About The Author

Born in a humble middle-class family in Jalandhar (Punjab) in 1962, Ravinder, an avid academic turned every obstacle into opportunity through sheer hard work, graduated in Bachelors of Commerce from DAV College, Jalandhar. After graduation he stepped into nonetheless a rigorous course of accountancy from Institute of Chartered Accountants of India and simultaneously done his Masters of Commerce from Himachal Pradesh University. All of this did not fulfill his appetite for knowledge he moved on to add another feather in his hat by doing Bachelors of Law.

Kicked off his career as a practicing Chartered Accountant, enlightened and awakened the masses on the taxation matters by writing articles in various leading newspapers and journals.

Climbing the ladder at a steady pace to scale mountainous heights and be at the helm of professional affairs with dignity made an unconditional contribution to the profession being Vice- Chairman of Jalandhar Branch of NIRC of ICAI from 1995-1998, Chairman Jalandhar branch of NIRC of ICAI for the year 2008-2009, Member Regional Tax Advisory Committee of CBDT, New Delhi, Member Direct Tax Committee of ICAI for the Year 2011-2012, Special Invitee Direct Tax Committee of ICAI for the Year 2012- 2013,Member Indirect Tax Committee of ICAI for the Year 2013-2014,Member Board of Studies of ICAI of 2014-15,Senate Member of Guru Nanak Dev University, Amritsar from 01.07.2014 to 30.06.2016, Member of Committee on Economic, Commercial Laws & WTO, and Economic Advisory of ICAI for the Year 2017- 2018..At present he is on the panel of authors of Tax Guru.

Tax laws are a part of the dynamic laws which always keep changing. Not only amendment but its interpretation and meaning also keeps changing, making it imperative for the taxpayers to keep a constant track of it on an ongoing basis.

The book ‘TDS: A 3-DEE SYSTEM’ is a mobile guide for the taxpayers. All the sections are incorporated in the form of Frequently Asked Question (FAQ). It is an attempt to keep the taxpayers updated as well as informed and provides all the information related to TDS in summarized as well as simple manner.

In case of any doubt or query, readers are requested to approach the author at ca.rskalra@yahoo.com. Author requests for the suggestions and feedback from the readers for making it better.

Wish you all a Happy Reading.

– CA R.S. KALRA

M No: 9888927000

Date 11/11/2020

CA SANJAY KUMAR AGGARWAL

FOREWORD

I am extremely glad to know that CA R.S.Kalra, is bringing out a book on “TDS: A 3-DEE System”. I had the opportunity of meeting CA R.S. Kalra in year 2006 in a Seminar. I have been going through various articles written by CA R.S. Kalra. He possesses a unique skill to explain highly complicated and intricate issues in very simple language exercising economy of words. He is able to put proper focus on the central theme of a complicated tax issue.

Speaking of Experience, CA R.S. Kalra has been practicing Chartered Accountant having an in depth experience of more than 33 years in Direct Taxes. There is no doubt that his vast experience and wisdom will contribute in the better understanding of Income Tax Law.

I have gone through this book. The book has been written in a style which is easy to grasp. The complexities of taxation issues related to TDS and TCS have been explained in a very simple manner. A tax payer as well as tax consultant can easily refer to this book for proper answer to the doubts plaguing his mind. The precautions to be observed by the taxpayers and the pitfalls to be avoided have been very clearly pointed out. I am of the firm view that this book will be of great help not only to the taxpayers but also to the members of professional bodies and the officials of the Income tax Department.

This book represents a systematic codification of all the ingredients required to understand the Tax Deduction provisions of the Income Tax Act,1961 It is a commendable compendium of legal and procedural aspects of Income Tax Act. The author has highlighted the relevant Circulars, Notification and rules. The analysis of the relevant provisions is also handled in a masterly fashion.

I congratulate CA R.S. Kalra for his commendable endeavor to bring out this wonderful book.

I wish him great success in this venture.

(C.A. Sanjay Kumar Aggarwal)

What Professionals Say:

“If there’s anyone who can explain Tedious TDS in so much detail yet in an interesting way, it is my dear friend R.S.Kalra”

~Advocate Dinesh Sarna

“Infused by a can-do spirit Kalra has done a commendable job on bringing the impressive breadth of TDS under the bundle of 194 pages, this book is very handy on practical issues involved in TDS.”

~CA Ashwani Jindal

“TDS plays a significant role in collection of Taxes that is why with each passing year more and more sources of income are brought under its purview, therefore it is inevitable part of Practice and Tedious TDS: A 3 Dee System has all that a professional needs.”

~CA Dr. Ashwani Gupta

“Self-Explanatory is the correct word I will use for Kalra’s works but this one all the more befitted it. It contains the TDS provisions in an exhaustive manner and the FAQ’s addresses the need of practical issues involved in TDS.”

~CA Ashwani Randeva

“In this informative and insightful book, R.S.Kalra brilliantly explains TDS, Indian Taxation system has come of age where it will need such authors to explain Income Tax provisions in a simplified manner, Elegantly written and passionately engaging, Tedious TDS:A 3 Dee Taxation System, is another substantial achievement from one of the finest author CA R.S.Kalra”

~CA Manoj Soni & CA Rajiv Makol

Acknowledgement

I express my gratitude to Mahamandleshwar Swami Shanta Nand Ji for their ever showering blessings and inspiration.

I am always indebted to CA Dr. Girish Ahuja & CA Ashok Batra for their valuable guidance and continuous support in the field of taxation.

Writing a book on a specialised topic on a subject with so much practical applicability, needs an enthusiastic team and constant efforts. Resultantly, constant and determined involvement of CA Arvind Tuli, CA H.S. Makkar, CA Gurleen Singh Sahni, CA Parampreet Kaur, CA Gagandeep Kaur and CA Jasmeet Singh is highlighted here.

I heartily thank Harjot Singh, Ritik Chopra and Shubham Beri for their suggestions during this project.

Above all, knowledgeable readers are appreciated for their unshakable faith and steadfast patronage even during rapidly changing times. There is always an opportunity for betterment, improvement and refinement in all areas including writing a book for professionals. Therefore, positive suggestions, unprejudiced views and healthy criticism, if any, of readers is always welcome.

~CA R.S. Kalra

INDEX

| SECTION | PARTICULARS | PAGE NO. |

| Introduction | 14 | |

| 192 | TDS on Salary | 16 |

| 192A | TDS on Payment of Accumulated Balance Due to an Employee | 27 |

| 193 | TDS From Interest On Securities | 29 |

| 194 | TDS on payment of dividend | 33 |

| 194A | TDS on Interest (other than Interest on Securities) | 35 |

| 194B | TDS on winnings from Lottery, Game Shows, Puzzle etc. | 45 |

| 194BB | TDS on Winning from Horse Races | 47 |

| 194C | TDS on Payment to Contractor | 48 |

| 194D | TDS On Insurance Commission | 55 |

| 194DA | TDS on Payment in respect of Life Insurance Policy | 57 |

| 194E | TDS on Payments to Non-Resident Sportsmen or Sports Association | 60 |

| 194EE | TDS on Payments in respect of Deposit under National Savings Scheme | 61 |

| 194F | TDS on Payments on account of repurchase of units by Mutual Fund or Unit Trust of India | 62 |

| 194G | TDS on Commission on Sale of Lottery Tickets | 63 |

| 194H | TDS on Commission and Brokerage | 65 |

| 194I | TDS on Rent | 68 |

| 194-IA | TDS on Purchase of Immovable Property | 73 |

| 194-IB | TDS on Rent of Property | 90 |

| 194-IC |

TDS on Payment Made Under Specified Agreement |

92 |

| 194J | TDS on Professional or Technical Fees | 93 |

| 194K | TDS on Income in Respect of units of Mutual Fund | 97 |

| 194-LA | TDS on Payments of Compensation on Acquisition of certain Immovable Property | 99 |

| 194-LB | TDS on Income by way of Interest from Infrastructure Debt Fund | 102 |

| 194-LBA | TDS on Certain Income from Units of a Business Trust | 103 |

| 194-LBB | TDS on Income in Respect of Units of Investment Fund | 105 |

| 194-LBC | TDS on Income in Respect of Investment in Securitization Trust | 106 |

| 194-LC | TDS on Income by way of Interest from Indian Company or Business trust | 107 |

| 194-LD | TDS on Income by way of Interest on certain Bonds / Government Securities | 109 |

