Disciplinary Committee (Bench-II) of the Institute of Chartered Accountants of India (ICAI) has formally reprimanded CA. Ravish Shashikant Maniyar for professional misconduct. The order, issued on May 9, 2024, concludes a disciplinary proceeding initiated by Dr. Rajkumar Kaluram Gaikwad, primarily concerning the auditor’s failure to disclose crucial information in an audit report for the financial year 2017-18.

The case, bearing file number PR/369/2018-DD/70/2019-DC/1360/2020, involved allegations of professional misconduct under Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949, which pertains to an auditor’s failure to exercise due diligence or gross negligence in professional duties.

Page Contents

Case Background and Respondent’s Defense

The Disciplinary Committee, composed of Presiding Officer CA. Ranjeet Kumar Agarwal, Mrs. Rani S. Nair (IRS Retd.), Shri Arun Kumar (IAS Retd.), CA. Sanjay Kumar Agarwal, and CA. Cotha S Srinivas, convened on March 19, 2024, to hear CA. Maniyar’s representation following the Committee’s initial findings dated February 7, 2024, which deemed him guilty.

CA. Maniyar attended the hearing via video conferencing and presented both verbal and written arguments. He asserted that there was no malicious intent or personal benefit from the alleged misconduct. He emphasized his relatively limited experience in professional practice at the time, having completed less than five years, and highlighted the potential adverse impact of an unfavorable decision on his two-partner firm and its ongoing work.

His defense included arguments that:

- He became aware of a one-time settlement with the bank only through management inquiry, and repayment defaults were resolved before the audit report was signed.

- Payments for the one-time settlement against due cheques were made, and all SARFAESI notices were subsequent events, with disclosures made only upon becoming known.

- While the bank’s name was not in the audit report, it was mentioned in the financial statements.

- The Committee’s calculation of materiality regarding loan defaults was incorrect, assuming the entire loan balance was defaulted instead of just the overdue installments.

- A Management Representation Letter confirmed the reported remarks.

- The company provided a Management Representation Letter confirming no pending litigation with major financial impact and a going concern status, aligning with Rule 11 of the Companies (Audit and Auditors) Rules, 2014.

- Principles of natural justice were not fully followed, as he was not given an opportunity to cross-examine the Complainant or argue against the Complainant’s post-hearing submissions.

- He contended it was mere conjecture that he was aware of the SARFAESI action.

- The Complainant did not properly specify the relevant clauses of misconduct in the complaint form.

- All promoters were aware of business developments, and no promoter’s interest was affected by the alleged misconduct. He stated that qualifications regarding SARFAESI proceedings were included in the subsequent year’s audit report once he became aware.

The Committee acknowledged the Respondent’s submissions regarding the non-specificity of misconduct clauses by the Complainant, stating that a complaint’s factual foundation takes precedence over incorrect or omitted legal provisions, provided the adjudicating authority has jurisdiction. It also noted that both parties had submitted written documents post-August 23, 2023, hearing, which were duly considered.

Committee’s Findings and Guiding Principles

The Disciplinary Committee’s findings, which are to be read in conjunction with the final order, primarily focused on five charges. CA. Maniyar was found “Not Guilty” on four of these charges after detailed examination:

- Provision for Construction Expenses Payable: The Committee found that the provision of ₹19.31 crore for “Construction Expenses Payable” was adequately verified with supporting documents, including board meeting minutes, a signed agreement, a management representation letter, and an architect’s certificate. The Respondent’s disclosure under “Emphasis of Matter” in the audit report confirmed due diligence.

- No Documentation for Short-Term Loans & Advances: The Committee noted that the Respondent had obtained balance confirmations for 71.25% of the total short-term loans and advances, along with a performa invoice for a significant portion, indicating sufficient documentation.

- No Documentation for Loan from Mrs. Smeeta Patil (Director): The Committee confirmed that the Respondent had obtained a board resolution, bank statements, ledger accounts, and a declaration from the director confirming the loan was from her own funds, satisfying documentation requirements.

- Missing Valuation of Building in Financial Statements: The Committee found that the valuation of the building was properly disclosed as “Capital Work In Progress” under “Non-Current Assets,” with detailed break-ups and supporting documents like loan account statements and architect certificates confirming construction progress.

However, CA. Maniyar was found “Guilty” on the most critical charge:

- Wrong Disclosure in Audit Report Regarding SARFAESI Proceedings: The Committee found that despite an order dated April 27, 2018, from the District Magistrate regarding the physical possession of the company’s property by Saraswat Co-operative Bank under the SARFAESI Act, 2002, the Respondent reported in his audit report that “no litigation is pending against the Company.”

- The loan became a Non-Performing Asset (NPA) in September 2017, and subsequent notices for property attachment were issued in July 2018, September 2018, and March 2019.

- Although a one-time settlement was attempted in August 2018, it was not adhered to, with only a fraction of the agreed amount being paid.

- The Committee emphasized that SARFAESI proceedings significantly impact the “Going Concern” assumption as per Accounting Standard – 1. An auditor is required by SA 570 (Revised) to evaluate management’s assessment of going concern and, if material uncertainty exists and is not adequately disclosed, to express a qualified or adverse opinion.

- The Committee rejected the Respondent’s argument of unawareness, stating that he should have inquired from the management about such critical events affecting the company’s ability to continue as a going concern.

- Furthermore, in his report under CARO, 2016, regarding repayment of loans, the Respondent failed to mention the name of the bank and the period of default, as required. He also reported that no litigation was pending despite his awareness of the SARFAESI action.

Judicial Precedents and Standard of Care

While the order does not explicitly reference specific judicial precedents, the finding of “gross negligence” and “lack of due diligence” under Item (7) of Part I of the Second Schedule aligns with established legal interpretations of an auditor’s responsibilities. Courts have consistently held that auditors must act with reasonable care and skill, and their reports must not be misleading. The principle that auditors are not mere “watchdogs but bloodhounds” in certain circumstances, as famously articulated in In re Kingston Cotton Mill Co. (No 2) [1896], underscores the expectation for auditors to investigate unusual circumstances.

More broadly, cases pertaining to auditor liability for non-disclosure of material facts, especially those affecting a company’s going concern status or solvency, like Caparo Industries Plc v Dickman [1990] (though a UK case, its principles on auditor duty of care are influential globally), or Indian cases that reinforce the auditor’s statutory duty to report on compliance and financial health, implicitly underpin such disciplinary actions. The ICAI’s stance reflects the statutory obligation on auditors to ensure that financial statements, along with their reports, present a true and fair view and adequately disclose all material information, particularly concerning financial stability and ongoing legal proceedings that could impact the entity.

Disciplinary Action

The Committee concluded that CA. Ravish Shashikant Maniyar was GUILTY of Professional Misconduct under Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949, due to his failure to exercise requisite due diligence and gross negligence in reporting a material fact and misstatement regarding pending SARFAESI action.

