MANAGERIAL PERSONNEL APPOINTMENT & REMUNERATION – A DETAILED COGNIZANCE IN THE LIGHT OF COMPANIES (AMENDMENT) ACT, 2017

This Article portrays detailed analysis on Managerial Personnel appointment and remuneration under the purview of Companies Act, 2013 including Companies (Amendment) Act of 2017. The Company Amendment Bill, 2017 passed by Lok Sabha on July 27, 2017; by Rajya Sabha on December 19, 2017 and received the assent of President on January 3, 2018. It has always been burdensome for the Corporate to pay the remuneration (exceeding certain limits as prescribed under the 2013 Act) to the Managerial Personnel in the occasion of Company which has incurred loss or profits are inadequate. Now provision under the 2017 Act has made it clear, flexible and generous to make the payment after complying with its provisions without Central Government approval.

Page Contents

- 1. Appointment of Managerial Personnel

- 2. Appointment of Key Managerial Personnel (KMP)

- 3. Managerial Personnel Remuneration

- 4. Relaxation In Managerial Remuneration For Certain Class Of Companies

- 5. Managerial Remuneration In Case Of No Profits/ Profits Are Inadequate

- 6. Can A Director Who Is Managing Director/ Whole Time Director Of A Company Receive Remuneration Or Commission From Its Holding Company Or Subsidiary Company?

- 7. Certain Disclosure by The Independent Auditors In Their Reporting

- 8. Managerial Remuneration Payable in Special Circumstances In Case Of Nil or In-Adequate Profits (Section III of Part II of Schedule V)

- 9. Perquisite Not Included In Managerial Remuneration (Section IV of Part II of Schedule V)

- 10. Checklist – Appointment of Managerial Personnel (Managing Director/ WTD Manager)

- 11. Conclusion

1. Appointment of Managerial Personnel

An individual can become Managing Director only if he is a director and is subordinate to Board of Directors. A Company shall not appoint Managing Director and Manager at same time due to the reason that both are encumbered with whole or substantially whole of Management powers of the Company and a Manager can’t again be delegated with such powers at same time. Managerial Personnel here means Managing Director, Whole Time Director and Manager. A Company (be it a Public or Private Company) shall not appoint Managerial Personnel for a term of more than 5 years and is eligible for reappointment. The vacation of Director’s office results into cessation of office of the Managing Director.

First proviso to Sec 196(3) (a) of the 2013 Act provides that a person who has attained the age of 70 years can be appointed as Managerial Personnel only after obtaining shareholder’s approval by Special Resolution. But as per the 2017 Act, a new second proviso has been inserted to the said Section that if for any reason no Special Resolution is passed, then such person may be appointed only after passing ordinary resolution and with the Central Government approval.

Appointment of Managerial Personnel including remuneration shall be approved by the Board of Directors followed by shareholders approval at next General Meeting. If terms and conditions of such appointment are in variance with Part I of Schedule V, Central Government approval is required (new amendment in Sec 196 (4)). But approval of Central Government is abandoned and replaced with Member’s Special Resolution for paying the remuneration which are in variance with Part II of Schedule V to the 2017 Act.

Return of Managerial Personnel Appointment in e-form MR-1 shall be filed within 60 days from the date of such appointment. Such return is not required for Company Secretary, CEO and CFO appointment w.e.f June 6, 2016.

Exemption from provisions of the Sec 196 of the 2013 Act:

| Sl. No. | Type of Company | Exemption Provision | Remarks |

| 1 | Private Company | Sec 196 (4) & (5) | E-Form MR-1 is not required to be filed with RoC. But E-form DIR-12 required for change in designation. |

| 2 | Government Company | Sec 196 (2) (4) & (5) |

* Central Government in exercise of power conferred under Sec 406 of the Companies Act, 2013 and in the public interest, issued the notification dated June 5, 2015 as amended from time to time, exempting certain sections to certain type of Companies.

2. Appointment of Key Managerial Personnel (KMP)

As per Sec 2 (51) of the 2013 Act, KMP in relation to the Company means

i. CEO or Managing Director or Manager;

ii. Company Secretary;

iii. Whole Time Director;

iv. CFO;

v. Such other officer not more than one level below the directors who is in whole time employment, designed as KMP by the Board; (This clause inserted vide the 2017 Act)

vi. Such other officer as may be prescribed

* Every KMP shall be appointed by Board resolution containing terms and conditions.