| 194M | TDS on payments of certain Sums by Individual & HUF | 111 |

| 194N | TDS on cash withdrawal from banks/post offices | 114 |

| 194O | TDS ON E-Commerce Operator | 119 |

| 195 | TDS on Non-Resident Payments | 122 |

| 195A | Income Payable “Net Of Tax” | 131 |

| 196B | TDS on long term capital gains (LTCG) from units referred to in section 115AB | 132 |

| 196C | TDS on Income from foreign currency bonds or GDRs | 133 |

| 196D | TDS on Income of foreign institutional investors from securities | 134 |

| 197 | Certificate For Deduction at Lower Rate | 135 |

| 197A | No Deduction to be Made In Certain Cases | 137 |

| 198 | Tax Deducted at Source shall be deemed to be income received | 143 |

| 199 | Credit For Tax Deducted | 144 |

| 200 (1) & (2) | Time Limit for Deposit of Tax Deducted at Source | 145 |

| 200 (3) | Forms And Time Limit For Submitting Quarterly Statement of Tax Deduction (TDS Returns) | 146 |

| 203 | TDS Certificate | 148 |

| 200A | Processing of statements of tax deducted at source | 150 |

| 201 | Consequences of Non-Compliance to TDS | 152 |

| 203A | Tax Deduction and Collection Account Number | 157 |

| 206AA | Mandatory Requirement of Furnishing PAN- TDS | 158 |

| 206C | Tax Collection at Source | 160 |

| 206CC | Mandatory Requirement of Furnishing PAN- TCS | 186 |

| Disallowance of Tax Deducted at Source | 188 |

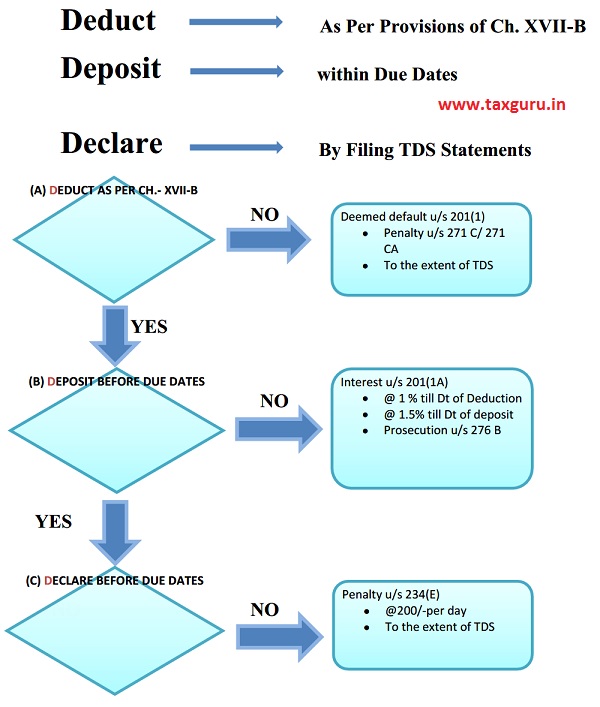

THREE DEE SYSTEM

(A) Changes in rate of Tax Deduction at Source (TDS)

[DEDUCT]

In order to provide more funds at the disposal of the taxpayers for dealing with the economic situation arising out of COVID-19 pandemic, the rates of Tax Deduction at Source (TDS) for the following non-salaried specified payments made to residents has been reduced by 25% for the period from 14th May, 2020 to 31st March, 2021. All sections other than Section 192 and 194N are covered under this:-

| S. No | Section of the Income-tax Act | Nature of Payment | Existing Rate of TDS | Reduced rate from 14/05/2020 to 31/03/2021 |

| 1 | 193 | Interest on Securities | 10% | 7.5% |

| 2 | 194 | Dividend | 10% | 7.5% |

| 3 | 194A | Interest other than interest on securities | 10% | 7.5% |

| 4 | 194C | Payment of Contractors and sub-contractors | 1% (individual/HUF)

2% (others) |

0.75% (individual/HUF)

1.5% (others) |

| 5 | 194D | Insurance Commission | 5% | 3.75% |

| 6 | 194DA | Payment in respect of life insurance policy | 5% | 3.75% |

| 7 | 194EE | Payments in respect of deposits under National Savings Scheme | 10% | 7.5% |

| 8 | 194F | Payments on account of re-purchase of Units by Mutual Funds or UTI | 20% | 15% |

| 9 | 194G | Commission, prize etc., on sale of lottery tickets | 5% | 3.75% |

| 10 | 194H | Commission or brokerage | 5% | 3.75% |

| 11 | 194-I(a) | Rent for plant and machinery | 2% | 1.5% |

| 12 | 194-I(b) | Rent for immovable property | 10% | 7.5% |

| 13 | 194-IA | Payment for acquisition of immovable property | 1% | 0.75% |

| 14 | 194-IB | Payment of rent by individual or HUF | 5% | 3.75% |

| 15 | 194-IC | Payment for Joint Development Agreements | 10% | 7.5% |

| 16 | 194J | Fee for Professional or Technical Services (FTS), Royalty, etc. | 2% (FTS, certain royalties, call centre)

10% (others) |

1.5% (FTS, certain royalties, call centre)

7.5% (others) |

| 17 | 194K | Payment of dividend by Mutual Funds | 10% | 7.5% |

| 18 | 194LA | Payment of Compensation on acquisition of immovable property | 10% | 7.5% |

| 19 | 194LBA(1) | Payment of income by Business trust | 10% | 7.5% |

| 20 | 194LBB(i) | Payment of income by Investment fund | 10% | 7.5% |

| 21 | 194LBC(1) | Income by securitisation trust | 25% (Individual/HUF)

30% (Others) |

18.75% (Individual/HUF)

22.5% (Others) |

| 22 | 194M | Payment to commission, brokerage etc. by Individual and HUF | 5% | 3.75% |

| 23 | 194-O | TDS on e-commerce participants | 1%

(w.e.f. 1.10.2020) |

0.75% |

(B) DATE TO DEPOSIT

[DEPOSIT]

| TAX DEDCUTED AT SOURCE (TDS) | TAX COLLECTED AT SOURCE (TCS) |

| 7th day of next month (30th April for TDS deducted in the month of March) | 7th day of next month (for TCS collected in the month of March – 7th April) |

(C) PAYMENT OF TAX, QUARTERLY STATEMENT AND FURNISHING TDS/TCS CERTIFICATE

[DECLARE]

| Quarter ending on | Due Date for Quarterly TDS Statement in Form no. 24Q/26Q/27Q | Due Date to issue TDS Certificate in Form no. 16A | Due Date for Quarterly TCS Statement in Form no. 27EQ | Due Date to Issue TCS Certificate in Form no. 27D |

| 30th June | 31St March,2021 | 15th August | 31St March,2021 | 15th April, 2021 |

| 30th September | 31st March,2021 | 15th November | 31St March,2021 | 15th April, 2021 |

| 31st December | 31st January, 2021 | 15th February | 15th January, 2021 | 30th January, 2021 |

| 31st March | 31st May, 2021 | 15th June (Due date for issuing Form 16 FY 20-21 is also 15th June) | 15th May, 2021 | 30th May, 2021 |

INTRODUCTION

TDS stands for ‘Tax Deducted at Source’. It was introduced to collect tax at the source from where an individual’s income is generated. The government uses TDS as a tool to collect tax in order to minimize tax evasion by taxing the income (partially or wholly) at the time it is generated rather than at a later date.

TDS is applicable on the various incomes such as salaries, interest received, commission received etc. TDS is not applicable to all incomes and persons for all transactions. Different rates of TDS have been prescribed by the Income Tax Act for different payments and different categories of recipients

TDS works on the concept that every person making specified type of payments to any person shall deduct tax at the rates prescribed in the Income Tax Act at source and deposit the same into the government’s account.

The person who is making the payment is responsible for deducting the tax and depositing the same with government. This person is known as ‘deductor‘. On the other hand, the person who receives the payment after the tax deduction is called ‘deductee‘.

How TDS works

The entity making a payment (which is subject to TDS) deducts a certain percentage of the amount paid, as tax and pays the balance to the recipient. The recipient also gets a certificate from the deductor stating the amount of TDS. The deductee can claim this TDS amount as tax paid by him (i.e. the deductee) for the financial year in which it is deducted.

The deductor is duty bound to deposit the TDS with the government. Once deposited this amount reflects in the Form 26AS of individual deductees on the TRACES website linked to the income tax department’s e-filing website.

Form 26AS is a statement which shows the amount of tax deducted and deposited in a person’s name/PAN. An individual can, therefore, view/check the TDS from incomes paid to him by viewing this Form 26AS. Each deductor is also duty bound to issue a TDS certificate certifying how much amount is deducted in the deductee’s name and deposited with the government.