Given the nature of the misconduct, the Disciplinary Committee decided that the “ends of justice” would be met by reprimanding CA. Ravish Shashikant Maniyar. Accordingly, he has been reprimanded under Section 21B(3)(a) of the Chartered Accountants Act, 1949.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

PR/369/2018-DD/70/2019-DC/1360/2020

[DISCIPLINARY COMMITTEE [BENCH-II (2024-2025)]

[Constituted under Section 21B of the Chartered Accountants Act, 1949]

ORDER UNDER SECTION 21B (3) OF THE CHARTERED ACCOUNTANTS ACT, 1949 READ WITH RULE 19(1) OF THE CHARTERED ACCOUNTANTS (PROCEDURE OF INVESTIGATIONS OF PROFESSIONAL AND OTHER MISCONDUCT AND CONDUCT OF CASES) RULES, 2007

[PR/369/2018-DD/70/2019-DC/1360/2020]

In the matter of:

Dr. Rajkumar Kaluram Gaikwad, ….Complainant

Versus

CA. Ravish Shashikant Maniyar…..Respondent

Members Present:-

CA. Ranjeet Kumar Agarwal, Presiding Officer (in person)

Mrs. Rani S. Nair, IRS (Retd.), Government Nominee) (through VC)

Shri Arun Kumar, IAS (Retd.), Government Nominee (in person)

CA. Sanjay Kumar Agarwal, Member (in person)

CA. Cotha S Srinivas, Member (in person)

Date of Hearing: 19th March, 2024

Date of Order: 9th May, 2024

1. That vide Findings under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Disciplinary Committee was ,inter-alia, of the opinion that Ravish Shashikant Maniyar (hereinafter referred to as the Respondent”) is GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

2. That pursuant to the said Findings, an action under Section 21B (3) of the Chartered Accountants (Amendment) Act, 2006 was contemplated against the Respondent and a communication was addressed to him thereby granting opportunity of being heard in person / through video conferencing and to make representation before the Committee on 19th March 2024.

3. The Committee noted that on the date of the hearing held on 19th March 2024, the Respondent was present through video conferencing and made his verbal representation on the Findings of the Disciplinary Committee, inter-alia, stating that neither there was any motive or bad intention on his part nor was he benefitted due to alleged misconduct. He had not completed even 5 years of his professional practice at the relevant time. He is practising in a firm of two partners and any adverse action would affect the existing and new professional work. The Committee also noted that the Respondent in his written representation on the Findings of the Committee, inter-alia, stated as under:

(a) One time settlement was known to the Respondent only based on his enquiry with the Management about the repayment defaults and the matter of repayment defaults was sorted out before the signing of the audit report.

(b) Payment against one time settlement against the cheques due till the audit report were duly made. All alleged notices in respect of SARFESAI were after the year end i.e. Subsequent Event. Disclosures made when the matter became known.

(c) Though the name of the Bank is not mentioned in Audit report, but, in the Financials, the name of the Bank- The Saraswat Co-operative Bank has been mentioned.

(d) Wrong calculation of materiality: It has been wrongly concluded that 65% of the long-term borrowings was a default amount of repayment by assuming that the entire loan balance of Rs. 1462.87 lacs outstanding as on 31st March 2018 represented the defaulted repayment, instead of considering only the amount of instalments due but not paid.

(e) Management Representation letter confirmed the remarks.

(f) In terms of Item No. 1 of Companies (Audit and Auditors) Rules, 2014, the requirement was to disclose the impact of pending litigation, if any, on the financial position in the financial statement. The Company gave Management Representation letter to the effect that there were no litigation pending having any major financial impact and the Company was a going concern.

(g) The principles of natural justice have not been followed as no opportunity of hearing for the purpose of the cross examination of the Complainant as well as for arguing in respect of the response from the Complainant on the matter after the hearing on 23rd August 2023 was given to Respondent.

(h) It is only a conjecture on the part of Hon’ble Disciplinary Committee that the Respondent was aware of SARFESAI action.

(i) The Complainant has not indicated in item number 5 of Form-1 of his complaint, the particulars of the allegation serially numbered together with corresponding clause/part of the relevant schedule under which the alleged act of commission / omission would fall. The Hon’ble Disciplinary Committee had agreed with Prima Facie opinion for a charge which was not applied at all in the Prima Facie Opinion i.e. Clause (1) of Part 1 of Second Schedule.

(j) All the promoters were aware of the developments in business and interest of none of them has been affected due to alleged misconduct of disclosure. The Respondent had given all the necessary qualification in the audit report of subsequent year when he became aware of the SARFESI proceedings.

4. The Committee considered the reasoning as contained in the Findings holding the Respondent Guilty of Professional Misconduct vis-à-vis written and verbal representation of the Respondent. As regard the submission of the Respondent that specific clause of the misconduct had not been defined by the Complainant, the Committee is of the view that it is trite that a Complainant is required as per law to state the allegations which are to form a factual foundation for an Adjudicating Authority to exercise jurisdiction and even if an incorrect provision of law/no clauses is mentioned by the Complainant in FORM I, that alone cannot be a ground to dismiss a complaint if otherwise the Authority has the jurisdiction to entertain the complaint. As regard the submission of the Respondent that no opportunity of hearing after the hearing on 23rd August 2023 was given to the Respondent, the Committee noted that pursuant to conclusion of the hearing held on 23rd August, 2023 and in compliance with its direction given in the said meeting, both the parties had submitted the written submissions/documents which were duly considered along with the other submissions and documents on record by the Committee before arriving at its Findings.

5. Keeping in view the facts and circumstances of the case, material on record including verbal and written representations on the Findings, the Committee is of the view that it has already been held that the Respondent, despite being aware of SARFAESI action against the client, had mentioned in his audit report that no litigation was pending against the Company which shows a lack of diligence by the Respondent in the conduct of his professional duties and thus, he failed to exercise requisite due diligence while auditing and was grossly negligent in reporting material fact and misstatement. Hence, professional misconduct on the part of the Respondent is clearly established as spelt out in the Committee’s Findings dated 7th February 2024 which is to be read in consonance with the instant Order being passed in the case.

6. Accordingly, the Committee was of the view that ends of justice will be met if punishment is given to him in commensurate with his professional misconduct.

7. Thus, the Committee ordered that CA. Ravish Shashikant Maniyar, Sangamner be reprimanded under Section 21B(3)(a) of the Chartered Accountants Act 1949.

sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

sd/-

(MRS. RANI S. NAIR, IRS RETD.)

GOVERNMENT NOMINEE

sd/-

(SHRI ARUN KUMAR, IAS RETD.)

