In a significant development, the National Financial Reporting Authority (NFRA) under the Government of India has issued Order No. 59/2023 on October 4, 2023, regarding a case involving CA Firm M/s Ashok Holani & Co. and CA Rahul Jangir. This Order, issued under Section 132(4) of the Companies Act 2013, addresses alleged misconduct in their role as statutory auditors for Lexus Granito India Limited (LGIL) for the Financial Years 2017-18 to 2019-20.

Executive Summary

The NFRA initiated an investigation into the professional conduct of the statutory auditors of LGIL based on information received from the Securities and Exchange Board of India (SEBI) regarding accounting irregularities in the company. Following a comprehensive examination of the Financial Statements and the Audit Files, NFRA found the auditors, M/s Ashok Holani & Co. and CA Rahul Jangir, prima facie guilty of professional misconduct, leading to the issuance of a Show Cause Notice on December 7, 2022.

Audit Irregularities

The Order highlights several significant shortcomings in the auditors’ performance:

- Failure to Meet Audit Standards: The auditors failed to meet the relevant Standards on Auditing (SA) in various critical aspects, indicating a lack of professional competence to audit a Public Interest Entity (PIE) like LGIL. Their negligence was evident in several areas, and they did not apply professional skepticism and due diligence adequately.

- Misstatement of Profits and Losses: LGIL unilaterally wrote back substantial liabilities as Other Income, resulting in an overstatement of profits by 21% in 2017-18 and an understatement of losses by 1123% in 2018-19 and 283% in 2019-20.

- Flawed Accounting Policy: LGIL adopted a flawed accounting policy for inventory during 2018-19 and 2019-20, not complying with relevant standards. The auditors reported this as a Key Audit Matter (KAM) without conducting a physical inventory count, which was required.

- Lack of Modified Opinion: Despite material and pervasive misstatements, the auditors did not consider a modified opinion as per SA 7051 for the relevant years. They reported these issues through KAM, which was not in compliance with the standards.

- Inadequate Documentation: The auditors failed to obtain sufficient appropriate audit evidence for related party transactions, particularly concerning the utilization of Initial Public Offer (IPO) proceeds.

Penalties and Sanctions

After due investigation and proceedings under Section 132(4) of the Companies Act, 2013, and providing the auditors with an opportunity to present their case, NFRA imposed the following penalties:

- A monetary penalty of Rupees Ten Lakhs on Audit Firm M/s Ashok Holani & Co., the appointed Statutory Auditor.

- A monetary penalty of Rupees Five Lakhs on CA Rahul Jangir, the Engagement Partner.

In addition to the monetary penalties, CA Rahul Jangir is debarred for three years from being appointed as an auditor or internal auditor and from undertaking any audit related to financial statements or internal audit functions and activities of any company or body corporate.

Conclusion

The NFRA’s Order No. 59/2023 serves as a significant regulatory action in response to alleged professional misconduct by statutory auditors. The penalties imposed on M/s Ashok Holani & Co. and CA Rahul Jangir underscore the importance of upholding audit standards and professional integrity in the financial reporting ecosystem. This case highlights the regulatory authorities’ commitment to ensuring transparency, accountability, and compliance within the corporate sector, ultimately contributing to the stability and trustworthiness of India’s financial markets.

*****

Government of India

National Financial Reporting Authority

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. 59/2023 Date: 04.10.2023

In the matter of CA Firm M/s Ashok Holani & Co. and CA Rahul Jangir under Section 132(4) of the Companies Act 2013.

1. This Order disposes of the Show Cause Notice (`SCN’ hereafter) no. NF-23/42/2021 dated 07th December 2022, issued to M/s Ashok Holani & Co., Jaipur, Firm registration no: 009840C (`Firm’ hereafter), an Audit Firm registered with Institute of Chartered Accountants of India (`ICAT’ hereafter) appointed as the Statutory Auditor of Lexus Granito India Limited, Morbi (TOL’ or ‘the company’ hereafter) for the Financial Years (`FY’ hereafter) 2018-19 and 201920 and to its partner CA Rahul Jangir, the Engagement Partner (`EP’ hereafter), ICAI Membership no: 435804 for the FYs 2017-18 to 2019-20 (both are collectively called as `Auditors’ hereafter).

2. This Order is divided into the following sections:

A. Executive Summary

B. Introduction & Background

C. Lapses in the audit

D. Lapses by the Audit Firm

E. Articles of Charges of Professional Misconduct by the Auditors

F. Additional Articles of Charges of Professional Misconduct specific to the Audit Firm

G. Penalty & Sanctions

A. EXECUTIVE SUMMARY

3. The National Financial Reporting Authority (`NFRA’ hereafter) initiated investigation into the professional conduct of statutory auditors of Lexus Granito India Limited, Morbi, Gujarat, for the FYs 2017-18 to 2019-20 under Section 132(4) of the Companies Act 2013 (`Ace hereafter). This was pursuant to information received from the Securities and Exchange Board of India (`SEBI’ hereafter) dated 06.08.2021 about its investigation into the accounting irregularities of the company. Based on further investigation and proceedings under S. 132 (4) of the Act, submissions of the Auditors and preliminary examination of the Financial Statements (TS’ hereafter) and the Audit Files, NFRA found the Auditors prima facie guilty of professional misconduct and issued a Show Cause Notice to the Auditors, M/s Ashok Holani & Co., on 07.12.2022.

4. As is set out in this Order, the Auditors failed to meet the relevant requirements of the Standards on Auditing (`SA’ hereafter) in several significant respects reflecting a serious lack of professional competence to perform audit of a Public Interest Entity (PIE) like the LGIL. In several areas of the audit identified in this Order, the Auditors were grossly negligent and failed Order in the matter of Statutory Audit of Lexus Granito India Limited for the FYs 2017-18 to 2019-20 to apply professional skepticism and due diligence sufficiently and adequately to challenge the management.

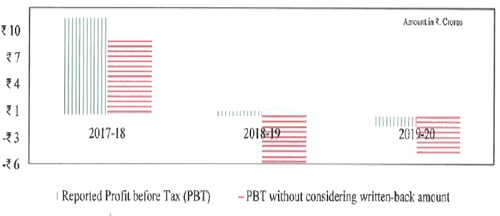

5. NFRA’s investigation found that LGIL had unilaterally written back substantial amounts of its liabilities and treated them as Other Income, which resulted in overstatement of profits by 2.3] crore (21% of the reported figures) in 2017-18 and understatement of losses by89 crore (1123%) in 2018-19 and 3.15 crore (283%) in 2019-20.

