Securities and Exchange Board of India

Discussion Paper

Review of delisting framework pursuant to open offer

Objective

1. The objective of this discussion paper is to seek comments / views from the public on the proposed new framework of delisting pursuant to open offer.

Issue

2. If an open offer is triggered either through direct or indirect acquisition by an incoming acquirer acquiring more than 49% from a large exiting shareholder and/or a fresh issue of shares (preferential allotment) by the listed company:-

a. the provisions of the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (“Takeover Regulations”) may take the incoming acquirer’s holding to above 75% and perhaps even 90% (between 49% and 64% under the agreement(s) and 26% from the public shareholders);

a. the provisions of the Securities Contract (Regulation) Rules, 1957 (“SCRR”) mandate the acquirer to reduce its holding below 75% within twelve months; and

b. the provisions of the SEBI (Delisting of Equity Shares) Regulations, 2009 (“Delisting Regulations”) do not permit the acquirer to attempt delisting requiring to reach 90% unless the acquirer holding is brought down to 75%.

3. It has been represented that such directionally contradictory transactions in a sequence pose complexity in the takeover of listed companies and dissuade an incoming acquirer from seeking to acquire control over listed companies.

Sub-group Report

4. The issue was tabled before the Primary Market Advisory Committee’s (“PMAC”) meeting dated July 27, 2020. After deliberation, the PMAC recommended SEBI to form a Sub-group to examine the issue and give its detailed recommendations. Accordingly, a Sub-group was formed out of the members of the PMAC, consisting advocates, law firms, merchant bankers, exchanges and the representative from investor’s associations. The Sub-group was requested to make recommendations on aligning the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (Takeover Regulations) and the SEBI (Delisting of Equity Shares) Regulations, 2009 (Delisting Regulations) to make M&A transactions for listed companies a more rational and convenient exercise, balancing the interests of all investors in the process.

5. The Sub-group has subsequently submitted its report to the PMAC. While agreeing with the recommendations of the Sub-group, PMAC advised SEBI to seek public comments on the report. The Sub-group’s report is placed at Exhibit – A.

6. The Sub-group has proposed a new framework to deal with the issues flagged at para 2 and 3 above. The recommendations made by the Sub-group mainly relate to disclosure of intent to attempt delisting upfront, Delisting Price and Takeover Price, Shareholder and Stock Exchange approval and Delisting attempt after the open offer. The Sub-group has suggested that the proposed framework may be made available only in the case of open offers under the Takeover Regulations for an incoming acquirer that is seeking to acquire sole or joint control under Regulation 3(1) or Regulation 4 (i.e., where there is a change of control because of a new acquirer).

Public comments

7. Considering the implications of the instant matter on the market participants including the investors, promoters and listed companies, public comments are solicited on the proposed framework. The main question for consultation is whether delisting pursuant to open offer should be permitted as per the proposed new framework. Specific comments/ suggestions as per the format given below would be highly appreciated:

| Name of entity/ person/ intermediary: | |||

| Name of organization (if applicable): | |||

| Contact details: | |||

| Sr. No. |

Pertains to para number | Comments / Suggestions |

Rationale |

8. Comments may please be sent at either takeoverreview@sebi.gov.in or sent by post at the following address latest by July 16, 2021.

The General Manager,

Division of Corporate Restructuring-II,

Corporation Finance Department,

Securities and Exchange Board of India

SEBI Bhavan

Plot No. C4-A, “G” Block

Bandra Kurla Complex

Bandra (East), Mumbai – 400 051

***

Exhibit – A

REPORT OF THE SUB GROUP FOR TAKEOVER – DELISTING

This sub-group of the PMAC has been formed to make recommendations on aligning the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (Takeover Regulations) and the SEBI (Delisting of Equity Shares) Regulations, 2009 (Delisting Regulations) to make M&A transactions for listed companies a more rational and convenient exercise, balancing the interests of all investors in the process. The list of members of the sub-group is set out in Annexure A.

The Background Note from SEBI for the initial meeting held on August 29, 2020 in this regard is set out at Annexure B.

