Case Law Details

Ashirwad Equipment Pvt. Ltd. Vs Commissioner of Central Excise & CGST (CESTAT Allahabad)

The appeal arose from an order rejecting the appellant’s claim for interest on the refund of ₹8,37,939, while allowing interest at 6% only on the statutory pre-deposit of ₹84,609 under Section 35F of the Central Excise Act, 1944, as made applicable to service tax matters through Section 83 of the Finance Act, 1994. The refund itself had been sanctioned after the CESTAT allowed the appellant’s earlier appeal and set aside the service tax demand, interest and penalties.

The department had initiated proceedings alleging non-payment of service tax on mining services and supply of tangible goods for the period 2008-09 to 2010-11. A show cause notice was issued, followed by an adjudication order confirming the demand along with interest and penalties. The appellant’s appeal before the Commissioner (Appeals) was rejected, after which the CESTAT allowed the appeal. Pursuant to the Tribunal’s order, the refund of ₹9,52,798, comprising ₹84,609 as pre-deposit, ₹8,37,939 as service tax and interest only on the statutory pre-deposit, was sanctioned. The appellant sought rectification, contending that interest should also be granted on ₹8,37,939, but the department rejected the request on the ground that the amount had been deposited as service tax and not as a pre-deposit under Sections 35F and 35FF. The Commissioner (Appeals) upheld that view, leading to the present appeal.

The Tribunal examined the factual record and noted that after issuance of the show cause notice, the appellant had deposited ₹8,37,939 and later made an additional deposit of ₹84,609 while filing the appeal before the CESTAT. It further observed that the Commissioner (Appeals), while entertaining the first appeal, had expressly recorded satisfaction that the appellant had complied with the mandatory pre-deposit requirement under Section 35F. The appeal memorandum also disclosed that the amounts of ₹4,12,000 and ₹4,25,939 deposited through challans dated 13.05.2015 formed part of the deposits relied upon for maintaining the appeal. The Tribunal found that the revenue had never disputed this factual position or challenged the Commissioner’s finding regarding compliance with Section 35F.

The Tribunal held that the subsequent refund order incorrectly treated the amount of ₹8,37,939 merely as tax deposited against the show cause notice while ignoring the factual position consistently accepted during the appellate proceedings. Accepting the department’s stand would imply that the Commissioner (Appeals) had entertained the appeal without ensuring compliance with the mandatory pre-deposit requirement, which was contrary to the record. Accordingly, the Tribunal concluded that the deposits of ₹4,12,000 and ₹4,25,939 together amounting to ₹8,37,939 had been treated as pre-deposit for hearing the appeal under Section 35F read with Section 83 of the Finance Act, 1994. Consequently, refund of the said amount was also governed by Section 35FF, entitling the appellant to statutory interest.

The Tribunal further observed that the impugned order proceeded on a legal proposition without properly examining the facts on record. It referred to the Board Circular dated 10.03.2017, which provides that where an appeal is decided in favour of the assessee, refund of the pre-deposit must be granted along with interest under Section 35FF from the date of deposit until the date of refund. The Tribunal held that subordinate authorities could not introduce qualifications inconsistent with the circular. Having decided the matter on the factual findings, the Tribunal found it unnecessary to examine the judicial precedents cited by the appellant.

Holding that the impugned order could not be sustained, the Tribunal allowed the appeal and held that the amount of ₹8,37,939 was to be treated as pre-deposit under Section 35F, making it eligible for interest on refund under Section 35FF of the Central Excise Act, 1944 read with Section 83 of the Finance Act, 1994.

FULL TEXT OF THE CESTAT ALLAHABAD ORDER

This appeal is directed against Order in Appeal NO.259/ST/APPL/ALLD/2025 dated: 03.12.2025 of the Commissioner (Appeal) Central Goods & Service Tax and Central Excise, Allahabad. By the impugned order the appeal filed by the appellant against order in original allowing interest @ rate of six percent on the amount of pre-deposit made in terms of Section 35 F of the Central Excise Act, 1944 read with Section 83 of the Finance Act, 1994 and not allowing interest on the remaining amount has been rejected.