6. Although the Inventory constituted more than half of the current assets and therefore was material, the LGIL had, during FYs 2018-19 and 2019-20, adopted a flawed accounting policy to account for the finished goods at the estimated market price (and not at Lower of Cost or Net Realisable Value), therefore not complying with the provision of AS 2. The Auditors merely reported such material non-compliances through Key Audit Matters (`KAM’ hereafter) in the FY 2019-20. The Auditors also failed to attend the physical count of inventory, which was required by the Standards.

7. Despite the presence of material and pervasive misstatements, the Auditors did not consider a modified opinion as per SA 7051 for the FYs 2017-18 to 2019-20, rather they reported these matters through KAM in the FYs 2018-19 and 2019-20, which was not in compliance with SA

8. The Auditors reported matters through KAM without recording any rationale for inclusion of such matters in KAM and without communicating these matters to Those Charged with Governance (`TCWG’, hereafter). There were also differences in the KAMs as documented in the Audit File and as included in the Annual Report submitted to National Stock Exchange (`NSE’ hereafter).

9. The Auditors failed to obtain sufficient appropriate audit evidence for the audit of related party transactions of the company. Approximately 44% of the Initial Public Offer (`IPO’ hereafter) proceeds were paid to one of its related parties, however, no sufficient appropriate documentation of audit procedures for verification of utilisation of IPO proceeds was found in the Audit File, except for a list of payments out of IPO proceeds.

10. The Audit Firm, having been appointed as the statutory auditor for the LGIL failed, in addition to being responsible for the lapses of the audit team, in its responsibility to ensure a proper quality environment for the audit and ensure that its personnel complied with professional standards and regulatory and legal requirements, and that the reports issued by the firm or engagement partners were appropriate in the circumstances.

11. Based on investigation and proceedings under section 132(4) of the Companies Act, 2013 and after giving them opportunity to present their case, we found the Audit Firm and its Engagement Partner, guilty of professional misconduct and impose through this order the following monetary penalties and sanctions that will take effect after 30 days from the date of this Order:

i. Imposition of a monetary penalty of Rupees Ten Lakhs upon the Audit Firm M/s Ashok Holani & Co., the appointed Statutory Auditor

ii. Imposition of a monetary penalty of Rupees Five Lakhs upon CA Rahul Jangir, the Engagement Partner. In addition, CA Rahul Jangir is debarred for three years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate.

B. INTRODUCTION & BACKGROUND

12. The National Financial Reporting Authority is a statutory authority set up u/s 132 of the Act to monitor implementation and enforce compliance of the auditing and accounting standards and to oversee the quality of service of the professions associated with ensuring compliance with such standards. NFRA is empowered u/s 132(4) of the Act to investigate the prescribed classes of companies and impose penalty for professional or other misconduct of the individual members or firms of chartered accountants.

13. The statutory auditors, both individual and firm of chartered accountants, are appointed by the members of a company u/s 139 of the Act. The statutory auditors, including the Engagement Partners and the Engagement team that conduct the audit, are bound by the duties and responsibilities prescribed in the Act, the rules made thereunder, the SAs, including the Standards on Quality Control (`SQC’ hereafter) and the Code of Ethics (the Code), the violation of which constitutes professional misconduct, and is punishable with penalty prescribed u/s 132(4)(c) of the Act.

14. LGIL was dealing in the business of manufacturing and trading of Tiles, and was a small and medium enterprise (SME) listed company at NSE and prepared its financial statements in accordance with the Accounting Standards (`AS’ hereafter) Framework, as it was not mandatory for the LGIL to adopt Indian Accounting Standard (Ind AS) Framework3. M/s Ashok Holani & Co. was appointed for the first time to conduct the statutory audit of LGIL in the FY 2017-18 and the company also got listed at NSE in the same year. CA Rahul Jangir was appointed as the Engagement Partner (EP) for the statutory audit.

15. NFRA took up suo motu investigation into the role of the statutory auditors of Lexus Granito India Limited under section 132(4) of the Act after receipt of a letter dated 06.08.2021 from SEBI pointing out discrepancies in the financial statements of LGIL due to improper writing-back of liabilities and reliance of the Auditors on management for valuation of inventory and utilisation of IPO proceeds.

16. Vide NFRA letter dated 04.02.2022, the Audit Files and other Documents were called from the Auditors, who submitted these on 07.03.2022. NFRA also sent a questionnaire dated 01.09.2022, which was responded to by the Auditors on 01.10.2022.

17. On examination of the Audit Files, it was observed that the audit had prima facie been conducted in disregard of most of the SAs and relevant requirements of the Act. Despite this, the EP had issued an unmodified audit opinion in the Independent Auditor’s Report on behalf of the Firm stating that “…financial statements… give a true and fair view in conformity with the accounting principles generally accepted in India…”.

18. On being satisfied that a sufficient cause existed to take action under sub-section (4) of section 132 of the Act, an SCN was issued to the Firm and to the EP on 07.12.2022, asking them to show cause why action should not be taken against them for Professional Misconduct in the Statutory Audit of LGIL for the FYs 2017-18 to 2019-20. The Auditors were charged with professional misconduct of:

a) failure to disclose a material fact known to them, which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement, where they are concerned with that financial statement in a professional capacity;

b) failure to report a material misstatement known to them to appear in a financial statement with which the auditor is concerned in a professional capacity;

c) failure to exercise due diligence, and being grossly negligent in the conduct of professional duties;

d) failure to obtain sufficient information which is necessary for expression of an opinion, or its exceptions are sufficiently material to negate the expression of an opinion; and

e) failure to invite attention to any material departure from the generally accepted procedures of audit applicable to the circumstances.

19. The reply to the SCN was submitted by the Auditors on 30.01.2023. CA Rahul Jangir and CA Ashok Holani also appeared before the Executive Body of NFRA on 28.03.2023 availing the opportunity of personal hearing offered to them in the During the personal hearing, they reiterated their written submissions as mentioned in their reply dated 30.01.2023.

20. We have perused the audit files and the written and oral responses of the Our findings are discussed in section C and D of this Order.

