Case Law Details

Pagadala Velugonda Reddy Vs ACIT (ITAT Raipur)

VSVS for Penalty ≠ VSVS for Quantum— CIT(A)’s Mistaken Assumption on VSVS Leads to Full Remand

Assessee, a senior citizen deriving agricultural income & not originally required to file return for AY 2013-14, faced reassessment completed ex-parte u/s 147 r.w.s.144 with addition of Rs.19,20,000 treating entire cash deposits as unexplained investment u/s 69. Before CIT(A)-NFAC, Assessee filed detailed submissions & evidence; however, CIT(A) dismissed appeal presuming Assessee had opted for settlement of quantum dispute under Vivad Se Vishwas Scheme (VSVS) 2020. Assessee clarified before Tribunal that VSVS application (Form-1 & Form-3 dated 12.11.2020 & 22.12.2020 ) pertained only to penalty u/s 271F & 271(1)(b) & not to quantum addition. Tribunal noted the identical mistake had been addressed earlier in Srinivas Rachiraju Vs ITO, ITA 361/RPR/2025, where CIT(A) had similarly misread VSVS for penalty as VSVS for quantum. Tribunal held that CIT(A) mis-appreciated facts, dismissed appeal under mistaken belief & failed to adjudicate merits. In the interest of justice, Tribunal set aside CIT(A)’s order & remanded matter for de-novo adjudication, directing verification of whether VSVS applied only to penalty & thereafter deciding quantum grounds as per law. Appeal allowed for statistical purposes.

FULL TEXT OF THE ORDER OF ITAT RAIPUR

The present appeal preferred by the assessee emanates from the order of the Ld.CIT(Appeals)/NFAC, dated 30.09.2025 for the assessment year 2013-14 as per the following grounds of appeal:

“1. In the facts and circumstances of the case and in law, the Ld. Jt. Commissioner of Income-tax (Appeals) has erred in dismissing appeal holding that appellant has opted for Vivad Se Vishwas Scheme Act, 2020 against assessment order, while declaration filed under VSVS Act was with respect to Penalty order and not against assessment order.

2. In the facts and circumstances of the case and in law, the Ld. Jt. Commissioner of Income-tax (Appeals), Chennai has erred in confirming initiation of re-assessment proceedings under section 147 of the Income-tax Act, 1961 which was initiated without fulfilling conditions stipulated in section 147 to 151 of the Act.

3. In the facts and circumstances of the case and in law, the Ld. Jt. Commissioner of Income-tax (Appeals), Chennai has erred in upholding addition of entire amount of cash deposit of Rs.19,20,000/- as unexplained investment u/s.69 of the Income-tax Act, 1961.

4. The impugned order is bad in law and on facts.

5. The appellant reserves the right to add, alter, omit all or any of the grounds of appeal with the permission of the Hon’ble appellate authority.”

2. Brief facts in this case are that the assessee is a senior citizen deriving income primarily from agricultural activities and was not required to file a return of income for A.Y.2013-14. Reassessment proceedings were initiated and completed ex-parte u/s. 147 r.w.s. 144 of the Income Tax Act, 1961 (for short ‘the Act’), resulting in an addition of Rs.19,20,000/-treating entire cash deposits as unexplained investment u/s.69 of the Act.

3. That aggrieved by the assessment order, the assessee had filed first appeal before the Ld. CIT(Appeals)/NFAC and detailed written submission a/w. documentary evidence were filed as submitted by the Ld. Counsel for the assessee. However, the Ld. CIT(Appeals)/NFAC had dismissed the appeal and did not adjudicate merits on the presumption that the assessee had opted for settlement of quantum dispute under Direct Tax Vivad Se Viswas Scheme, 2020. It is contended by the Ld. Counsel for the assessee that in reality, the Vivad Se Viswas Scheme, 2020 declaration filed by the assessee pertains only to penalty proceedings u/s. 271F & 271(1) (b) of the Act and not regarding the quantum addition. The Ld. Counsel had on similar facts relied on the decision of this Bench in the case of Srinivas Rachiraju Vs. ITO, Ward-2(2), Bhilai, ITA No.361/RPR/2025, dated 30.06.2025 wherein it was held and observed as follows:

