During the course of Inquiry, it is observed that company has not filed e-form regarding appointment of Internal Auditor u/s 138 of the Companies Act, 2013 for FY 2016-17, 2017-18, 2018-19, 2019-20. Whereas, Section 179(3)(k) of the Companies Act, 2013 read with Sub-Rule 5 of Rule 8 of the Companies (Meetings of Board and its Power) Rules, 2014 mandated to file Board resolution for appointment of Internal Auditors in the Company. Hence, the company, its directors, KMPs and officers in defaults of the company are liable for violation of Section 138 r/w Section 117 of the Companies Act, 2013. The company vide reply dated 23.06.2022 has committed the default by mentioning therein that ” the company has inadvertently missed to file the resolution with regard to Internal Auditor appointment for FY 2016-17″. In view of submission of the Company, it has been revealed that Company has failed to file Form MGT-14 with ROC and to that extent Company has not complied with the provisions of Section 117 read with Section 138 of the Companies Act, 2013 and thus company and its officers in default liable to penalize under Section 117(2) of the Companies Act, 2013.

it is concluded that the company and its Officers in default are liable for penalty under Section 117(2) of the Companies Act, 2013 for non-filing of Board’s resolution in MGT-14, which attracted non compliance of the provisions of Section 117(1) of the Companies Act, 2013 and the undersigned has reasonable cause to believe that the company and its Director(s) have violated the provisions of Section 117(1) of the Companies Act, 2013. In view the facts narrated above, the company and its directors /officers, in default are liable for penalty as per Section 117(2) of the Companies Act.

MCA impose penalty of Rs. 3,95,900 on company and its directors as prescribed under Section 117(2) of the Companies Act, 2013 for violation of section 117(1) of the Companies Act, 2013.

****

Order NO.ROC-GWADJ-Order/Section 454/ Hindustan Oil /2022-23/7165 7071 Dated: 31.01.2023

BEFORE THE ADJUDICATING OFFICER

REGISTRAR OF COMPANIES, GUJARAT, DADRA & NAGAR HAVELI

IN THE MATTER OF ADJUDICATION OF PENALTY UNDER SECTION 454 (3) OF THE COMPANIES ACT 2013 READ WITH RULE 3 OF THE COMPANIES (ADJUDICATION OF PENALTIES) RULES, 2014 FOR VIOLATION OF SECTION 117 READ WITH SECTION 179 OF THE COMPANIES ACT, 2013 AND RULES MADE THEREUNDER

IN THE MATTER OF M/S. HINDUSTAN OIL EXPLORATION COMPANY LIMITED

(L11100GJ1996PLCO29880)

Date of hearing- 30.01.2023

PRESENT :

1. Shri R.C. Mishra (ROC), Adjudicating Officer

2. Mr. Indrajit Vania (DROC), Presenting Officer

Company/ Officers/Directors/KMP/Authorized Representative : Ms. Deepika, Company Secretary on behalf of Company and Officers(KMPs)

Appointment of Adjudication Authority:-

1. The Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II dated 24.03.2015 has appointed the undersigned as Adjudicating Officer in exercise of the powers conferred under section 454 of the Companies Act, 2013 (hereinafter known as Act) read with Companies (Adjudication of Penalties) Rules, 2014 (Notification No. GSR 254(E) dated 31.03.2014) for adjudging penalties under the provisions of Act.

Company:

2. M/s. Hindustan Oil Exploration Company Limited (herein after referred to as “company”) is a company registered under the provisions of the Companies Act, 1956/2013 in the State of Gujarat, having CIN :L11100GJ1996PLCO29880 and presently having its registered office situated at “Tandalja Road Off Old Padra Road, Baroda, Gujarat-390020”.

Fact about of the case

3. Ministry/ Directorate was ordered to Inquiry of the subject company u/s 206 of the Companies Act, 2013. During the course of Inquiry, it is observed that company has not filed e-form regarding appointment of Internal Auditor u/s 138 of the Companies Act, 2013 for FY 2016-17, 2017-18, 2018-19, 2019-20. Whereas, Section 179(3)(k) of the Companies Act, 2013 read with Sub-Rule 5 of Rule 8 of the Companies (Meetings of Board and its Power) Rules, 2014 mandated to file Board resolution for appointment of Internal Auditors in the Company. Hence, the company, its directors, KMPs and officers in defaults of the company are liable for violation of Section 138 r/w Section 117 of the Companies Act, 2013. The company vide reply dated 23.06.2022 has committed the default by mentioning therein that ” the company has inadvertently missed to file the resolution with regard to Internal Auditor appointment for FY 2016-17″. In view of submission of the Company, it has been revealed that Company has failed to file Form MGT-14 with ROC and to that extent Company has not complied with the provisions of Section 117 read with Section 138 of the Companies Act, 2013 and thus company and its officers in default liable to penalize under Section 117(2) of the Companies Act, 2013.