C. LAPSES IN THE AUDIT

Lapses in evaluation of writing-back of liabilities

21. The Auditors were charged with failure to apply professional skepticism and for inappropriate reporting by the LG1L of extinguishment of liabilities unilaterally without entering into settlement with the counter party (creditors) and subsequent recognition of the amounts involved as ‘Gains’ under ‘Other Income, thereby artificially decreasing the liabilities and inflating the Some examples documented in the audit files corresponding to FYs 2017-18 to 2019-20 are as below:

a) Liabilities of31 crores under Purchases of Raw material were written back on account of poor quality of raw material and excess billing etc.

b) Liabilities of77 crores under Creditors were written back on account of excess billing and ordinary course of business operation etc.

c) Liabilities of66 crores under Capital goods were written back on account of defects and poor operational efficiency of the machines etc.

d) Liabilities of61 crores under Excess amount/ Advance received were written back on account of non-claiming by the customers / lenders etc.

Had these amounts not been written-back to P&L. LGII, would have had significantly lower profits or higher losses, as summarised below:

(Amount in Crores)

| Particular | 2017-18 | 2018-19 | 2019-20 |

| No. of write-back transactions | 60 | 143 | 49 |

| Written-back amount (considered as Gain) | 2.31 | 5.89 | 3.15 |

| Reported Profit before Tax (PBT) | 10.91 | 0.52 | -1.11 |

| PBT without considering the written-back amount | 8.59 | -5.37 | -4.26 |

| Overstatement of profit / Understatement of loss ( % of reported PBT) | 21.16% | 1123.89% | 283.88% |

Overstatement of profits / understatement of losses

The Auditors were charged with non-application of any audit procedures to test the appropriateness of the accounting for these transactions in conformity with the applicable Financial Reporting Framework (`FRF’ hereafter).

22. The Auditors stated that the extinguishment of the liabilities was made by the company commensurate to their trade practices, and the outstanding amounts were written-back after stopping of business dealings with the suppliers or due to trade related matters. The Auditors added that …these were obligations of the company to pay them at their carrying amounts but in actual, the company discharged its obligations at less than their carrying value… so the income from the above was in accordance with Generally Accepted Accounting Principle (`GAAP’ hereafter). As per GAAP ‘Revenues are Inflow of assets or settlement of Liabilities” resulting from operating activities of an entity…”.

The Auditors stated that these were usual business transactions; that there was no evidence of any material misstatement or misrepresentation; and that the management was of the opinion that these dues were no longer payable and therefore retaining of the same could lead to overstatement of liabilities in the FS. The Auditors added that as per accounting Framework for the preparation and presentation of Financial Statements issued in 2000 (`Framework 2000′ hereafter), an obligation may also be extinguished by other means, such as a creditor waiving or forfeiting its rights. In this case, creditors had not claimed their dues for a long time, as no complaint was filed by any of the creditors for such claims, and therefore the same was treated as waiving of their dues.

23. Para 10.2 of AS 294 defines Liability, as a present obligation for the enterprise that arises from past events and settlement of which is expected in an outflow of resources, embodying economic benefits. Further, vide Para 61 of the Framework 2000, liabilities may be settled in a number of ways, for example, by:

a) payment of cash;

b) transfer of other assets;

c) provision of services;

d) replacement of that obligation with another obligation; (4-

e) conversion of the obligation to equity.

An obligation may also he extinguished by other means, such as a creditor waiving or forfeiting its rights.

While the Framework permits extinguishment of an obligation by other means, such as a creditor waiving or forfeiting its rights, there was no documentary evidence in the Audit File of explicit waiver or forfeiting of the rights by the creditors, nor was there any evidence of the Auditors carrying any audit test to confirm such assumptions on the basis of which the liabilities were written back. The Auditors did not show any professional skepticism to question the management for such accounting treatment, which was in contravention of the requirement of AS 29 and the Framework 2000, and which led to the FS for the FYs 2017-18 to 2019-20 being materially misstated. Such misstatement’ had to be identified by the Auditors, who had to ensure6 that the financials of the company were prepared in accordance with the applicable FRF and if not, the Auditors had to duly consider modifying their audit opinion.

24. The Auditors in their written replies dated01.2023, stated that they were restrained by the management from obtaining third-party confirmation “stating counter party may aware (sic) about the liability or may use auditor confirmation as proof of liability in the hooks of company. ” The Auditors stated that they applied alternative audit procedures to assess the risk implication for determining whether management response was reasonable.

This attitude of the Auditors is totally unprofessional. It is expected that the Auditors would show a high level of professional skepticism and be alert to the possibility of mis-statement if restrained by the management from obtaining external confirmations, which is an essential component of independent audit. The Auditors should not only have re-assessed the risks posed by this restraint on their audit and performed alternative audit procedures to mitigate such risk (Para 8 of SA 505′) but also considered this in forming their audit opinion. Instead, we find that the auditors have given unmodified opinion ignoring the restraint imposed by the management on their independent audit. The procedures referred to by the Auditors neither meet the requirements of alternate audit procedures, nor were appropriate or documented. Therefore, we hold the Auditors responsible for carrying out the audit without due diligence and in a perfunctory manner.

25. Non-evaluation of accounting policy and accounting treatment has been viewed seriously by International Regulators as For example, the Public Company Accounting Oversight Board (`PCAOB’ hereafter), the US Regulator9, censured and imposed monetary penalty of $ 47,500 collectively on the firm and respondents in the matter of BDO Auditors, S.L.P. (Finn), Santiago Misstatement as defined by Pam I3(i) of SA 200 “a difference between the amount, classification, presentation or disclosure of a reported FS item and the amount, classification, presentation or disclosure that is required for the item to be in accordance with the applicable FRF.” Sane Figueres, and Jose Ignacio Algas Fernandez (Respondents), for their failure inter alia to report the departure of the company from US GAAP related to the extinguishment of certain liabilities and noted that “…failing to appropriately address PMG’s apparent departure from GAAP including (a) by failing to document any evaluation of the effects of that departure on PMG’s financial statements as a whole and (b) by failing to evaluate whether they should have expressed a qualified or adverse audit opinion…”

In another case, the PCAOB’°, in the matter of BMKR LLP (Firm) and CPA Joseph Mortimer (Respondent), revoked the registration of the Firm for two years; imposed monetary penalty of S 30,000 collectively on the firm and the respondent; and barred the member from being associated with a registered public accounting firm for their failure inter alia to properly evaluate the accounting for certain significant transactions of the company not being in conformity with US GAAP.

Failure in evaluation and attendance at physical verification of Inventory

26. The Auditors were charged with failure to evaluate the accounting policies and valuation of inventories as per Para 11 (c) of SA 315″ and not performing physical verification of inventory as per SA 50112.

