As Indian economy is adopting its pace with globalisation and digitisation, different spices of accounts suited for the intended economical/personal purpose has to be devised. Hence to cater and nourish these thought processes, Foreign Exchange Management (Deposit Regulations), 2016 has brought in various provisions and guidelines with regards to allow ability to open, operate, maintain Resident and Non-Resident bank accounts in India in Foreign currency and in Indian currencies. Non-Resident can open broadly two accounts: Non-Resident Ordinary Account (NRO) and Non-Resident (External) Rupee Accounts. Provisions also take care of accounts to be opened, maintained as well as to be closed as per the said provisions and guidelines of Deposit Regulations.

Foreign Exchange Management (Deposit) Regulations, 2016 come into force from the date of their publication in the Official Gazette except sub-regulation (2) of Regulation 7. Sub-regulation (2) of Regulation 7 is deemed to have come into force with effect from 21st January, 2016.

Page Contents

1. Important Definition

‘Deposit’ includes deposit of money with a bank, company, proprietary concern, partnership firm, corporate body, trust or any other person;

‘FCNR (B) account’ means a Foreign Currency Non-Resident (Bank) account referred to in clause (ii) of sub-regulation (1) of Regulation 5;

‘Non-Resident Indian (NRI)’ means a person resident outside India who is a citizen of India.

‘NRE account’ means a Non-Resident External account referred to in clause (i) of sub-regulation (1) of Regulation 5;

‘NRO account‘ means a Non-Resident Ordinary account referred to in clause (iii) of sub-regulation (1) of Regulation 5;

‘SNRR account’ means a Special Non-Resident Rupee account referred to in sub-regulation (4) of Regulation 5;

2. Types of Accounts

1. Non-Resident (Ordinary) Account

2. Non-Resident (External) Rupee Account Scheme

3. Special Non-Resident Rupee Account (SNRR)

4. Foreign Currency (Non-Resident) Account (Banks) Scheme (FCNR)

5. Exchange Earner’s Foreign Currency (EEFC) Account

6. Resident Foreign Currency (RFC) Account Resident Foreign Currency (Domestic) [RFC(D)] Account

7. Diamond Dollar Account Scheme

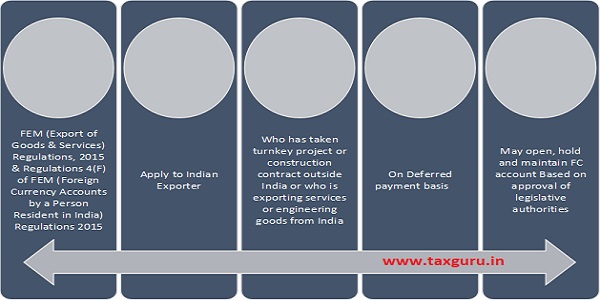

8. FC Account by exporter undertaking projects or supplying on deferred payment

9. FC Account by Indian Agent o shipping or airline companies incorporated outside India

10. Account by Ship manning/ crew managing agencies in India

11. Foreign Currency account by project offices of foreign companies

12. FC Account by Indian company receiving foreign Investment under FDI

13. FC Account by organizers of International seminars, conferences or conventions

14. Foreign Currency and SNRR Account by Unincorporated JV

15. FC Account by account of diplomatic staff

16. FC Account to adjust value of goods against imports and exports with RBI approval

3. Restriction on Deposits

Save as otherwise provided in the Act or Regulations or in rules, directions and orders made or issued under the Act, no person resident in India shall accept any deposit from, or make any deposit with, a person resident outside India:

Provided that the Reserve Bank may, on an application made to it and on being satisfied that it is necessary so to do, allow a person resident in India to accept or make deposit from or with a person resident outside India.

4. Differences Between Major Accounts

a. Non-Resident (Ordinary) Account (NRO)

b. Non-Resident (External) Rupee Account Scheme (NRE)

c. Special Non-Resident Rupee Account (SNRR)

d. Foreign Currency (Non-Resident) Account (Banks) Scheme (FCNR)

e. Exchange Earner’s Foreign Currency (EEFC) Account

f. Resident Foreign Currency (RFC) Account

NRO-Non-Resident (Ordinary) Accounts, NRE-Non-Resident (External) Rupee Account, FCNR-Foreign Currency NOn-Resident Account, RFC-Resident Foreign Currency Accounts, EEFC-Exchange Earner Foreign Currency Accounts, SNRR-Special Non-Resident Rupee Account