Further, as per notified Rule 8A of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, a company other than a company which is required to appoint a whole time key managerial personnel as discussed above and which is having paid up share capital of Rs. 5 Crores or more shall have a whole time Company Secretary.

A Company shall not appoint or re-appoint an Individual as chairperson and as Managing Director or CEO at same time unless its Article of Association provides for the same and Company does not carry on multiple businesses. But company engaged in multiple businesses can appoint the same Individual as the Chairperson who is also Managing Director or CEO if CEO’s have been appointed for each separate business. Recently the Indian Stock Market regulator, SEBI (Securities and Exchange Board of India) has approved the recommendations of Shri. Uday Kotak Committee on Corporate Governance for listed companies wherein recommendations inter-alia include splitting up the role of Chief Executive Officer/Managing Director and Chairperson for the top-500 listed firms with effect from April 1, 2020.

3. Managerial Personnel Remuneration

As per Section 2(78), Remuneration means any money or its equivalent given or passed to any person for services rendered for him and includes perquisites as defined under Income tax Act, 1961.

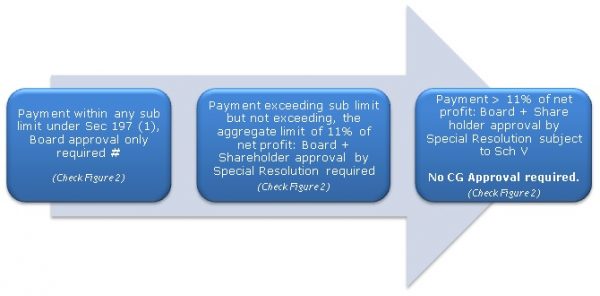

Section 197 deals with the Remuneration payable to Directors including Managerial Personnel. The Section applies only to Public Companies and hence private Companies are free to pay remuneration at any rate to such directors in case of adequacy or inadequacy of profits. The Company may pay the remuneration to the managerial personnel exceeding total limit of 11% of net profits (computed as per Sec 198 of the 2013 Act and Director’s remuneration deducted should be added back to the gross profit) with the approval of members at the general meeting. The proviso which required Central Government approval exceeding the said limit has omitted. But new provision has been inserted through third proviso to the section that if company defaulted in the payment of dues to any bank or public financial institution or non convertible debenture, their prior permission shall be obtained before getting approval of members in the general meeting.

4. Relaxation In Managerial Remuneration For Certain Class Of Companies

The 2013 Act read with Rule 7 of the respective rules has given relaxation to the companies other than listed companies and its subsidiaries for paying managerial remuneration without Central Government approval (ie., beyond ceiling limit in Section II, Part II of Schedule V) in the event of no profit or inadequate profit subject to the following conditions:

a. Approval of Nomination and Remuneration Committee (where Companies required to constitute such Committee under Section 178 of the Act) followed by Board resolution with clear reason recorded in writing for payment of remuneration beyond the limit.

b. Company has not made any default in repayment of any of its debts including public deposit or debentures or interest payable thereon and dividend on preference shares for a continuous period of 30 days in the preceding financial year.

c. The shareholders approval by special resolution at its general meeting for managerial remuneration for a period not exceeding 3 years.

d. Explanatory Statement to the notice calling the general meeting shall contain information referred to in Sch V (ie., sub clause (iv) of 2nd Proviso to Clause (B) of Section II of Part II of Sch V of the 2013 Act)

e. Has filed the financial statement and Annual Return which are due to be filed with Registrar of Companies.

(* In second proviso to Sec 197 (1) the 2017 Act – the term ‘Special Resolution’ was inserted in the place of ‘Ordinary Resolution’).

# As per Part III of schedule V, the appointment and remuneration referred to in Part I and II shall be subject to the approval of members at the general meeting.

While calculating managerial remuneration, sitting fees have to be excluded.

5. Managerial Remuneration In Case Of No Profits/ Profits Are Inadequate

The profit is considered as inadequate if remuneration paid to managerial personnel exceeding the limit as prescribed under Sec 197 (1) of the 2013 Act.

Section 197 of the 2013 Act prescribes that if there are no profits or inadequate profits, remuneration to managerial personnel should be as per Schedule V. Option for Central Government approval in the case of Companies which does not complies with Schedule V is eliminated through the 2017 Act. In same situation, remuneration to Non Executive Director can be made only through Member’s Special resolution. Section 197 (11) read with sub section (3), Increase in the remuneration on the grounds of no profit or inadequate profits where provisions contained in:

- Memorandum of Association (MoA) or

- Articles of Association (AoA) or

- Agreement entered in with by Company or

- Resolution passed in General meeting,

shall not have effect unless increase is in accordance with Schedule V. Schedule V shall have overriding over MoA, AoA, agreement and general meeting resolution. Hence, if Company is unable to comply with provisions of Schedule V, then no remuneration can be paid to Managerial Personnel except sitting fee.