27. Para 5 of AS 2 ‘Valuation of Inventories’ requires an entity to value its inventories at lower of

Cost or Net Realisable Value (NRV). Para 26 requires disclosure of the Accounting Policies and Cost Formulae adopted in the measurement of inventory. However, LGIL disclosed that raw material and Work in Progress (WIP) were valued at Cost for the FYs 2017-18 to 2019-20, whereas finished goods were valued at estimated market price in the FYs 2018-19 and 2019-20, and the cost formula used in the valuation of inventory was not disclosed.

28. Para 4 and 7 of SA 501 require the auditor to obtain sufficient appropriate audit evidence regarding existence and condition of inventory by attending the physical count and performing audit procedure to determine actual inventory count, and if it is not practicable to attend physical count of inventory, then auditor shall modify the opinion in accordance with SA 705.

29. The Auditors stated that Measurement and Disclosures for inventory is the responsibility of management and that they had applied due audit procedures to verify and evaluate the process of valuation of raw materials, WI? and finished goods and opined that the raw materials and WI? had been valued at lower of cost or NRV. They stated that their team had audited the stock valuation working sheet for the valuation of raw materials and also checked the bills of the latest purchases of the company to ascertain whether the same was lower than NRV. These documents being voluminous, were kept in digital form rather than as part of the audit file. The Auditors added that, the mere absence of documents from the audit file does not establish violation of the provision of SA 315. Further, every information in respect of valuation and disclosures was available in the FS and they had reported through KAM, so that the stakeholders could get true picture.

The Auditors further stated that they had not only asked the management for cost formulae but also verified that the FIFO method was used for valuation of raw material. The Auditors agreed that mandatory disclosures as per AS 2 required disclosure of the cost formula but the company had failed to do so. However, they did not consider it as a material fact after discussing and verifying with the management and satisfying themselves that the company had properly valued the inventory using the FIFO method.

The Auditors also added that they had carried out examination of records, valuation, disclosures and analytical review procedures and attended the stock count. These documents were further verified and checked with other supporting documents, like inward with purchase invoice, outward with sale invoices, consumption with job sheet, and valuation with purchase invoices. However, they admitted their failure to document the same in the audit file as the data was raw and voluminous.

30 As per AS 2, Inventory includes raw material; work-in-progress and finished goods (para1), and it is to be valued at lower of cost or NRV (para 5); however, for specific scenarios, materials and other supplies held for use in the production of finished goods can be valued at cost (para 24). Para 11(c) of SA 315 requires an auditor to evaluate whether the accounting policies of the entity were consistent with the applicable FRF and when not consistent, it had to be treated as Misstatement as per Para 13(i) of SA 200′. As LGIL had valued inventory of finished goods at estimated market price, the accounting policy for valuation of inventory was not in conformity with AS 2. Such accounting treatment led to overvaluation of the inventory and overstatement of profit. LGIL also failed to disclose the accounting formula used in the valuation of inventory. Inventory constituted more than half of the current assets and therefore was a material component. We do not find any audit evidence in support of the claim of the Auditors that they had checked whether valuation of the inventory was lower of the cost or NRV and therefore we hold the Auditors responsible for failure to disclose the misstatement resulting from such accounting treatment. Merely reporting of the improper accounting of finished goods through KAM was not appropriate or adequate, as discussed in Para 42 & 43 of this Order.

31. The contention of the Auditors that mere absence of any documents from the audit file did nor indicate that they had violated the provisions of SA 315, is not correct. Para S of SA 230′4 states that the objective of the auditor is to prepare documentation that provides sufficient and appropriate record of the basis for the auditor’s report; and evidence that the audit was planned and performed in accordance with SAs and applicable legal and regulatory Further, Para 14 of SA 230 requires the auditors to assemble all the audit documentation in the audit file within 60 days from the date of the auditor’s report. The Auditors had averred in their affidavit dated 05.03.2022 that they were submitting complete audit files and, therefore their later submission of additional documents viz., stock valuation sheet/ calculation sheet etc. on 30.01.2023 are deemed afterthought and not accepted.

32. As admitted by the Auditors, we also did not find any audit documentation regarding the physical count of the inventory. We note that SA 501 mandates an auditor to attend physical count of the inventory (para 4) and if it is impracticable’ to attend the physical count and not possible to apply alternative audit procedures, then the auditor is required to modify the audit opinion (para 7). In the case of LGIL, inventory constituted85% of the current assets in FY 2017-18, 65.10% in FY 2018-19 and 65.53% in FY 2019-20, making it a significantly material item for the Auditors to attend its physical count, but they failed to do the same. As per section 143 (9) of the Act, it is the statutory duty of the auditor to comply with the SAs and Para 18 of SA 200 also requires the auditor to comply with all the SAs relevant to the audit. Failure to attend the physical count of the inventory was a serious non-compliance of SA 501 and the provisions of the Act.

33. Considering the above, the charge that the Auditors did not comply with the provisions of SA 200, 230, 315 and 501 to obtain sufficient appropriate audit evidence for the audit of the inventory, is established.

34. Lapses in the audit of inventory have been viewed seriously by International Regulators as well. For example, the PCA0B16, in the matter of W.T. Uniack CPA, P.C. (firm) and William T. Uniack, CPA (respondent), revoked the firm’s registration and barred the respondent from being an associated person of a registered public accounting finn for their failure inter alia to obtain sufficient appropriate audit evidence and exercise due professional care and professional skepticism in the audit of inventory. The PCAOB noted that “An auditor who issues an audit opinion without employing procedures to observe inventories has the burden of justing the opinion expressed. Moreover, in such circumstances, tests of the accounting records alone will not be sufficient for [the auditor] to become satisfied as to quantities; it will always be necessary for the auditor to make, or observe, some physical counts of the inventory and apply appropriate tests of intervening transactions.”

Inappropriate reporting of matters through KAM

35. The Auditors were charged with reporting of the matters through KAM without obtaining sufficient appropriate audit evidence about the matters mentioned in KAM, and without making prior communication with the TCWG in the FYs 2018-19 and 2019-20. The SCN also alleged that there was difference in reporting of KAM in the Auditor’s report (FY 2018-19) as documented in the audit file and as available with NSE, as detailed below:

| Sr. No. | KAMs as per the Report available with NSE | KAMs as per the Report documented in the audit file |

| 1 | Default in payment to lenders | Default in payment to lenders |

| 2 | Unilateral extinguishment of trade payables | Written-off of Trade payables |

| 3 | Evaluation of uncertain tax positions | Valuation of inventories |

| 4 | Recoverability of Indirect tax receivables | – |

36. The Auditors replied that they had discussed their key findings (valuation of finished goods at market price, non-payments to the banking institutions on timely basis, delay in payments of statutory dues and write back of significant payable amounts etc.) with TCWG, had applied additional audit measures to mitigate the risk arising due to these findings, and, as these findings were significant, therefore they had included them in the KAM.