GOVERNMENT NOMINEE

sd/-

(CA. SANJAY KUMAR AGARWAL)

MEMBER

sd/-

(CA. COTHA S. SRINIVAS)

MEMBER

CONFIDENTIAL

DISCIPLINARY COMMITTEE [BENCH – II (2023-2024)]

[Constituted under Section 21B of the Chartered Accountants Act, 1949]

Findings under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007.

File No. – PR/369/2018-DD/70/2019-DC/1360/2020

IN THE MATTER OF:

Dr. Rajkumar Kaluram Gaikwad,…… Complainant

Versus

Sh. Ravish Shashikant Maniyar …..Respondent

MEMBERS PRESENT:

CA. Ranjeet Kumar Agarwal, Presiding Officer (In person)

Smt. Rani Nair, I.R.S. (Retd.), Government Nominee (Present in person)

Shri. Arun Kumar, I.A.S. (Retd.), Government Nominee (Present in person)

CA. Sridhar Muppala, Member (In person)

DATE OF FINAL HEARING: 23.08.2023

DATE OF JUDGEMENT : 18.09.2023

PARTIES PRESENT:

Complainant: Dr. Rajkumar Kaluram Gaikwad (Through Video Conferencing Mode)

Complainant Counsel: Mr. Ambernath Vibhute, Advocate (Through Video Conferencing Mode)

Respondent: CA. Ravish Shashikant Maniyar (Through Video Conferencing Mode)

Respondent Counsel: CA. Shashikant Barve (Through Video Conferencing Mode)

BACKGROUND OF THE CASE

1. The brief background of the case is:

a. That the Complainant along with other Directors purchased land measuring 2400 Sq. Meter at S. No 117, Manuj Kalas Pune on 7th Feb 2007 for a hospital project. They established M/s Orange Medicare and Research Centre Pvt. Ltd (hereinafter referred to as the “Company/OMRC”), a private limited Company and sold the land to it.

b. Saraswat Co-operative Bank extended a loan for the project which the Complainant and other directors guaranteed and mortgaged their personal properties as security.

c. Further, for the development of the project and project financial management of the Company, an agreement was entered into between the Company and its then directors including the Complainant on 11th February, 2016 with Mr. Sameer M. Patil, proprietor of M/s Samir Patil Group of Companies, Pune (hereinafter referred to as SPGOCP).

d. Loan taken from Saraswat Co-operative Bank became NPA in September 2017 due to non-payment of its installments. The bank took the action under SARFAESI Act, 2002 (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) and took the symbolic possession of the property of the Company on 24th April 2018 and District Magistrate issued an Order for taking over physical possession of the property of the Company.

e. The Complainant observed the discrepancies in the financial statements of the Company for the financial year 2017-18 audited by the Respondent.

CHARGES IN BRIEF:

2. The Complainant has alleged that the Respondent being statutory auditor of the Company by acting hand in glove with the management of the Company had manipulated the figures of the financial statements and thereby he had failed to show True and Correct picture of Company in his audit report on the financial statements of the Company for the financial year 2017-18 and also did not provide him the copy of the said financial statements. The Complainant vide his complaint dated 26th February 2019 has levelled 8 allegations against the Respondent out of which the Director (Discipline) has made him Guilty under only 4 charges. The details are as under:

| S. No. | Allegations | View of Director (Discipline) |

| 1. | Provision of Rs. 19,31,71,791/- against the Construction Expenses Payable is made without verifying any accounts only on the basis of representation of the management | Held Not Guilty.* |

| 2. | Wrong disclosure in Audit Report that no litigation expenses pending against the Company as the proceedings by Saraswat Co-operative bank under SARFAESI Act was pending | Held Guilty |

| 3. | Actual value of the land of hospital is more than the value shown in financial statement | Held Not Guilty |

| 4. | No documentation was made for Short term loan and Advances shown in financial statements | Held Guilty |

| 5. | No documentation was maintained for Loan from Mrs. Smeeta Patil shown in financial statements | Held Guilty |

| 6. | Valuation of Building was missing in financial statements. | Held Guilty |

| 7. | Respondent has manipulated the figures of the financial statements of the Company for the F.Y. 2017-18 by acting hand in glove with the management of the Company |

Held Not Guilty |

| 8. | Not provided the copy of the financial statement of the Company for the F.Y. 2017-18 to the Complainant. | Held Not Guilty |

* The Disciplinary Committee at the time of consideration of the prima-facie decided to investigate on this allegation also.

3. The Committee noted that the Respondent in his reply at the stage of PFO had, inter-alia, mentioned as under:

a. That merely because the Company was involved in the procedure under SARFAESI Act, 2002 does not mean that the Company was into litigation with the bank which would further impact or hinder the financial position of the Company. Apart from this, the Company was making efforts to enter into an OTS (One Time Settlement) with the bank and trying to settle the matter.

b. The amount shown under the head ‘Short term Loans and Advances’ examined and verified with the relevant documents produced to the Respondent. These documents are forming part of his working papers.

c. Documentary evidence is available with the Company about the Loan from Mrs. Smeeta Patil of Rs. 69,35,042/- during the Financial Year 2107-18. The same could also be verified from the bank statement of the year also. Further, she was a director in the Company, hence, no permission was required from any regulatory authority for such loan. The amount infused from the above loan was utilized towards repayment of loan from the Saraswat Co-operative bank, payment to various vendors of the Company relating to the project.

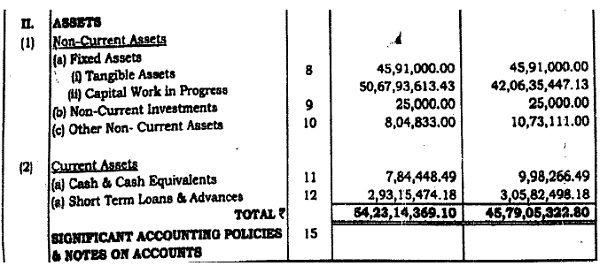

d. Regarding the allegation of valuation of building, the Respondent stated that the same is shown as ‘Capital Work in Progress’ for an amount of Rs. 50,67,93,613.43/- in the financial statement of the Company as on 31st March 2018. This amount constitutes the capital expenditure incurred by the Company on civil construction of the hospital building which was yet to be completed.

