The last date for furnishing of Annual Return in the FORM GSTR-9 / FORM GSTR-9A and Reconciliation Statement in FORM GSTR-9C for the financial year 2017-18 has been extended from 31st August, 2019 to 30th November, 2019. RoD Order No. 07/2019-CT dtd. 26.08.2019.

Last date for Annual Returns- Last Date for filing of Annual returns Annual return / Reconciliation Statement for the period from the 1st July, 2017 to 31st March, 2018 in FORMs GSTR-9, GSTR-9A and GSTR-9C Extended to 30th November, 2019.

Press Release

Subject:- Extension of Due Date to 30th November, 2019 for furnishing ‘Annual Return and Reconciliation Statement’ for FY 2017-18

It is hereby informed that the last date for furnishing of Annual Return in the FORM GSTR-9 / FORM GSTR-9A and Reconciliation Statement in the FORM GSTR-9C for the Financial Year 2017-18 is extended from 31′ August, 2019 to 30th November, 2019.

Order

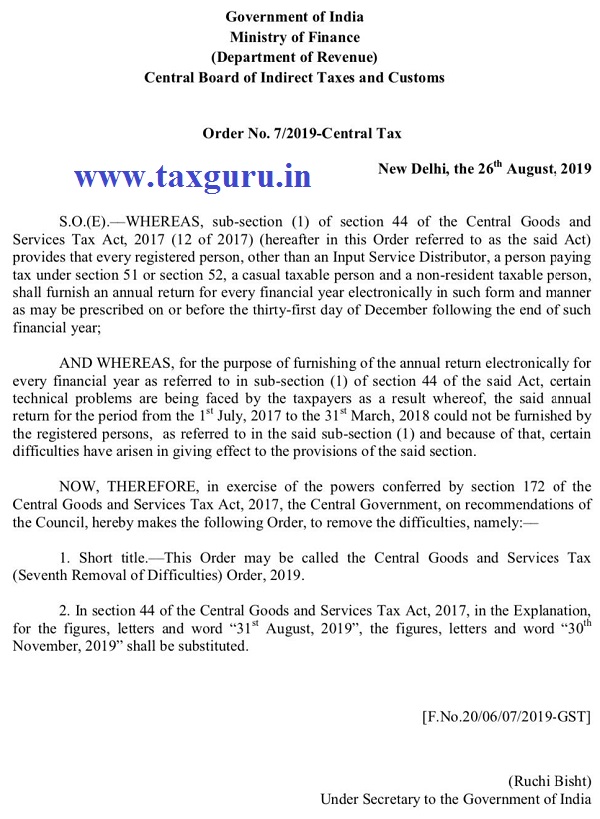

Government of India

Ministry of Finance

(Department of Revenue)

Central Board of Indirect Taxes and Customs

Order No. 7/2019-Central Tax

New Delhi, the 26th August. 2019

S.O.3071(E).—WHEREAS, sub-section (1) of section 44 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this Order referred to as the said Act) provides that every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return for every financial year electronically in such form and manner as may be prescribed on or before the thirty-first day of December following the end of such financial year;

AND WHEREAS, for the purpose of furnishing of the annual return electronically for every financial year as referred to in sub-section (1) of section 44 of the said Act, certain technical problems are being faced by the taxpayers as a result whereof, the said annual return for the period from the 1st July, 2017 to the 31st March, 2018 could not be furnished by the registered persons, as referred to in the said sub-section (1) and because of that, certain difficulties have arisen in giving effect to the provisions of the said section.

NOW, THEREFORE, in exercise of the powers conferred by section 172 of the Central Goods and Services Tax Act, 2017, the Central Government, on recommendations of the Council, hereby makes the following Order, to remove the difficulties, namely:—

1. Short title.—This Order may be called the Central Goods and Services Tax (Seventh Removal of Difficulties) Order, 2019.

2. In section 44 of the Central Goods and Services Tax Act, 2017, in the Explanation, for the figures, letters and word “31st August, 2019″, the figures, letters and word “30th November, 2019″ shall be substituted.

[F.No.20/06/07/2019-GST]

(Ruchi Bisht)

Under Secretary to the Government of India

So complicated and nobody knows full systems. But penalty is so high. Interest is 18%. First make system easy to layman. Otherwise many of us will have to

Close for escaping penalty happened by mistake. Give chance to revise the return

Extension is like the extension of CA Final Exam. Great relief when the exam got postponed but again a huge pain when the exam is approaching. Instead the GST Annual Return form should be made simpler rather creating huge tension to the traders and practitioners due to its complexity.In Annual Return traders must be able to revise the entire monthly return if they felt it was wrong and pay tax or claim refund on that basis.Though it was postponed, it is believed that only 50 to 60% of the people will comply it with by 30th Nov. All practitioners will start re open the case from 1st Nov onwards after Company Audit and Tax Audit.

DATE EXTENSION IS GOOD NEWS BUT IT ALSO VERY NECESSARY TO SIMPLIFY THE FORMATS OF GSTR 9,9A,9C. IT SHOULD BE DEVELOPED IN THE PATTERN OF INCOME TAX WHERE IS NO PROBLEM TO FILE THE ITR.

Facility for filing Revised Return for GSTR9/9C should be enabled. When there is a mismatch between GSTR1 and GSTR3B, there is no filed to capture this difference except the mismatch in ITC between 2A & 3B. Annual return should be made simple. Best thing is to scarp Annual Returns for 17-18.

It’s very nice to hear this news but feeling sad bcoz the returns need to be simplified as small entrepreneur cannot afford to pay huge fees for getting the work done.

They have enough of returns to be filed GST/PT/TDS/IT etc.

Instead of postponing the date all various returns pertaining to statutory liabilities must be simplified and not changed at the whims and fancies of the powers that be.

Thanks for the extension of the due date. Would recommend a simplified return and filing of DRC03 form. It is very painful to enter so many rows in the GST portal. It will definitely get timed out by the time we prepare everything online.

Would suggest that the department should allow all the ineligible credits for FY 2017-18 as they have been utilised unknowingly and not intentionally. All the Input Tax Credits utilised have been discharged by the goods or service providers. Govt. has received their due GST.

Now, just simplify the annual returns by merging all the months return to consolidate and file easily. Why to penalise with Interest when the GST in question has already been paid by the Goods or service providers.

I doubt that atleast 20% of the Tax Payers 2A report will match with the Input Tax Credits. The department has to be lenient as there are many errors committed by the vendors while reporting B2C Sales instead of B2B Sales.

These have to be waived with a lenient view as there is no loss to the Department as all the GST in question have been discharged by the respective vendors.

many errors have been

Instead of extension of date they should simplified the return otherwise same thing will happen in the month of November also. Why not they understood the problems facing by the assessee and consultant

Abhi CBEC ki website pr to ye order publish nhi hua hai, aapko kaise mil gya 😮 ?

Thanks for postponing the date.

goods news for all tax payers

Thanks for Extension of date and it is a good move.

very happy to given the government postponed submit of returns 2017-18 November thanks

Of course good news but they should simplify the return format.

instead of demanding repeated extensions, trade should actually demand a simplified format, which is a just an accumulation of all monthly returns filed. This should be thought of atleast for the 1st year.

Its very good action taken and get the extension.thank you.

Thank you for conveying the GOOD NEWS. Last few days I was very much worried, as I could not complete the task of preparing the GSTR 9. Thanks for the effort you have taken and for the articles on the subject.

thanks for your representation to government and get the extension

Good Move…of course time needed.