37. As per Para 17 and 18 of SA 701, the auditor shall communicate with TCWG those matters that are determined by him as KAM and document the same. As per Para 12, the auditor shall not include those matters in KAM on account of which he is required to modify the opinion. However, we do not find any working in the audit files in respect of inclusion of the matters in the KAM, nor communication of these matters with TCWG prior to their inclusion in the KAM. Therefore, the Auditors were not in compliance with the requirements of SA 701.

38. While responding to the charge of two different reporting through KAM, the Auditors stated that `uploading of annual report with the stock exchanges is the responsibility of the LGIL, not of the company auditor and the audit report available on NSE are uploaded by the LG1L. We were not aware that the company had re-drafted KAM and uploaded the same.’

When enquired by NFRA with the company, replied vide email dated 14.09.2023 that there was a failure on the part of the company as there was error on printer side while composing the Annual Report for better presentation. LGIL said that the error was unintentional and regretted the same.

I however, we observe that this does not appear to be a printing error, as there were differences not only in the number of the KAMs issued, but also there were differences in the subject matter of KAMs,

39. Para 13 of SA 720″ requires an auditor to determine through discussion with the management, the documents that comprise the annual report; the entity’s planning and timing of the issuance of such documents; make appropriate arrangements with the management to obtain the final version of the documents comprising the annual report in a timely manner and, if possible, prior to the date of the auditor’s Therefore, the reply of the Auditors attributing the errors to the company also shows ignorance of SA 720 and its eventual non-compliance.

Forming inappropriate Audit Opinion

40. The Auditors were charged with issuing of unmodified opinion despite the presence of below mentioned material misstatements, in the FS for the FYs 2017-18 to 2019-20.

41. As per their reply dated01.2023, the Auditors stated that “in case of valuation of inventory, we accept that reporting should not made in Key Audit Matters but report should be moded.” However, in case of writing back of liabilities, the Auditors justified inclusion in the KAM stating that such writing-back was in accordance of regular practice of the LGIL and since LG1L will not be paying these liabilities in future, carrying in the books will lead to overstatement of liabilities.

42. Para 6 of SA 705 prescribes the following situations where modification to the Auditor’s opinion is required:

a) The auditor concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement; or (Ref: Para. A2-A7)

b) The auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement. (Ref A8-Al2)

Para A3 and A4 of SA 705 state that a misstatement in the FS will arise when the selected accounting policies are not consistent with the applicable FRF. Para Al2 of SA 705 states that, examples of inability to obtain sufficient appropriate audit evidence include when the management prevents the auditor from requesting external confirmation of specific account balances.

43. We have observed earlier that the accounting policy regarding unilateral extinguishment of liabilities and valuation of finished goods was not in accordance with the FRF, and the Auditors were restrained from obtaining external confirmation in respect of extinguishment of liabilities. Therefore, the Auditors could not conclude that they had obtained sufficient appropriate audit evidence to state that the FS were free from material misstatements and to issue unmodified opinion, which they did.

Non-evaluation of utilisation of IPO proceeds

44. The Auditors were charged with not having sufficient appropriate audit evidence for reporting in the Companies (Auditor’s Report) order, 2016 (`CARO’ hereafter) regarding utilisation of IPO proceeds for the declared purpose. LGIL had raised Z 25.92 crores through IPO in August 2017 for working capital requirements and general corporate purposes as disclosed in the Red Herring Prospectus. Since the company was planning an IPO, there could be instances of higher risks associated with overstatement of revenue / assets or understatement of expenses / liabilities. Accordingly, the Auditors were required to evaluate the books of accounts of the company with professional skepticism during the year of IPO, including proper assessment of utilisation of the proceeds from IPO and report the same in CARO.

45. The Auditors replied that they had obtained and checked the complete list of payments, containing names of the parties; purpose of the payments; amounts paid; date of such payments; and verified the same with the bank account to minimize the risk to an acceptable level. Thereafter they had verified the transactions by reviewing the ledgers along with bills and invoices. LGIL had made payments of approx. Z 9.30 crores (44.29% of the IPO proceeds) to one of its related parties viz., M/s. Kartik Industries for supply of coal, therefore they had applied additional audit procedures to check this transaction viz., approval of Audit Committee minutes, assessment of whether the transaction was at market rates or whether it involved granting of any undue benefits. As they did not find anything contrary after applying all these audit procedures, they did not resort to external confirmation. The Auditors stated that “So mere asking and verffring from the receiver whether you receive the payment or not, we think this does not make any importance as with the detailed checking, we were in opinion that there is no material misstatement.”

46. The audit procedures mentioned by the Auditors in their reply to the SCN is not evidenced from the Audit File. Mere obtaining a certified copy from the management regarding utilisation of the IPO proceeds, does not relieve the Auditors from the responsibility of performing the required audit procedures. There is no evidence in the Audit File that the auditors had performed risk analysis of potential misstatements before the issuance of IPO (over statement of revenue / assets or understatement of expenses / liabilities to present rosy picture to the investors) and after realization of the IPO proceeds (misappropriation of the proceeds for purposes other than the declared purpose). The Auditors did not show the skepticism expected from them while reporting under CARO 2016 about proper utilization of money raised from the IPO, especially in light of the observed instances of artificial inflation of profits and reduction of liabilities by unilateral write-back of outstanding payables, and significant payments (44.29% of the IPO proceeds) to the related party from the IPO proceeds. These potential risks were not assessed by the Auditors to identify and assess the risk of material misstatements by designing and performing enhanced audit procedures to mitigate such assessed risk (Para 25 and 28 of SA 315). We did not find audit documentation by the Auditors addressing these risks, nor any assessment of the utilisation of IPO proceeds, except the list of payments made out of IPO proceeds.

47. Therefore, we hold the Auditors responsible for not performing the due audit procedures, for failure to obtain sufficient appropriate audit evidence for reporting under CARO 2016 about proper utilisation of IPO proceeds, and for their failure to comply with SA 315.

