This article enlightens about the company’s compliance with the Companies Act 2013 and the latest amendments thereof. The Ministry of Corporate Affairs in the early months of the new calendar year i.e. 2022 has issued various notifications introducing new Compliances and reporting requirements in the Corporate Circle.

Every company registered in India must abide by the provisions of the Companies Act, 2013. Non-compliance leads to the hefty penalty that will keep increasing with every passing day or litigation and compounding of the matter, disqualification of Director, and even strike off the company. Therefore, to help you to avoid such situations, we have brought for your information and reference the updated annual compliance Calendar for the year 2022-2023

DATE WISE COMPLIANCE TABLE

| Due Date | e-Form | Penalty/additional fees |

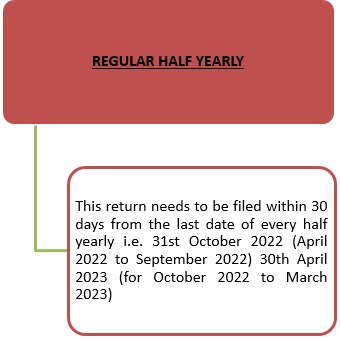

| April–September = 31st October 2022 and

October – March = 30th April 2023 |

MSME -1 | Company – 25,000

every officer in default- Fine 25, 000 to 3,00,000 Imprisonment- 6 months |

| 30.05.2022 | LLP Form – 11 (Annual Return) | Multiple times of normal government fees |

| 30.06.2022 | Form DPT -3 | An additional fee will be applicable in delay filing |

| 30.09.2022 | Form DIR-3 KYC | Delay filing- Rs. 5000 |

| 30.10.2022 | Form LLP-8 (For filing statement of Account & Solvency with the Registrar) | Multiple times of actual government fees |

| Within 30 days of AGM | Form AOC-4/ AOC-4 CFS (Financial Statements) | Rs. 100 per day is payable from the due date of filing return till the date actual return is filed. |

| Within 60 days of AGM | Form MGT-7 or MGT-7A (Annual Return) | Rs. 100 per day is payable from the due date of filing return till the date actual return is filed |

| Within 45 days beneficial interest in company | BEN-2 | INR 1000 per day after the failure |

E-FORM MSME-1

All companies, who get supplies of products or services from micro and small enterprises and whose payments to micro and small business enterprise suppliers exceed 45 days from the date of acceptance or the date of deemed acceptance of the goods or services as in step with the provisions of section 9 of the Micro, Small and Medium Enterprises Development Act, 2006, shall submit a return to the Ministry of Corporate Affairs within the interval mentioned below;

THE FACTORS COVERED INSIDE THE FORM:

- The amount of payment due and

- The reasons for the delay

EXEMPTION TO THIS RULE:

The Rules’ applicability is not for all the Companies but only for the Specified Companies whose payment to MSMEs suppliers exceed 45 days from the date of acceptance or deemed acceptance of the goods or services as per section 9 of the MSME Development Act, 2006.

An exemption is likewise applied in cases where payment against supplier exceeds 45 days however the supplier/Creditors gives a declaration that they do now not lie in the category of Micro or small Enterprises.

As per section 405 of the Companies Act, 2013, the Central Government made it necessary for all the “Specified Companies” to furnish the above-notified information regarding payment to micro and small enterprise suppliers.

PENALTY

Section 405(4) which includes non-furnishing/incomplete/incorrect information penalty states a fine up to INR 25000/- (Min) & INR 3 lacs (max) and imprisonment of 6 months for directors or both. Therefore it is mandatory for directors to file the MSME form 1

As per section 405 of the Companies Act, 2013, the Central Government made it necessary for all the “Specified Companies” to furnish the above-notified information regarding payment to micro and small enterprise suppliers.

LLP FORM – 11 (ANNUAL RETURN)

Every LLP is required to file an annual return in e-Form LLP Form No. 11 within 60 days of the closure of its financial year. The annual return shall be accompanied by a certificate from a company secretary that he has verified the particulars including from the books and records of the limited liability partnership and found them to be true and correct.

MCA vide its notification dated 4th March 2022, mandated the web-based filling of e-Form LLP-11.

PENALTY

Delay in filling LLP-11 shall lead to hefty penalties imposed by the government, which are multiple times the normal fees. The penalty could be 25 times (in the case of small companies) and 50 times (in cases other than small companies) the actual government fee.

