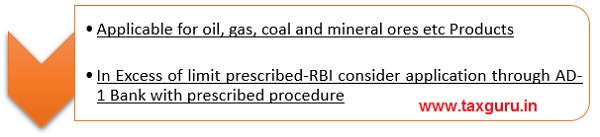

43. Investments in energy and natural resources sector-like Oil, Gas, Coal & Mineral ores

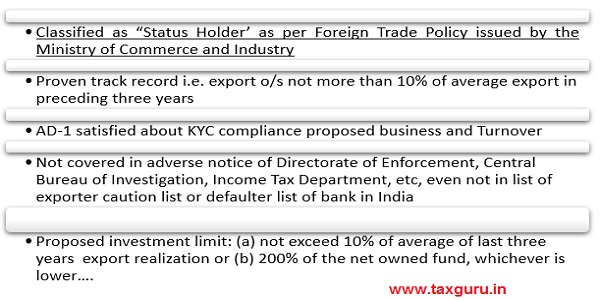

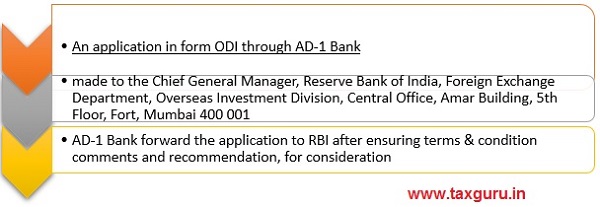

44. Overseas investments by proprietorship concerns/Unregistered Partnership firm- Eligibility Criteria-Approval Route Condition

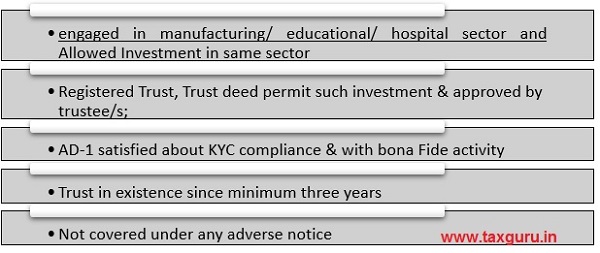

45. Overseas investments by Registered Trust-Eligibility Criteria-Approval Route Condition

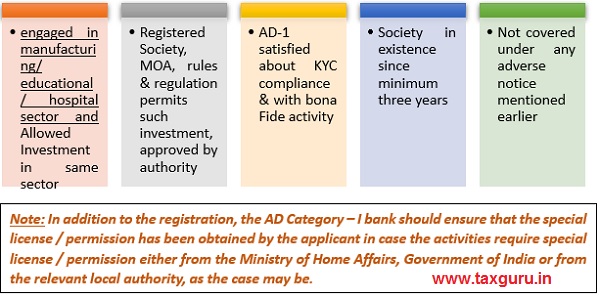

46. Overseas investments by Registered Society-Eligibility Criteria-Approval Route Condition

47. Investments in proprietorship concerns/Unregistered Partnership firm, Society or Trust- Compliance

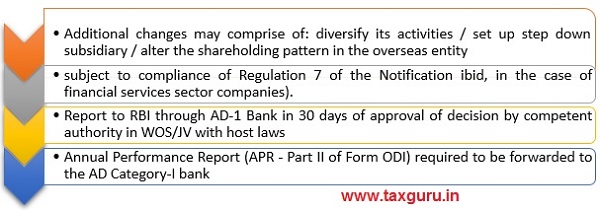

48. Post investment changes / additional investment (or financial commitment) in existing JV / WOS

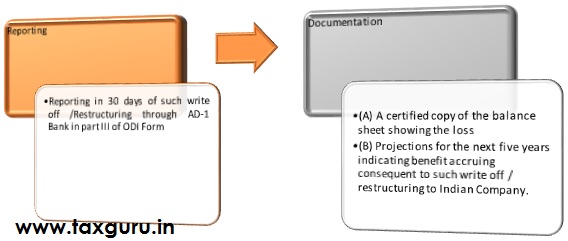

49. Restructuring of the balance sheet of the overseas entity involving write off of capital and receivables- Primary Details

