Credit received of taxes charged on inward supplies procured by a supplier of goods or services for business operations and furtherance means input tax credit.

Page Contents

- 1. Input tax Credit: Meaning (Sec 16 of CGST Act, 2017)

- 2. What constitutes input tax credit under GST?

- 3. Who is eligible to claim input tax credit (sec 16(2) of CGST Act, 2017)

- 4. Apportionment of Input Tax Credit (Rule 42 and 43)

- 5. Final Calculation for Rule 42 for the financial year

- 6. Blocked Credits

- 7. ITC apportionment in banking sector

- 8. ITC in hotel and restaurant sector

- 9. ITC in GTA sector

1. Input tax Credit: Meaning (Sec 16 of CGST Act, 2017)

Sec 16 of CGST Act states that Every registered person shall subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person.

2. What constitutes input tax credit under GST?

Such Input Tax credit shall envelope along with Central tax, State tax, integrated tax or Union Territory tax charged on any inward supply of goods or services or both made upon a dealer, the following inputs,

- Include IGST charged on the import of goods

- Tax paid under reverse charge provisions (Sec 9(4) and 9(3))

- Exclude any tax paid under the composition scheme

3. Who is eligible to claim input tax credit (sec 16(2) of CGST Act, 2017)

Every registered person shall be entitled to claim credit of any input tax in respect of any supply of goods or services or both to him if:

- He is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed; (all the applicable particulars as specified in the provisions of Chapter VI are contained in the said document. Further Notification 39/2018-Central Tax, dt. 04-09-2018 has also provided some relaxations.)

- He has received the goods or services or both. Where the goods are received in lots input credit shall be eligible upon receipt of the last lot or installment.

- Subject to the provisions of section 41, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilisation of input tax credit admissible in respect of the said supply.

- Registered Dealer has furnished the return under section 39.

- If recipient fails to pay to the supplier on supplies other than the supplies on which tax is payable on reverse charge basis, the value of supply along with tax payable

within a period of one hundred and eighty days from the date of issue of invoice by the supplier,

an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed. - No ITC will be allowed if depreciation has been claimed on tax component of a capital good.

- The dealer has not registered himself under composition scheme in GST.

4. Apportionment of Input Tax Credit (Rule 42 and 43)

Availability of input tax credit ought to be viable only up to the extent it is used as against taxable supplies.

Taxes paid on input goods and services are eligible for credit to a registered taxpayer subject to some conditions. But, apportionment of the same is equally important respecting the foundation on which Goods and services tax Act is based. For an instance, a registered dealer who supplies exclusively only exempted goods, providing credit of taxes paid on inputs and input services to the dealer would demean the laws of a cascading free tax regime.

To sustenance former points in eyes of law, we shall analyse following sections:

Sec 17(1) of CGST Act states, where the G/S/Both are used by the registered person partly for the purpose of any business and partly for other purposes, the amount of credit shall be restricted to so much of the input tax as is attributable to the purposes of his business.

Sec 17(2) of CGST Act states, where the G/S/Both are used by the registered person partly for effecting taxable supplies including zero-rated supplies under this Act or under the Integrated Goods and Services Tax Act and partly for effecting exempt supplies under the said Acts, The amount of credit shall be restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies.

There exists no ambiguity in determining input tax credit where a supplier is engaged exclusively in either taxable or on otherwise exclusively in exempted goods, ambiguity surely arises when it’s it matter of determining the availability of “right” credit to the supplier when he is engaged in both supply.

Sec 17(6) of CGST Act provides for Rules 42 and 43 of CGST rules to determine apportionment of the credit referred to in sub-sections (1) and (2) of Sec 17.

Rule 42 comes in as a tax filter to only allow those “eligible tax” in respect of inputs or input services credit to pass through to be stated as an available credit.