4. The Director Discipline had in his Prima facie Opinion dated 6th July, 2020, noticed that:

4.1 With respect to charge related to pendency of proceedings against bank under SARFAESI Act, it was noticed as under:

a. That since the proceedings under this SARFAESI were similar to the proceedings under the Insolvency/Liquidation hence the fact was required to be disclosed while presenting its financial statements, but the same was not disclosed.

b. The Respondent under para “Repayment of Loan” in Annexure A of his report under the requirement of Companies (Auditor’s Report) Order, 2016 had not mentioned the name of the bank and the period of default which were as per the requirement of the said Order to be mentioned in the report.

c. It was noticed that there was an Order of the District Magistrate on 27th April, 2018. The same was after the date of financial statements for the Financial Year 2017-18 but before the date of its approval on 29th September, 2018 i.e. on the date of AGM of the Company. Impact of the order was not incorporated by the Respondent in his reporting as events occurring after balance sheet date.

d. Balance of secured Loans from Saraswat Cooperative bank for the F.Y. 2017-18 was Rs. 1462.87 Lacs against the Total Long-term borrowings of Rs. 2217.24 Lacs which is around 65.97% of the long-term borrowings. Further, in Note no.6 – Other Current liabilities, there was a balance of Rs. 188.51 lacs under the head Interest payable on term loans in respect of which there was default in repayment of dues. Thus, in around 65.97% of the long term borrowings, there was default in repayment of dues.

e. Further, the Respondent with respect to the other matters to be included in the Auditor’s report in accordance with Rule 11 of the Companies (Audit and Auditors) Rules 2014 reported that the Company did not have any litigation pending which would impact its financial position.

f. Also, in the Notes to Accounts, under the head, events occurring after the Balance sheet date, the Respondent reported that there were no events occurring after the Balance sheet date till the date of completion of audit which requires separate disclosure. Thus, the reporting done by the Respondent in his audit report was not complete.

4.2 With respect to charge related to non-documentation for short term loans and advances, it was noticed that the Respondent by not taking the balance confirmation from the parties has failed to discharge his professional duty.

4.3 With respect to charge related to non-documentation for loan from Mrs. Smeeta Patil, it was noticed that the Respondent was silent in his submissions as to whether he had verified any Board resolution or any certificate received from Director about the source of funding required as per Section 179(3) of the Companies Act, 2013. He just mentioned about the verification of bank statement at the time of audit and had brought on record the ledger account of Mrs. Smeeta Patil in the books of the Company. Thus, it was felt that the Respondent had not applied required due diligence while certifying this amount and had not verified the relevant documents with respect to loan from one of the directors of the Company.

4.4 With respect to charge related to missing of valuation of building in financial statements noticed that the Respondent has not provided any document like copy of any invoice, external confirmation etc. verified by him to satisfy the sufficiency and accuracy of disclosure of material amount appearing in the Financial Statements of the Company. Thus, on account of non- seeking of sufficient audit evidence, the Respondent is held prima-facie Guilty in respect of this allegation.

5. Accordingly, the Respondent was held Prima-facie Guilty of Professional Misconduct falling within the meaning of Items (5), (7), and (8) of Part I the Second Schedule to the Chartered Accountants Act, 1949.

6. The said items in the Schedule to the Act states as under:

Item (5), (7) and (8) of Part I of the Second Schedule.

“A Chartered Accountant in practice shall be deemed to be guilty of Professional Misconduct if he: –

(5) fails to disclose a material fact known to him which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where he is concerned with that financial statement in a professional capacity.”

(7) does not exercise due diligence or is grossly negligent in the conduct of his professional duties.”

(8) fails to obtain sufficient information which is necessary for expression of an opinion, or its exceptions are sufficiently material to negate the expression of an opinion.”

SUBMISSIONS OF THE RESPONDENT IN RESPONSE TO PRIMA FACIE OPINION:

7. The Respondent had, inter-alia, made the submissions dated 9th December, 2020 in response to Prima Facie Opinion which were as under: –

a. As regards first charge, it was submitted that the addition to long term provision was Rs 606.76 lakhs and which was attributed towards Capital Work In Progress. Further, during Statutory Audit, he evaluated the information/explanation obtained through inspection/verification, etc. and also conducted physical site/ project visit and made inquiries there at as audit evidence.

b. As regards second charge, it was submitted that during the course of audit no documents relating to pending litigation (if any) were provided to him, except notes to accounts confirming that the Company does not have any pending litigation and which had any impact on financial position and there were no events occurring after Balance sheet date.

c. Without placing full reliance on oral submission, he in order to assess the probability of existence of any litigation, has carried out the analysis of existing obligation.

d. Further, before concluding as to presence or absence of any litigation which would impact its financial position, the Respondent obtained the schedules, notes to accounts prepared on “Going concern basis” also.

e. That during the course of proceedings before Disciplinary Directorate (at prima-facie stage), the Respondent was supplied with the copy of order of Hon’ble DRT (Pune) dated 27th April, 2018 by the Disciplinary Directorate. The same was brought to the notice of the Company and on the same it was replied by the Company that, during the tenure of audit, they were not in possession of any such information. It was also informed that in their WRIT they had also mentioned that they were not served upon any such communication by the bank till the date of filing of WRIT.

f. As regards to third charge, it was submitted that the Respondent had exercised his due diligence and balance confirmations as compelling evidence were vouched. In the absence of negative observations upon the subject matter, the Respondent only stated the matter under ‘Emphasis of Matter’.

g. As regards to fourth charge, it was submitted that the Respondent had verified various documents related to the matter, also undertaken critical analysis tracking the movement of funds from the stage of receipt of from the party till the utilization thereof towards payment of bank dues and vendor advances etc. Also confirmed that no interest has been paid/ credited to the party.

h. As regards to fifth charge, it was submitted that the Respondent before forming an opinion on capital work in progress had evaluated various documents as audit evidence and also conducted physical site visit and inquiries conducted thereat with the third party deployments/ personnel. The documents obtained from the Company were found to be consistent with that obtained from third party.

BRIEF FACTS OF THE PROCEEDINGS

8. The Committee noted that the instant case was fixed for hearing on following dates: –

| S. No | DATE | STATUS OF HEARING |

| 1. | 27.12.2021 | Adjourned due to paucity of time |

| 2. | 11.04.2023 | Part heard and Adjourned |

| 3. | 28.07.2023 | Part Heard and Adjourned |

| 4. | Concluded. Judgment Reserved | |

| 5. | 18.09.2023 | Final decision taken on the case |

9. On the day of first hearing held on 27th December 2021 the hearing was deferred due to paucity of time.

10. On the day of second hearing held on 11th April 2023, the Committee noted that the Complainant was present through Video Conferencing mode. The Committee further noted that the Respondent alongwith his Counsel CA. Shashikant Bharve were present through Video Conferencing mode. Both parties were administered an Oath. Thereafter, the Committee enquired from the Respondent as to whether he was aware of the charges. On the same, the Respondent replied in the affirmative and pleaded Not Guilty to the charges levelled against him. Thereafter, looking into the fact that this was the first hearing before the present bench, the Committee decided to adjourn the hearing to a future date. With this, the hearing in the matter was partly heard and adjourned.

