The Hon’ble Delhi High Court’s hearing in W.P. (C) 14882/2025 – Sumit Garg v. CBDT & Anr. on 29 October 2025 has brought to the fore a critical compliance anomaly: the exclusion of Transfer Pricing (TP) cases from the benefit of extended Income Tax Return (ITR) timelines under CBDT Circular No. 15/2025. This article presents a doctrinally enriched analysis of the proceedings, the CBDT’s stance, judicial directions, and historical precedents, with citations wherever available.

Page Contents

- I. Background: Circular No. 15/2025 and the Compliance Divide

- II. CBDT’s Submission Before the Delhi High Court

- III. Court’s Interim Directions and Procedural Status

- IV. Historical Practice: Inclusive Treatment of TP Cases

- V. Judicial Precedents: High Courts on ITR Extensions

- VI. Doctrinal Analysis and Stakeholder Impact

- VII. Conclusion: Awaiting Judicial Course Correction

I. Background: Circular No. 15/2025 and the Compliance Divide

CBDT’s Circular No. 15/2025, dated 29 October 2025, extended:

- Tax Audit Report (TAR) due date under Section 44AB to 10 November 2025

- ITR filing due date under Section 139(1) to 10 December 2025

However, Transfer Pricing reports (Form 3CEB) under Section 92E were excluded, creating two distinct compliance scenarios:

| Scenario | Applicability | Form 3CEB Due | TAR Due | ITR Due |

| 1 | TP only (Sec. 92E, no Sec. 44AB) | 31 Oct 2025 | NA | 30 Nov 2025 |

| 2 | TP + Tax Audit (Sec. 92E + Sec. 44AB) | 31 Oct 2025 | 10 Nov 2025 | 10 Dec 2025 |

This exclusion triggered litigation, with Sumit Garg’s petition challenging the arbitrary denial of extension to TP-only cases.

II. CBDT’s Submission Before the Delhi High Court

As per the record of proceedings and updates shared by counsel Divyanshu Agrawal:

- Section 44AB and Section 92E are independent obligations

- Form 3CEB utility was released on 1 April 2025, hence no delay

- Extension applies only to TAR, not TP reports

The Department argued that TP-only assessees (Scenario 1) were not prejudiced, as their ITR deadline remained 30 November 2025.

III. Court’s Interim Directions and Procedural Status

- Directed CBDT to file a detailed counter-affidavit, addressing:

> Infrastructure readiness

> Utility release timelines

> Rationale for TP exclusion

- Noted that AIFTP’s petition substantially covered the same issues

- Permitted withdrawal of Sumit Garg’s petition with liberty to assist in AIFTP’s case

- Next hearing scheduled for 25 November 2025

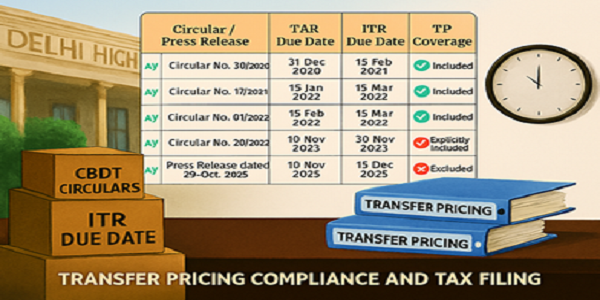

IV. Historical Practice: Inclusive Treatment of TP Cases

A review of CBDT circulars over the past six years shows consistent inclusion of TP cases in extended ITR timelines:

| AY | Circular / Press Release | TAR Due Date | ITR Due Date | TP Coverage |

| 2020–21 | Press Release dated 30th December 2020 | 31 Dec 2020 | 15 Feb 2021 | Included |

| 2021–22 | Circular No. 17/2021-Income Tax Dated: 09/09/2021 | 15 Jan 2022 | 15 Mar 2022 | Included |

| 2022–23 | Circular No. 01/2022-Income Tax | 15 Feb 2022 | 15 Mar 2022 | Included |

| 2024–25 | Circular No. 18/2024 (F. No. 225/205/2024/ITA-II) | 10 Nov 2024 | 15 Dec 2024 | Explicitly Included |

| 2025–26 | Press Release dated 29 Oct 2025 | 10 Nov 2025 | 10 Dec 2025 | Excluded |

This table reflects a clear departure in AY 2025–26, where Transfer Pricing cases were excluded from the extended ITR timeline for the first time in six years. Prior circulars either explicitly included TP cases or did so implicitly by extending deadlines for all audit-linked filings.

This year’s exclusion marks a departure from administrative consistency, raising concerns of arbitrariness and unequal treatment.