49. Restructuring of the balance sheet of the overseas entity involving write off of capital and receivables- Primary Details

50. Write off of capital and receivables Reporting Compliance & Documentation (Automatic & Approval Route)

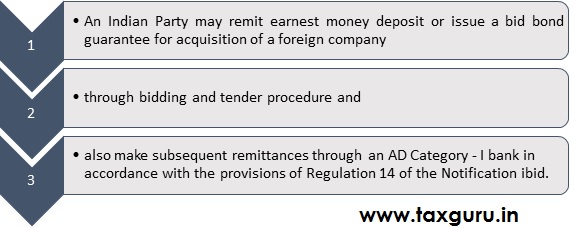

51.Acquisition of a foreign company through bidding or tender procedure

52. (1) Obligations of Indian Party (IP) and Resident Individual (RI) for Direct Investment Abroad

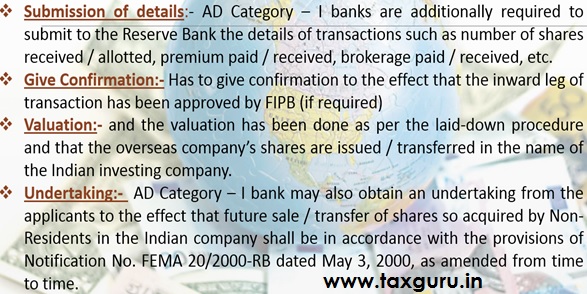

53. (1) Obligations of AD Category 1 Bank-Monitor Receipt of such documents and verify its Bona Fide of them

(2) Obligation-APR for Unincorporated Entity in the Oil Sector

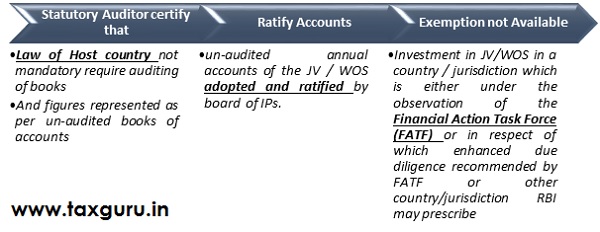

(3) Obligations by IPs-APR submitted based on Unaudited Accounts

Where the law of the host country does not mandatorily require auditing of the books of accounts of JV / WOS, the Annual Performance Report (APR) may be submitted by the Indian Party based on the un-audited annual accounts of the JV / WOS provided:

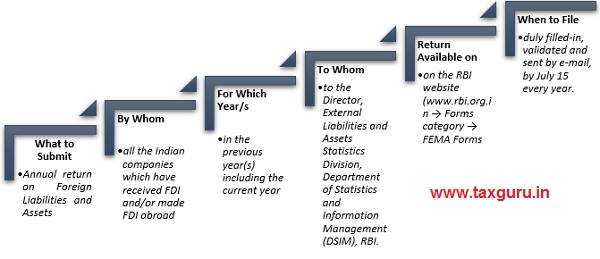

56. An annual return on Foreign Liabilities and Assets (FLA)

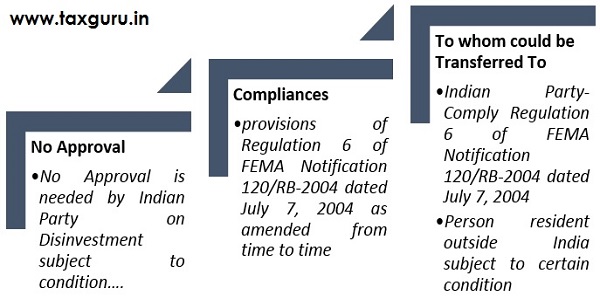

57. Transfer by way of sale of shares of a JV / WOS

58. Transfer by way of sale of shares of a JV / WOS to Resident outside India-Conditions

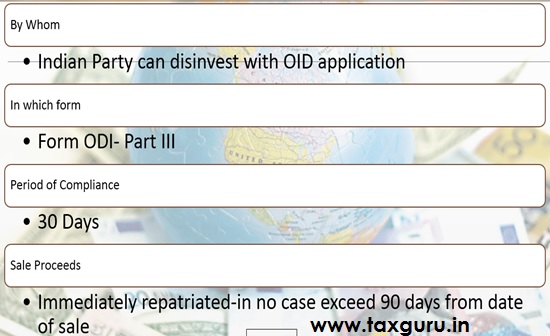

Note: India party is required to submit details of such disinvestment through its designated AD category-I bank within 30 days from the date of disinvestment.