2.1 An inquiry was initiated by the department against the appellants which revealed that during the period 2008-09 and 2010-11 they were providing mining service and supply of tangible goods taxable under section 65(105)(zzzy) and (zzzzj) respectively, of the Act, without obtaining registration and without paying service tax. On completion of enquiry a show cause notice dated 17.10.2013 was issued to the appellants for demanding service tax of Rs. 8,36,086/- under the provision of section 73(1) of the Act, alongwith interest and penalty.

2.2 The demand made was confirmed vide the Order-in-Original No. (ST-168/2013)87 of 2015 dated 21.12.2015, alongwith interest and penalty under section 75 and 78 of the Act, respectively. Besides penalty under section various sub-sections of section 77 of the Act was also imposed

2.3 Aggrieved the appellants filed an appeal before the Commissioner (Appeals) Allahabad, who vide Order-in-Appeal No. 36/ST/Alld/2018dated 11.01.2018 rejected the appeal filed by the appellants.

2.4 Appellant filed an appeal before the CESTAT, which vide Final Order No. 70044/2024 dated 31.01.2024 allowed the appeal of the appellants..

2.5 Vide Order-in-Original No. 175/Div-Vns/Refund/2023-24 dated 21.03.2024, allowed the claim of refund amounting to Rs. 84,609/- against pre-deposit of service tax and service tax amounting to Rs. 8,37,939/- (total Rs. 922548/-) alongwith interest @ 6% p.a. amounting to Rs. 30250/-. Thus in all the refund of Rs. 952798/- was sanctioned to the appellants against their claim of refund.

2.6 Appellant filed for rectification of the impugned order dated 21.03.2024. The Assistant Commissioner vide order dated 16.08.2024 held that:

> the Refund Sanction Order dated 21.03.2024 was sanctioned granting interest only on pre-deposit of Rs. 84609/-.

> no interest was granted on the amount of Rs. 837939/- as the same was deposited under the head of tax prior to filing of appeal and hence the same cannot be considered as amount paid under section 35F/35FF of the Central Excise Act, 1944.

> the application for rectification was disposed of on above observations.

2.7 Aggrieved appellant filed the appeal before Commissioner (Appeal) which has been dismissed as per the impugned order.

2.8 Aggrieved appellant has filed this appeal.

3.1 I have heard Shri Ravi Holani, Advocate for the appellant and Ms Chitra Srivastava, Authorized Representative for the revenue.

3.2 Arguing for the appellant learned counsel submitted:

> The fundamental legal principle, consistently affirmed by superior courts, is that once a Show Cause Notice has been issued, any amount deposited by an assessee, whether characterized as pre-deposit, payment under protest, or during investigation does not constitute payment of duty. Such deposits are in nature of security pending adjudication, and when the demand is ultimately set aside, the entire amount must be refunded with interest. Reliance on following decisions:

-

- Ucal Fuel Systems Ltd. [2014 (306) ELT 26 (Mad)];

- Sinkhai Synthetics & Chemical Pvt Ltd. [2002 (143) ELT 17 (SC)];

- com Pvt. Ltd. [2017 (49) STR (ALL)]

- Parle Agro Pvt. Ltd. [2022 (380) ELT 219 (T-ALL)]

- Emmar MGF Construction Pvt. Ltd. [2021 (55) GSTL 311 (T-Del)]

- Shri Rathi Steel Ltd. [(Cestat ALL – EA 70194 of 2021), order dated 07.06.2024, para 11]

- Asian Paints Ltd. [2023 (2) CENTAX 178 (Guj)]

> Any reliance placed on the decision of the Apex Court in the case of Gujarat Fluoro Chemicals [2014 (1) SCC 126] is totally misplaced, as the assessment framework under Income Tax Act, 1961 is structurally different from Chapter V of the Finance Act, 1994. In this case Hon’ble Apex Court was addressing the specific and narrow question ‘Whether interest is payable by the Revenue to the assessee if the aggregate of installments of Advance Tax or TDS paid exceeds he assessed tax?” which has no application to a deposit mad under protest following the show cause notice.