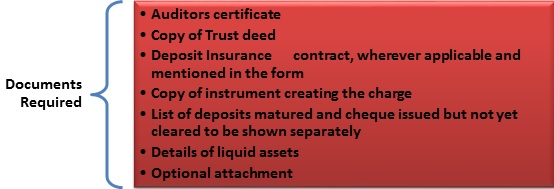

FORM DPT -3

MCA vide its notification dated 22nd January 2019 notified that every Company other than Government Company is required to file this form every year on or before 30th June in respect of return of Deposit and Particulars not considered as Deposit as on 31st March.

As per Rule 16 (A) (3) of the Companies (Acceptance of Deposits) Rules, 2014 Every company other than a Government company is required to file return for the period of 01st April 2021 to 31st March 2022 on or before 29th June 2022 by stating particulars of outstanding receipt of money or loan by a company but not considered as deposits.

One time return is filed by stating the following:-

- Net Worth as per the latest audited balance sheet preceding the date of the return

- Particulars of charge

- Total amounts of outstanding money or loan received by a company but not considered as deposits in terms of rule 2(1)(c) of the Companies (Acceptance of Deposits) Rules,2014

DOCUMENTS TO BE SUBMITTED

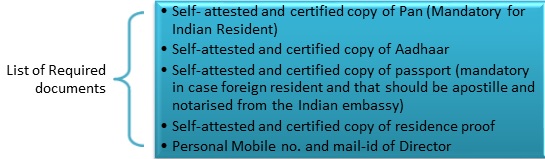

DIR-3 KYC

MCA has vide its notification dated 25th July, 2019, mandated the filing of e-Form DIR – 3 KYC for the following –

1. For Individuals to whom DIN was allotted on or before 31st March 2021 and who have filed the said form earlier:

A If there is no change in particulars of individuals filed in an earlier form, then web-Form DIR-3-KYC-WEB has to be filed;

B If there is any change in a personal mobile number or the e-mail address of the individual, then e-Form DIR-3 KYC has to be filed for this year;

C In case of changes other than those mentioned in 1(B), the individual has to file Form DIR-3 KYC WEB along with Form DIR- 6.

2 For Individuals to whom DIN was allotted on or after 01st April, 2021, the individuals are required to file e-Form DIR-3 KYC.

3 Due Date for e-Form DIR – 3 KYC and web-Form DIR-3-KYC-WEB: 30th September, 2022

4 MCA Fees for e-Form DIR – 3 KYC and web-Form DIR-3-KYC-WEB: Until 30th September, 2022, MCA fee shall be NIL. However, after 30th September, 2022, MCA fee shall be Rs. 5,000/- on account of delay filing.

5 Consequence of not filing e- Form DIR – 3 KYC and web-Form DIR-3-KYC-WEB:

A Director Identification Number of an individual shall be deactivated.

B Further, the deactivation of DIN shall continue until the filing of the said form along with Rs. 5,000/- (MCA Fee).

Note –For e-Form DIR – 3 KYC, the phone no. and mail id of the individual shall be verified through OTP. For web-Form DIR-3-KYC-WEB, there is no such verification required.

DOCUMENTS REQUIRED.

E-FORM AOC-4 (FINANCIAL STATEMENTS)

Every company needs to file its financial statements and mandatory attachments, via e-Form AOC4 within 30 days of date of AGM (due date of AGM if AGM not held or extended due date if any) as per section 137. In case financial statements are not adopted in AGM then un-adopted financial statements shall be filed.

The following is the complete list of documents that must be filed with AOC-4:

1. Copy of financial statements duly authenticated as per section 134 (including Board’s report, auditors’ report and other documents)

2. Statement of subsidiaries as per section 129 – Form AOC-1

3. Statement of the fact and reasons for not adopting financial statements in the Annual General Meeting (AGM)

4. Statement of the fact and reasons for not holding the AGM

5. Approval letter of extension of financial year or AGM

6. Supplementary or test audit report under section 143

7. Company CSR policy as per sub-section (4) of section 135

8. Details of other entity(s)

9. Details of salient features and justification for entering into contracts/Arrangements/transactions with related parties as per Sub-section (1) of section 188 – Form AOC-2

10. Details of comments of CAG of India

11. Secretarial Audit Report

12. Directors’ report as per sub-section (3) of section 134

13. Details of remaining CSR activities

14. Optional attachment(s), if any.

The following companies are required to file AOC 4 XBRL (extensible business reporting language):

- All companies listed with any stock exchange in India and their Indian subsidiaries.