TDS only applicable above a threshold level

One must remember that TDS on specified transactions is deducted only when the value of payment is above the specified threshold level. No TDS will be deducted if the value does not cross the specified level. Different threshold levels are specified by the Income Tax department for different payments such as salaries, interest received etc. For example, there will be no TDS on the total interest received on FD/FDs from a single bank if it is less than Rs 10,000 in a year from that bank.

Also, GST should be excluded while deducting TDS. [Circular No.23/2017 dated 19th July 2017]

Section 192 TDS on Salary

192. (1) Any person responsible for paying any income chargeable under the head “Salaries” shall, at the time of payment, deduct income-tax on the amount payable at the average rate of income-tax computed on the basis of the rates in force for the financial year in which the payment is made, on the estimated income of the assessee under this head for that financial year.

(1A) Without prejudice to the provisions contained in sub-section (1), the person responsible for paying any income in the nature of a perquisite which is not provided for by way of monetary payment, referred to in clause (2) of section 17, may pay, at his option, tax on the whole or part of such income without making any deduction therefrom at the time when such tax was otherwise deductible under the provisions of sub-section (1).

(1B) For the purpose of paying tax under sub-section (1A), tax shall be determined at the average of income-tax computed on the basis of the rates in force for the financial year, on the income chargeable under the head “Salaries” including the income referred to in sub-section (1A), and the tax so payable shall be construed as if it were, a tax deductible at source, from the income under the head “Salaries” as per the provisions of sub-section (1), and shall be subject to the provisions of this Chapter.

32[(1C) For the purposes of deducting or paying tax under sub-section (1) or sub-section (1A), as the case may be, a person, being an eligible start-up referred to in section 80-IAC, responsible for paying any income to the assessee being perquisite of the nature specified in clause (vi) of sub-section (2) of section 17 in any previous year relevant to the assessment year, beginning on or after the 1st day of April, 2021, shall deduct or pay, as the case may be, tax on such income within fourteen days—

(i) after the expiry of forty-eight months from the end of the relevant assessment year; or

(ii) from the date of the sale of such specified security or sweat equity share by the assessee; or

(iii) from the date of the assessee ceasing to be the employee of the person,

whichever is the earliest, on the basis of rates in force for the financial year in which the said specified security or sweat equity share is allotted or transferred.]

(2) Where, during the financial year, an assessee is employed simultaneously under more than one employer, or where he has held successively employment under more than one employer, he may furnish to the person responsible for making the payment referred to in sub-section (1) (being one of the said employers as the assessee may, having regard to the circumstances of his case, choose), such details of the income under the head “Salaries” due or received by him from the other employer or employers, the tax deducted at source therefrom and such other particulars, in such form and verified in such manner as may be prescribed, and thereupon the person responsible for making the payment referred to above shall take into account the details so furnished for the purposes of making the deduction under sub-section (1).

(2A) Where the assessee, being a Government servant or an employee in a company, co-operative society, local authority, university, institution, association or body is entitled to the relief under sub-section (1) of section 89, he may furnish to the person responsible for making the payment referred to in sub-section (1), such particulars, in such form and verified in such manner as may be prescribed, and thereupon the person responsible as aforesaid shall compute the relief on the basis of such particulars and take it into account in making the deduction under sub-section (1).

Explanation.—For the purposes of this sub-section, “University” means a University established or incorporated by or under a Central, State or Provincial Act, and includes an institution declared under section 3 of the University Grants Commission Act, 1956 (3 of 1956), to be a University for the purposes of that Act.

(2B) Where an assessee who receives any income chargeable under the head “Salaries” has, in addition, any income chargeable under any other head of income (not being a loss under any such head other than the loss under the head “Income from house property”) for the same financial year, he may send to the person responsible for making the payment referred to in sub-section (1) the particulars of—

(a) such other income and of any tax deducted thereon under any other provision of this Chapter;

(b) the loss, if any, under the head “Income from house property”,

in such form and verified in such manner as may be prescribed, and thereupon the person responsible as aforesaid shall take—

(i) such other income and tax, if any, deducted thereon; and

(ii) the loss, if any, under the head “Income from house property”,

also into account for the purposes of making the deduction under sub- section (1) :

Provided that this sub-section shall not in any case have the effect of reducing the tax deductible except where the loss under the head “Income from house property” has been taken into account, from income under the head “Salaries” below the amount that would be so deductible if the other income and the tax deducted thereon had not been taken into account.

(2C) A person responsible for paying any income chargeable under the head “Salaries” shall furnish to the person to whom such payment is made a statement giving correct and complete particulars of perquisites or profits in lieu of salary provided to him and the value thereof in such form and manner as may be prescribed.

(2D) The person responsible for making the payment referred to in sub-section (1) shall, for the purposes of estimating income of the assessee or computing tax deductible under sub-section (1), obtain from the assessee the evidence or proof or particulars of prescribed claims (including claim for set-off of loss) under the provisions of the Act in such form and manner as may be prescribed.

(3) The person responsible for making the payment referred to in sub-section (1) or sub-section (1A) or sub-section (2) or sub-section (2A) or sub-section (2B) may, at the time of making any deduction, increase or reduce the amount to be deducted under this section for the purpose of adjusting any excess or deficiency arising out of any previous deduction or failure to deduct during the financial year.

(4) The trustees of a recognised provident fund, or any person authorised by the regulations of the fund to make payment of accumulated balances due to employees, shall, in cases where sub-rule (1) of rule 9 of Part A of the Fourth Schedule applies, at the time an accumulated balance due to an employee is paid, make therefrom the deduction provided in rule 10 of Part A of the Fourth Schedule.

(5) Where any contribution made by an employer, including interest on such contributions, if any, in an approved superannuation fund is paid to the employee, tax on the amount so paid shall be deducted by the trustees of the fund to the extent provided in rule 6 of Part B of the Fourth Schedule.

(6) For the purposes of deduction of tax on salary payable in foreign currency, the value in rupees of such salary shall be calculated at the prescribed rate of exchange.

1) Who is responsible to deduct tax u/s 192?

All persons paying salary are responsible to deduct TDS on income chargeable under the head “Salary”. In other words none of the payer of Salary is excluded; Individual, HUF, Partnership firms, companies, cooperative societies, Trust and other artificial judicial persons have to deduct TDS on Salary.

2) Who is the payee?

Any employee having taxable income under the head “Salary” shall be treated as payee for TDS u/s 192. For application of Sec. 192, there must exist employer employee relationship between payer and payee.

For e.g

i. Director of company is not employee and as such no TDS u/s 192 on any amount paid to director

ii. Part-Time Directors of the company, visiting professors & visiting doctors are covered u/s194 J and not covered u/s 192. The whole-time directors are employees of the company and hence TDS is deductible u/s 192.

Case laws:

-

- PCIT(TDS) vs. National Health & Education Society [2019] 4112 ITR 404 (Bom):

Where there existed no relationship of employer and employee between assessee and Hospital Based Consultants (HBCs), provisions of section 192 would not be applicable

-

- CIT(TDS) vs. Asian Heart Institute and Research Centre (P.) Ltd. [2019] 104 taxmann.com 125 (Bom):

Where assessee trust, running a hospital, shared receipts from patients with consultant doctors in fixed ratio, TDS was to be deducted under section 194J as such payment was professional fees

3) Is TDS deducted on Salary Paid to Non-resident Employees?

Yes, TDS to be deducted by employers on payments made to non-resident employee u/s 192.

4) When to Deduct TDS under Section 192?

Liability to deduct tax at source shall arise at the time of actual payment of salary and not at the time of accrual. Thus, the employer is not required to deduct tax at source when salary has not been paid but merely credited to the account of the employee. Although, as per section 15 the salary is taxable in the hands of the employee either at the time of actual receipt or at the time of accrual whichever is earlier.

5) Threshold limit

No tax is required to be deducted at source unless the estimated salary exceeds the maximum amount not chargeable to tax. No TDS u/s.192 if tax payable (after taking rebate u/s.87A) by the employee is NIL.

6) Rate of TDS under Section 192

Under section 192 there is no specific TDS rate. TDS to be deducted is calculated according to the tax slabs and rates thereof applicable to the financial year for which the salary is paid. The requirement of deducting TDS u/s 192 shall be worked out, after considering all the exemptions, allowances, rebate and deductions which are available to the employee.

