CS Varun Kapoor

CS Varun Kapoor

“As you sow, so shall you reap,

And I say As Corporate serves

Society so the Society treats”

Introduction:

In simple words, Corporate Social Responsibility (CSR) is the responsibility of company towards society. CSR is attracting attention day by day. Like ‘Swachh Bharat Abhiyaan’ campaign started by our Prime Minister Narendra Modi, is the responsibility of each and every citizen of India, similarly Corporate Houses are also responsible for addressing the needs and desires of society in which they exist with intent to development of the nation.

Adam Smith a renowned Economist wrote in his book “Wealth of Nations” that people engage in Commerce or Business out of selfish reasons or for their personal benefit.

Benefits of CSR :

As per Better Business Journey, UK Small Business Consortium:

“88% of consumers said they were more likely to buy from a company that supports and engages in activities to improve society.”

- Better Credibility

- Enhancing Goodwill of the company

- Attracting the Investors

- Differentiate yourself from your competitors

- Provide access to investmentand funding opportunities

- Generate positive publicityand media opportunities due to media interest in ethical business activities

Although Many Companies have already been engaged in approaching CSR activities voluntarily, but new Companies Act put formal and greater responsibility on specified companies in India to do CSR activities mandatorily to set out clear framework and processes to strict compliance.

The Companies Act, 2013(hereinafter called the Act) has introduced the idea of CSR to the forefront and through its disclose-or-explain mandate, is promoting greater transparency and disclosure.

Legal provisions governing CSR:

- Section 135 of the Act

- Companies (Corporate Social Responsibility Policy) Rules, 2014 (CSR Rules)

- Schedule VII of the Act, which lists out the CSR activities, suggests communities to be the focal point

Section 135, CSR Rules and Schedule VII has come in to effect form 1st April, 2014

Definition of Corporate Social Responsibility as provided in the Act:

As per CSR Rules, Corporate Social Responsibility means and includes but not limited to:

(i) Projects or programs relating to activities specified in the Schedule VII of the Act or

(ii) Projects or programs relating to activities undertaken by the board of directors of a company (Board) in recommendations of the CSR Committee of Board as per declared CSR policy of the company subject to the condition that will cover subjects enumerated in Schedule VII of the Act.

The above mentioned Companies shall constitute a Corporate Social Responsibility Committee of the Board consisting of three or more directors, out of which at least one director shall be an independent director.

Section 135(2)-Disclosure in Board’s Report:

The Board’s report under sub-section (3) of section 134 shall disclose the composition of the Corporate Social Responsibility Committee.

Section 135(3)-Functions of CSR Committee:

The Corporate Social Responsibility Committee shall,—

(a) formulate and recommend to the Board, a Corporate Social Responsibility Policy which shall indicate the activities to be undertaken by the Company as specified in Schedule VII;

(b) recommend the amount of expenditure to be incurred on the activities referred to in clause (a); and

(c) monitor the Corporate Social Responsibility Policy of the company from time to time.

Section 135(4)-CSR Policy:

The Board shall,—

(a) after taking into account the recommendations made by the Corporate Social Responsibility Committee, approve the Corporate Social Responsibility Policy for the company and disclose contents of such Policy in its report and also place it on the company’s website, if any, in such manner as may be prescribed; and

(b) ensure that the activities as are included in Corporate Social Responsibility Policy of the company are undertaken by the company.

135(5)-Responsibilities of Board of Directors:

The Board shall ensure that the company spends, in every financial year, at least 2% of the average net profits of the company made during the three immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy

First Proviso to Section 135(5):

Provided that the Company shall give preference to the local area and areas around it where it operates, for spending the amount earmarked for Corporate Social Responsibility activities:

Second Proviso to Section 135(5)- Contravention based on Disclose or Explain:

Provided further that If the company fails to spend such amount, the Board shall, in its report made under Section 134(3)(o), specify the reasons for not spending the amount.

Companies (Corporate Social Responsibility Policy) Rules, 2014 (CSR Rules)

Calculation of Net Profit:

As per Rule 2(f):

“Net profit” means the net profit of a company as per its financial statement prepared in accordance with the applicable provisions of the Act, but shall not include the following, namely :-

(i)any profit arising from any overseas branch or branches of the company whether operated as a separate company or otherwise; and

(ii)any dividend received from other companies in India, which are covered under and complying with the provisions of section 135 of the Act

Provided that net profit in respect of a financial year for which the relevant financial statements were prepared in accordance with the provisions of the Companies Act, 1956 shall not be required to be re-calculated in accordance with the provisions of the Act:

Provided further that in case of a foreign company covered under these rules, net profit means

the net profit of such company as per profit and loss account prepared in terms of clause (a) of sub section (l) of Section 381 read with Section 198 of the Act.

