CS Varun Kapoor

One year back, the Ministry of Corporate Affairs (MCA) has came with the draft rules pertaining to Significant Beneficial Ownership. The draft rules got the green signal and became final and published in the gazette on June 13, 2018 as Companies (Significant Beneficial Owners) Rules, 2018. The rules bound every Significant Beneficial Owner (SBO) to file a declaration with the Company with effect to his/her shareholding in that Company in the relevant form in prescribed time. On the same side, the rules also bound every such Company to report further regarding the details shared by SBO.

COMPARATIVE CHANGES BETWEEN THE OLD SBO RULES AND NEW SBO

RULES:

Now, the MCA again came with the duly amended rules and published in the official gazette on February 08, 2019 as Companies (Significant Beneficial Owners) Amendment Rules, 2019, wherein some changes has been made which includes:

> Insertion of new definitions partnership entity, reporting company, significant beneficial owner with detailed explanations and significant influence

> Defining the duties of the reporting Company which indicates the duty to seek information from every SBO

> Coverage of pooled investment vehicles

> Substitution of BEN Forms

DIFFERENTIATE WITH BENEFICIAL OWNER(“BO”)

It is really important to know the difference between the BO and SBO to avoid any doubts/ confusion.

A person whose name is NOT entered in the register of members of a company as the holder of shares in that Company but who holds the beneficial interest in such shares shall be the “the beneficial owner

| Basis | Beneficial Owner | Significant Beneficial Owner |

| Meaning and

percentage of interest

|

A person whose name is NOT entered in the register of members of a company as the holder of shares in that Company but who holds the beneficial interest (any percentage) in such shares shall be the “the beneficial owner ” |

SBO is an individual holding ultimate beneficial interest at least 10% and whose name is NOT entered in the register of members of a Company.

|

| Legal Framework | BO is governed by Section 89 read with Rule 9 of Companies (Management and Admnistration) Rules, 2014 | SBO is governed by Section 90 read with SBO Rules |

| Form | BO is required to furnish declaration in Form MGT-5 |

SBO is required to furnish declaration in Form BEN-1 only if he holds more than 10 per cent |

FORMS

The forms for filing Declaration, Return to the ROC, Register, Notice to SBO are also specified by the MCA. The details of the forms are as under:

Name of Form |

Purpose |

To Whom to file /give/ record |

By Whom |

Time- limit |

BEN-1 |

Declaration by the beneficial owner who holds or acquires significant beneficial ownership in shares |

The Company in which he holds significant beneficial ownership |

SBO |

90 days of the SBO Rules coming into effect and 30 days of acquiring such significant beneficial ownership |

BEN-2 |

Return to the Registrar in respect of declaration under section 90 |

Jurisdictional Registrar of Companies |

The Company which has received the Form BEN-1. |

Within 30 (thirty) days of receiving Form BEN-1. |

BEN-3 |

Register of beneficial owners holding significant beneficial interest |

The Company which has significant beneficial ownership |

N.A. |

As applicable |

BEN-4 |

Notice seeking information about significant beneficial owners |

The significant beneficial owner |

The Company which has significant beneficial ownership |

At the earliest and as applicable |

From above, it can be easily understood that the duties are defined on both the Company as well as SBO.

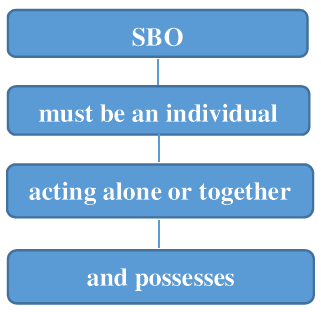

DEFINITION OF SIGNIFICANT BENEFICIAL OWNER(SBO)

The MCA in its notification dated 08.02.2019, has clearly defined the term SBO. As per the notification,

The SBO in relation to a reporting company means

an individual referred to in subsection (1) of section 90,

who

acting alone or together, or through one or more persons or trust,

possesses

one or more of the following rights or entitlements in such reporting company, namely:-

EXPLANATIONS w.r.t. SBO

NO HOLD:

> If an individual does not hold any right or entitlement indirectly as depicted above, he shall not be considered to be a significant beneficial owner.

DIRECTLY HOLDS:

> An individual shall be considered to hold a right or entitlement DIRECTLY in the reporting company, if he satisfies any of the following criteria, namely:

> the shares in the reporting company representing such right or entitlement are held in the name of the individual;

> the individual holds or acquires a beneficial interest in the share of the reporting company under subsection (2) of section 89, and has made a declaration in this regard to the reporting company.

INDIRECTLY HOLDS:

> An individual shall be considered to hold a right or entitlement INDIRECTLY in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company, namely:-

BODY CORPORATE:

> Where the member of the reporting company is a BODY CORPORATE (whether incorporated or registered in India or abroad), other than a limited liability partnership, and the individual,––

(a) holds majority stake in that member; or

(b) holds majority stake in the ultimate holding company (whether incorporated or registered in India or abroad) of that member;

HINDU UNDIVIDED FAMILY (HUF):

> Here the member of the reporting company is a HINDU UNDIVIDED FAMILY (HUF) (through karta), and the individual is the karta of the HUF;

PARTNERSHIP ENTITY:

Where the member of the reporting company is a PARTNERSHIP ENTITY (through itself or a partner), and the individual,-

(a) is a partner; or

(b) holds majority stake in the body corporate which is a partner of the partnership entity; or

(c) holds majority stake in the ultimate holding company of the body corporate which is a partner of the partnership entity.