TDS u/s 192 has to be deducted at the average of income tax computed on the basis of rates in force during the financial year. The total tax to be deducted on the estimated income of the employee for the relevant financial year is divided by the number of months of his employment. The amount so arrived is the monthly deduction of tax at source.

However, if the employee does not have PAN No., TDS shall be deducted 20% without including Health & Education Cess, if the normal tax rate in this case is less than 20%.

7) Whether employer is also liable to deduct TDS on non-monetary perquisites?

Section 192 (1)(a) provides an option to employer to pay tax on behalf of employee on non-monetary perquisites, however it is not mandatory for the employer to pay so. For the purpose of paying tax by employer u/s 1(a) tax shall be determined at the average rate of income tax in force on the income chargeable under the head salaries including the value of non-monetary perquisites.

ILLUSTRATION:

Estimated Salary of an employee below 60 years of age is ₹8.00 lakh out of which ₹50,000/- is on account of non-monetary perquisites and the employer opts to pay the tax on such perquisites as per the provisions of income tax act. Total salary income chargeable to Tax is ₹8.00 lakhs. Employers are required to deduct perquisite tax for the A.Y. 2020-21 computed as follows:

| Income Chargeable under the head “Salaries” inclusive of all perquisites | ₹8,00,000.00 |

| Tax on Total Salary (including Health & Education Cess ) | ₹65,000 |

| Average Rate of Tax [(₹65000/₹800000) * 100] | 8.125% |

| Tax payable on ₹50,000/ = (8.125% of ₹50,000) | ₹4062.5 |

| Amount required to be deposited each month | ₹339(i.e.₹4062.5/12) |

The tax so paid by the employer shall be deemed to be TDS made from the salary of the employee. This TDS contributed by employer is exempt in the hands of employee.

8) Excess or shortfall of TDS during the financial year

- Any excess/deficiency arising out of previous deduction or failure to deduct during the financial year can be adjusted subsequently as per Section 192(3).

- Thus, where assessee did not deduct tax from salaries in each month, rather it deducted tax at end of financial year, interest u/s. 201(1A) could not belevied–CIT v. Enron Expat Services Inc.(Uttarakhand HC)(ITANo.78/2007)

- If TDS u/s.192 is not deducted in equal installments intentionally (not bonafide) and the deficiency is made good in last months, interest u/s. 201(1A) is liable to be levied

–Madhya Gujarat Vij Co. Ltd. v. ITO (Ahmedabad Trib.) (ITA No.420/Ahd/2011)

9) RELIEF WHEN SALARY IS PAID IN ARREARS OR ADVANCE –SECTION 89(1)

- Advance Salary and Arrears of salary-Taxable in the year of receipt.

- However, eligible to claim relief u/s. 89(1).

- Relief to be computed as per Rule 21A.

- As per Sec.192 (2A), Form No.10 E is required to be submitted to the employer. Form No.10 E is also required to be submitted electronically on the e-filing portal.

- Section 89(1) and Section 10(10C):

If any amount received on voluntary retirement or termination of service as per VRS or in case of public sector company, a scheme of voluntary separation is claimed as exempt u/s. 10(10C), relief u/s. 89(1) cannot be claimed.

10) Other relevant points related to section 192

a. Every person responsible for paying salary income is first required to estimate the income chargeable under the head “Salaries”. The value of the perquisites provided by the employers to their employees shall be determined under rule 3 and shall be taken in to account while estimating income under the head “Salaries”.

b. Further, any income falling under section 10 (income which do not form part of total income) shall not be included in computing the income from salaries for the purpose of section 192 of the Act.

c. The person responsible for making payments shall also take into consideration amount deductible under section 80C, 80CCC, 80CCD, 80CCG, 80D, 80DD, 80DDB, 80E, 80EE, 80G, 80GG, 80GGA, 80TTA and 80U.

d. Section 192(2A) provides that deduction of tax at source is to be made after allowing relief u/s 89(1) and after considering the tax on perquisites agreed to be borne by employer.

e. Section 192(2D) further casts responsibility on the person responsible for paying any income chargeable under the head ‘Salaries’ to obtain from the assessee (employee), the evidence or proof or particulars of prescribed claims (including claim for set-off of loss) under the provisions of the Act in the prescribed form and manner for the purposes of –

i. estimating income of the assessee (employee); or

ii. computing tax deductible under section 192(1).

f. Section 192 (2) provides that where an assessee is employed under more than one employer, then the assessee (employee) may choose the employer for deduction of tax at source. Thereupon, that employer shall deduct tax at source from the aggregate salary of an employee. For this purpose, employee is required to furnish details of salary due or received by him from other employer(s) in Form No. 12B to one of the employers (as chosen by him).

g. As per the provision of section 192(3), the person responsible for paying the salary may, at the time of deducting tax at source, increase or reduce the amount to be deducted for the purpose of adjusting any excess or deficiency arising out of previous deduction or non-deduction.

> The employee MAY provide to the employer, particulars of:

-

-

- Other Income, including tax deducted thereon

- Loss, only if it is under the head ‘Income from house property’

-

> Income from House Property-

-

- Any other rental income may be informed to the employer.

- Deemed let out property- From A.Y. 2020-21, if assessee owns more than 2 Self occupied houses, such other house or houses shall be deemed to have been let out and its annual value shall be computed in accordance with Section 23(1). [Prior to A.Y. 2020-21, if the assessee owned 2 houses, the other house had to be deemed to have been let out]

- Assessee can claim deduction of interest paid on borrowed capital u/s 24(b) of the Act.

- Loss only under the head ‘Income from House Property’ can be informed to the employer. House Property loss can be set-off maximum upto Rs. 2 Lakhs. [Section 71(3A)]

- Particulars of ‘Other Income’ to be informed to the employer in simple statement duly verified by the employee- Rule 26 B

h. In case if the employee furnishes to his employer, the details regarding his other incomes, investments, eligible deductions etc., then for the purpose of TDS u/s 192, the employer shall be bound to consider such information.

11) Tax to be deducted from other incomes of the employee

- The employee may declare his other incomes to the employer for the purpose of tax deduction at source under this section.

- If he wants to declare, then particulars of

i. other income (not being a loss) and tax deducted thereon

ii. the loss under the head “Income from house property”

shall be submitted to the employer in a prescribed form and verified in a prescribed manner.

- On receipt of the same, employer shall deduct tax under section 192 after taking into account the other income.

- However, this shall not have the effect of reducing the tax deductible (except where the loss under the head “Income from house property” has been taken into account) from salary income below the amount that would be so deductible if the other income and tax deducted thereon had not been taken into account.

12) Whether benefit of lower deduction or no deduction of TDS is available u/s 192?

Yes. However assessee to whom the salary is payable may make an application in Form No. 13 to the Assessing Officer and if the Assessing Officer is satisfied that the total income of the recipient justifies the deduction of income tax at any lower rate or no deduction of income-tax, he may be given such certificate as may be appropriate.

W.E.F. 1-4-2010, as per section 206AA(4), no certificate under section 197 shall be granted unless the application made in Form No.13 under that section contains the Permanent Account Number of the applicant.

13) Whether provisions of Section 192 shall also apply to salary paid by non-resident employer to a non-resident employee for services rendered in India?

Yes, Provisions of Sec. 192 shall apply if the salary was paid for services rendered in India even though the employers as well as employee were non-resident and the payment is made outside India.

14) Evidence/Proof Of Claims To Be Submitted By The Employee –Section 192(2D)

The person responsible for making any payment of income chargeable under the head ‘Salaries’ shall obtain from the assessee the evidence or proof of particulars of prescribed claims made by him in Form No. 12BB:

a) Exemption of House Rent Allowance

– Amount of rent paid to the landlord

– Name and address of the landlord

– PAN of the landlord if aggregate rent paid during the previous year exceeds Rs. 1 lakh

– Rent receipts/ rent agreement from the landlord

b) Leave Travel Concession

– Evidence of expenditure is required to be furnished to the employer as per Rule 26C

– Leave Travel Concession cannot be claimed for foreign travel- Syndicate Bank Vs. ACIT (TDS) 164 ITD 319 (Bengaluru Trib.)

– However, if the assessee has, under bonafide belief that foreign travel costs can be claimed as exempt u/s 10(5), not deducted TDS, penalty u/s 271C could not be levied and the same was treated as reasonable cause for the purpose of Section 273 B- State Bank of India Vs. ACIT (TDS) [2019] 063 ITD 440 (Jaipur Trib.)

c) Deduction of Interest u/s 24 (b)

– Interest on borrowing can be set off against Salary income. (House Property) loss to the extent of Rs. 2 Lakhs)

– Details to be submitted:

– Interest payable/ paid to the lender

– Name, address and PAN/Aadhaar number of the lender.