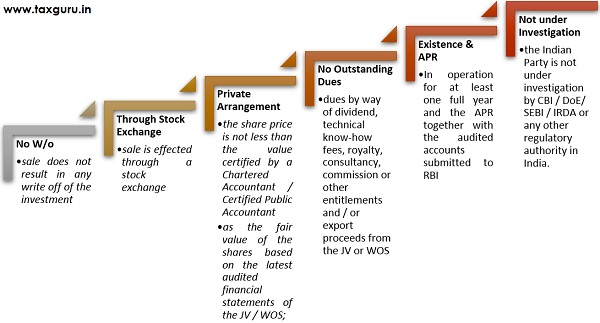

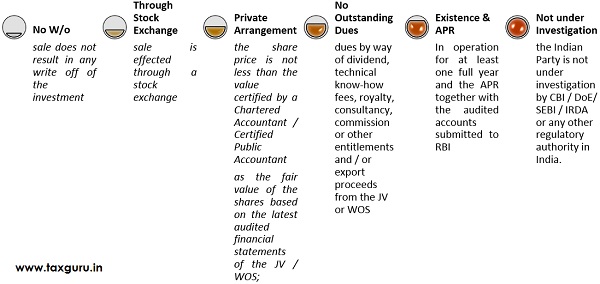

59. Transfer by way of sale of shares of a JV / WOS involving write off of the investment (or FC)-Automatic Route

(1) Indian party may disinvest Without prior approval of RBI where amount repatriated is less than the original amount invested:

60. Transfer by way of sale of shares of a JV / WOS involving write off of the investment (or FC)-Automatic Route

(2) Such disinvestments shall be subject to the conditions (same condition of without write off:

(3) If any of the condition mentioned earlier is not satisfied-RBI prior approval is required to be obtained

