On August 15, 2025, Prime Minister Narendra Modi delivered a powerful address on the occasion of India’s 79th Independence Day, outlining the Government’s vision for a self-reliant and sustainable future.

The day become more joyous when the Prime Minister of India declared a “Diwali Gift” by way of rationalization of tax rates under India’s Goods and Services Tax (GST) regime with the aim ease the tax burden on essential goods and to lead economic momentum.

This is particularly important given the increasing geopolitical tensions and the tariffs imposed by the United States on India, which have placed significant pressure on various sectors, including automobiles and auto components.

To give a perspective, the Indian automotive industry accounts for nearly 15% of total GST collections and is regarded as a cornerstone of the nation’s economic and technological progress.

To stimulate growth and incentivise the sector, the Government of India in the past have introduced key reforms in the form of FAME scheme, Production Linked Incentive schemes, PM-E Drive among other initiatives.

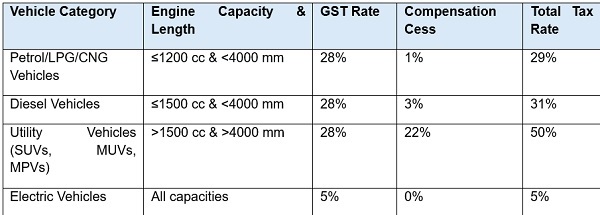

However, looking at the GST rates on the automotive sector, it appears that the rates has been disproportionate due to its placement in the highest tax bracket, as depicted in the table below:

This high tax burden not only inflates the vehicle prices but also dampens the consumer demand, and limits affordability. Thus, this “Diwali Gift” can be considered as a mechanism to boost the domestic demand.

Additionally, the government’s announcement on 15 August 2025 to phase out the compensation cess will create fiscal space for the Centre and provide greater flexibility to align tax rates for long-term sustainability.

Proposed Rationalization: A Game-Changer

As a part of major restructuring in the GST tax structures, the Government is now considering to retain only the 5% and 18% slabs with a special slab of 40% for luxury/ Sin goods, which could be transformative for the automotive sector as:

- Lower tax rates would make vehicles more affordable to the common people as the small vehicles are expected to be placed at 18% tax bracket, whereas the luxury vehicles are expected to be taxed at 40%;

- This increase in domestic demand would enable the Companies, both OEM and Component manufacturers to make up from the loss expected to be suffered from increased US tariffs and consequent drop in the global demand;

- This could lead to improved ease of doing business would attract investments and support Make in India initiative;

- Could lead to positive impact such as increase in investment, manufacturing capacity, Job creation;

- Simplified rates would reduce compliance burden;

- It is expected to reduce classification disputes, simplifying operations and lowering litigation risks in the longer run

All in all, the proposed GST rate rationalisation, combined with other Scheme offers a promising roadmap for revitalising India’s automotive sector even in the geopolitical headwinds that the world is facing in the longer run.

Challenges ahead:

However, despite the benefits that will accrue due to proposed GST rate rationalization, we anticipate following challenges to sustain at least in short term:

- EV’s might loose out on the competition to the traditional ICE vehicles due to shrinking tax rate gap which at present exists around 24% to 45%, could narrow down to 13% to 35%;

- Inverted duty structure may continue especially for EV’s in case the inputs continues to remain at a higher slab of 18%;

- Slow down can be anticipated in the short run as the dealers would be pushing to liquidate the existing inventory first and will be waiting for rate cuts before piling the stocks;

- End consumer would be delaying purchasing decisions till implementation of the rate cuts;

- These rate cuts would be a test of Cooperative Federalism as the State Government could resist tax cuts due to anticipated loss of GST revenue;

- Impact on Incentives: The GST rate rationalization could have significant implications for Companies availing state/ Central incentives, especially those based on GST payout. As many state industrial policies were framed assuming the original GST rates, the reduction in rates lead to reduced incentives payout and thus could make many projects unviable.

Way ahead:

The GST rate rationalisation is a reform opportunity but only for those who are wiling to act proactively through strategic preparedness. This could involve:

- Undertaking inventory & repricing decisions so as to ensure that there is no profiteering due to GST rate cuts;

- Conducting impact assessment of the rate cuts on margins, products, pricing etc.;

- Representing before Government and seeking solutions for issues such as inverted duty structure;

- to re-negotiate the existing incentives MOU’s between the State and the applicant to reflect the impact of reduced GST rates so as to avoid future disputes or delays in Incentives;

- Revisiting vendor and client contracts to adopt to new pricing based on revised GST rates;

- Re-configuration of IT Systems & ERP to adopt the updated rates from the appointed date;

- Working closely with distributors, dealers, and retailers to ensure uniform understanding of revised rates and documentation processes.

While GST rationalization offers a powerful stimulus to the Indian auto industry by boosting affordability for entry-level vehicles, trimming costs across the value chain, and igniting investor confidence in the longer run, the industry should also gear itself for the short-term challenges the rate cuts would inherent.

Author Bio