– Interest Certificate from the lender

d) Donations under sec. 80G – The donations are made under sec 80G (other than to a notified charitable institute) then the employer should allow that donation while calculating tax deductible. When donation is made to a notified public then the employer should not allow that donation while calculating tax deductible.

e) Other deductions- Deductions under sections 80C, 80CCC, 80CCD, 80CCG, 80D, 80DD, 80DDB, 80E, 80EE, 80GG, 80GGA, 80TTA, 80U.

15) TDS on Salary to Partners

Salary or remuneration paid to partners is not taxable in hands of partners as Salary but it is considered as income from business. No employer employee relationship exists between partner and partnership firm.

Explanation 2 of section 15 says that “Any salary, bonus, commission or remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as “salary”.

Therefore no TDS is to be deducted on salary paid to the partners

Some person argues that this provision only applies on salary paid to active partners Salary paid to inactive partners is not allowed as deduction to the partnership firm under section 40(b) but still it’s a business income for the partner. The above explanation doesn’t differentiate between active or inactive partner and thus salary paid to any partner is not liable to TDS.

16) TDS on Pension and Family Pension

There is difference between “Pension” and “Family Pension” for the purposes of Income Tax Act, 1961. The Income Tax treatment for “Pension” and “Family Pension” is different.

It is pertinent to point out that “Pension” received from a former employer is taxable under the head “Salary” since Section 17 of Income Tax Act specifically lays down in clause (ii) of sub-section (1) that “any annuity or pension” is included in “salary”. Therefore, “Pension” is taxed in the same way as “Salary” is taxed.

On the other hand, “Family Pension” is taxed under Section 56 as “Income from Other Sources”.

Now, Section 192 of Income Tax Act makes any income chargeable under the head “Salary” subject to Tax Deduction at Source (TDS). Since pension is also considered as Salary, therefore TDS is deducted on pension also, wherever applicable as per the prevailing rates.

On the other hand, Family Pension is not “Salary” but an “Income from Other Sources”. Therefore, TDS cannot be deducted on Family Pension under Section 192. Moreover, there is no other Section in the Income Tax Act which makes it mandatory to deduct TDS on family pension. Therefore, there is no TDS deduction on Family Pension.

In case of pensioners of a Govt. or other departments, receiving pension through nationalized banks, TDS has to be deducted by the bank u/s 192.

Further, the Banks are bound to issue Form No. 16 to such pensioners as per Section 203.

Form No. 16 cannot be denied merely because there is no Employer-employee relationship between the bank and such pensioner. [CBDT Circular No. 761 dated 13.01.1998]

17) Salary received by MP, MLA, Ministers

- Remuneration received by a Member of Parliament, Member of Legislative Assembly is not chargeable as Income under the head ‘Salary’. As there is no employer- employee relationship. It is chargeable under the head ‘Income from other sources’ – CIT Vs. Shiv Charan Mathur (Raj. HC) (ITA No. 96 of 2006) (Also refer CBDT Letter F. No. 40/29/67-IT(A-1) DATED 22.05.1967

- Salary received by Chief Minister or a minister is taxable under the head ‘Salary’ – Lalu Prasad Vs. CIT ( Patna ) (2009) 316 ITR 186

- Daily allowance, Constituency allowance, etc. received by MP/MLA is exempt u/s 10(17).

18) TDS under section 192 and Section 115BAC

Tax rates u/s 115 BAC inserted vide Finance Act, 2020

| Total Income | Rate of Tax |

| Upto Rs. 2,50,000 | Nil |

| From Rs. 2,50,001 to Rs. 5,00,000 | 5% |

| From Rs. 5,00,001 to Rs. 7,50,000 | 10% |

| From Rs. 7,50,001 to Rs. 10,00,000 | 15% |

| From Rs. 10,00,001 to Rs. 12,50,000 | 20% |

| From Rs. 12,50,001 to Rs. 15,00,000 | 25% |

| Above Rs. 15,00,000 | 30% |

When to exercise option u/s 115 BAC

> A person can opt under Section 115 BAC

-

- If having income from business or profession

- Option to be exercised on or before due date u/s 139(1)

- Option once exercised shall apply to subsequent years

- Can only be withdrawn once and thereafter, the assessee shall not be eligible to opt u/s 115 BAC.

> If NOT having income from business or profession

-

- Option to be exercised at the time of furnishing return of income

- Assessee will have option each assessment year to choose from either the normal provisions or Section 115 BAC.

19) TDS U/S. 192 IN LIGHT OF THE SECTION 115 BAC?

- Intimation to Employer-The employee, whether having any income under head ‘profits and gains from business or profession’ or not, has to intimate the employer about the intention to opt for concessional rate of taxation u/s.115BAC of the Act. The employer will deduct TDS accordingly.

- If no such intimation is made, TDS will be deducted without considering Section115BAC.

- Intimations made to the employer cannot be modified during the year.

- However, this intimation given to employer is not binding and the employee can choose different option while filing return of income.

- In respect of employee having income under PGBP head– intimation for subsequent years should not deviate from previous intimation, except when the employee opts out from Section115BAC.

- CBDT Circular No.C1 of 2020 dated April 13, 2020

Section 192A TDS on Payment of Accumulated Balance Due to an Employee

192A. Notwithstanding anything contained in this Act, the trustees of the Employees’ Provident Fund Scheme, 1952, framed under section 5 of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 (19 of 1952) or any person authorised under the scheme to make payment of accumulated balance due to employees, shall, in a case where the accumulated balance due to an employee participating in a recognised provident fund is includible in his total income owing to the provisions of rule 8 of Part A of the Fourth Schedule not being applicable, at the time of payment of the accumulated balance due to the employee, deduct income-tax thereon at the rate of ten per cent :

Provided that no deduction under this section shall be made where the amount of such payment or, as the case may be, the aggregate amount of such payment to the payee is less than fifty thousand rupees:

Provided further that any person entitled to receive any amount on which tax is deductible under this section shall furnish his Permanent Account Number to the person responsible for deducting such tax, failing which tax shall be deducted at the maximum marginal rate.

1) Who is responsible to deduct tax u/s 192A?

Tax is to be deducted by the trustees of Employees’ Provident Fund Scheme, 1952 or any other person authorized under the scheme to make payment of accumulated sum to employees.

2) When to Deduct TDS under Section 192A?

Tax is deductible at the time of payment.

3) Which amount is subject to tax deduction?

a. Tax is deductible from accumulated lump sum payment when the employee has not rendered continuous service of 5 years (other than the cases of termination due to ill health, contraction or discontinuance of business, cessation of employment etc.). RPF is exempt in the hands of the employee if the employee has resigned before completion of 5 years but he joins another employer who maintains recognized provident fund, and provident fund money with the current employer is transferred to the new employer.

b. Out of the lump sum payment, tax deduction shall be made on that portion of payment which is includible in the total income of the employee. Thus, tax deduction shall be made as under:-

| Component of lump sum payment | Is this component taxable in the hands of employee not completing continuous 5 years of service? | Is it subject to TDS if other conditions of section 192A are satisfied? |

| Employer’s Contribution | Taxable under head “Salary” | Subject to TDS |

| Interest on Employer’s Contribution | Taxable under head “Salary” | Subject to TDS |

| Employee’s Contribution | Not Taxable | No TDS required |

| Interest on Employee’s

Contribution |

Taxable under head “Other Sources” | Subject to TDS |

4) Threshold limit

Tax is not deductible where aggregate amount of taxable component of lump sum payment is less than ₹50,000.

5) Rate of TDS under Section 192A

Tax is deductible at the rate of 10 per cent of taxable component of lump sum payment. However, if employee fails to furnish PAN, then tax shall be deducted at maximum marginal rate.

6) No deduction of tax at source

No deduction of tax is to be made if the recipient of income furnishes a declaration in writing in duplicate in prescribed form [Form No. 15G/15H].

7) Further,if post retirement,if any interest is paid on the accumulated balance not withdrawn,tax is required to be deducted as per section 194A,since there is no employer –employee relationship.