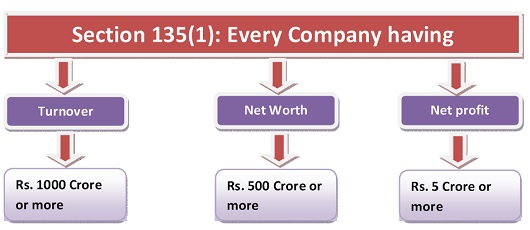

Category of Companies in which CSR provisions shall apply:

As per Rule 3:

Every company including its holding or subsidiary, and a foreign company defined under clause (42) of section 2 of the Act having its branch office or project office in India which fulfills the criteria specified in sub-section (l) of section 135 of the Act shall comply with the provisions of section 135 of the Act and these rules.

Provided that net worth, turnover or net profit of a foreign company of the Act shall be computed in accordance with balance sheet and profit and loss account of such company prepared in accordance with the provisions of clause (a) of sub-section (1) of section 381 and section 198 of the Act.

(2) Every company which ceases to be a company covered under sub-section (1) of section 135 of the Act for three consecutive financial years shall not be required to –

(a) constitute a CSR Committee; and

(b) comply with the provisions contained in sub-section (2) to (5) of the section 135

till such time it meets the criteria specified in sub-section (1) of section 135

CSR Committees:

As per Rule 5

(1) The companies mentioned in the rule 3 shall constitute CSR Committee as under.-

(i) an unlisted public company or a private company covered under sub-section ( I ) of section I 35 which is not required to appoint an independent director pursuant to sub-section (4) of section 149 of the Act, shall have its CSR Committee without such director

(ii) a private company having only two directors on its Board shall constitute its CSR Committee with two such directors:

(iii) with respect to a foreign company covered under these rules, the CSR Committee shall comprise of at least two persons of which one person shall be as specified under clause (d) of sub-section (1) of section 380 of the Act and another person shall be nominated by the foreign company.

(2) The CSR Committee shall constitute a transparent monitoring mechanism for implementation of the CSR projects or programs or activities undertaken by the company

CSR Policy:

As per Rule 6:

(1) The CSR Policy of the company shall, inter-alia, include the following, namely –

(a) a list of CSR projects or programs which a company plans to undertake falling within the purview of the Schedule VII of the Act, specifying modalities of execution of such project or programs and implementation schedules for the same; and

(b) monitoring process of such projects or Programs:

Provided that the CSR activities does not include the activities undertaken in pursuance of normal course of business of a company.

Provided further that the Board of Directors shall ensure that activities included by a company in its Corporate Social Responsibility Policy are related to the activities included in Schedule VII of the Act.

(2) The CSR Policy of the company shall specify that the surplus arising out of the CSR projects or programs or activities shall not form part of the business profit of a company.

CSR Expenditure

As per Rule 7:

CSR expenditure shall include all expenditure including contribution to corpus, for projects or programs relating to CSR activities approved by the Board on the recommendation of its CSR Committee, but does not include any expenditure on an item not in conformity or not in line with activities which fall within the purview of Schedule VII of the Act.

CSR Reporting

As per Rule 8:

(l) The Board’s Report of a company covered under these rules pertaining to a financial year commencing on or after the 1st day of April, 2014 shall include an annual report on CSR containing particulars specified in Annexure.

(2) In case of a foreign company, the balance sheet filed under sub-clause (b) of sub-section (l) of Section 381 shall contain an Annexure regarding report on CSR.

Display of CSR activities on its website:

As per Rule 9:

The Board of Directors of the company shall, after taking into account the recommendations of CSR Committee, approve the CSR Policy for the company and disclose contents of such policy in its report and the same shall be displayed on the company’s website, if any, as per the particulars specified in the Annexure.

Circular issued by Ministry of Corporate Affairs w.r.t. CSR:

General Circular No. 21/2014

No. 05/01/2014- CSR

Clarifications with respect to representations received in the Ministry on Corporate Social Responsibility (hereinafter referred as (‘CSR’) are as under:-

(i) The statutory provision and provisions of CSR Rules, 2014, is to ensure that while activities undertaken in pursuance of the CSR policy must be relatable to Schedule VII of the Companies Act 2013, the entries in the said Schedule VII must be interpreted liberally so as to capture the essence of the subjects enumerated in the said Schedule. The items enlisted in the amended Schedule VII of the Act, are broad-based and are intended to cover a wide range of activities as illustratively mentioned in the Annexure.