61. Pledge of shares of Joint Venture (JV), Wholly Owned Subsidiary (WOS) and Step Down Subsidiary (SDS)

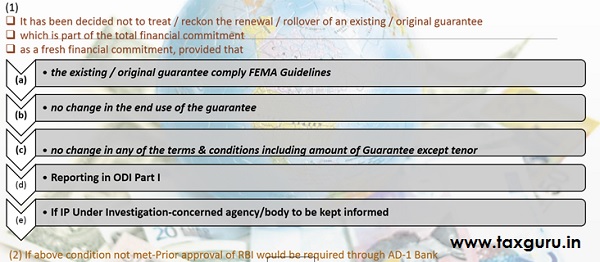

62. Rollover of Guarantees

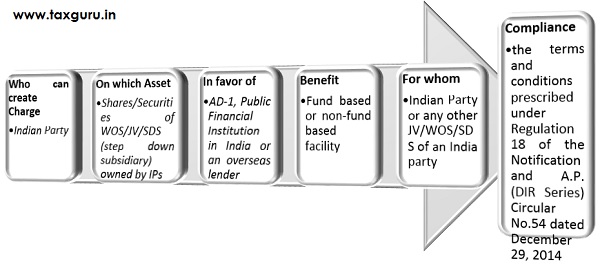

63. Creation of charge on domestic and foreign assets

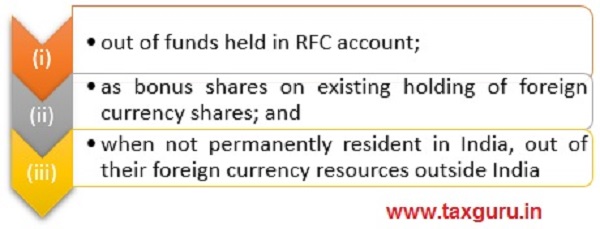

64. Overseas Direct Investments by resident individuals

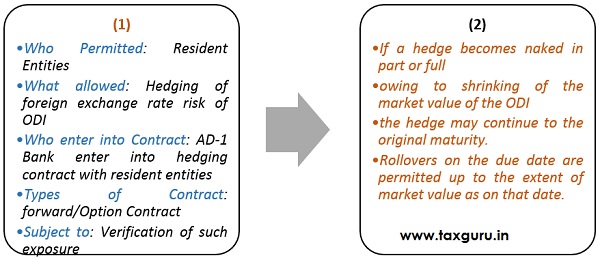

65. Hedging of overseas direct investments

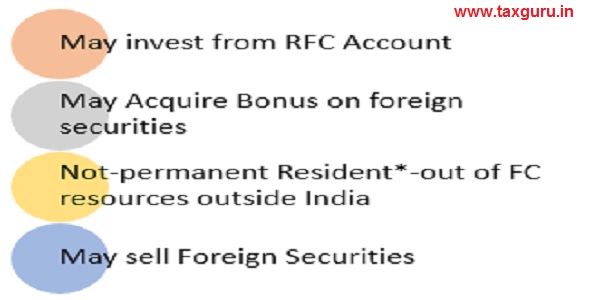

66. Opening of Foreign Currency Account abroad by an Indian Party- Conditions

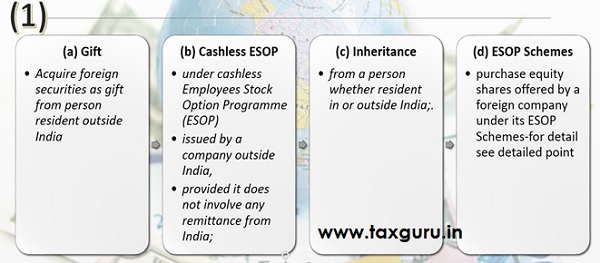

67. Permission for purchase/ acquisition of foreign securities in certain cases- “GENERAL PERMISSION TO RESIDENT ENTITY”

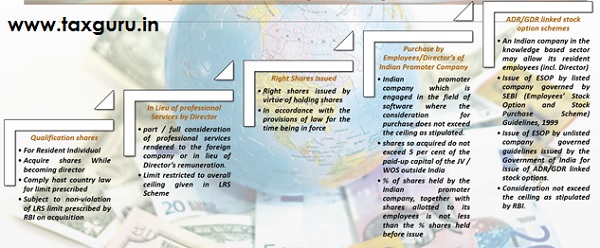