Problem Statement:

It would be useful to crystallise the problem statement for which solutions have been proposed by the working group.

a) Currently, the Takeover Regulations require a mandatory open offer for acquisition of shares held by all shareholders other than the acquirer2, if the acquirer has agreed to acquire shares representing an entitlement to vote 25%3 or more, or control4 over a listed company;

b) Such an open offer has to be made for a minimum size of 26%5;

c) Upon such acquisition, the acquirer may possibly cross 75%, which is the current maximum non-public shareholding under law6;

d) The SCRR stipulates a minimum public shareholding of 25% for all listed companies and if this limit is breached, the non-public shareholding has to be brought down to 75% within a year7;

e) The manner of achieving compliance with minimum public shareholding is regulated8;

f) The Delisting Regulations prohibit any attempt at delisting unless the company is compliant with applicable securities laws (which would include minimum public shareholding of 25%)9;

g) Delisting Regulations entail acquisition of shares at price discovered by a reverse book-building process, with the finishing line to be reached in order to achieve delisting being 90%10 shareholding;

Therefore, in a nutshell, if an open offer is triggered by a share purchase agreement or an overseas amalgamation entailing direct / indirect acquisition by an incoming acquirer of anything more than 49% from a large exiting shareholder and/or a fresh issue of shares (preferential allotment) by the listed company:-

> compliance with one body of law could bring the incoming acquirer’s holding to above 75% and perhaps even 90% (between 49% and 64% under the agreement(s) and 26% from the public shareholders);

> compliance with another body of law would force her down to below 75%;

> and the third body of law would not let the acquirer even attempt to reach 90% unless the holding is brought down to 75% (in situations where the acquirer seeks to delist under the Delisting Regulations, after the completion of the open offer).

As a result, even if the acquirer is desirous of acquiring 90% stake in a listed company in the first place, the acquirer, and indeed the other shareholders have to navigate three bodies of law to consider their respective rights and protections and effect three public transactions, each directionally contrary to the immediately preceding one.

The consecutive flow of public transactions would also confuse investors in the secondary market who need not already be shareholders in the listed company – with an offer to buy their shares (open offer under the Takeover Regulations), followed by an offer to sell shares to them (to comply with SCRR), and then an offer to buy their shares (offer under the Delisting Regulations).

Such directionally contradictory transactions in a sequence pose complexity in the takeover of listed companies and dissuade an incoming acquirer from seeking to acquire control over listed companies.

Regulation 5A:

An attempt to link the Takeover Regulations and the Delisting Regulations was made with the introduction of Regulation 5A of the Takeover Regulations11, which essentially entails announcing an open offer under the Takeover Regulations, suspending it to attempt an offer under the Delisting Regulations and if delisting does not occur, coming back to pick up where the open offer was left under the Takeover Regulations. Therefore, it is a mere sequencing provision and does not provide a framework for addressing a convenient and smooth flow of all constituents respective rights and obligations. The uncertainties and the complications involved above are not resolved by this provision – they are merely sequenced.

TRAC Report:

One of the elements of a recommendation in the TRAC Report could be adapted to reform the regulatory framework. It must be borne in mind that the context of the recommendation in the TRAC was the fundamental reform sought to be made, to adjust equities across all shareholders of a listed company. The foundational reform sought in the TRAC Report was that every open offer must be made for all the remaining shares of the listed company – for example, if an acquirer agrees to acquire 60%, the open offer must be for the remaining 40%. Therefore, if the response were to be in the order of say, 30%, the acquirer would have crossed the delisting threshold, and therefore, it would be unfair to her and the public shareholders to have to deal with the problem outlined above.

Therefore, the TRAC Report also contained a reform measure by which, the acquirer would have to make known upfront if she intended to delist or remain listed. If it was intended that the target company would remain listed, she would have the option of scaling down the purchases under the agreement for substantial acquisition and from the public shareholders in proportion to remain at 75% at the end of the transaction. The acquirer would also have the option of not scaling down such purchases and then becoming compliant with the minimum public shareholding requirements under the SCRR (the policy underlying it has been fluid and been modified from time to time).

If the acquirer intended that the target company would be delisted, the acquirer would make known such intent. Therefore shareholders who tender shares, would do so, fully conscious of the possibility of a delisting, and if the threshold of 90% were to be crossed, the company would stand delisted.