Section 193 TDS from Interest on Securities

193. The person responsible for paying to a resident any income by way of interest on securities shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax at the rates in force on the amount of the interest payable :

Provided that no tax shall be deducted from—

(i) any interest payable on 4 per cent National Defence Bonds, 1972, where the bonds are held by an individual, not being a non-resident; or

(ia) any interest payable to an individual on 4 per cent National Defence Loan, 1968, or 4 per cent National Defence Loan, 1972; or

(ib) any interest payable on National Development Bonds; or

(ii) [***]

(iia) any interest payable on 7-Year National Savings Certificates (IV Issue); or

(iib) any interest payable on such debentures, issued by any institution or authority, or any public sector company, or any co-operative society (including a co-operative land mortgage bank or a co-operative land development bank), as the Central Government may, by notification in the Official Gazette, specify in this behalf;

(iii) any interest payable on 6 per cent Gold Bonds, 1977, or 7 per cent Gold Bonds, 1980, where the Bonds are held by an individual not being a non-resident, and the holder thereof makes a declaration in writing before the person responsible for paying the interest that the total nominal value of the 6 per cent Gold Bonds, 1977, or, as the case may be, the 7 per cent Gold Bonds, 1980, held by him (including such bonds, if any, held on his behalf by any other person) did not in either case exceed ten thousand rupees at any time during the period to which the interest relates;

(iiia) [***]

(iv) any interest payable on any security of the Central Government or a State Government:

Provided that nothing contained in this clause shall apply to the interest exceeding rupees ten thousand payable on 8% Savings (Taxable) Bonds, 2003 or 7.75% Savings (Taxable) Bonds, 2018 during the financial year;

(v) any interest payable to an individual or a Hindu undivided family, who is resident in India, on any debenture issued by a company in which the public are substantially interested, if—

(a) the amount of interest or, as the case may be, the aggregate amount of such interest paid or likely to be paid on such debenture during the financial year by the company to such individual or Hindu undivided family does not exceed five thousand rupees; and

(b) such interest is paid by the company by an account payee cheque;

(vi) any interest payable to the Life Insurance Corporation of India established under the Life Insurance Corporation Act, 1956 (31 of 1956), in respect of any securities owned by it or in which it has full beneficial interest; or

(vii) any interest payable to the General Insurance Corporation of India (hereafter in this clause referred to as the Corporation) or to any of the four companies (hereafter in this clause referred to as such company), formed by virtue of the schemes framed under sub-section (1) of section 16 of the General Insurance Business (Nationalisation) Act, 1972 (57 of 1972), in respect of any securities owned by the Corporation or such company or in which the Corporation or such company has full beneficial interest; or

(viii) any interest payable to any other insurer in respect of any securities owned by it or in which it has full beneficial interest;

(ix) any interest payable on any security issued by a company, where such security is in dematerialised form and is listed on a recognised stock exchange in India in accordance with the Securities Contracts (Regulation) Act, 1956 (42 of 1956) and the rules made thereunder.

Explanation—For the purposes of this section, where any income by way of interest on securities is credited to any account, whether called “Interest payable account” or “Suspense account” or by any other name, in the books of account of the person liable to pay such income, such crediting shall be deemed to be credit of such income to the account of the payee and the provisions of this section shall apply accordingly.

Explanation 2.—[Omitted by the Finance Act, 1992, w.e.f. 1-6-1992.]

1) Who is responsible to deduct tax u/s 193?

Any person responsible for paying any interest on securities to a resident is required to deduct tax at source.

2) When to Deduct TDS under Section 193?

Tax shall be deducted under this section, either at the time of credit to the account of the payee or at the time of payment thereof, whichever is earlier.

For this purpose, credit to “Interest payable account” or “Suspense account” or any other name shall be deemed to be a credit of such income to the account of the payee.

For this purpose, “payment” can be in cash or by issue of a cheque or draft or by any other mode.

3) Meaning of interest on securities

Section 2(28B) defines interest on securities. It means:

1. interest on any security of Central Government or State Government

2. interest on debentures or

3. interest on other securities for money issued by or on behalf of a local authority or a company or a corporation established by a Central, State or Provincial Act.

4) Rate of TDS under Section 193

As per section 193 read with Part II of First Schedule of Finance Act, tax is to be deducted @ 10% (7.5% w.e.f. 14.05.2020 to 31.03.2021) from the amount of interest.

a) No surcharge, plus Health & Education Cess shall be added to the above rates. Hence, tax will be deducted at source at the basic rate.

b) As per section 206AA(1), if the permanent account number is not provided by the deductee, the tax shall be deducted at the higher of the following rates, namely:—

i. at the rates specified in the relevant provisions of the Act

ii. at the rate or rates in force

iii. at the rate of 20%.

c) Further, as per section 206AA(4), no certificate under section 197 for deduction of tax at Nil rate or lower rate shall be granted unless the application made under that section contains the Permanent Account Number of the applicant.

d) Similarly, declaration under 15G/15H shall not be valid if it does not contain the permanent account number of the declarant. In case any declaration becomes invalid, the deductor shall deduct the tax @ 20%.

5) When No Tax shall be deducted U/s 193?

In the following cases tax is not to be deducted under section 193:

A. Interest payable to insurance companies, etc.:

Any interest payable to:—

i. Life Insurance Corporation of India;

ii. General Insurance Corporation of India or any of four companies formed under it;

iii. Any other insurer, in respect of any securities owned by them, or in which they have full beneficial interest.

B. Interest paid or credited by widely held company not exceeding ₹ 5,000:

No tax is to be deducted at source if the following conditions are satisfied:

i. if debentures are issued by a widely held company;

ii. such debentures may or may not be listed on a stock exchange in India;

iii. interest is paid/payable to an individual or HUF who is resident in India; and

iv. interest is paid by account payee cheque; and

v. the amount or the aggregate of the amounts of such interest paid or payable during the financial year does not exceed ₹ 5,000.

C. Any interest payable on any security issued by a company, where such security is in dematerialized form and is listed on a recognized stock exchange in India in accordance with the Securities Contracts (Regulation) Act, 1956 and the rules made thereunder.

D. Interest paid or credited on 8% saving (Taxable) Bonds 2003 issued by the Central Government provided the interest on such bonds does not exceed ₹ 10,000.

E. Where a self-declaration under Form No. 15G/15H is furnished by a particular person [Section 197A (1A), (1B) and (1C)]:

A person, other than a company or firm may furnish a declaration in writing in duplicate in new Form No. 15G to the payer to the effect that there is no tax payable on his Total Income. In this case, the payer shall not deduct any tax at source.

F. Any payment made to New Pension System Trust [Section 197A (1E)]:

No deduction of tax shall be made from any payment to any person for, or on behalf of, the New Pension System Trust referred to in section 10(44).

G. No deduction of tax from specified payment to notified institutions, association or body, etc. [Section 197A (1F)]:

No deduction of tax shall be made from such specified payment to such institution, association or body or class of institutions, associations or bodies as may be notified by the Central Government in the Official Gazette, in this behalf. No tax shall be deducted at source from the payments of the nature specified under section 10(23DA) received by any securitization trust.

H. Certain entities required to file return under section 139(4A) or 139(4C) [Rule 28AB]:

As per rule 28AB certain entities who are required to file their return of income under section 139(4A) or 139(4C) may apply under Form No. 13 for no deduction of tax at source provided certain conditions are satisfied.

I. Certain entities whose income is unconditionally exempt under section 10:

In case of certain entities whose income is unconditionally exempt under section 10 and who are statutorily not required to file return under section 139 there will be no requirement for TDS since their income is in any way exempt.

Section 194 TDS on payment of dividend

194. The principal officer of an Indian company or a company which has made the prescribed arrangements for the declaration and payment of dividends (including dividends on preference shares) within India, shall, before making any payment 33[by any mode]in respect of any dividend or before making any distribution or payment to a shareholder, who is resident in India, of any dividend within the meaning of sub-clause (a) or sub-clause (b) or sub-clause (c) or sub-clause (d) or sub-clause (e) of clause (22) of section 2, deduct from the amount of such dividend, income-tax 34[at the rate of ten per cent] :

Provided that no such deduction shall be made in the case of a shareholder, being an individual, if—

(a) the dividend is paid by the company by 35[any mode other than cash]; and

(b) the amount of such dividend or, as the case may be, the aggregate of the amounts of such dividend distributed or paid or likely to be distributed or paid during the financial year by the company to the shareholder, does not exceed 36[five thousand] rupees:

Provided further that the provisions of this section shall not apply to such income credited or paid to—

(a) the Life Insurance Corporation of India established under the Life Insurance Corporation Act, 1956 (31 of 1956), in respect of any shares owned by it or in which it has full beneficial interest;

(b) the General Insurance Corporation of India (hereafter in this proviso referred to as the Corporation) or to any of the four companies (hereafter in this proviso referred to as such company), formed by virtue of the schemes framed under sub-section (1) of section 16 of the General Insurance Business (Nationalisation) Act, 1972 (57 of 1972), in respect of any shares owned by the Corporation or such company or in which the Corporation or such company has full beneficial interest;

(c) any other insurer in respect of any shares owned by it or in which it has full beneficial interest.