10.1 The Committee also noted that the Respondent had made submissions dated 7th April 2023 wherein he had, inter-alia, mentioned as under: –

a. Principles of Natural Justice have not been followed by adding the charge rendering the proceedings as improper.

b. There is clearly an attempt on the part of the Complainant to make wrongful use of Disciplinary mechanism of ICAI by trying to make the Respondent being the auditor of the Company as a scapegoat when the issues raised factually relate to the differences of opinion and actions between the Complainant and the other shareholders/directors of the Company.

c. The Complainant has certain claims against the Company which are under dispute.

d. With respect to charge 1, the PFO itself has concluded that the Respondent has exercise due diligence in auditing the provision of Construction expenses payable. Further, the Respondent had already specified that the said expenditure was duly authorized by Board resolution, service agreement and all the necessary supporting vouchers.

e. With respect to charge 2, the Respondent was not aware of any recovery proceedings initiated through court by the bank till the audit was completed for FY 2017-18. The Respondent became aware of the OTS and litigations at the time of audit for next year 2018-19 and has accordingly reported therein about the same.

f. With respect to charge 3, the Respondent has provided the balance confirmation letters from the three parties which are amounting to 71% of the Short term loans and advances which are now been located from his working files.

g. With respect to charge 4, the Respondent enclosed a copy of the board resolution for accepting the loans from Mrs. Smeeta Patil and her declaration about the source of funds.

h. With respect to charge 5, that the amount of capital work in progress was checked with relevant vouchers that were available with the Company and are not available on the working file of the Respondent. He has also submitted copy of opinion from the firm of architects indicating the stage of completion. Since the hospital project was not completed hence there is no requirement to disclose the asset wise break up of capital work in progress.

i. The Respondent has acted honestly and had no intention to contravene any provisions of Code of Ethics nor he had contemplated receiving any benefit out of such contravention, if any.

j. On the date of the third hearing held on 28th July 2023, the committee noted that the Respondent and his Counsel CA. Shashikant Barve were present through Video Conferencing Mode. The Committee noted that the Complainant was also present through Video Conferencing Mode. Thereafter, the Respondent was asked to make his submissions.

11.1 The Respondent in his submissions had, inter-alia, made as under:

a. That the Respondent would also like as an abundant caution to point out that the case related to provision for construction expenses payable was gone to NCLT after 2-3 years and this amount was accepted as payable by the Insolvency Resolution Professional.

b. That the Respondent had given the breakup of the expenditure, had given the proper disclosure in Emphasis of Matter and all these items are also appearing in the capital work in progress.

c. With respect to charge no. 2, it is submitted that the concerned year is 2017-18 and notice was given in April 2018 and therefore it is not reported. Infact the reporting has been done that there are no subsequent events after the balance sheet date affecting the financial position of the Company.

d. Further, the audit report was signed on 8th September 2018 whereas one time settlement was done by the Company with the bank on 23rd August, 2018.

e. That around Rs. 16.5 crore was due including interest and there is proposal for one time settlement of dues at Rs. 13 crores. Therefore, the litigation was not reported.

f. Subsequently, after a few months the one time settlement got disputed and in 2018-19, it came to light that this settlement did not take place. However, by that time 2.5 crores had already been paid by the Company.

g. The Respondent has given the entire disclosures in the next year’s report, has reported the material uncertainty related to going concern and has also given the disclosure of pending litigation.

h. With respect to third charge, it is submitted that there were total advances of Rs 2.93 crores out of which balance confirmations of 71% amount were given. Apart from that, advances of Rs 25 lakh have subsequently been settled. So more than 75% balance confirmations have now been made available. These confirmations were lying with the Company and the copies of the same were lying on the files of the Respondent but that working paper file was not traceable at the time of giving reply at the stage of Prima facie Opinion, hence not given at that time.

i. With respect to the fourth charge, it is submitted that at the time of PFO, bank statement and ledger account of the director was given and board resolution was also given. The only thing which was not given was the declaration of the director that the loan was given out of own funds. Now the declaration has been obtained from the director and the same has also been submitted.

j. With respect to the fifth charge, it is submitted that as per Companies Act, 2013 there is no requirement to show project wise capital work in progress. Further, the breakup is also provided in financial statement but item wise declaration is not provided which however is not required.

k. The Respondent has also submitted the copy of Architect certificate stating that how much percentage of work is completed.

11.2 When the Complainant was asked to make his submissions, he submitted that the facts presented by the Respondent are not correct since the Respondent has not disclosed in his report about the action under SARFAESI Act. The Respondent was required to go through the amount. He as an auditor cannot simply go by the management representation.

11.3 The Committee posed certain questions to the Complainant and the Respondent to understand the issue involved and the role of the Respondent in the case. On consideration of the same, the Committee decided to give one more opportunity to Complainant to present his arguments and to submit any further submissions/documents he wants to submit. With this, the hearing in the matter was partly heard and adjourned.

12. On the date of the final hearing held on 23rd August, 2023, the Committee noted that the Complainant Counsel Mr. Ambernath Vibhute, Advocate was present through Video Conferencing Mode. The Committee further noted that the Respondent along with his Counsel CA. Shashikant Barve were also present through Video Conferencing Mode.

12.1 Thereafter, the Committee asked the Complainant’s Counsel to make his submissions. The Complainant’s Counsel in his submissions had, inter-alia, made as under:

a. With respect to first charge, it is submitted that the Written Statement and the Audit Report of the Respondent are contrary to each other. Further, if the Respondent has taken into consideration the management representation then he has to disclose it in writing.

b. With respect to second charge, it is submitted that the Respondent has not disclosed about the pending litigation in his report and explanations given by him are afterthought.

c. With respect to third charge, it is submitted that if the Respondent has taken the balance confirmations from parties he should have reported in his report about the same.

d. With respect to fourth charge, it is submitted that around Rs. 1.93 crores were received from Ms Smeeta Patil without any proof and the Respondent had failed to understand the jugglery of numbers played by her.

e. With respect to fifth charge, it is submitted that the Complainant is leaving the said charge at the Committee’s discretion. That the valuation of the building is wrong as expenses are to the tune of Rs 50 crores, however, the Respondent has shown it to the tune of Rs. 45 crores.

12.2 Thereafter, the Respondent was asked to make his submissions. On the same, the Respondent/ his Counsel, apart from reiterating his earlier submissions made in the previous hearing, submitted that the Committee was not empowered to add such additional charges while making the enquiry. Further, the amount of provision has been accepted by the Insolvency Resolution Professional. The Respondent also briefed his submissions on other allegations which he made in the previous hearing, the same are as under:

a. The Respondent with respect to charge related to pending litigation submitted that the notice received in April 2018 only includes the instruction from collector to the Naib Tehsildar to go ahead in the matter of enforcing and possession however the same never happened.

b. Further, three more notices were issued.

c. Notice issued on 6th July, 2018 mentioned that the possession was expected to be given by 23rd August, 2018.

d. However, before that the Company approached the bank for one time settlement.

e. Thereafter, in September 2018, the same notice was again received wherein the possession date was mentioned as 31st October, 2018.

f. Till February, 2019 the same notice was continued however in March, 2019 it was threatened that the possession may be taken.