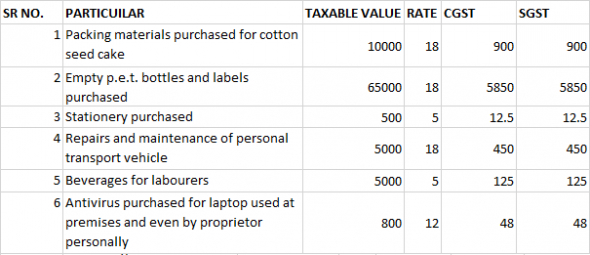

For instance let us examine a XYZ Pvt Ltd. having an oil mill of extracting cotton oil from cotton seeds, in this particular case the oil is a taxable item under GST regime and the residue i.e. cotton seed cake being an exempted good.

Let’s have assumable list of input credits co. have in Jan 2018 month (GST rates may differ from actual)

Taking into consideration Subsections 1, 2 and 5 of Section 17 of CGST Act

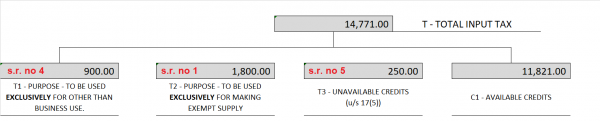

On first instance while proportioning the input credits, it is no doubt to place the exclusive credits in its own place.

- Credits exclusively relatable to purposes other than business activities.

Repairs of vehicles used by proprietor is for purposes other than business, and hence it is straightway made ineligible for credit. - Credits exclusively relatable to exempted goods.

Inputs on packing materials exclusively for cotton seed cake (exempt product) shall undoubtedly be disallowed to form a part of eligible credits. - Credits which are not available u/s 17(5)

Blocked credits which Sec 17(5) deals with, restricts among many, inputs of foods & beverages by a registered dealer. Hence, input tax on beverages for labour shall not form part of eligible credit.

Leaving us with balance credits which can be further bifurcated in to two categories:

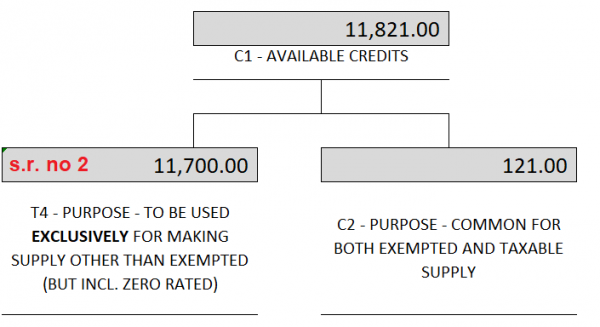

1. Credit Purpose – to be used exclusively for making supply other than exempted (but incl. Zero rated). This credit shall be fully available w/o restrictions.

Thus, empty p.e.t. bottles and labels which would “exclusively” be used for outward taxable supplies, input tax charged on those shall be eligible for credit to the registered supplier.

2. Credit Purpose – Common for both exempted and taxable supply (incl. Zero rated). This shall further be processed.

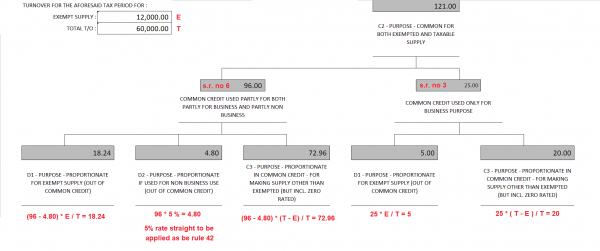

Further, we would be left with two categories of input tax credits:

- credits purpose: commonly used for taxable supply + exempt supply + non business

- credits purpose: commonly used for taxable supply + exempt supply

Now, according to rule 42 of cgst rules, we shall apportion them into 3 parts:

- Ineligible common credits used for exempt supplies (D1)

Common credit * exempt t/o for the period / total t/o of the period

- Ineligible common credits purpose – non business (D2)

Common credit * 5%

- Eligible common credits (∅2) (C3)

Common credit * (total - exempt) t/o for the period / total t/o of the period

Thus, referring to the following calculations, ∅1 and ∅2 shall only be eligible to be constituted as eligible input tax credits.

Sec 17(3) states the value of exempt supply under sub-section (2) shall be such as may be prescribed, and shall include:

Sec 17(3) states the value of exempt supply under sub-section (2) shall be such as may be prescribed, and shall include:

- Supplies on which the recipient is liable to pay tax on reverse charge basis,

- Transactions in securities,

- Sale of land and,

- Subject to clause (b) of paragraph 5 of Schedule II, sale of building.