4. Ld. Regional Director, NWR, Ministry of Corporate Affairs, Ahmedabad has issued instructions vide dated 03.10.2022 to take necessary action in the matter of violation of Section 138 read with Section 117 of the Companies, 2013 pointed out in Inquiry report and submit action taken report to the Directorate.

5. Relevant Provisions of Companies Act, 2013:

SECTION 138(1) of the companies Act, 2013 provides that Such class or classes of companies as may be prescribed shall be required to appoint an internal auditor, who shall either be a chartered accountant or a cost accountant, or such other professional as may be decided by the Board to conduct internal audit of the functions and activities of the company.

As per the requirement of Rule (1)(a) of Companies (Accounts) Rules, 2014, every listed company shall be required to appoint an internal auditor which may be either an individual or a partnership firm or a body corporate.

As per the requirement of Section 179(3) (k) of the Companies Act, 2013 read with Rule 8(4) of Companies (Meetings of Board and its Powers) Rules, 2014, the Board of Directors of a company shall exercise the powers on behalf of the company by means of resolutions passed at meetings of the Board to appoint Internal Auditors in the company.

Section 117(1) of the Companies Act, 2013:

A copy of every resolution or any agreement, in respect of matters specified in subsection (3) together with the explanatory statement under section 102, if any, annexed to the notice calling the meeting in which the resolution is proposed, shall be filed with the Registrar within thirty days of the passing or making thereof in such manner and with such fees as may be prescribed ;

Rule 24 of the Companies (Management and Administrations) Rules, 2014 provides that “A copy of every resolution or any agreement required to be filed, together with the explanatory statement under section 102, if any, shall be filed with the Registrar in Form No. MGT.14 along with the fee.”

Section 117(2) of the Companies Act, 2013 [prior to Companies (Amendment) Act, 2020 vide Notification dated 28th September, 2020 Amendment Effective from 21st December 2020]

If any company fails to file the resolution or the agreement under sub-section (1) before the expiry of the period specified therein, such company shall be liable to a penalty of one lakh rupees and in case of continuing failure, with further penalty offive hundred rupees for each day after the first during which such failure continues, subject to a maximum of twenty-five lakh rupees and every officer of the company who is in default including liquidator of the company, if any, shall be liable to a penalty of fifty thousand rupees and in case of continuing failure, with further penalty offive hundred rupees for each day after the first during which such failure continues, subject to a maximum offive lakh rupees.

Section 117(2) of the Companies Act, 2013 got amended w.e.f. 21.12.2020, which now reads as follows:

If any company fails to file the resolution or the agreement under sub-section (1) before the expiry of the period specified therein, such company shall be liable to a penalty of ten thousand rupees and in case of continuing failure, with a further penalty of one hundred rupees for each day after the first during which such failure continues, subject to a maximum of two lakh rupees and every officer of the company who is in default including liquidator of the company, if any, shall be liable to a penalty of ten thousand rupees and in case of continuing failure, with a further penalty of one hundred rupees for each day after the first during which such failure continues, subject to a maximum of fifty thousand rupees.

Show Cause Notice, reply and personal Hearing:-

6. Under the compliance of instructions of the Directorate’s dated 03.10.2022, an Adjudication Notice was issued to company and its directors/KMPs at the relevant time of default vide No. ROC-GJ/ADJ-64/STA(V)/u/s 454/ HINDUSTAN OIL/2022-23/5173 to 5178 dated 17.10.2022 under Section 454 of the Companies Act, 2013 read with Companies (Adjudication of Penalties) Rules 2014 for violation of Section 117(1) read with Section 138/179 of the Companies Act, 2013. The Company has furnished its reply vide letter dated 16.11.2022 and has committed the default of the provisions of Companies Act, 2013 as described detailed in the Show cause Notices. In its reply the company submitted that “in order to rectify thethe inadvertence, the company at its board meeting held on November 09, 2022 passed a resolution ratifying the decision of the board taken during the financial year 2016-17 in relation to appointment of the internal Auditor. Further the company has filed the said resolution with ROC in the e-Form MGT-14 vide SRN F43889393 dated 15.11.2022”. It is observed from MCA21 portal that said e-form has been approved via STP mode by delay of more than 5years.