The proportionate reduction of purchases was a fundamental equitable reform, and indeed, it was in the context of a full size open offer being mandatory. The non-implementation of such open offer size, coupled with objections raised by promoters who did not want to be scaled down in their exits, led the entire package of reform not finding its way into the Takeover Regulations.

The group noted empirical data on the actual usage of Regulation 5A, which is reflective of the practical difficulties faced by the market in putting this provision to use. A summary of the information in this regard is set out in Annexure C;

There is consensus that if M&A transactions are abandoned due to the complexity set out in the problem statement above, it would be detrimental to the investor community;

Investors too would like some definitive gap between multiple public transactions since it causes confusion about the state of play about the listed companies particularly between an open offer, an offer for sale and a delisting. Stock exchanges feel these transactions are now well understood and if necessary, greater awareness building efforts may be undertaken;

Group Recommendations – Potential Solution:

The group explored the possibility of borrowing from the thinking articulated in the TRAC Report and addressing the serious inconvenience arising from it, keeping in mind the need to ensure that the checks and balances in the Delisting Regulations are not lost sight of.

In view of the Covid pandemic, the group conducted its meetings by video conference with an initial focused meeting on August 29, 2020, followed by consideration of empirical data and inputs from members thereafter, with a follow-up meeting on September 5, 2020. After the initial submission of the report on October 28, 2020, the group was reconvened to discuss some facets of the reform on June 4, 2021.

The group has built broad consensus with a fair degree of detailing, which is set out below:-

Consensus on Need to Reform:

1. There is indeed a need to streamline the operation of the Takeover Regulations, the SCRR and the Delisting Regulations;

2. In the course of streamlining, one must not compromise on balancing competing interests;

3. The discovery of price for delisting (which is arrived under the reverse book building process) is the public shareholders’ right and that right can be suitably addressed since shareholders would retain the right to accept or reject the offer price by tendering or refraining from tendering their shares under the open offer;

4. Under the current Delisting Regulations, the price discovery is set by the public shareholders and the acquirer is given the right to reject the price and also make a counter-offer. A new streamlined framework is proposed below for being availed of in situations of change in control (whether completely or from sole to joint) with the entry of new incoming acquirers.

5. Such open offers involving a new incoming acquirer may avail of this framework whereby public shareholders may respond to the open offer and agree to delisting in a unified single process. In such a framework, the acquirer must stipulate the higher price that she is willing to pay for delisting and the public shareholders get to reject it if they dislike it.

Disclosure of Intent to Attempt Delisting Upfront:

6. In an open offer under the Takeover Regulations, the acquirer must state upfront in the first public announcement triggered by the mandatory tender offer as well as in the detailed public statement, whether delisting is intended or if the acquirer is desirous of retaining listed status for the Target Company. In an indirect acquisition that is not a deemed direct acquisition under Regulation 5(2) of the Takeover Regulations, this intention to delist may be stated initially in the detailed public statement12.

7. If the acquirer states upfront that it opts for remaining listed, and the total stake at the end of the tendering period is above 75%, then acquirer may opt for:-

a. either proportionately scaling down purchases under both, the underlying share purchase agreement(s) and purchases of the shares tendered, such that the 75% threshold is never crossed;

b. or by becoming compliant with minimum public shareholding within the time stipulated therefor subject to a nuanced modification set out below;

8. This aforesaid optionality would make it incumbent on the acquirer to make a conscious choice – if despite being given the option of pro-rating a scale-down in purchase, the acquirer does not opt for it, then the acquirer cannot complain about being dragged in opposite directions by the law. This feature of optionality would also be necessary because the exiting substantial shareholder may not be willing to agree for a partial exit and the acquirer may yet desire to go ahead with an open offer. If we make it mandatory to scale down and without giving a choice, fewer open offers may get contracted and that would hurt the public shareholders;

Delisting Price and Takeover Price:

9. If the acquirer is desirous of delisting, a differential pricing must be proposed by the acquirer – an open offer price no lower than the minimum offer price under the current framework of the Takeover Regulations (“takeover price”) and a higher price with a suitable premium reflecting what the acquirer is willing to pay if delisting were successful (“delisting price”).