37[***]

1) Who is responsible to deduct tax u/s 194?

The principal officer of an Indian company or a company which has made the prescribed arrangements for the declaration and payment of any dividend (including dividends on preference shares) to a shareholder, who is resident in India, is required to deduct tax at source.

2) What is threshold limit u/s 194?

No deduction upto Rs. 5000, if dividend is paid by any mode, other than cash.

3) When to Deduct TDS under Section 194?

Such tax shall be deducted before making payment of dividend.

4) Rate of TDS under Section 194

Tax is to be deducted at the rate of 10% (7.5% w.e.f. 14.05.2020 to 31.03.2021). If the recipient of income doesn’t furnish his PAN to deductor then TDS is to be deducted at the rate of 20%.

5) Other Points-

-

- Only Individual Shareholder can furnish Form No. 15G or 15H, as the case maybe.

- No deduction on dividend paid to LIC, GIC or any other connected insurer.

Summary

| Particular | Rate of TDS | Remarks |

| Resident Shareholders |

|

|

| Non Resident Shareholders (Other than FPI) | 20% plus applicable surcharge and cess or rates as per DTAA whichever is beneficial |

|

| FPI | 20% plus applicable surcharge and cess | |

| Compliance Requirements |

|

Section 194A TDS on Interest (other than Interest on Securities)

194A. (1) Any person, not being an individual or a Hindu undivided family, who is responsible for paying to a resident any income by way of interest other than income by way of interest on securities, shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force :

Provided that an individual or a Hindu undivided family, whose total sales, gross receipts or turnover from the business or profession carried on by him exceed 38[one crore rupees in case of business or fifty lakh rupees in case of profession] during the financial year immediately preceding the financial year in which such interest is credited or paid, shall be liable to deduct income-tax under this section.

Explanation.—For the purposes of this section, where any income by way of interest as aforesaid is credited to any account, whether called “Interest payable account” or “Suspense account” or by any other name, in the books of account of the person liable to pay such income, such crediting shall be deemed to be credit of such income to the account of the payee and the provisions of this section shall apply accordingly.

(2) [Omitted by the Finance Act, 1992, w.e.f. 1-6-1992.]

(3) The provisions of sub-section (1) shall not apply—

(i) where the amount of such income or, as the case may be, the aggregate of the amounts of such income credited or paid or likely to be credited or paid during the financial year by the person referred to in sub-section (1) to the account of, or to, the payee, does not exceed—

(a) 39[forty] thousand rupees, where the payer is a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution, referred to in section 51 of that Act);

(b) 40[forty] thousand rupees, where the payer is a co-operative society engaged in carrying on the business of banking;

(c) 40[forty] thousand rupees, on any deposit with post office under any scheme framed by the Central Government and notified by it in this behalf; and

(d) five thousand rupees in any other case:

Provided that in respect of the income credited or paid in respect of—

(a) time deposits with a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act); or

(b) time deposits with a co-operative society engaged in carrying on the business of banking;

(c) deposits with a public company which is formed and registered in India with the main object of carrying on the business of providing long-term finance for construction or purchase of houses in India for residential purposes and which is eligible for deduction under clause (viii) of sub-section (1) of section 36 ;

the aforesaid amount shall be computed with reference to the income credited or paid by a branch of the banking company or the co-operative society or the public company, as the case may be :

Provided further that the amount referred to in the first proviso shall be computed with reference to the income credited or paid by the banking company or the co-operative society or the public company, as the case may be, where such banking company or the co-operative society or the public company has adopted core banking solutions:

Provided also that in case of payee being a senior citizen, the provisions of sub-clause (a), sub-clause (b), and sub-clause (c) shall have effect as if for the words “41[forty] thousand rupees”, the words “fifty thousand rupees” had been substituted.

Explanation.—42[***]

(ii) [***]

(iii) to such income credited or paid to—

(a) any banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies, or any co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank), or

(b) any financial corporation established by or under a Central, State or Provincial Act, or

(c) the Life Insurance Corporation of India established under the Life Insurance Corporation Act, 1956 (31 of 1956), or

(d) the Unit Trust of India established under the Unit Trust of India Act, 1963 (52 of 1963), or

(e) any company or co-operative society carrying on the business of insurance, or

(f) such other institution, association or body or class of institutions, associations or bodies which the Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette:

43[Provided that no notification under this sub-clause shall be issued on or after the 1st day of April, 2020;]

(iv) to such income credited or paid by a firm to a partner of the firm;

(v) to such income credited or paid by a co-operative society (other than a co-operative bank) to a member thereof or to such income credited or paid by a co-operative society to any other co-operative society;

Explanation.—For the purposes of this clause, “co-operative bank” shall have the same meaning as assigned to it in Part V of the Banking Regulation Act, 1949 (10 of 1949);

(vi) to such income credited or paid in respect of deposits under any scheme framed by the Central Government and notified by it in this behalf in the Official Gazette;

(vii) to such income credited or paid in respect of deposits (other than time deposits made on or after the 1st day of July, 1995) with a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(viia) to such income credited or paid in respect of,—

(a) deposits with a primary agricultural credit society or a primary credit society or a co-operative land mortgage bank or a co-operative land development bank;

(b) deposits (other than time deposits made on or after the 1st day of July, 1995) with a co-operative society, other than a co-operative society or bank referred to in sub-clause

(a), engaged in carrying on the business of banking;

(viii) to such income credited or paid by the Central Government under any provision of this Act or the Indian Income-tax Act, 1922 (11 of 1922), or the Estate Duty Act, 1953 (34 of 1953), or the Wealth-tax Act, 1957 (27 of 1957), or the Gift-tax Act, 1958 (18 of 1958), or the Super Profits Tax Act, 1963 (14 of 1963), or the Companies (Profits) Surtax Act, 1964 (7 of 1964), or the Interest-tax Act, 1974 (45 of 1974);

(ix) to such income credited by way of interest on the compensation amount awarded by the Motor Accidents Claims Tribunal;

(ixa) to such income paid by way of interest on the compensation amount awarded by the Motor Accidents Claims Tribunal where the amount of such income or, as the case may be, the aggregate of the amounts of such income paid during the financial year does not exceed fifty thousand rupees;

(x) to such income which is paid or payable by an infrastructure capital company or infrastructure capital fund or a public sector company or scheduled bank in relation to a zero coupon bond issued on or after the 1st day of June, 2005 by such company or fund or public sector company or scheduled bank;

(xi) to any income by way of interest referred to in clause (23FC) of section 10:

44[Provided that a co-operative society referred to in clause (v) or clause (viia) shall be liable to deduct income-tax in accordance with the provisions of sub-section (1), if—

(a) the total sales, gross receipts or turnover of the co-operative society exceeds fifty crore rupees during the financial year immediately preceding the financial year in which the interest referred to in sub-section (1) is credited or paid; and

(b) the amount of interest, or the aggregate of the amounts of such interest, credited or paid, or is likely to be credited or paid, during the financial year is more than fifty thousand rupees in case of payee being a senior citizen and forty thousand rupees in any other case.]

Explanation 1.—For the purposes of clauses (i), (vii) and (viia), “time deposits” means deposits (including recurring deposits) repayable on the expiry of fixed periods.

45[Explanation 2.—For the purposes of this sub-section, “senior citizen” means an individual resident in India who is of the age of sixty years or more at any time during the relevant previous year.]

(4) The person responsible for making the payment referred to in sub-section (1) may, at the time of making any deduction, increase or reduce the amount to be deducted under this section for the purpose of adjusting any excess or deficiency arising out of any previous deduction or failure to deduct during the financial year.]

46[(5) The Central Government may, by notification in the Official Gazette, provide that the deduction of tax shall not be made or shall be made at such lower rate, from such payment to such person or class of persons, as may be specified in the said notification.]

Explanation.—[Omitted by the Finance Act, 1992, w.e.f. 1-6-1992.]

1) Who is responsible for tax deduction (payer)?

The person (other than an individual or a Hindu Undivided Family) who is responsible for paying to a resident any income by way of interests other than ‘interest on securities’ is required to deduct tax thereon at the rates in force.