68. Purchase equity shares offered by a foreign company under its ESOP Schemes- “GENERAL PERMISSION”- Detailed

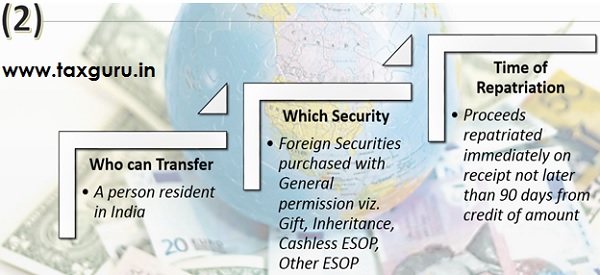

69. Transfer by way of sale of foreign securities in certain cases- “SPECIAL PERMISSION TO RESIDENT ENTITY”

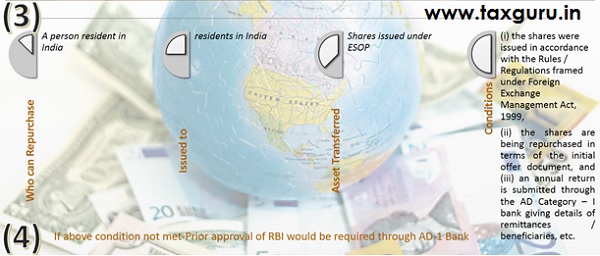

70. Transfer by way of Repurchase of shares by Foreign Company- “SPECIAL PERMISSION TO RESIDENT ENTITY”

71. General permission in certain cases-Foreign Security acquired by Resident Entity, if it represents

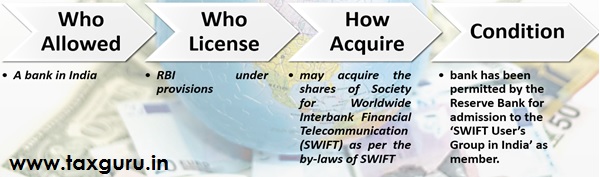

72. Acquiring the shares of SWIFT by a resident Bank

73. Issue of Indian Depository Receipts (IDRs)

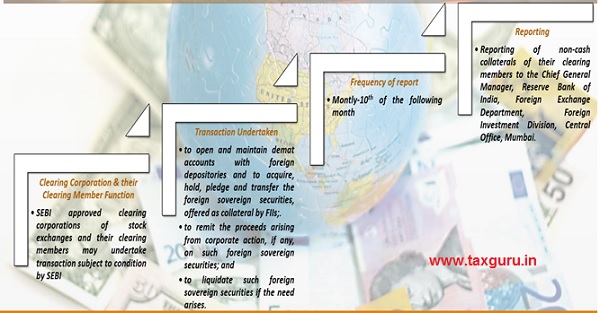

74. Maintenance of collateral by FIIs for transactions in derivative segment- opening of demat accounts by Clearing Corporations and Clearing Member