10. The Takeover Regulations currently provide for differential pricing depending on the response to the open offer, subject to compliance with the minimum pricing requirements – to incentivise a response from the shareholder, one could consider such a differential pricing framework with the higher delisting price being payable, if delisting were successful;

11. Technically, it is possible to argue that even the takeover price should work as the delisting price too, since the outcome is totally dependent on whether shareholders accept that price to tender their shares to the extent of 90%, but the group holds the counter-view that a 90%-plus equity ownership of a company confers a near-absolute control as compared with the strong degree of control available with a 75% threshold, which would give power over special resolutions. Under company law, shareholders holding 10% have the power to requisition a general meeting13. Such a shareholding threshold is also necessary for complaining about oppressive, unfair or prejudicial conduct by the majority14. Besides, the absence of rigours of listing in itself provides a higher degree of control to the acquirer. The group is of the view that the 90% ownership threshold, must therefore, command a premium;

12. Therefore, the consensus view is that the regulations must provide for a higher delisting price as compared with the takeover price for a normal open offer. Therefore, where the acquirer desires to make an attempt at delisting as a logical consequence of the open offer, the proposed delisting price must be offered upfront along with the announcement of the takeover price, with an explanation setting out the rationale and basis for justifying the delisting price. In the case of indirect acquisitions triggering an open offer, where the detailed public statement is required only after the primary acquisition is consummated, the delisting price must be notified at the time of making the detailed public statement;

13. The requirement under the Takeover Regulations that the Committee of Independent Directors must provide their comments on the takeover price should apply to the delisting price as well. The PMAC has already recommended that the Committee of Independent Directors must express its views on the merits of delisting, which requirement would also have to be met;

Outcome and Consequences:

14. If the response to the offer leads to the delisting threshold of 90% being met, all shareholders who tender their shares must be paid the same delisting price;

15. If the response to the offer leads to the delisting threshold of 90% not being met, all shareholders who tender their shares must be paid the same takeover price;

Shareholder and Stock Exchange Approval:

16. Two specific checks and balances, found in the Delisting Regulations must be retained:-

a. shareholders must have the power to reject a delisting effort, with the framework providing for an affirmative vote by a majority of the minority shareholders15; and

b. stock exchanges need to confirm that the listed company is in compliance with listing requirements including payment of dues to exchanges;

17. If the acquirer has announced her intention to delist, an approval of shareholders in general meeting with a positive vote by the requisite majority of the minority and the approval of stock exchanges may be retained – these two conditions may be met at any time after the public announcement is made and before the tendering period starts;

18. If these approvals are not received, the delisting element of the open offer would stand rendered void and the open offer would continue with the takeover price;

Delisting Attempt After the Open Offer:

19. A further nuance suggested is that if a company does not get delisted pursuant to the open offer under this framework, and the acquirer crosses 75% due to the open offer, a period of a18 months from the date of completion of the open offer may be provided for further attempts to delist under the Delisting Regulations including the price discovery method thereunder to be made. [If delisting during this extended 18-month period is not successful, the acquirer must ensure compliance with minimum public shareholding within a period of 12 months from the end of such period. Consistent with the current regulations, there should continue to be a six month gap between two attempts at delisting and a minimum period of six months should lapse between the date of completion of the open offer and the next attempt at delisting.

20. In other words, the prohibition on attempting delisting does not continue during the 18 months from the date of completion of the open offer for acquirers who have opted for this route and failed to delist. However, if any sale of shares is effected to dilute from the level reached post-open offer, the right to attempt delisting must not be available for the 18-month period. This would prevent potential abuse of effecting covert sale of shareholding blocks to concert parties, and would also prevent sending conflicting signals about a continued desire to delist even while selling down shares at the same time. In any case, the options available to the acquirer (as discussed in paragraph 6 above) are available to the acquirer who chooses to stay listed.

21. If a delisting attempt is to be made from a level of above 75% without coming down to 75%, the finishing line for success of such a delisting effort would be the higher of:-

a. 90%; and

b. 50% of the residual public shareholding.

22. The aforesaid position had been the legal position before the uniform public shareholding requirement had been implemented.

23. It is clarified for the avoidance of doubt that the right to make further attempts at delisting within the period of 18 months from the date of completion of the open offer would be available only in respect of companies where the 75% threshold has been crossed due to the open offer.

