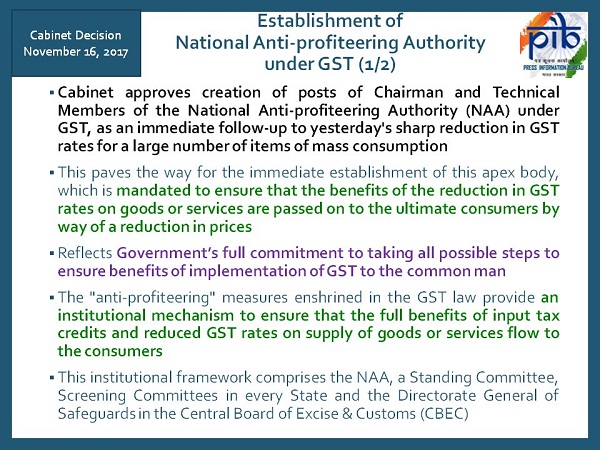

The government of India, taking lessons from the past mistakes of other countries who have implemented the GST model, has established the National Anti-Profiteering Authority to ensure that the benefit of rates reduction by GST council as on November 14, 2017, passes to the final consumer.

Any reduction in the rates of GST for supply of goods or services, or availability of input tax credit should be passed on to the final consumer by the way of reduction in prices of the commodities, but it was observed that these benefits were not passed on by the supplier of goods and services to the ultimate consumer. Many suppliers were indulging into illegal profiteering.

The union cabinet chaired by Prime Minister Narinder Modi has given approval for creation of National Anti-Profiteering Authority under GST laws to curb illegal profiteering. The aim is to ensure full implementation of GST in India and uphold the principal on consumer first.

The finance ministry assures that it is one more measure aimed at reassuring consumers that government is fully committed to take all possible steps to ensure the benefits of implementation of GST in terms of lower prices of the goods and services reach them

The anti-profiteering measures will ensure that GST provides an institutional approach to ensure that the benefit of rate reduction and input tax credit is passed on by the supplier of goods and services to the ultimate consumer.

Since implementation of GST sometimes leads to increase in prices and inflation, this measure aims at keeping the prices low and inflation in check.

Constitution of authority

The National anti-profiteering authority shall consist of 5 members one being chairman and 4 technical members.

The authority shall be in existence for 2 years from the date on which chairman enters upon his office. However, council may recommend otherwise.

Duties of authority

The main duty of authority shall be to ensure that any benefit arising from reduction in rates of GST on supply of goods or services or availability of input tax credit to suppliers, has been passed on to the ultimate consumer.

In order to ensure benefit of consumer, the authority will identify the registered person who have not passed on the benefit of rate reduction or availability of input tax credit to the ultimate consumer by commensuration reduction in price of commodities.

After identifying that the authority can cancel the registration or impose penalty or grant relief to the consumer.

How to apply

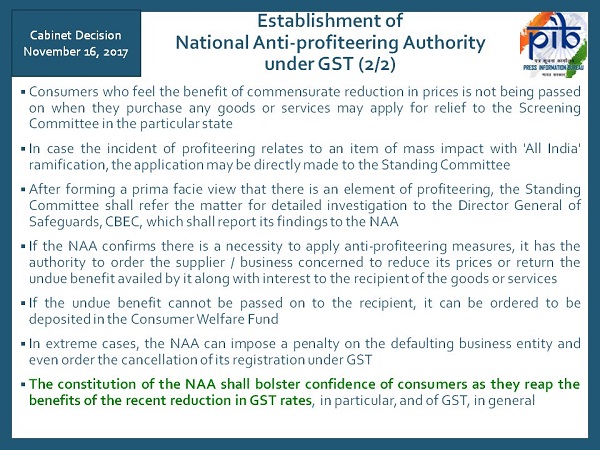

Where the affected consumer feels that the benefit of any rate reduction is not provided by the supplier, he may apply for relief to screening committee of any state.

After forming a prima facie view that there is element of profiteering the standing committee may refer the case to NAA.

If NAA confirms that profiteering by supplier exist it may provide for anti-profiteering measures like reduction in rates of commodities, extending relief to consumer or imposing penalty etc.

However if element of profiteering relates to an item of mass impact with all India ramifications, application can be made directly to NAA.

The constitution of NAA will bolster confidence amongst consumer to reap the benefit that is intended to be provided by the council and uphold the principal of consumer first.