POINTS |

NRO |

NRE |

FCNR |

RFC |

EEFC |

SNRR |

Intention |

Going abroad with intention of being NRI |

Remittance of Fund in Free Foreign Exchange |

Keep the FC in the same denomination |

Specially useful for NRI returning to India allowed to maintain FC for trans from overseas bank accounts |

Crediting its foreign exchange income |

Any Non-Resident having interest in business in India |

Currency |

INR |

INR, deposit in FC convert in INR at Buying rate |

FC (10 major FC) |

FC like AUD, CAD, Euro, GBP, JPY, USD etc |

FC |

INR |

Source of Fund |

From within the country (India), FN-only credit of Interest |

Travelers cheques, notes, only repatriable income is credited, INR not deposited, |

Export receipts, remittance abroad, local investment |

From employment or business abroad, Super-annuation or pension, sale of assets, bank a/c, int & dividend from abroad, fund from FCNR & NRE |

Foreign exchange earnings excl. claim settled by ECGC / insurance co in INR, pay PC in INR or FC |

Incidental to the business |

Who can Open |

NRI, Intention deposit from India & not to repatriate, Foreign Nationals, No Pakistan & Bangladesh National except approval of RBI |

NRI, PIO/OCI, for opening account, FC need to be deposited for opening, only NRI/PIO can open not POA |

BY NRI |

Resident Indian without approval of RBI with condition foreign stay min 1 yrs short trip to India ignored |

Indian Resident like SEZ |

Any Non-Resident, Entity or person from Pakistan & Bangladesh required prior approval of RBI |

Period |

No Restricted, Foreign National- Max 6 Month, no other credit to account other than int |

No Restriction |

=1 yr but <2 Yr, >=2 yrs but <3 yrs, 3 yrs, 1-3 yr (USD, GBP, DKK, CHF, SEK) & 1-2 yr (Euro, JPY, CAD, AUD) |

NA |

No restriction |

Max 7 years or business operations being closed, whichever is earlier |

Type of Account |

Current, Saving, Recurring, Fixed |

Current, Saving, Recurring, Fixed |

Only TD |

TD, SD, Current |

Current A/c |

Current A/c |

Min. Deposit |

Rs. 5L, Rs. 1L for Term Deposit |

Rs. 5L, Rs. 1L for Term Deposit |

USD-1000, GBP-500, JPY-125000, Euro-750 , CAD & USD-1500, DKK-CHF-SEK-1000 |

USD-5000, GBP-3500, JPY-500000, EUR-5000 |

NA |

NA |

Joint Account |

Resident in India-Former or Survivor Basis, NRI with NRI-PIO |

Only with other NRI, with resident –former or survivor can act as POA |

With two or more Non-Resident not allowed with Indian resident |

With NRI or with Indian Resident (former or survivor basis) |

NA |

NA |

Nomination |

Allowed |

Allowed |

Not required perhaps as two or more account holder |

Can be Resident or other NRI, if resident after demise transfer fund in INR or else remitted abroad |

NA |

Allowed-NRI, after demise fund transferred to NRO account |

Rate of Interest |

Saving-Normal

|

Saving-Ceiling at of six months USD LIBOR, TD-Ceiling rate of USD LIBOR of corres-ponding period |

Fixed or Floating-celling rate of LIBOR or SWAP rates |

NA |

NA |

No Interest |

Taxation of Interest (TDS) |

TDS Rate |

Tax free till the time not permanently returning to India Sec 10(4) (ii), no tax on wealth as balance |

Exempt U/s 10(15) (iv)(fa) |

NA |

No interest hence no tax |

No tax |

Transfer of Funds |

NRO to NRE-Sub to Tax-Eligible Credit |

Resident account or RFC account if permanently settled |

As NRE account |

Going abroad back for longer period, either remit in foreign or transfer to NRE or FCNR a/c |

Credited to FCNR or NRE after change of status |

NRO to SNRR not allowed |

Power of Attorney |

Allowed, Limited-local payment, remittances only to NRI account, investment in local if allowable, can’t transfer to other NRE, can not gift to other NRI on behalf of NRI account holder |

Allowed, Limited-local payment, remittances only to NRI account, investment in local if allowable, can’t transfer to other NRE, can not gift to other NRI on behalf of NRI account holder |

Allowed |

Allowed same as NRE but can not open account on behalf |

Not allowed |

Not allowed |

Foreign Currency Risk |

Yes |

Yes |

No |

No |

No |

Yes |

Repatriabiity |

Remittance of Max. 1 Million sub to bona fide purpose |

No cap limit, if NRI/PIO deceased, fund transferred to NRI nominee account abroad |

Fully repatriable subject to approval and AD find it bona fide. |

Fully repatriated |

NA |

Eligible for repatriation |

Loan Against |

Allowed subject to Margin requirement, Usage not allowed for relending & other banned criteria |

Allowed subject to condition |

Same as NRE Deposits |

No Loans allowed |

Not allowed |

Not allowed |

Immediate Close |

FN-temp a/c opened to collect their dues in India hence converted Resident a/c to NRO-after purchase closed |

After permanently being settled in India |

Like NRE deposits |

If permanently going back to abroad then remit fund abroad or transfer to FCNR or NRE a/c & then close this a/c |

NA |

NA |

Legal Backing |

Schedule 3-Regulation 5(1)(iii) |

See Regulation 5(1) (i) |

Regulation 5(1) (ii) Schedule 2 |

NA |

NA |

NA |

Status Changed |

NA |

Changed to Resident account or RFC account (if eligible), can credit like PF settlement to NRO account |

If changed to Resident then even continue to hold deposit till maturity and after maturity transfer to either RFC or resident deposit account |

Transfer the amount to FCNR or NRE account or remit abroad if he becomes back NRI |

NA |

After becoming resident, account will be changed to Resident deposit account |

Premature withdrawal |

NA |

NA |

Allowed, penal int charged around 1%, if withdrawn for taking higher interest benefit, penal interest not charged if renewed for more than unexpired period |

NA |

NA |

NA |

5. Other Accounts Descriptions

(A) Diamond Dollar Account Scheme

(B) FC Account by exporter undertaking projects or supplying on deferred payment

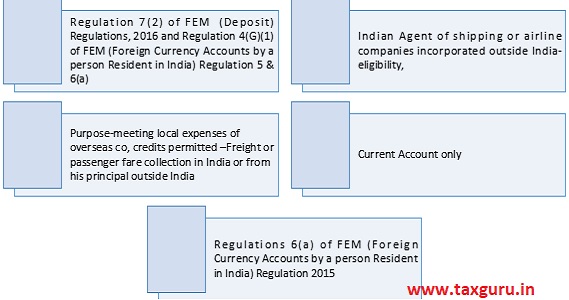

(C) FC Account by Indian Agent or shipping or airline companies incorporated outside India

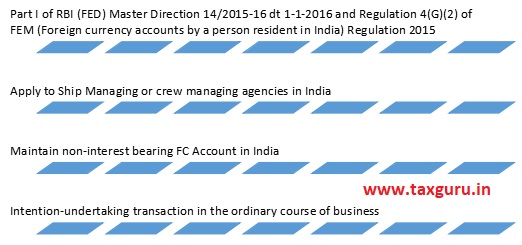

(D) FC Account by Ship manning/ crew managing agencies in India

(E) Foreign Currency account by project offices of foreign companies

Part I of RBI (FED) Master Direction 14/2015-16 dt 1-1-2016 and Regulation 4(G)(3) of FEM (Foreign currency accounts by a person resident in India) Regulation 2015

Apply Project Office of Foreign companies

Maintain non-interest bearing FC Account in India

Intention-for the project to be executed in India

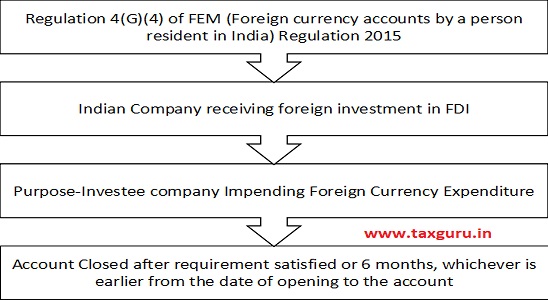

(F) FC Account by Indian company receiving foreign Investment under FDI

6. Resources Or Base Of Article

RBI Notification:

Link: https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10325&Mode=0

7. Conclusion:

Having realised importance of specific circumstances and need of economy development of India, different kind of accounts have been developed but due to pace and intensity with complexity of digital transactions are concerned, it is recommended strongly all International Organisation to form specific committee who would shelter legal tenability for digital transactions which is to be routed through specific mechanism only and to develop specific account of those who do not have physical PE but who are falling themselves into either SEP (Significant Economic Presence) and EL (Equalisation Levy) with virtual presence could be tendered & monitored more strictly and direct control of RBI would be there to check tax evasion.

Source: Foreign Exchange Management (Deposit) Regulations, 2016

Author Bio