- All companies with a capital of 5 crores or above.

- All companies with a turnover of 100 crores or more.

- All companies which were covered till date under the Companies Rules 2011.

FORM MGT-7 and MGT-7A (ANNUAL RETURN)

Pursuant to Section 92(1) of the Companies Act, 2013, Every company shall prepare an annual return in the form MGT-7 or MGT-7A as the case may be within 60 days of the Annual General Meeting, containing the particulars as they stood on the close of the financial year regarding:

1. Its registered office, principal business activities, particulars of its holding, subsidiary, and associate companies;

2. Its shares, debentures, and other securities and shareholding pattern;

3. Its indebtedness;

4. Its members and debenture-holders along with changes therein since the close of the previous financial year

5. Its promoters, directors, key managerial personnel along with changes therein since the close of the previous financial year;

6. Meetings of members or a class thereof, Board and its various committees along with attendance details;

7. Remuneration of directors and key managerial personnel;

8. Penalty or punishment imposed on the company, its directors or officers and details of compounding of offenses and appeals made against such penalty or punishment;

9. Matters relating to certification of compliances, disclosures as may be prescribed;

10. Shareholding pattern of the company; and such other matters as required in the form.

* MGT- 7A for small companies or one-person companies OPC, introduced by THE MINISTRY OF CORPORATE AFFAIRS, dated 5 March, 2021.

Small Companies- A company whose paid-up share capital does not exceed INR Fifty Lakhs and the turnover as per the latest accounting books does not exceed INR Two Crore

DOCUMENTS MUST BE FILED WITH FORM MGT-7 or MGT-7A :

- List of shareholders, debenture holders would be mandatory in case of a company having a share capital.

Form LLP-8 (For filing statement of Account & Solvency with Registrar)

Form 8 is also known as Statement of Account & Solvency. Form 8 has contains a Statement of Solvency, Statement of Accounts, and Statement of Income & Expenditure. In addition to the financial position, the LLP must also declare:

- Declare that the turnover is above or below Rs. 40 lakhs.

- Declare that the obligation of contribution is above or below Rs. 25 lakhs

- Declare that the LLP has already filed a statement indicating the creation of charges or modification or satisfaction till the present financial year.

- Declare that the partners/authorized representatives have taken proper care and responsibility for the maintenance of adequate accounting records and preparation of accounts.

The following documents must be attached with Form 8:

- Disclosure under Micro, Small, and Medium Enterprises Development Act, 2006.

- In case contingent liabilities exist, a Statement of contingent liabilities is to be attached.

Any other information can be provided as an optional attachment.

PENALTY

Delay in filling LLP-11 shall lead to hefty penalties imposed by the government, which is multiple times the normal fees. The penalty could be 25 times (in the case of small companies) and 50 times (in cases other than small companies) the actual government fee

BEN-2

Form BEN-2 is the declaration that a company is required to file with the registrar under section 90 of the company act, 2013.

Form BEN-2 is the form in which the beneficial owner is required to declare a disclosure to the Registrar of his interest in the shares of the company within forty-five days of acquiring such beneficial interest in such a company.

Section 90(4) of the Companies Act, 2013 mandates every company to file a declaration in form BEN-2 with the Registrar disclosing his beneficial interest in the company.

What are the consequences of non-filing?

Section 90(11) of the Act, 2013 provides for penal provisions for the failure of the part of the company and every officer in default in complying with the provisions of Section 90(4) i.e. filing of the above return and changes therein with the Registrar with a fine:-

For the company and every officer in default:- Rs. 10 Lakhs – Rs. 50 Lakhs

For Continuing default: – Upto Rs. 1000 for every day after the first day of failure

DISCLAIMER

The entire contents of this article have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, the author assumes no responsibility therefore. Users of this information agree that the information is not professional advice and is subject to change without notice.

The author assumes no responsibility for the consequences of the use of this information.

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL, OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

THE AUTHOR – CS MONIKA MALHOTRA (PRACTICING COMPANY SECRETARY) CAN BE REACHED AT csmonikamalhotra26@gmail.com or +91-9958089808

Declare that the LLP has already filed a statement indicating the creation of charges or modification or satisfaction till the present financial year.

What if we do not have any charges?