5. Final Calculation for Rule 42 for the financial year

Before the due date for furnishing of the return for the month of September following the end of the financial year to which such credit relates, final calculation is to be done in following manner:

First, Calculate D1 and D2 for the full financial year in aggregate

Secondly, Sum up D1 and D2 for each individual months of the whole financial year If : D1 and D2 for full financial year is greater than sum of D1 and D2 of each individual months Such excess shall be added to output tax liability along with interest at the rate of 18%

If not, such deficit shall be claimed as credit by the registered person in his return.

Provisions under Rule 43 of the Central Goods and Services Tax (CGST) Rules, 2017 relating to “Manner of Determination of Input Tax Credit in respect of Capital Goods and Reversal thereof in certain Cases”, are as under:

On first instance, the amount of input tax in respect of capital goods used or intended to be used for effecting outward supplies:

1. Exclusively for non-business purposes or used or intended to be used exclusively for effecting exempt supplies – shall be disallowed.

2. Exclusively for effecting supplies other than exempted supplies but including zero-rated supplies – shall constitute eligible credit.

3. Then, amount of input tax in respect of capital goods not covered under clauses (a) and (b), denoted as ‘A’, shall be credited to the electronic credit ledger and the useful life of such goods shall be taken as five years from the date of the invoice for such goods.

Common Credit: Total Credit (-) Ineligible Credit (-) exclusively eligible credit.

Total common (Tc) credit shall be Sum of all Common credits.

Provided that where any capital goods earlier covered under clause (b) is subsequently covered under clause (c), the value of ‘A’ arrived at by reducing the input tax at the rate of five percentage points for every quarter or part thereof shall be added to the aggregate value ‘Tc’;

Step 1: Common credit Tm per month would be Tc / 60 months i.e. 5 years of useful life.

Step 2: the amount of input tax credit, at the beginning of a tax period, on all common capital goods whose useful life remains during the tax period, be denoted as ‘Tr’ and shall be the aggregate of ‘Tm’ for all such capital goods;

step 3: the amount of common credit attributable towards exempted supplies, be denoted as ‘Te’, and calculated as: Te=(E÷ F) x Tr. This Te shall be stated as ineligible credit out of the common credit.

where,

‘E’ is the aggregate value of exempt supplies, made, during the tax period, and

‘F’ is the total turnover of the registered person during the tax period.

Thus, input taxes exclusively used for effecting supplies other than exempted supplies and Balance input taxes out of common credit after deducting ineligible credit out of the common credit, shall be termed as eligible credit w.r.t capital goods.

Notes:

A. the amount Te along with the applicable interest shall, during every tax period of the useful life of the concerned capital goods, be added to the output tax liability of the person making such claim of credit.

B. The amount Te shall be computed separately for central tax, State tax, Union territory tax and integrated tax.

6. Blocked Credits

Sec 17(5) states, notwithstanding anything contained in sub-section (1) of section 16 and subsection (1) of section 18, input tax credit shall not be available in respect of the following, namely:-

1. Inputs in respect of motor vehicles and other conveyances except when they are used for :

a. for making the following taxable supplies – further supply of such vehicles or conveyances or transportation of passengers or imparting training on driving, flying, navigating such vehicles or conveyances.

b. for transportation of goods.

For instance, input taxes charged on repairs and maintenance of a bus transporting workers to and after duty is disallowed to be taken as credit. But, Input taxes charged on R&M of truck of same industry used for transportation of goods, shall be allowed as credit to the dealer.

2. Following supply of goods or services or both—

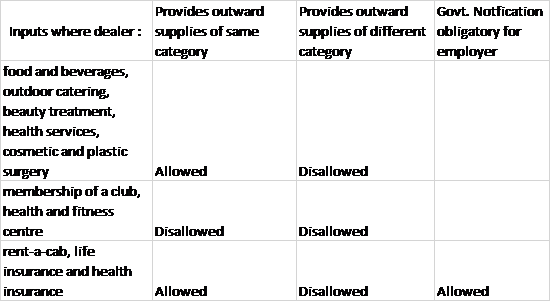

a. Input taxes in respect of food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery shall be disallowed to a dealer. except,

a. if used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply;

b. membership of a club, health and fitness centre;

c. rent-a-cab, life insurance and health insurance

except, if used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply or Government notifies the services which are obligatory for an employer to provide to its employees under any law for the time being in force.

d. travel benefits extended to employees on vacation such as leave or home travel concession.