> Impugned order is manifestly contrary to the decisions of Hon’ble Supreme Court (Sinkhai Synthetics), the Hon’ble Allahabad High Court (Ebiz.com) and multiple Division Benches of this tribunal (Parle Agro, Emmar MGF, Shri Rathi Steel)

3.3 Authorized Representative re-iterated the findings recorded in the impugned order.

4.1 I have considered the impugned order along with the submissions made in appeal and during the course of arguments. I have also taken on record the written submissions filed by the appellant alongwith the email dated 07.06.2026.

4.2 Impugned order records the finding as follows:

“5.3 I have carefully considered the submissions made by the appellants in their grounds of appeal and contents of order in original read with rectification order. I find that the present appeal is limited to the question of sanction of interest on the service tax deposited by the appellants consequent to the issuance of the show cause notice. The Adjudicating Authority had sanctioned the refund of the service tax amounting to Rs. 837939/- without interest and refund of pre-deposit of Rs. 84609/- alongwith interest @ 6%. It was observed by the Adjudicating Authority the since the payment of service tax of Rs. 84609/- was made prior to filing of appeal and as such the same is not covered under section 35F/35FF of the Central Excise Act, 1944. Therefore, no interest is applicable on this amount.

However, the appellants have the contention that since the service tax of Rs. 837939/- was deposited after 06.08.2014 hence interest would be payable.

5.4 In this regard I find that the appellants deposited the service tax of Rs. 837939/- against the demand raised in the show cause notice. To contest the same before First Appellate Authority, they had to make pre-deposit of Rs. 84609/-. By the order of Hon’ble CESTAT Allahabad, the case was decided in favour of the appellants and hence the service tax deposited by the appellants was refunded. Also the refund of pre-deposit was made alongwith interest @ 6% p.a. Now the question before me is to decide as to whether the amount of deposited as service tax is covered under section 35F of the Central Excise Act, 1944. For the sake of brevity the contents of section 35F and 35FF are reproduced as under-

Section 35F Deposit of certain percentage of duty demanded or penalty imposed before filing appeal. –

The Tribunal or the Commissioner (Appeals), as the case may be, shall not entertain any appeal-

(i) under sub-section (1) of Section 35, unless the appellant has deposited seven and a half per cent of the duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance, of a decision or an order passed by an officer of Central Excise lower in rank than the Principal Commissioner of Central Excise or Commissioner of Central Excise;

(ii) against the decision or order referred to in clause (a) of sub-section (1) of Section 35-B, unless the appellant has deposited seven and a half per cent of the duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance of the decision or order appealed against;

(iii) against the decision or order referred to in clause (b) of sub-section (1) of Section 35-B, unless the appellant has deposited ten per cent of the duty, in case where duty or duty and penalty are in dispute, or penalty, where such penalty is in dispute, in pursuance of the decision or order appealed against:

Provided that the amount required to be deposited under this section shall not exceed Rupees Ten crores:

Provided further that the provisions of this section shall not apply to the stay applications and appeals pending before any appellate authority prior to the commencement of the Finance (No. 2) Act, 2014.

Explanation. For the purposes of this section “duty demanded” shall include,-

(i) amount determined under Section IID;

(ii) amount of erroneous CENVAT credit taken;

(iii) amount payable under Rule 6 of the CENVAT Credit Rules, 2001 or the CENVAT Credit Rules, 2002 or the CENVAT Credit Rules, 2004.]

