INTRODUCTION

The Corporate vehicle is considered as channel by defaulters for siphoning of funds for illegitimate purposes like money laundering, tax evasion, corruption, terror financing and illegal activities. In the wake to prevent the misuse of funds & money laundering, the Financial Action Task Force (FATF), an inter-governmental organization formulated various recommendations to tap such funds and based on the same, Ministry of Corporate Affairs (“MCA”) notified revised Section 89 (10) and 90 of the Companies Act, 2013 (“the Act”) through Companies (Amendment) Act, 2017 (“the Amendment Act”) read with the Companies (Significant Beneficial Owners) Rules, 2018 (“the 2018 Rules”) which came into effect from 14.06.2018 and amended through Companies (Significant Beneficial Owners) Amendment Rules, 2019 (“the 2019 Rules”) dated 08.02.2019. Such regulatory framework brought in mainly to identify individual (natural person) who hold significant stake indirectly in reporting company and who is standing behind the screen.

This article deliberates on various provisions of the Act together with respective rules thereunder in respect of Significant Beneficial Owners (“SBO”) along with examples.

UNDERSTAND THE CONCEPT “SIGNIFICANT BENEFICIAL OWNER”

The SBO is defined under Rule 2 (h) of the 2019 Rules and in relation to a reporting company(1), SBO means individual who acting alone or together(2) or through one or more person or trust, possesses one or more of following rights or entitlement in such reporting Company, namely:-

(i) holds indirectly, or together with any direct holdings, not less than 10% of the shares(3);

(ii) holds indirectly, or together with any direct holdings, not less than 10% of the voting rights in the shares;

(iii)has right to receive or participate in not less than 10% of the total distributable dividend, or any other distribution, in a financial year through indirect holdings alone, or together with any direct holdings;

(iv)has right to exercise, or actually exercises, significant influence(4) or control(5), in any manner other than through direct-holdings alone:

Various definitions connected to the concept “SBO”

(1)“Reporting Company” means a company as defined in clause (20) of section 2 of the Act, required to comply with the requirements of section 90 of the Act;

(2)if any individual (s) acting through any person or trust, act with a common intent or purpose of exercising any rights or entitlements, or exercising control or significant influence, over a reporting company, pursuant to an agreement or understanding, formal or informal, such individual, or individuals, acting through any person or trust, as the case may be, shall be deemed to be ‘acting together’. (Explanation V to Rule 2(h) of 2019 Rules)

(3) The instruments in the form of Global Depository Receipts(GDR), Compulsorily Convertible Preference Shares or Compulsorily Convertible Debentures shall be treated as ‘shares’.

(4) “Significant Influence” means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but is not control or joint control of those policies (Rule 2 (i) of 2019 Rules)

(5)“control” means control as defined in Section 2 (27) of the Act to include

a) right to appoint majority of directors or

b) to control the management or

c) policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly including by virtue of their shareholding or management rights or shareholders agreements or voting agreement or in any other manner. (Rule 2 (b) of 2019 Rules along with Sec 2 (27) of the Act)

The Points to be noted to become SBO:

Step-I

He must be Individual (Natural Person)

Step-II

Such Person is acting either alone/together/ through one or more person or trust.

Step-III

Who possess any of the following rights in the Reporting Company:

I. holds indirectly + any direct holdings > 10% of the shares;

2. holds indirectly + any direct holdings > 10% of the voting rights in the shares,

3. has right to receive or participate > 10% of the total distributable dividend, or any other distribution (proceeds from Buy hack of Securities etc.), in a FY through indirect holdings alone/ + any direct holdings;

3. has right to exercise significant influence;

4. has right to exercise control .

IMPORTANCE OF “INDIRECT HOLDING OF RIGHT OR ENTITLEMENT”

It is pertinent to note that if an individual who holds any of the aforesaid rights or entitlement indirectly in the reporting company, then such individual is considered as “SBO”. Now let’s understand the concept “Indirect holding of right or entitlement”. An individual shall be considered to hold a right or entitlement indirectly in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company.