12.3 On consideration of the same, the Committee gave directions to the Respondent to submit the following within next seven days with a copy to the Complainant:

a. Reconciliation statement of loan account of Ms. Smeeta Patil.

b. Confirm the dates on which action has been taken under the SARFAESI Act.

c. Copy of three notices/letters relating to proceedings/action under SARFAESI Act

The Complainant was also directed to submit his submissions on the Respondent’s response within 7 days of the receipt of the same.

12.4 Thereafter, the Committee, looking into the Respondent’s submissions against the charges levelled, recorded his plea and accordingly concluded the hearing by reserving its judgment.

13. Thereafter, this matter was placed in hearing held on 18th September 2023 wherein the same members, who heard the case earlier, were present for consideration of the facts and arriving at a decision by the Committee. The Committee noted that pursuant to its direction given in the meeting held on 23rd August, 2023, both the parties had submitted the submissions/documents.

13.1 The Committee noted that the Respondent in his Written Submission dated 26th August, 2023 had, inter-alia, mentioned as under: a. That the Disciplinary Committee had concluded the instant matter in its meeting held on 23rd August, 2023 and had directed the Respondent to submit certain documents in respect of charge no 2 and 4.

a. That the Complainant had referred to an order dated 27th April, 2018 as the matter of pending litigation and was subjudiced with Court, whereas the Respondent signed the audit report on 7th September, 2018.

b. Subsequently, there have been three such notices by the Naib Tehsildar Pune for the execution of the above said notice for taking possession. However, the matter was not executed even till March 2019. The Copies of notices are also attached. Further, the Company went for one time settlement with the bank after receiving the notice dated 27th April, 2018.

c. It is to be noted that the Company had issued the letter dated 23rd August, 2018 about the one time settlement as agreed with the bank whereby total payment of Rs. 13 crore was required to be made against loan outstanding however only Rs. 2.50 crore were actually received by the Bank.

d. Thus, before date of signing of balance sheet, the Company and the directors had agreed with the bank about the one-time settlement and also had acted on the same. Similarly, there had not been the handing over of possession of any of the property even till March, 2019. Further, no such possession of property has been given till year 2021.

e. Thus, there is no case of pending litigation on the date of signing of Balance Sheet having any financial impact.

f. That with respect to charge no. 4, during the hearing the Complainant raised a concern whether the funds were actually brought in by the director Mrs. Smeeta Patil and therefore the Respondent is enclosing a copy of bank statement from the Saraswat Co. Op. Bank which reflects the receipt of loan amount on various dates depending upon the requirements.

13.2 Accordingly, keeping in view the facts and circumstances of the case, the material on record and the submissions of the parties, the Committee passed its judgment.

FINDINGS OF THE COMMITTEE

14. The Committee noted that first charge relates to provision of Rs.19,31,71,791/- against the Construction Expenses Payable is made without verifying any accounts.

14.1 The Committee noted that long term provision as appearing on the face of audited balance sheet and as detailed at note no. 4 annexed to the financial statements was apparently as under:

14.2 Hence, the addition to long term provisions was only Rs. 6,06,76,302/- which relates to current year i.e. 2017-18 and the remaining is the opening balance of financial year 2016-17.

14.3 The Respondent regarding this addition submitted that this long term provision/‘Construction Expenses payable’ constitutes the amount of expenditure which Sameer Patil Group of Companies (SPGOCP) had incurred on the project on behalf of the Company.

14.4 The Respondent also submitted copy of minutes of Board meeting of the Company held on 25th January 2016 wherein vide resolution no. 3, approval was given for execution of an agreement with M/s Sameer Patil Group of Companies to carryout and complete the hospital/ project construction.

14.5 The Committee also noted that the Respondent also submitted copy of agreement entered on 11th February 2016 with M/s Sameer Patil Group of Companies. The Committee on perusal of the same noted that the Complainant was also one of signatory to the agreement.

14.6 The Respondent in his defence also brought management representation letter dated 9th August 2018 regarding confirmation of provision amount of Rs. 606.76 lakhs for construction expenses payable.

14.7 The Committee further noted that the Respondent has also brought on record letter submitted by Company to General Manager, Saraswat Co-operative bank regarding proposal for review of the project wherein the details of investment made by SPGOCP have been submitted, meaning thereby that the Company has given details regarding various amount incurred towards construction and development of the project through SPGOCP till the F.Y 2016-17.

14.8 The Committee further noted that the Respondent had also provided the breakup of figure of Rs. 6,06,76,302/- set aside as provision as under:

| Sr. No. | Particular | Amount |

| 1 | Security and Maintenance | 24,00,000.00 |

| 2 | Plumbing work | 55,30,320.00 |

| 3 | MSEB HT Line Work | 70,20,120.00 |

| 4 | Constructions Expenses | 3,51,71,562.00 |

| 5 | Furniture and Fixtures | 45,54,300.00 |

| 6 | Professional Fees | 60,00,000.00 |

| Total | 6,06,76,302.00 |

14.9 The Respondent also enclosed copy of certificate of the Architect dated 22nd February 2017 whereby he confirmed that 90% of construction work is completed.

14.10 Accounting Standard- 29 ‘Provisions, contingent liabilities and contingent assets’ defines provision as a liability that can be measured using a substantial degree of estimation.

Since this provision involves significant amount of estimation, the Respondent has given proper disclosure regarding this fact under para ‘Emphasis of Matter’ in his audit report to draw user’s attention which is stated below:

‘The said provision has been created in financial statement on the basis of representation made by the management.’

The said fact was also reported under Note no. 4: Long term borrowings in the financial statement of the company for the Financial Year 2017-18.

14.11 Accordingly, the Committee noted that the Respondent had verified the relevant documents related to said provision. Hence, it is concluded that the Respondent has exercised due diligence in auditing the provision of Construction expenses payable. He verified the details of the amount and gave proper disclosure in his report to specifically apprise the fact to the users of the financial statement.

14.12 Thus, on the basis of above facts, the Committee held the Respondent NOT GUILTY of professional misconduct for the said allegation within the meaning of Item (5) and (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

15. The Committee observed that the second charge relates to wrong disclosure in Audit Report wherein it was noted that no litigation is pending against the Company whereas the proceedings by Saraswat Co-operative bank under SARFAESI Act was pending.

15.1 It was noted by the Committee that the loan taken by the Company from Saraswat Co-operative bank became NPA in September, 2017 and the Complainant had submitted a copy of Order dated 27th April, 2018 of District Magistrate wherein it is mentioned that the physical possession of the Company’s property was to be handed over to the Authorized Officer of the Saraswat Co-operative Bank for recovery of its loan from the Company.