7. Thereafter, a “written Notice” vide No. ROC-GJ/ADJ-64/STA(V)/u/s 454/ HINDUSTAN OIL/2022-23/6712 to 6717 dated 10.01.2022 were issued to the company and its officers as per sub-section 4 of 454 of the Companies Act, 2013 read with Rule 3 of Companies (Adjudication of Penalties) Rules, 2014 and a hearing was fixed for 30.01.2023.

8. Ms. Deepika Company Secretary attended the hearing conducted on 30.01.2023 on behalf of the company and /or the director(s)/KMPs for the relevant time and submitted that the company has duly filed the necessary e-form MGT-14 in relation to appointment of M/s. Guru & Ram LLP, Chartered Accountants as an internal Auditor of the company since the financial year 2014-15 till present date except for the financial year 2016-17 with the Registrar of Companies, Gujarat. Additionally appointment of M/s Guru & Ram LLP, Chartered Accountants as an internal auditor of the company was also recorded in the report of the Board of Directors of the Company for the financial year from 2014-15 to 2022-23 which was filed with the RoC in the relevant e-form. However, Board meeting of the company held on 18.04.2016 was inadvertently missed and hence resolution was not filed with ROC in the e-Form MGT-14. Ms. Deepika requested to impose minimum penalty for the above mention default of provisions of Section 117(1) r.w. 179(3)(k) of the Companies Act, 2013.

9. The Presenting Officer responded that the company was required to file Board’s resolution dated 18.04.2016 within 30days, however, such resolution under MCA21 portal on 15.11.2022 which required to file in e-form MGT-14 on or before 17.05.2016 in pursuant to Section 117(1) of the Companies Act, 2013. Therefore, the company and its officers/KMPs at the relevant time are liable for a penalty as per Section 117(2) of the Companies Act, 2013 for non-filing of required e-form MGT-14 within due time.

10. The Presenting Office further submitted that the object of filing such information under the MCA-21 portal/public Domain is in the public interest, to enable the investors, public and whosoever interested in the Listed company can access the information pertaining of the such Company under the Law. Non-filing of documents under the MCA portal will result in denial of information to public /stake holders and this type of activity should be avoided.

11. By keeping in mind, the ease of doing business in India and oral submission made by Ld. CS as well in compliance to instructions dated 03.10.2022 received from Directorate in the instant case, the undersigned is considered penalty provided under the Companies (Amendment) Act, 2020 vide Notification dated 28th September, 2020 Effective from 21st December 2020 for default regarding filing of Board’s resolution dated 18.04.2016 in MGT-14 on 15.11.2022 committed prior to 21.12.2020.

12. Under the above circumstances, it is concluded that the company and its Officers in default are liable for penalty under Section 117(2) of the Companies Act, 2013 for non-filing of Board’s resolution in MGT-14, which attracted non compliance of the provisions of Section 117(1) of the Companies Act, 2013 and the undersigned has reasonable cause to believe that the company and its Director(s) have violated the provisions of Section 117(1) of the Companies Act, 2013. In view the facts narrated above, the company and its directors /officers, in default are liable for penalty as per Section 117(2) of the Companies Act.

13. While adjudging quantum of penalty under section 117(2) of the Act, the Adjudicating Officer shall have due regard to the following factors, namely;

a. The amount of disproportionate gain or unfair advantage, whenever quantifiable, made as a result of default.

b. The amount of loss caused to an investor or group of investors as a result of the default.

c. The repetitive nature of default.

14. The Presenting Officer further submitted that with regard to the above factors to be considered while determining the quantum of penalty, it is noted that the disproportionate gain or unfair advantage made by the noticee or loss caused to the investor as a result of the delay on the part of the notice to redress the investor grievance are not available on the record. Further, it may also be added that it is difficult to quantify the unfair advantage made by the noticee or the loss caused to the investors in a default of this nature.