Eg. MMT Travels lends out a car to XYLO Travels and FRIGO Industries, a manufacturing industry. Then XYLO Travels can claim ITC on the same but FRIGO industries cannot be eligible to claim ITC.

3. Works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service.

eg. TGM Industries gives contract to AGM contractors to construct an immovable property in their premises, and for this it utilizes services of other sub-contractors. Assuming, all parties are registered under GST, TGM industries will not be eligible for credit. AGM contractors would be eligible for credit from input supplies of various subcontractors.

4. Goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

For point 3 and 4, the expression “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalisation, to the said immovable property.

5. Input taxes paid on goods or services or both on which tax has been paid under section 10e. composition levy.

6. Input taxes charged on goods or services or both received by a non-resident taxable person except on goods imported by him.

7. Input taxes paid on goods or services or both used for personal consumption.

8. Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

9. Any tax paid in accordance with the provisions of sections 74, 129 and 130.

7. ITC apportionment in banking sector

Sec 17(4) of CGST Act provides for a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances to have a option of :

a. To comply with the provisions of sub-section (2) of Sec 17; or

b. To avail of, every month, an amount equal to fifty per cent of the eligible input tax credit on inputs, capital goods and input services in that month and the rest shall lapse.

Provided that the option once exercised shall not be withdrawn during the remaining part of the financial year.

Also, provided further that the restriction of fifty per cent shall not apply to the tax paid on supplies made by one registered person to another registered person having the same Permanent Account Number.

8. ITC in hotel and restaurant sector

The GST Council in its 23rd Meeting held at Guwahati on 10th of November, 2017 recommended key changes in Tax rates for a uniform rate of 5% tax would be levied on all the Restaurants without distinction of Air Conditioned or Non-Air Conditioned without the benefit of claiming Input Tax Credit (ITC). (Notification No. 46/2017-Central Tax (Rate), dated 14th November 2017).

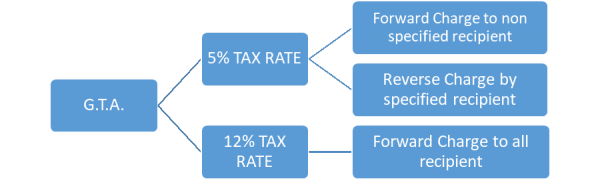

9. ITC in GTA sector

Taking into consideration these 3 notifications: Notification No. 13/2017, Notification No. 11/2017, Notification No. 20/2017 Central Tax (Rate) for Goods and Transport agency sector, we shall conclude that they shall have following options:

GTA services (including transportation of used household goods for personal use) attract a GST rate of either 5 percent (2.5 percent CGST, 2.5 percent SGST), or 12 percent (6 percent CGST, 6 percent SGST). The rate of 5 percent is subject to the condition that service providers have not taken input tax credit (ITC) for the tax charged on the goods or services used in supplying the service.

The entire scheme of taxation under GST is to reduce the cascading effect. It being a destination based consumption tax; the burden of tax shall be borne by the ultimate consumer. At each stage of taxation, input tax credit is allowable to the registered taxable person. This, input taxes should be according to the nature and its use in a dealers for effecting outward supplies, some credits should be apportioned and disallowed, some should be blocked and some reversed in interest of laws and its principals.

Kindly find the attached Excel utility for working out calculations of Rule 42 and 43 of CGST Rules 2017

Also note : All above mentioned facts and illustrations are personal interpretation of laws of author, Reliance on them shall not construe legal obligation.

Read about section 80E deductions for interest on education loan here

Author Bio

Very goods Articles and very useful to the common persons.

CAN ITC AVAILABLE FOR REPAIR OF BUILDING?