Thus I note that the language of section 35 of the Central Excise Act, 1944 clearly deals with the issue relating to pre-deposit to file an appeal before the Commissioner (Appeals). Since the service tax deposited against the show cause notice issued to the appellants does not amount to pre-deposit hence there is no relevancy of section 35F of the Central Excise Act, 1944. Further section 35FF of the Central Excise Act, 1944 talks about the grant of interest on the amount deposited under section 35F. When initially the deposit of service tax does not qualify the provisions of section 35F, the effect of section 35FF would not come into play. For clarity the contents of section 35FF and Notification No. 24/2014-CE(NT) dated 12.08.2014 is given as under-

Section 35FF Interest on delayed refund of amount deposited under Section 35F. –

Where an amount deposited by the appellant under Section 35F is required to be refunded consequent upon the order of the appellate authority, there shall be paid to the appellant interest at such rate, not below five per cent and not exceeding thirty-six per cent per annum as is for the time being fixed by the Central Government, by notification in the Official Gazette, on such amount from the date of payment of the amount till, the date of refund of such amount:

Provided that the amount deposited under Section 35F, prior to the commencement of the Finance (No. 2) Act, 2014, shall continue to be governed by the provisions of Section 35FF as it stood before the commencement of the said Act.]

Notification No. 24/2014-CE (N.T.) dated 12.08.2014-

In exercise of powers conferred by section 35FF of the Central Excise Act, 1944 (1 of 1944), the Central Government hereby fixes the rate of interest at six percent per annum for the purpose of the said Section.

Thus, I hold that the Adjudicating Authority has rightly refunded the amount deposited as service tax without interest and refund of pre-deposit with interest @ 6% in terms of Notification No. 24/2014 CE (N.T.) dated 12.08.2014 read with Para No 1.3 of the Circular No. 984/08/2014-CX dated 16.09.2014 issued under F. No. 390/Budget/1/2012-JC.”

4.3 Before I further proceed in the matter some facts are essential to be considered. As result of enquiry investigations undertaken a Show Cause Notice dated 18.10.2013 was issued to the appellant demanding service tax amounting to Rs 8,36,086/- for the period 2008-09 to 2010-11. Demand of service tax was made along with proposal for interest and penalty and penalty.

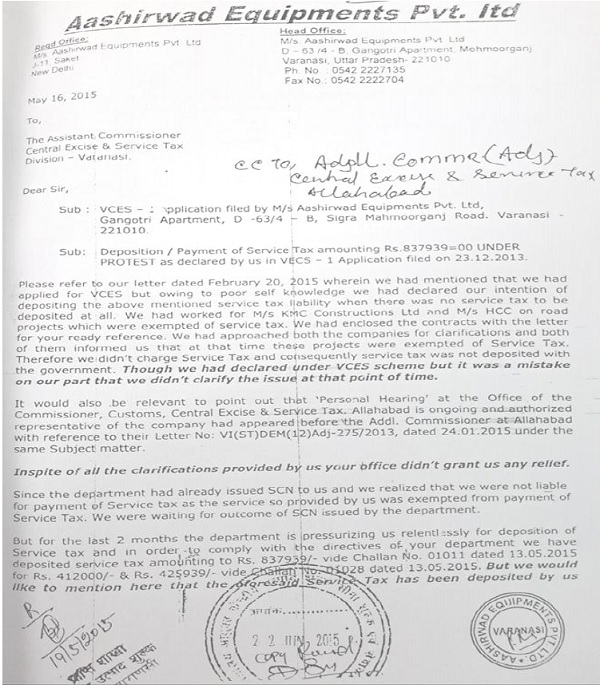

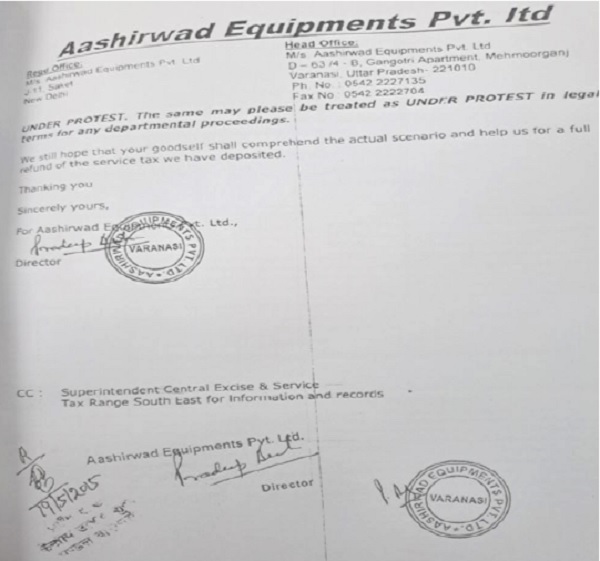

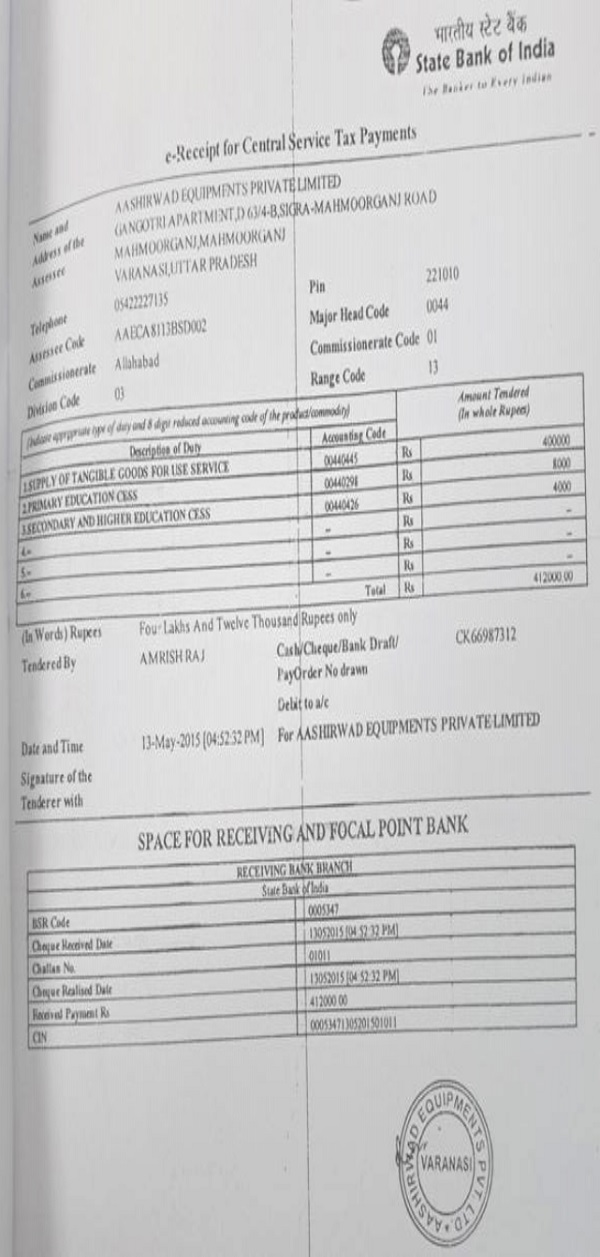

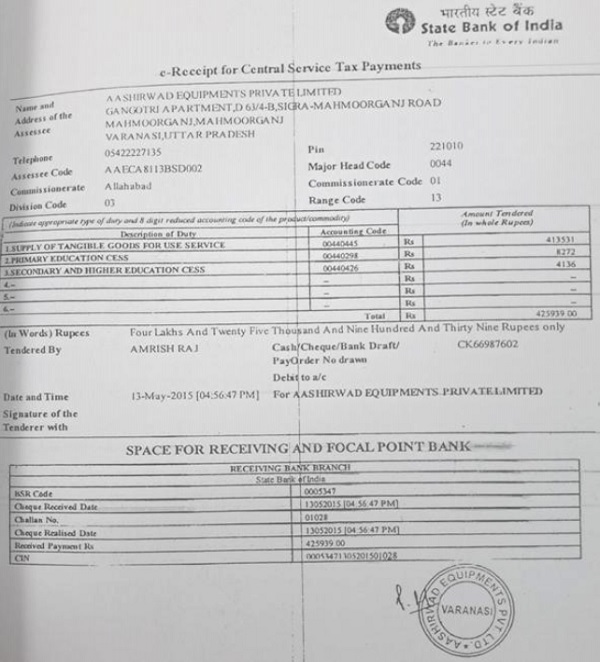

4.4 Subsequent to the issue of the show cause notice appellant made a application under Service Tax Voluntary Compliance Encouragement Scheme 2013, on 23.12.2013. In their application they declared their admitted liability of Rs 8,37,939.00/-. They made the deposited of their admitted liability of the service tax and filed the letter before the adjudicating authority along with the challans evidencing the payment of admitted liability. The letter filed and the challans for the deposit of the said amount are reproduced below:-

4.5 The show cause notice was adjudicated as per the order in original dated 21.12.2015 confirming the demand of Rs.8,36,086/- and the service tax deposited was appropriated against the demand confirmed. Demand of interest was upheld and penalties were imposed upon the appellant.

4.6 Appellant filed appeal before the Commissioner (Appeal) who vide order in appeal dated 11.01.2018 upheld the order in original with some modifications. Aggrieved appellant filed the appeal before the CESTAT. At SI No 14 of the appeal memorandum (ST-5) appellant stated as follows:

“Service Tax

Rs 84609/- (i.e. 10% of Rs 846086/- vide Challan No 00127 dt 28.03.2018) plus Rs………. (i.e. 7.5% of Rs 8,36,086 vide Challan No 01011 dt 13.05.2015) Rs 4,12,000/- Challan No 01028 dt 13.05.2015 Rs 425939.00 Total Rs 837939.00″

From what has been stated above it is evident that appellant made deposit of Rs 84,609/- vide challan dated 28.03.2018 which is after the date of order in appeal. Hence I have no hesitation in concluding that this pre-deposit was made at the time of filing the appeal before CESTAT. As per Section 35 F of Central Excise Act, 1944 read with the Section 83 of the Finance Act, 1994, 4.7 Commissioner (Appeal) could not have taken the appeal for consideration without ensuring that appellant had deposited the 7.5% of the disputed tax amount. In fact Commissioner (Appeal) in his order recorded as his satisfaction in following words:

“4. Discussion & Findings: It is observed that the appeal has been filed within the time limit specified under Section 85 (3A) of the Act inasmuch as the appellant had received the impugned order, on 22.01.2016, and have filed the appeal on 16.03.2016, along with the pre-deposit required under Section 35F of the Central Excise Act, 1944 as made applicable to the Service Tax matters vide Section 83 of the Act.”

Appellant had not deposited any other amount subsequent to the order in original dated 21.12.2015. They had in their appeal memorandum before Commissioner (Appeal) at K of statement of facts stated as follows:

“K. The agreement was on record. Our understanding was also on record. It was also on record that we paid Rs 8,37,939/- on account of Service Tax but under protest with pointing out our reservation about tax liability.”

4.7 I have earlier pointed out that adjudicating authority has appropriated this amount paid by the appellant against the demand confirmed. From the facts as narrated above the undisputed conclusion, is that Commissioner (Appeal) had considered the payment made by the appellant vide two challans dated 13.05.2015 as pre-deposit required in terms of Section 35 F of the Central Excise Act, 1944 read with Section 83 of the Finance Act, 1994. Revenue never disputed the same and filed any appeal challenging this aspect. Thus I conclude that revenue authorities including Commissioner (Appeals) have all along considered the amount deposited by the appellants vide these challans as pre-deposit for consideration of the appeal by the First Appellate authority.

4.8 Order in original dated 21.03.2024, ignoring the above have recorded the findings as follows for allowing the refund claim to the extent of Rs 9,52,798/-:

