Investor Education and Protection Fund Authority

Ground Floor, Jeevan Vihar Building, 3,

Parliament Street, New Delhi-110001

File No: IEPFA-13/13/2022

Dated: 09th January, 2023

NOTICE

Sub: Notice inviting comments from various Stakeholders on Consultation papers for refund process of IEPF Authority

Investor Education and Protection Fund Authority invites comments on the consultation Paper on refund process at IEPF Authority to simplify and expedite the process of claim refund filed with IEPF Authority under Companies Act 2013.

2. The comments may be suggested through e- consultation module available at MCA website and via email iepfa.consultation@mca.gov.in at till 27th January, 2023. Comments may be provided in the following format (soft copy as well as in signed pdf):-

| S.N | Para of consultation paper | Comments | Justification |

(Gaurav Gupta)

Deputy Director

IEPF Authority

Annexure A

Consultation Paper on refund process at IEPF Authority

A. Objective: To simplify and expedite the process of claim refund filed with IEPF Authority under Companies Act 2013.

B. Background: Government of India, has in accordance with the provisions of subsection (5) of section 125 of Companies Act, 2013, established IEPF Authority (the Authority) for administration of the Investor Education and Protection Fund (the fund). The Authority has been entrusted with the responsibility to administer the fund as per section 125 (3) of Companies Act 2013 which mandates utilization of fund for:

(a) the refund in respect of unclaimed dividends, matured deposits, matured debentures, the application money due for refund and interest thereon;

(b) promotion of investors’ education, awareness and protection;

(c) distribution of any disgorged amount among eligible and identifiable applicants for shares or debentures, shareholders, debenture-holders or depositors who have suffered losses due to wrong actions by any person, in accordance with the orders made by the Court which had ordered disgorgement;

(d) reimbursement of legal expenses incurred in pursuing class action suits under sections 37 and 245 by members, debenture-holders or depositors as may be sanctioned by the Tribunal; and

(e) any other purpose incidental thereto, in accordance with such rules as may be prescribed.

2. For the purpose of facilitating refund of claims in respect of shares, unclaimed dividends, debentures etc. the Central Govt. has on 05.09.2016 notified Investor Education and Protection Fund (Accounting, Audit, Transfer and Refund) Rules, 2016. For effecting transfer of shares to the Authority, two DEMAT Accounts, one for each of the depositories have been opened. NSDL and CDSL have been engaged as depositories to maintain the DEMAT accounts of the Authority.

3. IEPF Fund:

| Financial Year | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | 2022-23# |

| Total Balance amount in the IEPF at the end of the year (in Rs. crore) | 1,673.20 | 2,016.72 | 2,423.19 | 4,310.36 | 4,816.03 | 5,262.25 | 5,685.25 |

| Total No. of Unclaimed Shares in the IEPF at the end of the year (In lakhs) | NIL* | 4,729.52 | 6,482.11 | 7,932.58 | 9,192.78 | 10,552.24 | 11,688.37 |

*The first due date of transfer of shares by companies was 31.10.2017.

##The data is provisional upto 30.11.2022.

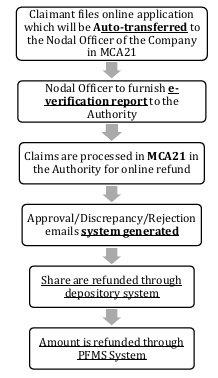

4. Refund from IEPF: For filing refund with the Authority, the investors make an online application on the website of the Authority (www.iepf.gov.in). These refunds are settled after verification of the claims by the companies. The flow chart of the claim process is as below:

5. Broad categorization of claims filed with Authority:

| Shares in the name of | Form filed by | Type of claim | Remarks |

| A | A | Demat | Source & Destination demat account same |

| A | A | Demat | Source & Destination demat account different |

| A | A | Physical | Physical to Demat account |

| A | B | Physical | Death of A, Physical to Demat account |

| A and B | A | Physical | Death of B, RTA to delete name of B |

| A and B | C | Physical | Death of A & B, transmission executed by RTA |

| A | B | Physical | Shares sold by A to B, transfer deed executed by RTA |

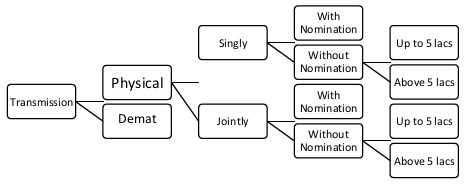

6. Categorization of transmission claims filed with Authority:

7. Major documentation requirement for claims filed with Authority as per Standard Operating Procedure:

| Cases | Documents Required |

| Minor Difference in Name | Same name affidavit |

| Major name in Difference | Newspaper or Gazette Publication |

| Difference in address | Notarized Affidavit and New address Proof |

| Loss of Original Security | FIR Copy, Indemnity, Surety Bond, Newspaper Advertisement (depending on valuation of securities) |

| Unclaimed Suspense Account | Transaction statement and CML of Company’s Unclaimed Suspense Account |

| Name Difference on Death Certificate | Same name affidavit by Legal Heir |

| Claim with No excel data in MCA 21 | On the basis of challan & year wise details submitted by the company duly verified by the Nodal Officer evidencing that the amount and share actually transferred to IEPF. |

8. Major reasons for discrepancies in claim filed with the Authority:

- In case of Physical securities: Folio no. is not mentioned or not correctly mentioned

- In case of Demat securities : Demat Account number is not mentioned or not correctly mentioned

- Wrong or Incomplete Aadhaar/ Passport detail

- Wrong or Incomplete Bank Account Detail

- Wrong or Incomplete Demat Account Detail

- Physical Securities Certificate Lost/ Misplaced and Documents for Loss not provided or Transmission documents not provided as per Schedule II

- Client Master list is not provided

- Mismatch in name and address of claimant with KYC and company records

- Indemnity Bond executed on plain paper

9. Major reasons for rejection in claim filed with the Authority:

- Claim rejected by Company in its verification report

- Duplicate Claims filed by Claimant

- Verification report is not filed by the company within timelines prescribed under rule 7(3) or revised verification report is not filed by the company within timelines prescribed under rule 7(7)

- Claim filed in the name of deceased shareholder

- Request received from the companies in case of merger, demerger, amalgamation etc

10. Claim and refund statistics:

Detail of Claims filed & disposed as on 30th Nov 2022 (Provisional) is as below:

| Sl No. | Particulars | 2016-17 to 2019-20 |

2020-21 | 2021-22 | 2022-23 $ | Total |

| 1. | No. of applications (e-form IEPF 5) filed on MCA – 21 System | 39,723 | 14,032 | 28,647 | 22,944 | 1,05,346 |

| 2. | No. of applications for which verification report received in the Authority during the period | 25,676 | 10,702 | 23,083 | 19,332 | 78,793 |

| 3.

(a) (b) |

No. of applications settled | 9,367 | 14,219 | 25,021 | 16,067 | 64,674 |

| Approved | 7,866 | 7,262 | 10,472 | 5,840 | 31,440 | |

| Rejected | 1,501 | 6,957 | 14,549 | 10,227 | 33,234 | |

| 4. | No. of shares refunded | 63,37,539 | 37,72,666 | 61,21,291 | 55,37,915 | 2,17,69,441 |

| 5. | Amount refunded (in Rs.) |

9,66,5 5,599/- | 7,05,6 4,324/- | 10,85 ,52,226/- | 4,05,8 1,513/- | 31,63,5 3,662/- |

11. Steps taken by IEPF Authority to ease the process of claim refund:

The Authority regularly invites suggestions from industry, companies and investors to make the process more investor friendly and relaxations and amendments are made in rules accordingly. A process re-engineering was carried out in the claim settlement process by amending rules under TheInvestor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund) Rules, 2016 in August 2019. The salient changes were as enlisted below:

- A new simplified web based e-form IEPF-5 having features of PAN based verification was implemented.

- Online processing of e-form IEPF-5 by the companies and submission of verification reports to the Authority.

- Standard document list and Standard Operating Procedure for processing of claims including those involving transmission and loss of share certificates prescribed through Schedules.

b. Subsequently, rules were further relaxed through Investor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund) Second Amendment Rules 2021. Changes were as below:

For Claimants:

a) Requirement of Advance Receipt has been waived off.

b) Requirement of Succession Certificate/ Probate of Will/ Will has been relaxed up to Rs 5,00,000 (five lacs) both for Physical & DEMAT shares.

c) Notarization of documents has been replaced with self-attestation and d) requirements of Affidavits and Surety relatively have been eased.

For Companies:

a) Requirement of attaching documents related to Unclaimed Suspense Account has been eased.

b) Companies have been given flexibility to accept transmission document viz. Succession Certificate, Will etc. as per their internal approved procedures.

c) Newspaper Advertisement requirement for loss of physical Share Certificate has been waived off up to an amount of Rs.5,00,000.

C. Current regulatory provisions for IEPF Claim refund Process: The current rules are prescribed under IEPFA (Audit, Account, Transfer and Refund) Rules ..

2. Some of the observations on the current process are as below:

a. According to rule 7 of Investor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund) Rules, the claim filed to the authority needs to first verified by the Companies. The companies are mandated to send an e-verification report along with documents submitted by the claimant. There is often a considerable delay in submission of the e-verification report by companies or the companies submit report without requisite documents required under the rules or the companies reject the claim in its verification report without intimating the claimant.

b. Currently, there is a provision of levying additional fee for delay in filing of verification report by the company to the tune of Rs 50 per day, maximum up to Rs 2500, beyond the timeline of 30 days from the date of filing of the claim by the claimant. After the timeline of 75 days, the company and its nodal officer are punishable as per the provisions of the Act.

c. Though standard list of documentary requirement has been prescribed through schedules in the rule, some companies insist on additional documents or verification, even physical verification in some cases. Some companies do not enclose all the mandatory documents prescribed under the rules while forwarding the verification report, as a result of which the Authority seeks additional documents in order to comply with the rules. It is noticed that submission with incomplete set of documents is often done to comply with the deadline and avoid additional fee.

d. As real-time information on the claim along with verification report submitted by company is not available to the claimant, it creates information asymmetry for the claimant. The delay attributable to the process of reverification by companies or seeking additional documents by the companies/authority makes the process of claim, time consuming for the claimant.

e. More than 50 percent of cases involve scenarios, where claimant has lost original share certificate/dividend warrants/bond/ debenture certificate etc. or there is change in name or there is a case of transfer or transmission etc. Thus, there is issue of establishment of entitlement as these claims pertains to securities issued prior to DEMAT era and do not have KYC seeded to it.

f. The Authority processes the claims using the MCA 21 where processing is enabled on First in First out (FIFO) Logic. However, claims which are pertaining to original shareholders are also getting clogged due to entitlement issues and verification of claims categorized under bullet e.

g. The Authority refunds shares in DEMAT form to the DEMAT account of the claimant and the unclaimed money in the bank account of the claimant through Depositories and PFMS System respectively which have separate maker, checker and verifier roles.

D. Suggestions to ease the process of claims and refund: In order to ease the process of refund, suggestions are invited on the following options:

a. Realtime Online interface between IEPFA, Claimant and Company: After the claim is filed by the Claimant, the Claimant and the Company will be able to iterate the case between them online on realtime basis, till documentary requirements are complete and case is considered for final approval by the company. The IEPFA will enforce the timelines and the documentation procedure within which the Company has to dispose the claim.

b. Cases, claims are proposed to be categorised according to their nature (Loss cases, Transfer, Transmission, Death Cases, Name Change etc.) and also on the threshold of their market value. Certain type of claims below a threshold, for the same shareholder/investor, where there are minor changes like address change, bank account number change can be made STP (Straight Through Process) based on approval report of the company.

c. Documentary requirement can be further relaxed with the Authority continuing to process the claim above the threshold and doing share transfer and amount transfer to claimant. This will resolve the issue of rejection of the cases at the end of company and will provide real-time status and monitoring of the case to all stakeholders

d. Shares transferred through Reverse Corporate Action: After the approval, share and amount will be transferred by the Authority to the respective company through reverse corporate action, which in turn will transfer the same to respective claimants. Company will be responsible to transfer the shares and amount to claimant through corporate action, once it is received by it from IEPFA. The Authority will enforce the timelines through penalties and interest.

e. Limitation Threshold: It can also be considered to bring a limitation threshold (in years, say 10 years from date of transfer of shares to Authority) after which the Authority can sell the shares to convert it into amount and the claimant can claim the amount so realized. This can be considered as a measure of Investor Protection as Companies undergo many corporate restructurings including merger, demerger, delisting etc. Also, in case of such restructuring or in case company fails or become insolvent, the value of the share gets eroded. After a period of limitation (say 20 or 25 years), the claims can be considered time barred.

E. Questions which may be considered for suggestions:

a. Should the approval process of claims filed remain with Authority, or delegated to Company up to a certain threshold for certain types of claims, or delegated completely?

b. Should the shares and amount be transferred by the Authority directly to the claimant or to the company which will further transfer it to the claimant?

c. Should any threshold of limitation be brought by which claims can be settled only as a value of share or time barred?

*********