TRUST:

Where the member of the reporting company is a TRUST (through trustee), and the individual,-

(a) is a trustee in case of a discretionary trust or a charitable trust;

(b) is a beneficiary in case of a specific trust;

(c) is the author or settlor in case of a revocable trust.

POOLED INVESTMENT VEHICLE:

Where the member of the reporting company is,-

(a) a POOLED INVESTMENT VEHICLE; or

(b) an ENTITY CONTROLLED BY THE POOLED INVESTMENT VEHICLE, based in member State of the Financial Action Task Force on Money Laundering and the regulator of the securities market in such member State is a member of the International Organization of Securities Commissions, and the individual in relation to the pooled investment vehicle,-

(A) is a general partner; or

(B) is an investment manager; or

(C) is a Chief Executive Officer where the investment manager of such pooled vehicle is a body corporate or a partnership entity.

> If any individual, or individuals acting through any person or trust, act with a common intent or purpose of exercising any rights or entitlements, or exercising control or significant influence, over a reporting company, pursuant to an agreement or understanding, formal or informal, such individual, or individuals, acting through any person or trust, as the case may be, shall be deemed to be ‘acting together’.

> The instruments in the form of global depository receipts, compulsorily convertible preference shares or compulsorily convertible debentures shall be treated as ‘shares’.

> SIGNIFICANT INFLUENCE means the power to participate, directly or indirectly, in the financial and operating policy decisions of the reporting company but is not control or joint control of those policies’.

RESPONSIBILITY OF REPORTING COMPANY

COMPANY TO IDENTIFY SBO:

> In terms of the Rule 2A, every reporting company SHALL IDENTIFY any individual who is a significant beneficial owner, as explained above, and cause such individual to make a declaration in Form No. BEN-1 and give notice to such member, seeking information in accordance in Form No. BEN-4.

Declaration of significant beneficial ownership under section 90

SBO TO FILE DECLARATION IN 90 DAYS IN FORM BEN-1:

> According to the Rule 3, every individual who is a significant beneficial owner in a reporting company, shall file a declaration in Form No. BEN-1 to the reporting company WITHIN NINETY DAYS from such commencement.

ANY CHANGE IN EXISTING OR NEW SBO TO FILE DECLARATION IN 30 DAYS IN

FORM BEN-1:

- Every individual, who subsequently becomes a significant beneficial owner, or where his significant beneficial ownership undergoes any change shall file a declaration in Form No. BEN-1 to the reporting company, WITHIN THIRTY DAYS of acquiring such significant beneficial ownership or any change therein.

APPLICATION TO THE TRIBUNAL

> The reporting company shall apply to the Tribunal, –

FAILURE TO PROVIDE BEN-1 BY SBO:

(i) where ANY PERSON FAILS to give the information required by the notice in Form No. BEN-4, within the time specified therein; or

INCOMPLETE INFORMATION BY SBO:

(ii) where the information given is NOT SATISFACTORY,

in accordance with sub-section (7) of section 90, for order directing that the shares in question be subject to restrictions, including:

(a) restrictions on the transfer of interest attached to the shares in question

(b) suspension of the right to receive dividend or any other distribution in relation to the shares in question

(c) suspension of voting rights in relation to the shares in question

(d) any other restriction on all or any of the rights attached with the shares in question.

NON- APPLICABILITY

> The SBO rules shall not be made applicable to the extent the share of the reporting company is held by,-

(a) the authority constituted under sub-section (5) of section 125 of the Act;

(b) its holding reporting company:

Provided that the details of such holding reporting company shall be reported in Form No. BEN-2.

(c) the Central Government, State Government or any local Authority;

(d) (i) a reporting company, or

(ii) a body corporate, or

(iii) an entity,

controlled by the Central Government or by any State Government or Governments, or partly by the Central Government and partly by one or more State Governments;

(e) Securities and Exchange Board of India registered Investment Vehicles such as mutual funds, alternative investment funds (AIF), Real Estate Investment Trusts (REITs), Infrastructure Investment Trust (InVITs) regulated by the Securities and Exchange Board of India,

(f)Investment Vehicles regulated by Reserve Bank of India, or Insurance Regulatory and Development Authority of India, or Pension Fund Regulatory and Development Authority.

Disclaimer: This article contains interpretation of the Act, Rules, Regulations and personal views of the author are based on such interpretation. Readers are advised either to cross check the views of the author with the Act or seek the expert’s views if they want to rely on contents of this article. I assume no responsibility therefore. This is only a knowledge sharing initiative and author has no intention to solicit any business or profession.

About Author: The above has been compiled by CS Varun Kapoor, proprietor of V Kapoor & Associates, Rohini, New Delhi. For any queries or suggestions, he can be approached at varun@vkacs.com, pcsvarunkapoor@gmail.com

Source: Companies Act, 2013 and Rules made thereunder and MCA Notifications

Author Bio