Month: March 2026

2,081 articlesCompany Law

Company Law

Application u/s. 59 of Companies Act rejected as issuance of share certificate not within its scope

Corporate Law

Corporate Law

Odisha–Zimbabwe Partnership: How a Strategic Alliance Could Accelerate Odisha’s Industrial Growth

DGFT

DGFT

DGFT Extends Export Obligation for Advance Authorisation & EPCG till 31st Aug 2026

Corporate Law

Corporate Law

EPFO Tightens Pension Conversion Compliance Because Earlier Guidelines Were Not Followed

Goods and Services Tax

Goods and Services Tax

Grant vs Subsidy Under GST: When Grant-in-Aid Becomes Taxable Consideration

Goods and Services Tax

Goods and Services Tax

Unified GST Recovery Framework Introduced as Section 74A Merges Fraud & Non-Fraud Cases

Goods and Services Tax

Goods and Services Tax

GST Recovery Stayed Because Assignment of Leasehold Rights Issue Pending Before SC

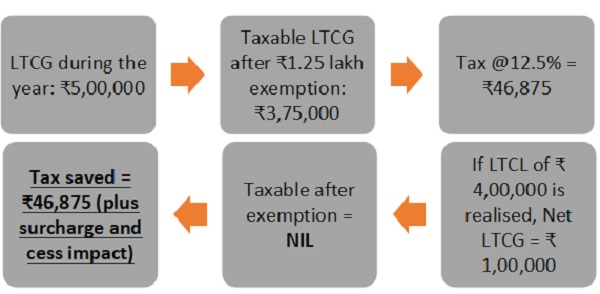

Income Tax

Income Tax

How Tax Loss Harvesting Helps Reduce Capital Gains Tax on Shares?

Goods and Services Tax

Goods and Services Tax

जीएसटी विवाद मार्गदर्शन: प्री-डिपॉजिट रिफंड अधिकार, धारा 74 दंड पर सुप्रीम कोर्ट की सीमित राहत और 100% जुर्माने से बचने की अनिवार्य शर्तें

Goods and Services Tax

Goods and Services Tax