15.2 The Committee noted that the Respondent in his submissions has mentioned as under:

a. That he was not aware of any recovery proceedings initiated through court by the bank till the audit was completed for FY 2017-18 as the management made no document available on the subject matter except notes to accounts confirming that the Company does not have any pending litigation which have any impact on financial position and there are no events occurring after balance sheet date.

b. Further, he also sought verbal explanation from the Company before coming to any conclusion.

c. That the attachment of properties was not taken till 2021.

15.3 The Committee noted that during the course of hearing Respondent had submitted 3 more notices from Naib Tehsildar for attachment of properties of Company dated 6th July, 2018, 11th September, 2018 and 11th March, 2019.

15.4 It is seen that after receiving the notice dated 6th July, 2018, the Company went for one time settlement with the bank on 23rd August, 2018 for 6 properties out of 8 properties mentioned in the notice.

15.5 Further, on perusal of One time settlement it was noted that the same was given for Rs 13 crores as under:

| Amount Given by | Date | Amount |

| By The Company (OMRC) | Cheques given on 23rd Aug 2018 | Rs. 3.66 crores |

| By Dr. Anil Varpe | Cheques given on 23rd Aug 2018 | Rs. 3.28 crores |

| By. Dr. Vikas Pol | Cheques given on 23rd Aug 2018 | Rs. 1.39 crores |

| By Dr. Vitthal Baujadi | Cheques given on 31st October 2018 | Rs. 2.33 crores |

| Dr. Rajkumar Gaikwad (Complainant) | Paid separately by Sadhana Gaikwad as per discussion with bank | Rs. 1.00 crores |

| Dr. Rajkumar Gaikwad (Complainant) | NOT PAID | Rs. 1.33 crores |

| TOTAL | Rs. 13.00 crores |

15.6 The Committee noted that out of the above details of Rs. 13 Cr, the payments actually credited (received) by Bank are as under : –

| From Dr. Anil B. Varpe | Rs. 0.87 Cr. |

| From Dr. Vikas Pol | Rs. 0.38Cr. |

| From Dr. Vitthal Bhujadi | Rs. 0.25Cr. |

| From Mrs. Sadhana Gaikwad | Rs. 1.00 Cr. |

| Total | Rs. 2.50 Cr. |

15.7 The Committee noted that the payment was made for only Rs. 2.5 crores hence, it is clear that the one-time settlement offered by the Company was not adhered to. It is further noted that the Company has not gone for any settlement with the bank for the remaining two properties.

15.8 The Committee observed that as per order dated 27th April, 2018 under SARFAESI Act, 2002, the physical possession of the Company’s property was to be handed over to the Authorised Officer of the Saraswat Co-operative Bank for the recovery of its loan from the Company. The Order to attach the Company’s property effects the fundamental accounting assumption of ‘Going concern’ as per paragraph 10 (a) of Accounting Standard – 1 which states as under:

“10 The following have been generally accepted as fundamental accounting assumptions:—

a. Going Concern

The enterprise is normally viewed as a going concern, that is, as continuing in operation for the foreseeable future. It is assumed that the enterprise has neither the intention nor the necessity of liquidation or of curtailing materially the scale of the operations.”

Accordingly, the management of the Company is required to disclose the fact while presenting its financial statements. The proceedings under this act are similar to the proceedings under the Insolvency/Liquidation.

15.9 The Committee further noted that SA 570 (Revised), Going Concern provides guidance on Reporting. However, the auditor’s conclusion on Going Concern Assumption is merely based on the adequacy of disclosures provided by the management. Moreover, it is expected that auditor shall inquire from the management of any events or conditions beyond management’s assessment that may cast significant doubt over going concern assumption as a part of additional audit procedures. The auditor shall evaluate the management’s assessment of going concern thoroughly by obtaining sufficient audit evidences and critically examining the past and present situation of the Company, the progress and the planned course of action in foreseeable future. It may be noted that paragraph 23 of SA 570 (Revised) Going Concern reads as below:

“23. When a material uncertainty exists relating to events or conditions that may cast significant doubt on an entity’s ability to continue as a going concern

‘Implications for the Auditor’s Report Use of Going Concern Basis of Accounting is Inappropriate’

If adequate disclosure about the material uncertainty is not made in the financial statements, the auditor shall: (Ref: Para. A32–A34).

(a) Express a qualified opinion or adverse opinion, as appropriate, in accordance with SA 705 (Revised)4; and

(b) In the Basis for Qualified (Adverse) Opinion section of the auditor’s report, state that a material uncertainty exists that may cast significant doubt on the entity’s ability to continue as a going concern and that the financial statements do not adequately disclose this matter.”

15.10 On perusal of above provisions vis-à-vis order/notices under SARFAESI Act, the Committee noted that though the Bank has not taken over the physical possession of the Company however, it can take the possession anytime since the Company has not made the payment of loan and also for the one time settlement.

15.11 Thus, the Respondent being the auditor of the Company should enquire from the Management as it cast significant doubt on entity’s ability to continue as a Going Concern. Considering the facts of the extant case, the Respondent was required to express modified opinion in his Audit Report. He cannot take the excuse that he was not aware of such order at the time of his audit hence his contention is not tenable.

15.12 The Committee further noted that the Respondent as statutory auditor of the company has disclosed in Annexure A of his report under the requirement of Companies (Auditor’s Report) Order, 2016 under para “Repayment of Loan” as follows:

‘Based on our audit procedure performed for the purpose of reporting the true and fair view of the financial statements and according to information and explanations given by the management, we are of the opinion that the company has defaulted in repayment of dues to a bank as on 31st March, 2018. The Company has outstanding interest of Rs. 188.51 Lacs in the nature of loan or borrowings of a financial institution as on 31st March, 2018.’

The Committee noted that in this disclosure too, the Respondent has not mentioned the name of the bank and the period of default which are as per the requirement of the said Order to be mentioned in the report.

15.13 On perusal of the financial statement of the company for the F.Y. 2017-18, it is noted that in Note no.3 – Long term borrowings, there is a balance of around Rs. 1462.87 Lacs under the head secured loans from Saraswat Cooperative bank against the total long term borrowings of Rs. 2217.24 Lacs. Further, in Note no.6 – Other Current liabilities, there is a balance of Rs. 188.51 lacs under the head Interest payable on term loans in respect of which there is default in repayment of dues. Thus, in around 65 % of the long term borrowings there is default in repayment of dues.

15.14 Further, the Respondent with respect to the other matters to be included in the Auditor’s report in accordance with Rule 11 of the Companies (Audit and Auditors) Rules 2014 reported as under:

“The company does not have any litigation pending which would impact its financial position.”