“Discussion and findings

1. Instant refund is scrutinized and I find that the claimant had deposited following amount as detailed below.

| S.N. | Challan No. & Date | Head | Amount (Rs.). |

| 1 | 127 dated 28.03.2018 | Pre-deposit for filing Appeal before the CESTAT Allahabad | 84,609/- |

| 2 | 1028 dated 13.05.2015 | Tax | 4,25,939/- |

| 3 | 1011 dated 13.05.2015 | Tax | 4,12,000/- |

I find that the appellate Authority vide 0-I-A No. 36/ST/Alld/2018 dated 11.01.2018 upheld the the confirmation of demand of service tax (including Cesses) of Rs. 8,36,086/- along with interest and imposition of penalty of Rs. 8,36,086/- under Section 78 of the Act as confirmed and imposed by 04-0 No. (ST-168/2013) 87 of 2015 dated 21.12.2015. However, penalty imposed under section 77 (1) (a) of the Act, was reduced to Rs. 10,000/-vide aforesaid 0-I-A. The Hon’ble CESTAT, Allahabad vide Order dated 31.01.2024 has set aside the demand of Service Tax and Interest & penalties imposed vide 0-I-A No. 36/ST/Alld/2018 dated 11.01.2015 passed by the Commissioner (Appeals), CGST & Central Excise Allahabad.

2. I also find that in terms of Section 35FF of the Central Excise Act, 1944 as made applicable to the Service Tax matter vide Section 83 of the Finance Act, 1994 read with Notification No. 24/2014-CE (NT) dated 12.08.2014, the party is entitled for interest @6% per annum for the period from the date of deposit, which comes out to Rs. 30,459/-(Rupees Thirty Thousand Four Hundred Fifty Nine Only) for pre-deposit. Thus, the claimant is entitled for the Refund amounting to Rs. 9,52,798/- as detailed below.

| S.N. | Head | Refund Amount (Rs.) |

| 1 | Pre-deposit | 84,609/- |

| 2 | Interest on Pre-deposit | 30,250/- |

| 3 | Tax | 8,37,939/- |

| 4 | Total | 9,52,798/-“ |

4.9 If the above finding was to be accepted then it would amount to saying that Commissioner (Appeal) has decided the appeal of appellant vide order in appeal dated 11.01.2018 without ensuring the compliance with section 35F of the Central Excise Act, 1944 read with Section 83 of the Finance act, 1994. In absence of any appeal filed by the revenue challenging the observations made by the Commissioner (Appeal) in para 4 of this order, I am constrained to accept the said observation which in fact is correct finding of fact recorded by the Commissioner (Appeal). Having said so, I hold that amount of Rs 8,37,939/-[Rs 4,12,000 (Challan No 1011 dated 13.05.2015) + Rs.4,25,939 (Challan No 1028 dated 13.05.2015)] was towards pre-deposit for hearing the appeal by Commissioner (Appeal) as per Section 35F of the Central Excise Act, 1944 read with Section 83 of the Finance act, 1994 and provisions of Section 35FF shall apply while considering the refund of the said amount.

4.10 Impugned order which errs on the specific facts as are evident from the records cannot be upheld. The impugned order has without examining the facts as available on record has made pronouncement in law, which cannot be disputed. But the pronouncement in law cannot be contrary to fact on records. If facts point this amount has been considered as pre-deposit, then amount needs to be refunded along with interest as per Section 35FF of the Central Excise Act, 1944. In case of Tikkan Lal Khatri & Sons [Final Order No 70648/2024 dated 15.10.2024 in Service Tax Appeal No 70242 of 2021] after referring to Circular dated 10.03.2017, I have observed as follows:

“4.8 By circular no 1053/02/2017-CX dated 10.03.2017 Board has clarified as follows without any qualification as follows:

26. Refund of pre-deposits:- (i) Where the appeal is decided in favour of the party/assessee, he shall be entitled to refund of the amount deposited along with the interest at the prescribed rate from the date of making the deposit to the date of refund in terms of Section35FF of the Central Excise Act, 1944.

Since the said Circular has been issued without any qualification it would not be open to authorities subordinate to introduce qualification as has been sought to by the impugned order and not apply the said circular.

4.9 In view of the discussions as above, I do not find any merits in the impugned order.”

4.11 As I have concluded the matter on the facts of case in hand, I do not take up any of the decisions referred by the appellant for consideration, which in any case are to totally irrelevant for the controversy in the present appeal.

4.12 I do not find any merits in the impugned order.

5.1 Appeal is allowed.

(Order pronounced in open court on-25 June, 2026)

Author Bio