Non-evaluation of Related Parties Transactions

48. The Auditors were charged with failure to perform necessary audit procedures to verify and report the Related Party Transactions (`RPT’ hereafter). LGIL had reportedly purchased coal amounting to I I crores and 20.51 crores in the FYs 2017-18 and 2018-19 respectively from one of its related parties. These were substantial amounts, being 28% & 38% of the expenditure under `power & fuel’ in respective years. As per sections 177, 185, 186 and 188 of the Act, the Auditors had to confirm whether the approval for such transactions had been given by the Audit Committee Board of directors Shareholders and whether these transactions were in the ordinary course of business and on arm’s length basis. From the audit files, we note that the Auditors failed to do so and were charged with non-compliance of the provisions of SA 550.

49. The Auditors replied that the resolution of the Audit Committee had been obtained by them and the ET had discussed all audit matters including They had also obtained list of related parties over mail, kept the ledger accounts of the same in the digital form, and compared the RPT with the previous year, and checked its being on arm’s length prices. They stated that the major documents of the audit were kept in the digital form rather than in the audit file for better accessibility, due to which NFRA could not verify the same.

50. SA 550k deals with auditor’s responsibilities in respect of related parties. There are specific accounting and disclosure requirements for related party relationships, transactions and balances to enable users of the financial statements to understand their nature and actual or potential effects on the FS (Para 3). The auditors have the responsibility to perform audit procedures to understand, identify, assess and respond to the risks of material misstatement arising from the entity’s related party relationships and transactions, as fraud may easily be committed through related parties (Para 5). There is emphasis on the susceptibility to fraud risk requiring documentation of discussion among the Engagement Team (`ET’ hereafter) addressing such risk (Para 12) and requirement of enquiry with the management regarding the identification of related parties, including changes from the prior period; nature of the relationships between the entity and these related parties; the type and purpose of the transactions with these related parties during the period (Para 13). The auditor is also required to obtain sufficient appropriate audit evidence to verify that related party transactions are on an arm’s length basis (Para 24) and obtain management representation letter regarding identification of related parties and RPTs and that management have appropriately accounted for and disclosed the RPT in the financial statements as per applicable framework (Para 26).

We do not find any audit documentation by the Auditors in respect of verification of the RPTs, except for obtaining the list of Related Parties and their transactions. It is also observed that the Auditors arc frequently mentioning of keeping the data in the digital files, which could easily be made part of the audit files, but the same was not done. The Auditors while replying to the SCN submitted minutes of meeting of the Audit Committee for three FYs and price comparison statement of purchase of coal from the related party with the price from the other parties etc. as a token of their performance in accordance with SA 550. This is not evidenced from the audit files, and therefore is deemed an afterthought, as Para 8 and 14 of SA 230 requires the assembling of such documents in the audit file within 60 days after the date of the auditor’s report, which the Auditors failed to do.

51. Notwithstanding the above, we observe that the minutes of the meeting of Audit Committee dated 10.04.2019, submitted by the Auditors at the time of reply to the SCN, do not pertain to LGIL but another entity viz., Lexus Granito (India) Private Limited. The dates of the meetings (02.05.2017, 30.05.2018 and 10.04.2019) mentioned in the minutes were not reported by LGIL in its respective annual reports. Therefore, the veracity of such Audit Committee meetings cannot be ascertained. Therefore, we are unable to attach any importance to the submissions made by the Auditors as sufficient appropriate audit evidence and conclude that the Auditors failed to perform audit of RPT in accordance with SA 550.

52. Auditor’s failure to obtain sufficient appropriate audit evidence in respect of RPTs has been viewed seriously by the International Regulators as well. For example, PCA0B19, in the matter of Cheryl L. Gore, CPA and Stanley R. Langston, CPA (Respondents), barred the respondents from being associated with a registered public accounting firm and imposed monetary penalty of $30,000 collectively for their failure inter alia to obtain sufficient appropriate audit evidence with respect to related party transactions.

In another case, PCAOB20, in the matter of Yichien Yeh, CPA (Firm) and Yichien Yeh (Respondent), revoked the firm’s registration and barred the respondents from being associated with a registered public accounting firm and imposed monetary penalty of $10,000 collectively for their failure inter alia to obtain sufficient appropriate audit evidence with respect to related party transactions.

Non-implementation of Quality Control Measures

53. The Auditors were charged with (i) failure to document the compliance with the independence requirements as per Para 11 of SA 22021, which requires an EP to form a conclusion on compliance with the independence requirements and (ii) violating Para 19(a) of SA 220 which requires an EP to determine the appointment of EQCR for the statutory audit of a listed company, and (iii) failure to document his conclusions on compliance with the independence requirements and consultations undertaken during the course of audit engagement as per para 24.

254. The Auditors replied that their firm had designated Senior Partner Mr. Ashok Holani as EQCR for the audit of LGIL; that matters concerning the audit of LGIL were discussed in meeting of partners and professional staff; and that the work done in audit is left for review of Senior Partners. For compliance of independence requirements, they replied that the Firm’s personnel are prohibited from having a financial or business relationship with entities of which a list is prepared and made available to the concerned personal from time to time so they may evaluate their independence. Vide an email dated 08.08.2023, CA Ashok Holani has also confirmed that he was the EQCR for the statutory audit of LGIL for the FYs 2017-18 to 2019-20.

55. We did not find any workpaper in the audit file to establish that the personnel of the firm had disclosed their financial interest in the company to ensure their independence.

56. As per Para 60 of SQC 1, Audit firms are responsible for establishing policies and procedures for quality control review. SQC 1 requires appointment of an EQCR for all listed entities and set out criteria for other entities. The quality policy of the firm was however silent about the same.

57. We also did not find any audit documentation establishing that CA Ashok Holani was appointed sip EQCR. Name of CA Ashok Holani has been referred at only one of the workpapers named `Activity Log’ at page no. 3.1 of the audit files, however it does not establish his appointment as EQCR. The EQCR is duty bound to document his work as per Para 25 of SA 220, however we did not find any working of EQCR in the audit files, establishing performance of his work during the audit. Therefore, the Auditors’ failure in implementation of quality control measures and ensuring of independence is established.