| SI. No | Member of Reporting Company | Who is an SBO |

| 1 | Body Corporate (whether incorporated or registered in India or abroad) |

a. An individual holds majority stake in such Body Corporate; or

b. An individual holds majority stake in the ultimate holding company (whether incorporated or registered in India or abroad) of such Body Corporate. |

| 2 | Hindu Undivided Family (HUF) | An individual who is the Karta of the HUF |

| 3 | Partnership entity (through itself or a partner) | a. Individual who is a partner; or

b. Individual who holds majority stake in the body corporate which is a partner of such partnership entity; or c. Individual who holds majority stake in the ultimate holding company of the body corporate which is a partner of such partnership entity. |

| 4 | Trust (through trustee) | a. individual is a trustee in case of a discretionary trust or a charitable trust (discretionary trust means trust whose beneficiary is not known in advance);

b. Individual who is a beneficiary in case of a specific trust (Specific trust means trust whose beneficiary is known in advance); c. Individual who is the author or settlor in case of a revocable trust. |

| 5 | a. a pooled investment vehicle; or

b. an entity controlled by the pooled investment vehicle, based in member State of the Financial Action Task Force (FATF) on Money Laundering & the regulator of the securities |

a. Individual is a general partner; or

b. Individual is an investment manager; or c. Individual is a CEO where the investment manager of such pooled vehicle is a body corporate or a partnership entity. |

Various definitions connected to the concept “Indirect holding of right or entitlement”

“majority stake” means;-

- holding more than one-half of the equity share capital in the body corporate; or

- holding more than one-half of the voting rights in the body corporate; or

- having the right to receive or participate in more than one-half of the distributable dividend or any other distribution by the body corporate;(Rule 2 (d) of 2019 Rules)

“Partnership Entity” means a partnership firm registered under the Indian Partnership Act, 1932 or a limited liability partnership registered under the Limited Liability Partnership Act, 2008. (Rule 2 (e) of 2019 Rules)

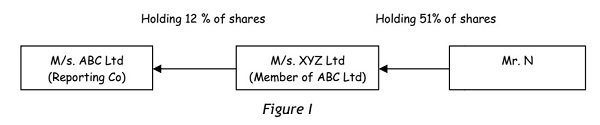

Holding 12 7. of shares Holding 51% of shares

Mr. N has to give declaration as to SBO in relation to M/s. ABC Limited which is reporting Company.

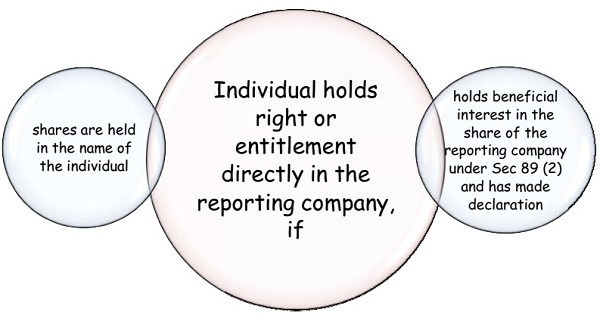

ESTABLISHING “DIRECT HOLDING OF RIGHTS OR ENTITLEMENT”

An individual who hold rights or entitlements directly in reporting Company, the concept of SBO will not attract. We can now determine the concept of “direct holding of rights or entitlement”. An individual shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, namely.

INTERPRETATION OF “BENEFICIAL INTEREST” UNDER SEC 89

There are 2 different concepts under the Sec 89 ie. REGISTERED OWNER (legal owner) and BENEFICIAL OWNER. Registered owner means a person whose name is entered in the Register of Members of the company as the holder of shares in that company but who from the date of deployment of the said e-form.

- Every reporting company shall take necessary steps to find out SBO and cause such individual to make a declaration in Form No. BEN-1.

- A company shall give notice seeking information to any person (whether or not a member of the company) whom the company knows or has reasonable cause to believe:

a. to be a SBO of the company;

b. to be having knowledge of the identity of SBO or another person likely to have such knowledge; or

c. to have been a SBO of the company at any time during the three years immediately preceding the date on which the notice is issued, and who is not registered as a SBO with the company as required under section 90 (5), in Form No. BEN-4. (Sec 90 (5) read with Rule 6)

- Every reporting company shall in all cases where its member (other than an individual), holds not less than ten per cent of its;-

a. shares, or

b. voting rights, or

c. right to receive or participate in the dividend or any other distribution payable in a financial year,

give notice to such member, seeking information in accordance with subsection (5) of section 90, in Form No. BEN-4.

REGISTER OF SBO (Rule 5)

The company shall maintain a register of SBO in Form No. BEN-3 and shall be open for inspection during business hours on every working day as the board may decide on payment of such fee which shall not exceeding Rs. 50 for each inspection.

APPLICATION TO THE NCLT (Rule 7)

The reporting company shall apply to the NCLT within 15 days of expiry of period as

specified in notice,

i. Where any person fails to give the information required by the notice in Form No. BEN-4, within a period of not exceeding 30 days of the date of the notice; or

ii. Where the information given is not satisfactory.

CONCLUDING REMARKS

The disclosures submitted in the regard are expected to bring transparency of shareholding and at same time help the government recognize the benami transactions and prevent money laundering activities.

Author Bio