Next Steps:

24. The group believes that the aforesaid framework provides a right balance between retaining all the regulatory objectives involved in open offers under the Takeover Regulations and well as Delisting Regulations, making it easier and more logical for acquirers to transact without compromising the substantive rights of public shareholders.

25. It is clarified for the avoidance of any doubt that the aforesaid framework is only available in the case of open offers under the Takeover Regulations for an incoming acquirer that is seeking to acquire sole or joint control under Regulation 3(1) or Regulation 4 (i.e., where there is a change of control because of a new acquirer).

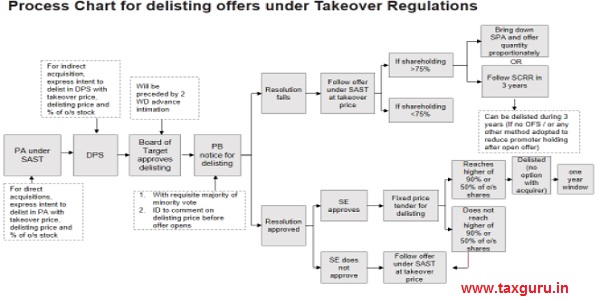

26. Actual draft amendments to implement these changes may be drafted once the PMAC approves of this group’s report and before the recommendations are published inviting public comment. A graphic depiction of a transaction executed through the proposed framework is set out in Annexure D.

Glossary of Terms:

| Delisting Regulations | SEBI (Delisting of Securities) Regulations, 2009 |

| IBC | Insolvency and Bankruptcy Code, 2016 |

| PMAC | Primary Market Advisory Committee |

| SCRR | Securities Contracts (Regulation) Rules, 1957 |

| TRAC Report | Report dated July 19, 2010 by the Takeover Regulations Advisory Committee, chaired by Mr. C. Achuthan, former Presiding Officer, Securities Appellate Tribunal |

| Takeover Regulations | SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 |

| Target Company | A company whose shares carrying voting rights are listed on stock exchanges |

*******

Annexure ‘A’

LIST OF MEMBERS OF THE SUB-GROUP

1. Shri Somasekhar Sundaresan, Counsel

2. Sandip Bhagat, Partner, S&R Associates

3. Shri J N Gupta, Founder and MD, Stakeholder Empowerment Services

4. Shri Anay Khare, Chairperson, AIBI

5. Shri Venkatesan S, Management Committee Member, Tamil Nadu Investor Association

6. Shri Gopalkrishnan Iyer, BSE

7. Shri Hari K., NSE

8. Shri Rajesh Gujjar, GM, SEBI (Convener)

Annexure ‘B’

Takeover and Delisting

Background

1. The issue relating to delisting pursuant to open offer was discussed by the Takeover Regulations Advisory Committee (TRAC). The relevant extract of the TRAC report is as follows:

- An acquirer, who is making a mandatory offer triggered by either substantial acquisition (viz. above 25 %) or acquisition of control, but not pursuant to creeping acquisition, would be permitted to state upfront while making the open offer that if his holding in the target company along with persons acting in concert crosses the delisting threshold pursuant to the open offer, the target company may be delisted.

2. SEBI Board at its meeting held on July 28, 2011 did not accept the recommendation of TRAC to provide for delisting pursuant to an open offer. Therefore, the provisions relating to delisting pursuant to open offer were not included in the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (“Takeover Regulations”).

3. Subsequently, the SEBI (Delisting of Equity Shares) Regulations, 2009 (“Delisting Regulations”) was reviewed in 2015 and the issue relating to delisting and open offers was also discussed. The framework for providing an option to the acquirer to delist the company through the Takeover Regulations was introduced in 2015 in both Takeover Regulations (regulation 5A) and Delisting Regulations, in the following manner:

a. The Acquirer has to declare upfront his intention to delist at the time of making the detailed public statement (DPS)

b. In case, the acquirer selects the option to delist the company, the exit price shall be determined in accordance with the Reverse Book Building (RBB) process. Therefore, the Acquirer is required to attempt delisting in terms of the process prescribed under Delisting Regulations.

c. If the delisting is successful, the shareholders are provided exit at the delisting price and the company gets delisted.

d. In the event of failure of the delisting offer, the open offer obligations are required to be fulfilled by the acquirer.