58. Failure to appoint an EQCR has been viewed seriously by International Regulators as well. For example, PCA0B22 in the matter of Robert C. Duncan Accountancy Corp. (Firm) and Robert C. Duncan, CPA (Respondent), revoked the firm registration and barred the respondent from being associated with a registered public accounting firm and imposed monetary penalty of $30,000 for their failure to obtain an engagement quality control review and issuance of Audit report without

D. LAPSES BY THE AUDIT FIRM

59. In addition to the lapses in the audit performed by the Auditors, discussed in the forgoing paragraphs of this Order, the Audit Firm was specifically charged with failure to establish and maintain a system of quality control within the Firm and to fulfil its duties prescribed under section 143 of Companies Act and SQC 1. The powers and duties of the statutory auditors have been prescribed u/s 143 of the Act. The duties include making their report to the members of the company after taking into account the provisions of the Act, the accounting and auditing standards (subsection 2); stating in report and expressing opinion on matters listed in subsection 3; stating the reasons, if any of the matters required to be included in the audit report under this section is answered in the negative or with a qualification (subsection 4); complying with the auditing standards (subsection 9); and reporting to the Central Government matters which he believes involve the offence of fraud (subsection 12). Para 2 of SA 220 and Para 3 of SQC 1 stipulate that Quality Control Systems, Policies and Procedures are the responsibility of the Audit Firm that has an obligation to establish and maintain a system of quality control to provide it with reasonable assurance that:

a) The firm and its personnel comply with professional standards and regulatory and legal requirements; and

b) The reports issued by the firm or engagement partners are appropriate in the circumstances.

Para 5 of SQC I makes it applicable to all the firms. SQC 1 establishes standards and provides guidance regarding a firm’s responsibilities for its system of quality control for audits and reviews of historical financial information, and for other assurance and related service engagements.

60. The Audit Firm responded that “our, firm is a small firm and had four partners in the FY 201718, 2018-19 and three partners in the FY 2019-20. The .firm has its SQC 1 policy, which is applicable to all personnel working in the firm. The firm ensure that the firm and its personnel complied with the professional standards, regulatory, legal requirements and the audit reports issued by the firm or engagement partners are appropriate in the circumstances.”

61. Statutory Audits are performed by the EP on behalf of the Audit Firm appointed as statutory auditor under section 139 of the Act. The responsibility of the audit firm is to ensure its systems and processes are conducive to a high-quality audit and that it is in compliance with the laws and Professional Standards. The audit reports are signed on behalf of the audit firm and therefore, the audit firm remains responsible for all the acts of omissions and commissions by the EP as well as for violation of duties and responsibilities specifically required of the audit firm.

62. M/s Ashok Holani & Co. was the statutory auditor of LGIL for the FYs 2017-18 to 2019-20 and, as discussed above, the Audit Firm and the EP have made departures from the SAs and the Companies Act, 2013 and have been grossly negligent in performing the audit of LGIL, by placing blind reliance on the assertions of the management in accounting of unilateral extinguishment of liabilities, valuation of inventory, verification of the utilisation of IPO proceeds and RPTs etc. The contention that they are a small audit firm, cannot be accepted as auditors are duty bound to comply with the requirements of the statutes to safeguard the interest of public. Therefore, in addition to the EP, we hold the Audit Firm also responsible for the lapses discussed in the preceding paragraphs.

63. Failure to establish an effective quality control policy by the audit firm has been viewed seriously by international regulators as well. For example, PCAOB23, in the matter of Deloitte LLP, censured the firm and imposed penalty of $350,000 on the Firm for its failure to establish, implement, and communicate appropriate quality control policies and procedures to provide the Firm with reasonable assurance that the work performed by engagement personnel complied with applicable professional standards, regulatory requirements, and the Firm’s standards of quality.

In another case, PCAOB24, in the matter of K G Somani & Co. LLP (the Firm) and Anuj Somani, censured the firm and Anuj Somani, and imposed penalty collectively of $175,000 for its failure inter alia to perform all necessary audit procedures, and its violations of PCAOB standards concerning the performance, supervision, documentation of the audit, and quality control standards.

E. ARTICLES OF CHARGES OF PROFESSIONAL MISCONDUCT BY THE AUDITORS

64. As discussed in the foregoing paragraphs, the Auditors have made a series of serious non-compliances of the Standards on Auditing and the Law in their conduct of the audit of LGIL for the FYs 2017-18 to 2019-20. The Auditors had issued unmodified opinion on the Financial Statements despite existence of material misstatements in FS. The poor quality of Audit, the cover up in terms of submission of additional documents that did not exist in Audit File, incomplete documentation and attempt to mislead through untenable replies, further compound the professional misconduct on the part of the Auditors. Based on the foregoing discussion and analysis, we conclude that the Auditors committed Professional Misconduct in terms of section 22 of the Chartered Accountants Act 1949 (`CA Act’ hereafter) as amended from time to time, as defined under Section 132 (4) of the Companies Act 2013, and as detailed below:

i. The Auditors committed professional misconduct as defined by clause 5 of Part I of the Second Schedule of the CA Act, which states that an auditor is guilty of professional misconduct when they ‘fails to disclose a material fact known to him which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where he is concerned with that financial statement in a professional capacity”. This charge is proved as the Auditors failed to disclose in their report, the material non-compliances by the Company as explained in para 21 to 34 above.

ii. The Auditors committed professional misconduct as defined by clause 6 of Part I of the Second Schedule of the CA Act, which states that an auditor is guilty of professional misconduct when they “fails to report a material misstatement known to him to appear in a financial statement with which he is concerned in a professional capacity”. This charge is proved as the Auditors failed to disclose in audit report the material misstatements made by the Company as explained in para 21 to 34

iii. The Auditors committed professional misconduct as defined by clause 7 of Part I of the Second Schedule of the CA Act, which states that an auditor is guilty of professional misconduct when they “does not exercise due diligence or is grossly negligent in the conduct qf his professional duties”. This charge is proved as the Auditors failed to conduct the audit in accordance with the SAs and applicable regulations in many critical areas of the audit and failed to report non-compliances made by the Company, as explained in para 21 to 58

iv. The Auditors committed professional misconduct as defined by clause 8 of Part I of the Second Schedule of the CA Act, which states that an auditor is guilty of professional misconduct when they ‘fails to obtain sufficient information which is necessary for expression of an opinion or its exceptions are sufficiently material to negate the expression of an opinion”. This charge is proved as the Auditors failed to modify the report in respect of material misstatements in the financial statements arising from unilateral extinguishment of liabilities to overstate the profits or to understate the losses and failed to obtain SAAE in respect of critical areas such as RPTs, Inventory as required by the SAs and applicable regulations, as explained in the para 21 to 58 above.

v. The Auditors committed professional misconduct as defined by clause 9 of Part 1 of the Second Schedule of the CA Act, which states that an auditor is guilty of professional misconduct when they ‘fails to invite attention to any material departure from the generally accepted procedure of audit applicable to the circumstances”. This charge is proved since the Auditors failed to conduct the audit in accordance with the SAs as explained in the para 21 to 58 above.