An individual or a HUF is liable to deduct TDS under section 194A, if total sales, gross receipts or turnover exceed one crore rupees in case of business or fifty lakh rupees in case of profession during the financial year immediately preceding the financial year in which such interest is credited or paid.

LIABILITY TO DEDUCT TAX AT SOURCE

BY INDIVIDUAL AND HUF

-

- Liability to deduct tax at source under section 194A, 194C, 194H, 194I and 194J was first introduced by the Finance Act, 2002 by inserting various proviso to the respective sections.

Proviso to section 194A(1), Proviso to Section 194C(1), Second Proviso to 194H(1), Second Proviso to Section 194I(1), Second Proviso to 194J(1) were inserted by Finance Act, 2002 w.e.f. 01-06-2002

“Provided that an individual or a Hindu undivided family, whose total sales, gross receipts or turnover from the business or profession carried on by him exceed the monetary limits specified under section 44AB (a)/(b) during the financial year immediately preceding the financial year in which such sum is credited or paid, shall be liable to deduct income-tax under this section.”

-

- Finance Act, 2020 amended all the above sections w.e.f. 01-04-2020, and after amendment, above proviso reads as under:

Provided that an individual or a Hindu undivided family, whose total sales, gross receipts or turnover from the business or profession carried on by him exceed the one crore rupees in case of business or fifty lakh rupees in case of profession [Substituted by FA, 2020 w.e.f. 01.04.2020] during the financial year immediately preceding the financial year in which such sum is credited or paid, shall be liable to deduct income-tax under this section.

-

- Impact of Amendment

> The effect of above amendment is that individual or Hindu undivided family are required to deduct tax at source under section 194A, 194C, 194H, 194I and 194J if total sales, gross receipts or turnover exceed

(A) one crore rupees in case of business or

(B) fifty lakh rupees in case of profession

during the financial year immediately preceding the financial year in such sum is credited or paid.

> As a result, the individual or HUF carrying on business and whose total sales, gross receipts or turnover exceeds Rs. 1 crore but does not exceed Rs. 2 crore in preceding financial year and opted for section 44AD of the Act are now liable to deduct tax at source under section 194A, 194C, 194H, 194I and 194J w.e.f. 01-04-2020.

> Similarly, the individual or HUF engaged in plying, hiring and leasing of goods carriages and whose total sales, gross receipts or turnover exceeds Rs. 1 crore in preceding financial year and opted for section 44AE of the Act are now liable to deduct tax at source under section 194A, 194C, 194H, 194I and 194J w.e.f. 01-04-2020.

ILLUSTRATION–

Mr. A, proprietor of AB enterprises made turnover of ₹ 150 lakhs during previous year 2018-19, his turnover for the year ended 31-03-2020 was ₹ 85 lakhs. Decide whether he is liable to deduct tax at source under section 194A in PY 2019-20?

Since Mr. A’s turnover exceeds ₹ 100 lakhs in the immediately preceding financial year i.e. FY 2018-19, he is liable to deduct tax at source under section 194A in the previous year 2019-20, irrespective of his turnover being less than ₹ 100 lakhs in the Financial year 2019-20. He will not be required to deduct tax for the FY 2020-21 as his turnover for the FY 2019-20 is below ₹ 100 Lakhs.

Therefore if any partnership firm, LLP, Company, AOP, society pays interest exceeding the threshold limit, it is required to deduct TDS.

2) Who is the recipient?

A resident person

3) What is the nature of payment covered?

Interest other than interest on securities

4) When is tax to be deducted?

At the time of credit or payment, whichever is earlier.

5) What is the rate of tax deduction?

i) 10% (7.5% w.e.f. 14.05.2020 to 31.03.2021)

ii) 20% (if no PAN is furnished)

No surcharge, plus Health & Education Cess shall be added to the above rates. Hence, tax will be deducted at source at the basic rate.

6) When TDS on Interest (other than Interest on Securities) under section 194A not deductible?

TDS under section 194A is not deductible where the aggregate amount of interest credited/paid (or likely to be credited/paid) during the FY does not exceed the amount given below:

| Payer | Threshold limit (₹) (w.e.f. 01.04.2019) | Threshold limit (₹) for Senior Citizen (w.e.f. 01.04.2018) |

| Banking company (on time deposit) | 40,000 | 50,000 |

| Co-operative society carrying on banking business (on time deposit) | 40,000 | 50,000 |

| Co-operative whose turnover exceeds Rs 50 Crores during the previous financial year | 40,000 | 50,000 |

| Post office (on SCSS) | 40,000 | 50,000 |

| Any other person | 5,000 | 5,000 |

Time deposits shall include recurring deposits within its scope for the purposes of deduction of tax under section 194A (w.e.f. 01.06.2015). However, the existing threshold limit of ₹40,000 for non-deduction of tax shall also be applicable in case of interest payment on recurring deposits to safeguard interests of small depositors.

7) How threshold limit on interest income under section 194A computed?

Until 31st May, 2015, the threshold limit was computed with reference to the income credited/paid by a branch of the banking company or co-operative society, as applicable.

W.e.f. 1st June 2015, the computation of interest income for the purposes of deduction of tax under section 194A should be made with reference to the income credited/paid by the banking company or the co-operative society or the public company (i.e. all branches) which has adopted core banking solutions.

8) When provisions of under section 194A are not applicable?

Tax u/s 194A is not deductible in the following cases:

1) The aggregate amount of interest credited/paid (or likely to be credited/paid) during the FY does not exceed the specified threshold limit.(SEE POINT 6)

2) Interest is paid/credited to any banking company, co-operative bank, public financial institutions, LIC, UTI, an insurance company, co-operative society carrying the business of insurance or notified institutions.

3) Interest is paid/credited by the firm to its partner(s).

ILLUSTRATION–

M/s. X & Co., partnership firm, pays ₹ 15000 as interest on capital to partner Mr. R, a resident in India and ₹ 25000 as interest on capital to partner Mr. N, a non-resident.

In such a case, as per section 194A tax is not to be deducted from interest paid or payable by a partnership firm to its partner, who is resident in India. Hence, the firm need not deduct tax at source from payment of interest to its partner, Mr. R.

However, payment of interest by the firm to its non-resident partner is not governed by Section 194A. The same is governed by Section195, which requires deduction of tax at source from interest paid or payable to any non-resident.

4) Interest is paid/credited by co-operative society( not including co-operative bank) whose turnover does not exceeds Rs. 50 Crores (w.e.f. 01.04.2020) during the previous Financial year to its members [i.e. interest on time deposits /other deposits to members holding one share or to any other co-operative society.]

5) Interest is paid/credited in respect of deposits under the schemes of Post Office (Time Deposits), Post Office (Recurring Deposits), Post Office Monthly Income A/c, Kisan Vikas Patra, NSC VIII Issue, Indira Vikas Patra.

6) Interest is paid/credited on deposits (other than time deposit made on/after July 1, 1995) with a banking company or interest paid/credited to non-members on deposit with a co-operative bank.

7) Interest paid/credited in respect of deposits (by non-members) with a primary agricultural credit society or primary credit society or co-operative land mortgage bank or co-operative land development bank.

8) Interest paid/credited by Central Govt. under different provisions of Direct Taxes.

9) Interest paid/credited on compensation awarded by the Motor Accidents Claim Tribunal if the aggregate amount does not exceed ₹50,000. Threshold limit of ₹50,000 is applicable separately where interest is to be shared by 2 or more claimants. (w.e.f. 1stJune 2015, deduction of tax u/s 194A from interest payment on the compensation amount awarded by the Motor Accident Claim Tribunal shall be made only at the time of payment, if the amount of such payment or aggregate amount of such payments during the FY exceeds ₹50,000.)

10) Income paid/payable by an infrastructure capital company/fund or public sector company in relation to zero coupon bonds.

11) Interest paid/payable by an Offshore Banking Unit on deposits made (or borrowings) on/after Apr 1, 2005, by a person who is resident but not ordinarily resident in India

12) Interest referred to in section 10(23FC)*.

| *Section 10(23FC)-

Any income of a business trust by way of interest received or receivable from a special purpose vehicle. Explanation.—For the purposes of this clause, the expression “special purpose vehicle” means an Indian company in which the business trust holds controlling interest and any specific percentage of shareholding or interest, as may be required by the regulations under which such trust is granted registration. |

9) When is tax deducted at nil rate or lower rate?

A. When a declaration is submitted in form 15G/15H u/s 197A:

If a declaration is submitted u/s 197A by the recipient to the payer along with his/her PAN, then no tax is deductible as discussed in a later chapter.

B.When an application is submitted in form 13 u/s 197: