Often, entrepreneurs form Limited Liability Partnerships but are not able to maintain the same. Also, the penalty for LLPs defaulting in filing of any statutory return is Rs.100/- per day, without any maximum limit. Hence, it is often best to strike off/close dormant LLPs so that there is no requirement to file LLP Form 11, LLP Form 8 and Income Tax Return for the LLP each financial year to maintain compliance and avoid penalty.

In this article, we shall study about the various aspects of striking off a LLP:

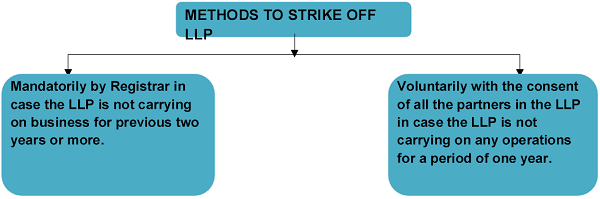

The provisions of striking off of LLP are governed by Rule 37(1) of the Limited Liability Partnership Rules, 2017. Accordingly, the LLP can be stroked off in following two ways, likewise that of a Company:

Mandatory Striking of the LLP:

Under mandatory striking off, the ROC shall send a notice to the LLP of his intention to strike off the name of the LLP from the register and requesting them to send their representations within a period of one month from the date of the notice in the case the LLP is not carrying on any business for a period of two preceding years. Here it is important to note that the ROC shall have reasonable cause to believe that the LLP is not doing any business in case Form 8 and Form 11 are not filed for previous two years.

Voluntary Striking off the LLP:

Under voluntarily striking off of LLP, the LLP may make an application in e-Form 24 to the Registrar with the consent of all the partners of the LLP for striking off its name from the register.

Now, we shall discuss the important points after interpretation of the relevant rule with respect to striking off the LLP:

1. Where the Limited Liability Partnership is regulated under a special law, the application for removal of name shall be accompanied by approval of the regulatory body constituted or established under that law.

2. The contents of the notice issued the ROC and the application made by the LLP shall be placed on the website of the Ministry of Corporate Affairs for the information of the general public for a period of one month.

3. As discussed, in case of mandatory strike off, the Registrar shall send a notice to the LLP to give reasonable opportunity of being heard as to why the LLP shall not be dissolved. The correspondence of the said notice shall have to be made within a period of one month or else the Registrar shall strike its name off the register, and shall publish notice in the Official Gazette thereof.

4. The liability of the every designated partner of the LLP dissolved as such shall continue and may be enforced as if the LLP had not been dissolved.

Further, it is important to note that the following shall be the attachments to e-Form 24:

- Affidavit signed by the designated partners [as per the format given sub clause (b) of clause (II) of sub rule (1A) to rule 37)];

- Copy of authority to make the application duly signed by all the partners;

- Copy of acknowledgement of latest ITR, in case filed;

- Consent of all the partners;

- Statements of accounts disclosing nil assets and nil liabilities certified by a Chartered Accountant in practice made up to a date not earlier than thirty days of the date of filing; and

- Application disclosing the reasons for strike off and the operative status of the Company.

FAQS REGARDING STRIKING OFF THE LLP

1. In case the LLP has not opened any bank account and has not carried on any operations since incorporation, then also can we file Form 24?

Yes, in case the LLP has been inoperative since incorporation, then Form 24 can be filed giving the same reason.

2. In case the Company has been operative for initial two years and thereafter got inoperative, then also the LLP can get itself stroked off without filing Form 11 and Form 8?

Yes, in accordance with the provisions, the LLP shall file overdue returns in Form 8 and Form 11 only the financial year till when it has ceased to carry on business operations. For instance, the LLP shall worked for FY 2013-14 and 2014-15 and thereafter ceased to carry on operations, then also it can make an application for strike off in Form 24 in the year 2018 without filing overdue Form 8 and Form 11.

3. What shall be format to issue a statement of assets and liabilities by the Chartered Accountant?

In accordance with the provisions of the LLP Act, 2009, there is no fixed format for statement of assets and liabilities of an LLP. However, in general parlance, the auditors prepare the accounts of the LLP as per the format of Form 8 and accordingly, the said format shall be followed for preparing the said statement of assets and liabilities.

Author Bio

Hello Mam,

Can you please provide drafts of application, affidavit and indemnity bonds and other documents required as attachments under form 24.

Please be noted that, at least, annual returns for one F.Y. is to filed filed, irrespective of business done or not, without which From 24 can not be uploaded.

Please you note that in 2017 notification came out that any LLP, which is inoperative since incorporation or particular year is not required to file LLP returns and can go ahead for strike off. So don’t spread rumors.

Please you note that notification came in 16th May, 2017 that any LLP which is inoperative since incorporation and since any particular year, then LLP is not required to file returns and can proceed for strike off. So please before commenting check it.

Madam,

If an llp is inoperative from its incorporation i.e., 2 yrs

But filed nill form 8 for first year

And remaining forms are due till now

Can we file form 24 without filing

Form 11 for both the years and form 8 for the second year