F. ADDITIONAL ARTICLES OF CHARGES OF PROFESSIONAL MISCONDUCT SPECIFIC TO THE AUDIT FIRM

65. In addition to above, the Audit Firm has committed Professional Misconduct as defined in Section 132 (4) of the Act read with section 22 of the CA Act, as amended from time to time, by failing to exercise due diligence and being grossly negligent in the conduct of professional duties in respect of matters explained at Section D above and thus, violated the SAs mentioned in the foregoing paragraphs and SQC

66. Therefore, we conclude that all the charges of professional misconduct in the SCN stand proved based on the evidences in the Audit File, the Audit Reports issued by the EP on behalf of the Firm, the submissions made by the Auditors and the Financial Statements of LGIL for the FYs 2018-19 and 2019-20.

G. PENALTY & SANCTIONS

67. It is the duty of an auditor to conduct the audit with professional skepticism and due diligence and report his opinion in an unbiased manner. Statutory audits provide useful information to the stakeholders and public, based on which they make their decisions on their investments or do transactions with the public interest entity’s. Without a credible audit, Users of Financial Statements would be handicapped. The corporate governance system would fail and result in a breakdown in trust and confidence of investors and the public at large if the auditors do not perform their job with professional skepticism and due diligence and adhere to the standards.

68. Section 132(4)(c) of the Companies Act, 2013 provides for penalties in a case where professional misconduct is proved. The seriousness with which proved cases of professional misconduct are viewed, is evident from the fact that a minimum punishment is laid down by the law as below:

(A) imposing penalty of— (I) not less than one lakh rupees, but which may extend to five times of the fees received, in case of individuals; and (II) not less than ten lakh rupees, but which may extend to ten times of the fees received, in case of firms; and

(b) debarring the member or the firm from—(I) being appointed as an auditor or internal auditor or undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate; or (II) performing any valuation as provided under section 247 of the Act, for a minimum period of six months or such higher period not exceeding ten years as may be determined by the National Financial Reporting Authority.

69. The Auditors in the present case placed blind reliance on the assertions of the management relating to accounting of unilateral extinguishment of liabilities, valuation of inventory, verification of the utilisation of 1PO proceeds and RPTs, instead of discharging their statutory duty to protect public interest by exercising professional skepticism and questioning the management’s decisions for material misstatements in the Financial Statements. The Auditors abdicated their specific responsibility provided in the SAs of physical verification of inventory. They failed to perform the required audit procedures with due professional skepticism and report the material misstatement. The Firm, M/s Ashok Holani & Co. has also failed to exercise appropriate control and monitoring of the work of the EP and the ET during the audit engagement and has abdicated its responsibility to ensure audit quality as per professional standards. Under the circumstances, we proceed to impose sanctions, keeping in mind the deterrence, proportionality, and the signaling value of the sanctions.

70. As per information furnished by M/s Ashok Holani & Co. vide email dated 27.04.2023, the statutory audit fees of LGIL for the FYs 2017-18, 2018-19 and 2019-20 was, and respectively. Total professional fees received by the audit firm during the FYs 2017-18, 2018-19 and 2019-20 was and respectively. Total professional fees earnec.1 bile EP, CA Rahul Jangir during the FYs 2017-18, 2018-19 and 2019-20 was and respectively.

71. Considering the fact that professional misconducts have been proved and considering the nature of violations and principles of proportionality, we, in exercise of powers under Section 132(4)(c) of the Companies Act, 2013, order:

i. Imposition of a monetary penalty of Rupees Ten Lakhs upon the Audit Firm M/s Ashok Holani & Co., the appointed Statutory Auditor

ii. Imposition of a monetary penalty of Rupees Five Lakhs upon CA Rahul Jangir, the Engagement Partner. In addition, CA Rahul Jangir is debarred for three years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate.

72. This Order will become effective after 30 days of its issue.

Sd/-

(Dr Ajay Bhushan Prasad Pandey)

Chairperson

Sd/-

(Praveen Kumar Tiwari)

Full-Time Member

Sd/-

Full-Time Member

(Smita ./hingran)

Authorised for issue by the National Financial Reporting Authority,

Date: 04.10.2023

Place: New Delhi

(Vidhu Sood)

Secretary NFRA

Copy To: –

Secretary, Ministry of Corporate Affairs, Government of India, New Delhi.

Securities and Exchange Board of India, Mumbai.

Secretary, Institute of Chartered Accountants of India, New Delhi.

Lexus Granito (India) Limited

1T-Team, NFRA for uploading the order on the website of NFRA.

Notes

1 SA 705 ‘Modifications to the Opinion in the Independent Auditor’s Report’

2 SA 701 ‘Communicating Key Audit Matters in :he Independent Auditor’s Report’

3 Proviso to sub rule 1 of rule 4 of Companies (Indian Accounting Standard) Rules, 2015

4 AS 29 ‘Provisions, Contingent Liabilities and Contingent Assets’

6 As per Para 3 of SA 200, statutory auditor possesses a responsibility to enhance the degree of confidence of the users in the FS by expressing an opinion on the FS that whether the PS are prepared, in all material respects, in accordance with the applicable FRF.

7 SA 505 ‘External Confirmations’

8 Para A8 to A10 read with para 8 of SA 505.

9 PCAOB Release No. 105-2017-039

10 PCAOB Release No. 105-2022-003

11 SA 315 ‘Identifying and Assessing the Risk of Material Misstatement through Understanding the Entity and its Environment’

12 SA 501 ‘Audit Evidence-Specific Considerations for Selected Items’

13 SA 200 ‘Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing’

14 SA 230 ‘Audit Documentation’

15 Para A 12 of SA 501 provides reference on impracticality of auditors for physical verification of inventory.

16 PCAOB Release No. 105-2017-028

17 SA 720 ‘The Auditor’s Responsibilities Relating to Other Information’

18 SA 550 ‘Related Parties’

19 PCAOB Release No. 105-2021-020

20 PCAOB Release No. 105-2021-011

21 SA 220 ‘Quality Control for an Audit of Financial Statements’

22 PCAOB Release No. 105-2022-010

23 PCAOB Release No. 105-2021-014

24 PCAOB Release No. 105-2023-020

25As defined in Rule 3 of NFRA Rules 2018

NFRA is becoming increasingly hostile towards practicing chartered accountants.