Following are the provisions governing Managerial Remuneration payable by the Companies having Nil or Inadequate profits (Section II of Part II of Schedule V)

|

Remuneration to a Managerial Person shall not exceed limit under (A) and (B) given below |

||

|

(A) |

(B) |

|

| Where effective capital * is | Limit of yearly remuneration payable shall not exceed (Rs.) | If managerial person who is functioning in professional capacity # |

| Negative or less than Rs. 5 Crores | 60 Lakhs | No Central Government approval is required if such person is not having any interest in

· Capital of the Company or Holding Company or any of its subsidiaries directly or indirectly · No interest to directors or promoters of the Company or holding Company or any of its subsidiaries during 2 years before appointment and must possess graduate level qualification and specialisation in the field in which Company operates. Also any Employee holding shares not exceeding 0.5% of paid up capital under Employee stock option plan (ESOP) shall be deemed to be person not having any interest in the capital of the Company. |

| Rs. 5 Crores and above but less than Rs. 100 Crores | 84 Lakhs | |

| Rs. 100 Crores and above but less than 250 Crores | 120 Lakhs | |

| Rs. 250 Crores and above | 120 lakhs

plus 0.01% of effective capital in excess of Rs. 250 Crores |

|

| If these remuneration need to be doubled, then resolution by way of special resolution must be passed by the Company in the General meeting | Professional Directors can be paid remuneration irrespective of the limit. | |

* Effective Capital is defined in Explanation I of Section IV to Part II of Schedule V

# Substituted by Notification no. S.O. 2922(E) dated 12.09.2016 w.e.f. 12.09.2016

Limit specified under items (A) and (B) above shall apply only if:

- The payment of remuneration is approved by Nomination and Remuneration Committee.

- The Company has not committed any default in repayment of any of any debts (including public deposits) or debentures or interest payable thereon for a continuous period of 30 days in the preceding financial year before the date of appointment of such managerial personnel.

- Special Resolution has been passed by the Company for payment of remuneration for a period not exceeding 3 years.

- Explanatory Statement along with Notice calling the general meeting shall contain prescribed information.

Section 197 (9) of the 2017 Act states that, if any director draws remuneration in excess of limit prescribed under Sec 197 or without any approval, he shall refund sums to the Company within 2 years or such lesser period as may be allowed by the Company and until such time, he shall hold it in trust. The Company may renounce the excess remuneration paid if it passes the special resolution within 2 years from the date of sum becomes refundable. The Company should additionally get the prior permission of Bank/ public financial institutions/ non convertible debenture holders or other secured creditors before getting approval for waiver, if it has defaulted in payment of such dues of such person.

Insurance taken by Company for Director is not treated as a part of Managerial remuneration but if such person is guilty of offence, premium shall be treated as a part of remuneration.

6. Can A Director Who Is Managing Director/ Whole Time Director Of A Company Receive Remuneration Or Commission From Its Holding Company Or Subsidiary Company?

As per Sec 197 (14) of 2013 Act, A Managing Director/ Whole Time Director who is in receipt of Commission and remuneration from Company shall be qualified to receive remuneration or Commission from Holding Company or Subsidiary Company of such Company subject to the disclosure in Board Report. As per Section V of Part II of Schedule V, managerial personnel shall draw remuneration from one or more Companies, provided total remuneration drawn from the companies does not exceed higher maximum limit permissible from any one of the Companies of which he is a managerial personnel.

7. Certain Disclosure by The Independent Auditors In Their Reporting

A new provision is inserted through Sub Section (16) wherein the auditors shall mention in their report (under Sec 143 of the 2013 Act) as to whether the remuneration paid by the Company to its directors is in accordance with provisions of this section.

SCHEDULE V

This schedule deals with conditions that must be satisfied for the appointment and remuneration of Managerial Personnel without central government approval.

Moreover Part II of Schedule V confers with Managerial Remuneration

8. Managerial Remuneration Payable in Special Circumstances In Case Of Nil or In-Adequate Profits (Section III of Part II of Schedule V)

A. where the remuneration in excess of the limits specified in Section I or Section II can be paid to Managerial Personnel by following companies:

- Foreign Company

- Any other Company subject to following conditions –

- obtain the approval of its shareholders to make such payment;

- treats this amount as managerial remuneration for the purpose of section 197 and

- the total managerial remuneration payable is within permissible limits under section 197.