(ii) It is further clarified that CSR activities should be undertaken by the companies in project programme mode [as referred in Rule 4 (1) of Companies CSR Rules, 2014]. One-off events such as marathons/ awards/ charitable contribution/ advertisement/ sponsorships of TV programmes etc. would not be qualified as part of CSR expenditure.

(iii) Expenses incurred by companies for the fulfillment of any Act/ Statute of regulations (such as Labour Laws, Land Acquisition Act etc.) would not count as CSR expenditure under the Companies Act.

(iv) Salaries paid by the companies to regular CSR staff as well as to volunteers of the companies (in proportion to company’s time/hours spent specifically on CSR) can be factored into CSR project cost as part of the CSR expenditure.

(v) “Any financial year” referred under Sub-Section (1) of Section 135 of the Act read with Rule 3(2) of Companies CSR Rule, 2014, implies ‘any of the three preceding financial years’.

(vi) Expenditure incurred by Foreign Holding Company for CSR activities in India will qualify as CSR spend of the Indian subsidiary if, the CSR expenditures are routed through Indian subsidiaries and if the Indian subsidiary is required to do so as per section 135 of the Act.

(vii) ‘Registered Trust’ (as referred in Rule 4(2) of the Companies CSR Rules, 2014) would include Trusts registered under Income Tax Act 1956, for those States where registration of Trust is not mandatory.

(viii) Contribution to Corpus of a Trust/ society/ section 8 companies etc. will qualify as CSR expenditure as long as (a) the Trust/ society/ section 8 companies etc. is created exclusively for undertaking CSR activities or (b) where the corpus is created exclusively for a purpose directly relatable to a subject covered in Schedule VII of the Act.

Amended Schedule VII of the Act:

Activities which may be included by Companies in their Corporate Social Responsibility Policies:

- eradicating hunger, poverty and malnutrition, promoting preventive health care and sanitation and making available safe drinking water;

- promoting education, including special education and employment enhancing vocation skills especially among children, women, elderly, and the differently abled and livelihood enhancement projects;

- promoting gender equality, empowering women, setting up homes and hostels for women and orphans; setting up old age homes, day care centres and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups;

- ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agroforestry, conservation of natural resources and maintaining quality of soil, air and water;

- protection of national heritage, art and culture including restoration of buildings and sites of historical importance and works of art; setting up public libraries; promotion and development of traditional arts and handicrafts:

- measures for the benefit of armed forces veterans, war widows and their dependents;

- training to promote rural sports, nationally recognised sports, paralympic sports and Olympic sports;

- contribution to the Prime Minister’s National Relief Fund or any other fund set up by the Central Government for socio-economic development and relief and welfare of the Scheduled Castes, the Scheduled Tribes, other backward classes, minorities and women;

- contributions or funds provided to technology incubators located within academic institutions which are approved by the Central Government

- rural development projects;

SEBI CONSIDERED CSR COMPULSORY

SEBI vide its circular CIR/CFD/DIL/8/2012 dated August13, 2012 has made it mandatory for top 100 listed companies (by market capitalization) to report certain critical information as part of their business responsibility.

A new Clause 55 has been inserted to read as under:

“Listed entities shall submit, as part of their Annual Reports, Business Responsibility Reports, describing the initiatives taken by them from an environmental, social and governance perspective, in the format suggested in the circular”

This includes

- How much the company is spending on CSR as a percentage of its net profit,

- The number of stakeholders’ complaints received and resolved,

- Details of any pending case filed by stakeholder against any unfair trade practice, irresponsible advertising or anti-competitive behavior adopted by the company.

This will enable the shareholders to have a better understanding of the manner in which their companies’ function and adopt responsible business practices.

The circular exhorts the companies to follow the national voluntary guidelines on social, environmental and economic responsibility that have been formulated by Ministry of Corporate Affairs in July 2011.

Conclusion: This is the first year of CSR implementation by Companies under the Act. The likely amount of CSR expenditure for the year 2014-15 would be known only after the Annual Financial Statements are filed by Companies due after September, 2015.

Source: Companies Act, 2013, MCA circular and SEBI circular

Disclaimer: This article contains interpretation of the Act, Rules and personal views of the author are based on such interpretation. It is not intended to be a professional advice and should not be relied upon for real time professional facts. Readers are advised either to cross check the views of the author with the Act or seek the expert’s views if they want to rely on contents of this article. Author accepts no responsibility whatsoever and will not be liable for any losses, claims or damages which may arise because of the contents of this write up. Kindly share your opinion.

Other Article from CS Varun Kapoor- Provisions governing Buy Back of Shares under Companies Act 2013

Author Bio

Kindly Confirm whether we have to reduce foreign branch profit from section 198 profit

Please send me the following on my registered email id.