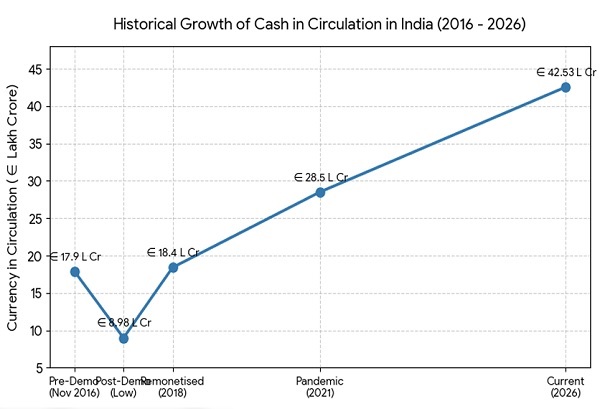

According to the latest data from the Reserve Bank of India (RBI), the total Currency in Circulation (CiC) in India has reached an all-time high of ₹42.53 lakh crore (₹42.53 trillion). From the demonetisation (November 2016) lows of ₹8.98 lakh crore the present high of ₹42.53 lakh crore is mind boggling. Cash usage continues to scale records despite unprecedented growth in UPI and digital payments. The economy functions heavily on both systems simultaneously.

In November 2016, demonetisation instantly wiped out 86% of India’s cash, dropping Currency in Circulation to a low of ₹8.98 lakh crore. Within one year, cash returned to ₹18.4 lakh crore as the RBI rapidly printed new ₹500 and ₹2000 notes. The COVID-19 spike caused a massive panic-hoarding phase, pushing cash to ₹28.5 lakh crore by early 2021. At ₹42.53 lakh crore, the cash in circulation is now more than double the pre-demonetisation levels of 2016. The growth surge during the FY 2026 at 11.9% year-on-year increase, marks the sharpest annual acceleration in cash demand since the pandemic.

The primary reasons for this surge in physical cash point to three distinct underlying behavioural and structural catalysts

1. Buoyant Rural Demand: Robust agricultural output and a structural revival in cash-dependent rural market ecosystems have organically escalated transactional cash requirements

2. Physical Cash as support in uncertain times: Amid skyrocketing prices for gold and silver, domestic savers are increasingly treating physical currency as a primary, liquid store of value during macroeconomic uncertainties.

3. The GST Compliance Backlash: Recent data-driven GST notices served to small vendors for crossing threshold limits have triggered unintended friction. To avoid crossing registration ceilings, small merchants are actively pivoting back to cash ecosystems and deliberately suppressing digital payment trails.

While macroeconomic factors like agricultural cycles or commodity valuation remain beyond immediate regulatory control, the Government holds full administrative leverage over GST frameworks. By replacing rigid enforcement measures with pragmatic, incentivized compliance pathways, policymakers can re-route these parallel cash flows into the formal financial architecture

The primary driver for small merchants return to parallel cash economy is the fear of retrospective penalties and complex compliance. To pull these cash transactions into the formal organised system, the Government must replace rigid punishments with pragmatic economic bridges. Let us delve what Government can do.

1. Retrospective Amnesty Scheme for small merchants:

Government must formalise small merchants who crossed the registration threshold of Rs. 20 lakh* but remained unregistered in the previous years and operating in cash. Government may consider retrospective regularisation window allowing these traders to enter the Composition Scheme under Section 10 of the CGST Act, 2017 from their date of liability. Instead of facing crippling litigation, they will pay a consolidated GST rate of 2% (Regular 1% tax with the additional 1%) explicitly absorbing all accrued penalties and interest. This converts an unenforceable punitive measure into an attractive mechanism for voluntary formalisation, immediately digitising their cash-based supply chains and acts as an excellent onboarding mechanism into GST.

2. Expand Composition Scheme:

Government must prevent formalised businesses from slipping back into the cash economy when they grow. Currently, when a merchant crosses the Rs. 1.5 cr* turnover threshold, they lose composition benefits and face complex Input Tax Credit (ITC) bookkeeping. To avoid this paperwork, many artificially suppress their sales invoices and transact in cash. To eliminate this incentive for cash evasion, Government may consider expanding the Composition Scheme under Section 10, ibid, to a new tier: businesses with a turnover between Rs. 1.5 cr to Rs. 3 cr. Because these growing traders forgo their rightful Input Tax Credit benefits by choosing simplicity, Government may consider levying a concessional, flat GST rate of 5% on the turnover within this bracket. Crucially, these traders will remain fully eligible for the Composition Scheme in subsequent years also, provided they remain under the new Rs. 3 cr ceiling. This eradicates the systemic incentive to under-report revenue. By extending this compliance runway, Government may eliminate the fear of growth, remove the incentive to hide revenue in cash, and permanently lock these small merchants into the transparent, digital economy and reduces the cash in circulation.

3. Lowering E-Way Bill Thresholds:

Government may consider lowering the limit of e-way bill generation to Rs. 20,000 instead of present Rs.50,000 limit under Rule 138 of CGST Rules, 2017. This will help in digitising more transactions and capturing these turnovers in the GST fold.

4. Banking Channel Mandate for ITC:

Government may mandate the dealers settling the payments to the vendors through banking channels as eligible criteria for availing Input Tax Credit will be helpful in reducing the cash economy and extending the formal economy. This structural link forces business ecosystems to police themselves, making digital business-to-business settlements mandatory across supply chains.

Wide spread cash circulation is often a defensive reaction to complex administrative systems. By smoothing out rigid compliance curves, clearing widespread misapprehensions among small merchants, expanding the scope of the Composition Scheme and giving wide publicity to the expanded composition scheme, the Government can foster an environment of economic trust. This also helps in boosting the income tax assessees base and collections as ripple effect.

Simplifying the GST architecture provides small merchants with a secure path into the organized sector, turning the goal of a less-cash economy into a sustainable structural reality and go long way in reducing the cash in circulation in India economy.

(*Note: GST registration threshold limits may vary from State to State and turnover threshold limits vary from goods to services)

Author Bio