15. The Presenting Officer further submitted that Company is listed entity. Hence, as per Section 2(85) of the Companies Act, 2013 read with Companies (Specification of definition details) Amendment Rules, 2022 notified vide Ministry’s Notification No. G.S.R. 700(E) dated 15.09.2022, 2013, the Company does not fall under the ambit of “small company”. Therefore, the provisions of imposing lesser penalty as per the provisions of Section 446B of the Companies Act, 2013 do not apply to the company.

ORDER:

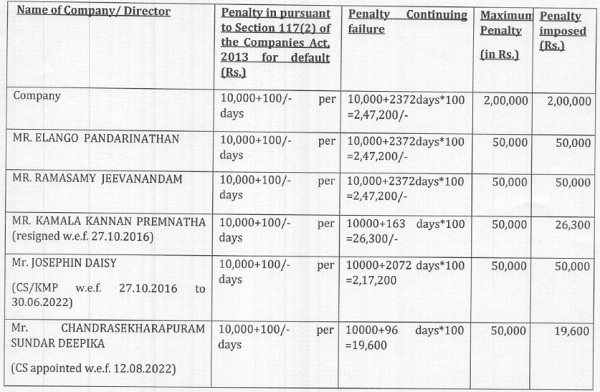

1. Having considered the facts and circumstances of the case and submissions made by the Presenting Officer and oral submission made by Ld. CS and after taking into accounts the factors above, I hereby imposed following penalty on company and its directors as prescribed under Section 117(2) of the Companies Act, 2013 for violation of section 117(1) of the Companies Act, 2013, I am of the opinion that penalty is commensurate with the aforesaid failure committed by the Noticees:

Penalty on company and Officers/KMPs in default for the aforesaid default are as under:

[Default calculated w.e.f. 17.05.2016 to 14.11.2022 (as MGT-14 filed on 15.11.2022)]

2. The noticee shall pay the amount of penalty individually for the company and its officers from their personal sources/income by way of e-payment available on Ministry website www.mca.gov.in under “Pay miscellaneous fees” category in MCA fee and payment Services under Rule 3(14) of Company (Adjudication of Penalties) (Amendment) Rules, 2019 within 60 days from the date of receipt of this order and copy of this adjudication order and Challan/SRN generated after payment of penalty through online mode shall be filed in INC-28 under the MCA portal without further reference.

3. Appeal against this order may be filed in writing with the Regional Director, North Western Region, Ministry of Corporate Affairs, ROC BHAVAN, OPP. RUPAL PARK, NR. ANKUR BUS STAND, NARANAPURA, AHMEDABAD (GUJARAT)-380013 within a period of sixty days from the date of receipt of this order, in Form ADJ setting forth the grounds of appeal and shall be accompanied by the certified copy of this order. [Section 454(5) & 454(6) of the Companies Act, 2013 read with the Companies (Adjudicating of Penalties) Rules, 2014 as amended by Companies (Adjudication of Penalties) Amendment Rules, 2019].

4. Your attention is also invited to Section 454(8)(i) and 454(8) (ii) of the Companies Act, 2013, which state that in case of non-payment of penalty amount, the company shall be punishable with fine which shall not less than Twenty Five Thousand Rupees but which may extend to Five Lakhs Rupees and officer in default shall be punishable with Imprisonment which may extend to Six months or with fine which shall not be less than Twenty Five Thousand Rupees by which may extend to one Lakhs Rupees or with both.

The adjudication notice stands disposed of with this order.

(R.C. MISHRA,ICLS)

REGISTRAR OF COMPANIES &

ADJUDICATING OFFICER

MINISTRY OF CORPORATE AFFAIRS

GUJARAT, DADRA & NAGAR HAVELI

(R.C. MISHRA, ICLS)

REGISTRAR OF COMPANIES &

ADJUDICATING OFFICER

MINISTRY OF CORPORATE AFFAIRS

GUJARAT, DADRA & NAGAR HAVELI

NO.ROC-GJ/ADJ-Order/Section 454/ Hindustan Oil /2022-23/ Dated:

[Copy to:

Ministry of Corporate Affairs, (Through Proper Channel)

The Regional Director, (NWR), Ministry of Corporate Affairs, Ahmedabad-380013

(for information please)