15.15 The Committee on consideration of the same noted that the Respondent, despite being aware of SARFAESI action against the client, had mentioned in his audit report that no litigation was pending against the Company. The same shows lack of diligence by the Respondent in the conduct of his professional duties. Accordingly, the Committee decided to hold the Respondent GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949 with respect to aforesaid charge.

16. The Committee with respect to third charge relates to no documentation for short term loans & advances, noted that in financial year 2017-18 disclosure regarding short term advances is as under:

16.1 The Committee on perusal of the above noted that out of total short-term loans and advances of Rs. 2.93 crores, approx. Rs 2,21,000/- pertains to 2017-18 and the balance amount were carried forward from last year(s). The Committee noted that the Respondent had submitted a performa invoice dated 13th June, 2017 for the amount of Rs 2,21,000/- to establish his defence.

16.2 As regards other parties, the Committee noted that the Respondent with respect to confirmation of short-term advances had submitted the balance confirmations from 3 parties (viz., M/s Allengers Medical Limited, M/s Medimek Industries and M/Elite Main) which constitute 71.25% of the total short term loans & advances.

16.3 The Committee noted that since the confirmation for a substantial amount is taken by the Respondent, it cannot be presumed that no documentation is

available with the Respondent regarding Short term loans & Advances.

16.4 Accordingly, held him NOT GUILTY of professional misconduct for the said allegation within the meaning of Item (7) and (8) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

17. The Committee with respect to fourth charge related to no documentation maintained for loan from Mrs. Smeeta Patil (one of the directors of the Company) observed that as per section 73 (2) of the Companies Act, 2013 read with Companies (Acceptance of Deposits), Rules, 2014, the loan received by the Company from its directors shall be considered as exempted deposit. Further, the loan given by the director or his/her relative should be out of his/her own funds and not from borrowed funds and the Company should obtain such declaration from the said director before accepting the loan.

17.1 The Committee noted that the Respondent in his defence had also submitted the board resolution wherein the resolution was passed by the members of board to accept the said loan. The Respondent has also submitted the copy of bank statement to show the movement of transactions and ledger account of Mrs Smeeta Patil.

17.2 The Committee noted that the Respondent has brought on record the declaration from Mrs. Smeeta Patil wherein it is accepted by her that the loan given by her was out of her own funds and not from borrowed funds.

17.3 Further, the Respondent in financial statement of the Company for 2017-18 has given the disclosures in notes to accounts for the same.

17.4 Thus, on the basis of above facts, the Committee concluded that the Respondent has obtained proper documentation for loan from director. Accordingly, the Committee held him NOT GUILTY of professional misconduct for the said allegation within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

18. The Committee with respect to fifth charge related to missing of valuation of Building in financial statement noted that the Respondent in his defence submitted that valuation of building was shown as Capital Work In Progress under the head “Non- current assets” to the tune of Rs. 50,67,93,613.22/-. The Committee on perusal of the Balance Sheet for the F.Y. 2017-18 noted that the same is disclosed as under:

18.1 The Committee noted that the addition in current year work in progress as compared to the previous year was approx. Rs. 861.58 lakhs.

18.2 The Committee noted that the bifurcation given for above figure by the Respondent is as under:

| a. | Construction expenses payable (as mentioned in para 14.8 above) | Rs. 606.76 Lakhs |

| b. | Interest accrued/paid/payable in respect of bank borrowings | Rs. 188.51 Lakhs |

| c. | Construction expenses incurred by the Company | Rs. 66.31 Lakhs |

| Toral | Rs. 861.58 Lakhs |

18.3 As regards Interest accrued/paid/payable in respect of bank borrowings, the Committee noted that the Respondent had brought on record loan account statement. Further, the Respondent had brought on record copy of certificate obtained from Chartered Architect detailing the stage of completion in respect of both the financial years 2016-17 and 2017-18 wherein it was mentioned that the 90% of Construction work is completed and all other works of building are in progress.

18.4 Apart from the same, the Committee noted that the Respondent had also provided the break-up of the same as under:

| Sr. No. | Particular | Amount |

| 1 | Govt. License Fees | 90,86,631.67 |

| 2 | Operative Expenses | 12,12,22,813.46 |

| 3 | Construction Expenses | 31,78,74,939.00 |

| 4 | Electric Work | 12,00,028.09 |

| 5 | Fire Fighting system | 5,88,395.00 |

| 6 | Land excavation for Hospital | 57,47,136.00 |

| 7 | Furniture | 3,53,67,095.00 |

| 8 | Equipment | 1,57,06,575.00 |

| Total | 50,67,93,613.22 |

18.5 The Committee further noted that the Respondent has verified the various documents such as copy of bank/loan statements to evaluate the time period for which the interest was capitalized and confirm the accuracy of the transaction, Copy of ledger account of capital work in progress as appearing in the books of accounts depicting accumulation to the projects, copy of purchase order, vouchers, tax invoices, etc. in relation to expenses directly incurred by the Company.

18.6 Thus, on the basis of above facts, the Committee concluded that the Respondent has obtained sufficient audit evidence before giving any opinion in the instant matter. Accordingly, the Committee held him NOT GUILTY of professional misconduct for the said allegation within the meaning of Item (5) and (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

CONCLUSION

19. In view of the findings stated in above paras vis a vis material on record, the Committee gives its charge wise findings as under:

| Charge | Findings (para ref.) | Decision of the Committee |

| Provision of Rs.19,31,71,791/- against the Construction Expenses Payable is made without verifying any accounts only on the basis of representation of the management. | 14 to 14.12 | Not Guilty – Item (5) and (7) of Part I of the Second Schedule |

| Wrong disclosure in Audit Report that no litigation pending against the Company as the proceedings by Saraswat Co-operative bank under SARFAESI Act was pending. | 15 to 15.15 | GUILTY – Item (7) of Part I of the Second Schedule |

| No documentation was made for Short term loan and Advances shown in financial statements. | 16 to 16.4 | Not Guilty – Item (7) and (8) of Part I of the Second Schedule |

| No documentation was maintained for Loan from Mrs. Smeeta Patil shown in financial statements. | 17 to 17.4 | Not Guilty – Item (7) of Part I of the Second Schedule |

| Valuation of Building was missing in financial statements. | 18 to 18.6 | Not Guilty – Item (5) and (7) of Part I of the Second Schedule |

20. In view of the above findings stated in the para 19 vis-a-vis material on record, the Committee, in its considered opinion, holds the Respondent GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(MRS. RANI NAIR, I.R.S. RETD.)

GOVERNMENT NOMINEE

Sd/-

(SHRI ARUN KUMAR, I.A.S, RETD.)

GOVERNMENT NOMINEE

Sd/-

(CA. SRIDHAR MUPPALA)

MEMBER

DATE: 07/02/2024

PLACE: NEW DELHI