B. Managerial remuneration up to two times the amount permissible under Section II can be paid in following class of Company:

- Newly incorporated company, for a period of seven years from the date of its incorporation, or

- is a sick company, for which a scheme of revival or rehabilitation has been ordered by the Board for Industrial and Financial Reconstruction (BIFR) or National Company Law Tribunal (NCLT), for a period of five years from the date of sanction of scheme of revival, or

- Company in relation to which resolution plan has been approved by NCLT under Insolvency and Bankruptcy Code, 2016 for a period of 5 years from such approval.

C. Where remuneration of a managerial person exceeds the limits in Section II but the remuneration has been fixed by the BIFR or the NCLT subject to certain conditions.

D. a company in a Special Economic Zone as notified by Department of Commerce from time to time may pay remuneration up to Rs. 2,40,00,000 per annum if it:

- has not raised any money through public issue of shares or debentures in India, and

- has not made any default in India in repayment of any of its debts (including public deposits) or debentures or interest payable thereon for a continuous period of thirty days in any financial year.

9. Perquisite Not Included In Managerial Remuneration (Section IV of Part II of Schedule V)

1. Managerial personnel shall be eligible for the following perquisites which shall not be included in the remuneration mentioned in Section II and Section III

- Contribution to Provident Fund, Superannuation fund or annuity fund to the extent not taxable under Income tax Act, 1961.

- Gratuity payable at a rate not exceeding half a month’s salary for each completed year of services; and

- Encashment of leave at the end of tenure.

2. In addition to the above, an expatriate managerial personnel shall be eligible to following perquisite which shall not be included in the remuneration:

- Children’s education allowance: In case children studying in or outside India, an allowance of Rs. 12000 per annum per child or Actual expenses incurred whichever is lower, subject to the maximum of 2 Children.

- Holiday passage for children studying outside India or family staying abroad: Return Holiday passage once in a year by economy class or once in 2 years by first class to children and to the family members

- Leave travel concession: Return passage for self and family for spending leave in accordance with the rules specified

10. Checklist – Appointment of Managerial Personnel (Managing Director/ WTD Manager)

Listed Public Company

1.Check Articles of Association authorised for the appointment of Additional Director.

2. Send the 7 days’ advance notice in writing along with following documents to Board members at its address registered with Company and such notice shall be sent by hand delivery or by post or by electronic means:

- Agenda,

- Notes to Agenda and

- Draft resolution.

3. Obtain DIN, consent letter, Disclosure of interest in Form MBP-1 and Declaration on non disqualification in form DIR – 8 from the Director.

4. Convene Board Meeting for appointment a person as Additional Director and also as Managerial Personnel including remuneration and pass the following items:

- Approve the Draft agreement for Managerial Personnel appointment.

- Pass Board Resolution for Additional Director and Managerial Personnel appointment

- Authorize any director/ Company Secretary to file forms with the Registrar of Companies.

- Authorise Company Secretary/ Director to issue General Meeting Notice

5. As per Reg 30 read with Schedule III Part A of SEBI (LoDR) Regulations, 2015 Company shall intimate about such appointment with his brief profile to stock exchanges.

6. File E-form DIR-12 (appointment of Additional Director) within 30 days along with following attachments:

a. Consent letter in Form DIR – 2

b. Resolution for appointment as Additional director

7. File MGT-14 (appointment of Managerial Personnel) within 30 days of appointment along with Certified true copy of resolution

8. File DIR-12 (appointment of Managerial Personnel) within 30 days of appointment along with following attachments:

a. Consent letter in Form DIR – 2

b. Certified true copy of resolution

9. Make necessary entries in Register of directors under Sec 170 of the 2013 Act.

At the time of General Meeting

10. Issue 21 days clear notice to the members along with explanatory statement containing details of Managing Director appointment.

11. Hold the General meeting and pass the resolution.

12. File Form MR-1 w.r.t. return of Managerial Personnel appointment within 60 days of appointment.

11. Conclusion

With this amendment, the 2017 Act has made it clear, flexible and generous to make the payment of Managerial Remuneration after complying with its provisions without Central Government approval.

Author Bio

WHAT IF REMUNERATION PAYABLE TO WTD IS ZERO, HOW THE MR-1 SHALL BE FILED?