V. Judicial Precedents: High Courts on ITR Extensions

1. Chamber of Tax Consultants v. CBDT (2020) [2020] 121 taxmann.com 11 (Bom)

This landmark Bombay High Court decision arose during the COVID-19 pandemic when the CBDT delayed the release of audit utilities and issued last-minute circulars extending due dates. The Chamber of Tax Consultants argued that such unpredictability disrupted professional schedules and created unnecessary compliance pressure. The Court acknowledged the hardship faced by taxpayers and professionals, emphasizing that the government must adopt a predictable and transparent approach to deadline management. It criticized the practice of issuing extensions at the eleventh hour and urged the CBDT to consult stakeholders before finalizing timelines. Although Transfer Pricing was not the central issue, the judgment implicitly covered TP cases by recognizing the broader compliance ecosystem. The ruling set a precedent for judicial scrutiny of administrative delay and opacity.

2. All Gujarat Federation of Tax Consultants v. Union of India, R/SPECIAL CIVIL APPLICATION NO. 13653 of 2020, Date : 08/01/2021

In this case, the Gujarat High Court dealt with representations from tax professionals seeking extensions due to pandemic-related disruptions and technical glitches in the income-tax portal. The Court directed the CBDT to consider these representations sympathetically and avoid penalizing taxpayers for delays caused by systemic issues. It invoked the principles of natural justice and legitimate expectation, holding that taxpayers should not suffer due to administrative inefficiencies. Transfer Pricing cases were part of the extended compliance window, and the judgment reinforced the expectation that all categories of taxpayers—including those with international transactions—should be treated equitably. The decision is often cited for its balanced approach to taxpayer rights and administrative accountability.

VI. Doctrinal Analysis and Stakeholder Impact

Article 14 Violation: Unequal Treatment of TP-Only Assessees

The exclusion of Transfer Pricing (TP)-only assessees from the extended ITR timeline under CBDT Circular No. 15/2025 raises serious concerns under Article 14 of the Constitution, which guarantees equality before the law. Assessees with international transactions but no audit obligation under Section 44AB are denied the same compliance relief granted to those with both TP and audit obligations. This creates a discriminatory classification without any intelligible differentia or rational nexus to the objective of easing compliance burdens. The CBDT’s justification—that Form 3CEB utility was released early—is procedural, not substantive, and fails to address the complexity of TP documentation. Courts have consistently held that administrative convenience cannot override constitutional guarantees of equal treatment.

Compliance Burden: TP Documentation Involves International Benchmarking

Transfer Pricing compliance under Section 92E is inherently more complex than standard tax audits. It requires detailed documentation of international transactions, functional and economic analyses, and benchmarking studies using global comparables. These tasks often involve coordination with foreign affiliates, external consultants, and database subscriptions—none of which are trivial or time-bound by domestic utility release dates. The assumption that early availability of Form 3CEB utility equates to readiness for compliance ignores the substantive workload involved. Denying TP-only assessees an extension disregards the real-world challenges of cross-border documentation and undermines the principle of fair opportunity to comply.

Administrative Inconsistency: Past Circulars Included TP Cases Without Exception

CBDT’s past circulars—such as 30/2020, 17/2021, 01/2022, 20/2023, and 18/2024—either explicitly or implicitly extended ITR deadlines for all assessees subject to audit, including those under Section 92E. This consistent administrative practice created a legitimate expectation among taxpayers that TP cases would be treated on par with other audit-linked filings. The sudden exclusion in 2025, without stakeholder consultation or explanatory rationale, breaks this continuity and introduces uncertainty into the compliance framework. Such inconsistency not only disrupts planning but also erodes trust in the regulatory process. Courts have previously emphasized that deviation from settled practice must be justified with cogent reasons—none of which have been offered in this case.

Disruption of Parity: TP-Only Assessees Face Compressed Timelines Compared to TP + Audit Cases

Ironically, taxpayers with both TP and audit obligations are granted more time to file their ITRs (up to 10 December 2025), while TP-only assessees must comply by 30 November 2025. This creates a paradox where those with greater compliance burden enjoy longer timelines, while those with lesser obligations are penalized with shorter windows. The disparity is not only illogical but also procedurally unfair, as TP-only assessees often face the same documentation challenges without the benefit of extended relief. Such compressed timelines increase the risk of errors, last-minute filings, and potential penalties. The principle of parity demands that similarly situated taxpayers be treated alike—CBDT’s current stance violates this foundational tenet.

VII. Conclusion: Awaiting Judicial Course Correction

The Delhi High Court’s intervention in W.P. (C) 14882/2025 is a critical moment for tax compliance jurisprudence. The exclusion of TP cases from the 2025 extension is unprecedented and legally tenuous, especially in light of past inclusive practice and judicial guidance.

The tax fraternity awaits a reasoned ruling on 25 November 2025—one that restores equity, consistency, and administrative accountability. If the CBDT’s stance is upheld, it risks setting a regressive precedent. If corrected, it will reaffirm the judiciary’s role as a constitutional check on executive discretion.

Author Bio