GENERAL PART -II- OPERATIONAL INSTRUCTIONS TO AUTHORIZED DEALER BANK

1. Designated Branches

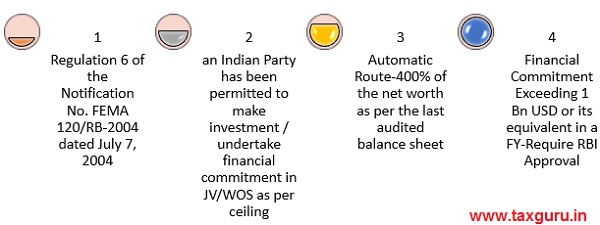

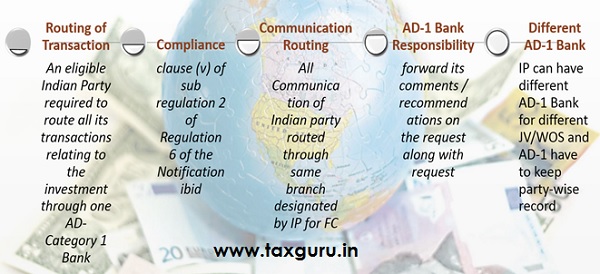

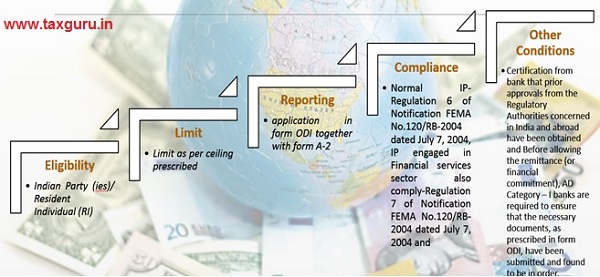

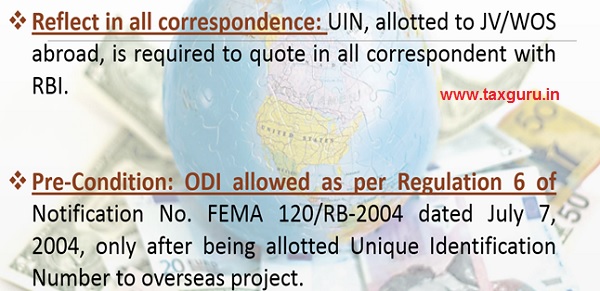

2. Investments under Regulation 6 of Notification No. FEMA 120/2004-RB dated July 7, 2004

3. Investments under Regulation 6 of Notification No. FEMA 120/2004-RB dated July 7, 2004- Explanation

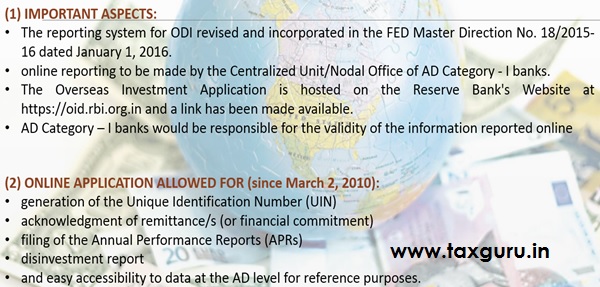

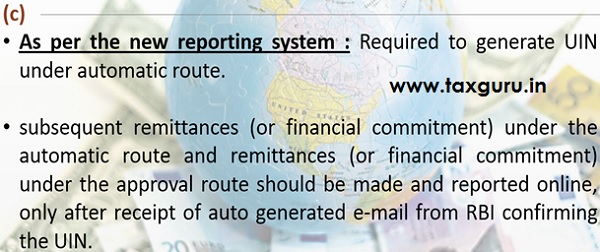

4. General procedural instructions- Online Reporting Allowed for ODI Transactions

5. General procedural instructions- Online Reporting Allowed for ODI Transactions-Continue

6. General procedural instructions- Online Reporting Allowed for ODI Transactions-Continue

7. General procedural instructions- Online Reporting Allowed for ODI Transactions-Continue

8. Investments (or financial commitment) under Regulation 11 of Notification No. FEMA.120/2004-RB dated July 7, 2004

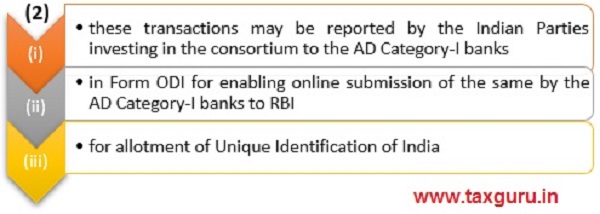

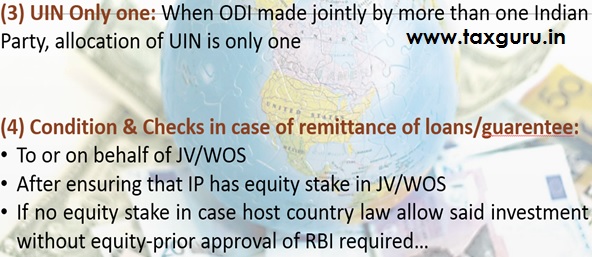

9. Allotment of Unique Identification Number (UIN)

10. Investment by way of share swap

11. ODI under Regulation 9 of Notification No. FEMA.120/2004-RB dated July 7, 2004- Certain Cases require prior approval

12. Purchase of foreign securities under ADR / GDR linked Stock Option Scheme

13. Transfer by way of sale of shares of a JV / WOS outside India

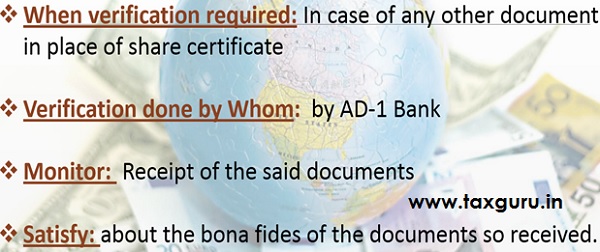

14. Verification of evidence of investment

15. Opening of Foreign Currency Account abroad by an Indian Party

Conclusion:

Almost simplified procedures for ODI reflects lenient approach of government as compared to FDI regulations which keeps on changing so frequently which shows extra precautions by Indian government. Legal issues found more in Foreign Direct Investment (Now Non-Debt Instrument and Debt Instrument Regulations from FY 2019) than Foreign Investment in Joint Venture or Wholly Owned Subsidiary related litigations.

Author Bio