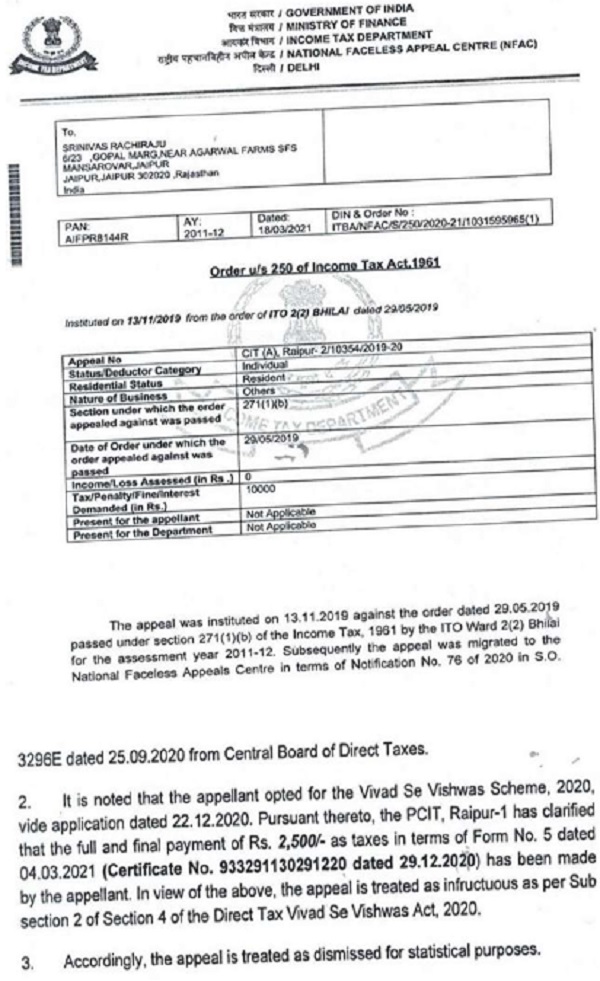

“6. At the outset, it is submitted by the Ld. AR before us that the assessee in the present case had not opted for VSVS, 2020. However, for the same assessment year a penalty was imposed upon the assessee u/s. 271(1)(b) of the Act for Rs. 2500/-, which was settled by opting for VSVS, 2020, accordingly, a separate appeal filed by the assessee against penalty order was dismissed by the Ld. CIT(A), copy of said order is placed before us, which is extracted hereunder for the sake of complete of facts:

7. It is further clarified by the Ld. AR that the assessee’s opting for VSVS, 2020 to settle the penalty imposed has been misconstrued under wrong impression by the Ld CIT(A), that the appellant had also opted for VSVS, 2020 to settle the quantum additions, accordingly, the appeal for quantum additions was also dismissed. However, the assessee had never opted for VSVS, 2020 towards pending appeal qua the quantum additions. It was the submission that the appeal of the assessee has been dismissed under factual misunderstanding. To substantiate this fact, Ld. AR drew our attention to observations of Ld CIT(A) in both the appeals (extracted supra) that the same certificate No. 933291130291220 dated 29.12.2020 for Rs. 2,500/-mentioned in the penalty appeal by the Ld. CIT(A) is noted in the quantum appeal also. On perusal of Ld. CIT(A)’s impugned order, this fact is clearly emerging that the same certificate no. and amount has been cited while dismissing the appeal against the quantum addition, whereas the amount of quantum addition was Rs. 7,54,409/- and no certificate was issued under VSVS, 2020. Such facts shows that the assessee’s application for VSVS, 2020 for penalty addition are misconstrued by the Ld. CIT(A) and the information has been repeated in the quantum appeal also, consequently, the appeal is dismissed under mistaken belief about the facts.