4. There have been representations made at various fora to revisit this issue, particularly considering the following concerns:

c. The shareholding of the incoming acquirer could reach more than 75% or even more than 90% pursuant to the open offer in terms of the Takeover Regulations”. As per current regulatory framework in terms of Delisting Regulations, such acquirer is required to bring the shareholding back to 75% (within MPS compliance) within a year and then attempt delisting.

d. It has been suggested that if the acquirer expresses its intent to delist, such acquirer should be permitted to delist if the shareholding reaches to 90% or more, pursuant to open offer.

Analysis / Our comments

5. In terms of the current regulatory framework, there are two scenarios:

a. Acquirer has not expressed its intention to delist during the open offer; and

b. Acquirer has expressed its intention to delisting during the open offer. Scenario 1

6. In the first scenario, since the acquirer has not expressed his intention to delist during the open offer, the Acquirer is required to bring back the shareholding within the maximum permissible promoter shareholding norms (75%) within the timeline prescribed under the Securities Contract Regulation Rules, 1957, i.e. one year. In such case, delisting is permitted after compliance with minimum public shareholding requirement and through the reverse book building (RBB) process.

Scenario 2

7. In case the Acquirer has expressed his intention to delist the company at the stage of DPS, the acquirer is required to comply with the provisions of regulation 5A of Takeover Regulations (as brought out in paragraph 3 above).

8. It may be noted that the option of counter offer introduced by SEBI w.e.f. November 14, 2018 broadly addresses the issues raised/ concerns raised in this regard.

a. In terms of regulation 5A of Takeover Regulations, the acquirer can attempt delisting;

b. The acquirer can offer the open offer price in the counter offer and attempt delisting;

c. If the public shareholders tender their shares in such counter offer at the open offer price and the promoter shareholding reaches 90%, the company can get delisted.

9. The suggestion to directly delist the company pursuant to open offer (if shareholding reaches 90%) without proceeding with the delisting process has the following implications / consequences:

Benefit to acquirer

a. In terms of process, it would be simpler as there would be no requirement to attempt two processes (delisting and then open offer). It would ease the delisting of companies (which is currently stringent mainly due to high delisting price discovered through RBB) and therefore contribute towards ease of doing business.

RBB

b. The suggested approach would circumvent the RBB process prescribed for voluntary delisting. Therefore, the suggested approach could be used by existing promoters as a backdoor to avoid the RBB process. Whereas, the regulatory framework introduced in 2015 ensures that RBB process is followed for delisting.

Public Shareholders

c. Whether the company would remain listed or not is conditional upon promoter shareholding reaching 90% or more. Therefore, from the perspective of public shareholders, while the public shareholders would be informed about the likelihood that the company could get delisted, there would be no clarity at the time of tendering on whether their shares are being tendered for open offer or for delisting. The same would depend on the overall outcome of the tendering.

10. In view of the above, we seek the comments of PMAC on this issue.

Annexure ‘C’

DELISTING OFFERS UNDER REGULATION 5A OF TAKEOVER REGULATIONS, 2011 IN LAST TEN YEARS

| Name of Target |

DPS | Delis-ting PA | O/s shares | SAST Price |

Delis-ting floor price |

Delis-ting Size Rs Crore | Success/ Failure | Disco-vered price |

| Bombay Swadeshi Stores Ltd. | May-

15 |

Sep-15 | 20.88% | 126.00 | 126.00 | 13.00 | Success | 126.00 |

| Anupama Steel Ltd | Jun-

16 |

Feb-17 | 49.80% | 40.00 | 40.00 | 4.00 | Success | 40.00 |

| Xchanging Solutions Ltd. | May-

16 |

Aug-16 | 25.00% | 39.23 | 39.23 | 109 | Failure | 109.00 |

| Linde India td | Nov-

18 |

Jan-19 | 25.00% | 328.21 | 428.50 | 913 | Failure | 2025.00 |

CONDITIONAL OFFER UNDER REG 19 OF TAKEOVER REGULATIONS, 2011 IN LAST TEN YEARS

| Name of Target |

PA | Offer size |

Conditional

to |

Response |

| ICRA Ltd | Feb-

14 |

26.50% | 21.50% | 21.55% |

Annexure D