8. Considering the aforesaid facts and circumstances of the present case, it can be safely construed that the appeal of the assessee has been dismissed by Ld. CIT(A), based on misreading of facts, therefore, it would be appropriate to restore this matter back to the file for Ld. CIT(A) for reconsideration, to which both the parties herein had fairly agreed to.

9. Accordingly, the impugned order of Ld. CIT(A) dated 01.04.2021 passed against the order u/s 147 r.w.s. 144 dated 05.12.2018 is set aside, with directions to revisit the matter and adjudicate denovo.

10. Needless to say, the assessee shall be afforded with reasonable opportunity of being heard in the set aside appellate proceedings, wherein the assessee shall cooperate and assist proactively, failing which the Ld. CIT (A) would be at liberty to decide the case in accordance with the mandate of law.

11. In result, appeal of the assessee is allowed for statistical purposes, in terms of over aforesaid observations.”

4. The Ld. Sr. DR also conceded that there is no objection if the matter is remanded to the file of the Ld. CIT(Appeals)/NFAC for re-adjudication considering the submissions of the assessee that the settlement of Direct Tax Vivad Se Viswas Scheme, 2020 of the Department was not in respect of quantum addition but it pertains to penalty u/s.271F & 271(1)(b) of the Act.

5. I have carefully considered the documents on record, heard the submissions of the parties herein and analyzed the facts and circumstances of this case. The Ld. CIT(Appeals)/NFAC had observed and held as follows:

“4.1 On considering the reply submitted by the appellant it is seen that appellant had applied under vivad se viswas scheme (VSVS), 2020 and it is also seen that the Form 1 dated 12.11.2020, Form 3 dated 22.12.2020 are available on record. From the submission it is seen that the appellant has opted Direct Tax Vivad Se Viswas Scheme, 2020 for the settlement of the dispute for the year under consideration against the order u/s 143(3) r.w.s. of the Act, dated 30112018 and accordingly submitted the application in Form 1 & 2 vide dated 12.11.2020 under the Direct Tax Vivad Se Viswas Scheme, 2020.

It is also pertinent to note that even for the hearing notices issued u/s.250 of the Act requesting the appellant to submit the documentary evidence in support of his claim made in the grounds of appeal, the appellant submitted the above Forms of VSV. Hence, considering the response of the appellant in filing Forms of VSV scheme and since the appellant himself doesn’t want to pursue the appeal as he had opted for the VSV Scheme, 2020 for the settlement of dispute as it is evident from the response submitted by the appellant as above in response to notice u/s 250 of the Act, the appeal filed by the appellant and issue of which appeal was preferred become infructuous and not sustainable.

5. Conclusion: In the result, the appeal is dismissed.”

6. That on perusal of the order of the Ld. CIT(Appeals)/NFAC as well as submission made by the Ld. Counsel for the assessee, it is validated that an opportunity must be given to both the parties to ascertain the issue, for which, the assessee had preferred settlement under vivad se viswas scheme, 2020 of the department, is it for the quantum or is it for the penalty as assailed by the assessee? That upon determination of the said issue, the merits have to be considered. In the interest of justice, I set-aside the order of the Ld. CIT(Appeals)/NFAC and remand the same to its file for denovo adjudication on the issue as spelt out aforestated while complying with the principles of natural justice. The assessee shall comply with hearing notices issued from the office of the Ld. CIT(Appeals)/NFAC and accordingly, the Ld. CIT(Appeals)/NFAC shall pass an order in terms with Section 250(4) & (6) of the Act.

7. As per the above terms grounds of appeal raised by the assessee are allowed for statistical purposes.

8. In the result, appeal of the assessee is allowed for statistical purposes.

Order pronounced in open court on 5th day of December, 2025.

Author Bio