Securities and Exchange Board of India

Feb 22, 2023 | Reports : Reports for Public Comments

Part A of Consultation Paper – Regulatory Framework for ERPs

1. In recent years, climate change and sustainable development concerns have become a priority at global and national levels. There has been an increase in interest of stakeholders, including investors and financial regulators, in examining Environmental, Social and Governance (ESG)-related issues. The growing investor interest in ESG factors reflects the view that environmental, social and corporate governance issues – including risk and opportunities – can affect the long-term performance of companies and therefore should be given appropriate consideration in investment decisions.

2. Specifically, the role of ESG Rating Providers (ERPs) has become important in making investment decisions. However, since the activities of ERPs are typically not subject to regulatory or supervisory oversight at present, increasing reliance on such unregulated services in the securities markets raises concerns about the potential risks it poses to investor protection, efficiency of markets, risk pricing, capital allocation and greenwashing, among others.

3. In this context, on January 24, 2022, SEBI had published a Consultation Paper on ERPs for Securities Market, which contained proposals on regulation/ accreditation of ERPs and sought public comments on the various issues, including scope of regulations, entities eligible to act as ERPs, conditions for accreditation, ESG rating products, standardization of ESG rating scales, transparency, governance and business models of ERPs.

4. Regulators in other jurisdictions such as Japan, South Korea, European Union, UK, as well as international standards setting bodies such as the International Organization of Securities Commissions (IOSCO) have also taken various measures towards increasing scrutiny over providers of ESG ratings.

5. Based on the responses received on the aforesaid consultation paper, discussions held with various stakeholders, and global regulatory developments, SEBI proposes to introduce a regulatory framework for “ESG Rating Providers” or “ERPs”.

6. It is proposed that ERPs may register with SEBI under the SEBI (Credit Rating Agencies) Regulations, 1999, and the CRA Regulations shall be amended to include a chapter for ERPs. The proposed regulatory framework for ERPs is detailed below at Annexure I, on which SEBI is seeking public comments through this consultation paper.

7. While regulators in certain jurisdictions have opted for a voluntary code of conduct for ERPs, SEBI proposes an enforceable regulatory and supervisory framework for ERPs, in view of SEBI’s experience with credit rating agencies (for which SEBI regulations came into effect in 1999, well before the global financial crisis, which led regulators in various jurisdictions to begin regulating or to tighten the regulatory framework for CRAs).

8. However, given the nascent nature of the ERPs and to provide for scope for further innovation, SEBI has attempted to follow a principles-based approach, while balancing SEBI’s mandate of protection of interest of investors in the securities market.

9. This consultation paper also draws reference to IOSCO’s call for action for financial markets voluntary standard setting bodies and industry associations to promote good practices to counter the risk of greenwashing in ESG ratings. In this context, SEBI recommends ESG rating providers, who wish to operate in the Indian securities market, to form an industry association and play an active role in development of a regulatory framework for ERPs in the Indian securities market and engage with SEBI at its ESG advisory committee.

Part B of Consultation Paper – Proposals regarding ESG ratings based on recommendations of the SEBI ESG Advisory Committee

10. In May 2022, SEBI constituted an advisory committee on ESG matters in securities market, wherein ESG disclosures, ESG investing and ESG ratings were deliberated in an integrated manner.

11. With regard to ESG ratings, the terms of reference of the committee were as under:

11.1 Developing separate/ parallel approach for ESG rating suitable to emerging markets e.g. focus on ‘S’ including employment generation, etc.

11.2 Developing uniform indicators of ‘G’ as input to ESG ratings and / or credit ratings

11.3 Disclosures in the rationale by ESG rating providers on what and how qualitative factors were factored in to the ESG ratings / observations

12. Based on the recommendations of the committee and internal deliberations, the proposed approach for ESG ratings / ESG rating providers (ERPs) is detailed below.

13. Additional type of ESG Ratings – based on ‘Core’ Business Responsibility and Sustainability Reporting (BRSR)

13.1 SEBI, in its recent consultation paper on ESG disclosures, ESG ratings and ESG investing dated February 20, 2023, has inter alia proposed a ‘BRSR Core’ format comprising of select essential indicators across all principles that can become the foundation of the assurance process.

13.2 In context of the new BRSR Core framework, it also proposed that ERPs may also provide a Core ESG Rating, based on assured indicators.

13.3 In this context, it is further proposed that while Core ESG ratings must necessarily be based on assured or verified data, ERPs may be allowed to provide an additional commentary / outlook / observations on data that may not be verified/ assured.

13.4 For instance, an unverified controversy must not be factored in the Core ESG rating/score. However, ERPs shall have the discretion to provide a commentary on the same, if they so desire.

| Views sought on:

(i) Whether the above proposal on additional commentary in rating rationale of Core ESG rating is appropriate? |

14. Disclosures in the rationale by ESG rating providers

14.1 ESG rating providers generally follow either a subscription-based business model or an issuer-pays business model. In either of the case, there is an ESG rating rationale or a report containing ESG rating of an entity, along with a detailed rationale behind the assigned ESG rating.

14.2 It is essential that the ESG rating rationale be articulated in detail to enable a stakeholder to assess the reasons behind an assigned ESG rating. This is further necessitated by the divergence in ESG ratings across providers1.

14.3 Therefore, in order to provide for greater transparency in the ESG rating process, it is proposed that the ESG rating rationale/ ESG report may contain the following minimum disclosures:

14.3.1 Current ESG rating/score

14.3.2 Change in rating/score from the previous evaluation (direction) 14.3.3 Last review date

14.3.4 Summary of key drivers both qualitative (including controversies and their impact) and quantitative factors considered for arriving at the overall ESG rating

14.3.5 Pillar wise E, S and G scores – key drivers (including industry comparison of material parameters) both quantitative and qualitative being considered for carrying out such assessment

14.3.6 Weights of E, S and G scores in the assigned ESG rating

14.3.7 Brief explanation of rating intent to clarify if it represents unmanaged risks/ performance against risks/ impact etc. In case this is available in a methodology document, cross-linking of the relevant document would suffice

14.3.8 Summary or link to methodology used.

|

Views sought on: (i) Whether any additional disclosure is required in the ESG rating rationale? (ii) Whether the above disclosures are adequate and appropriate for ESG rating providers following either a subscription-based model or an issuer-pays model? |

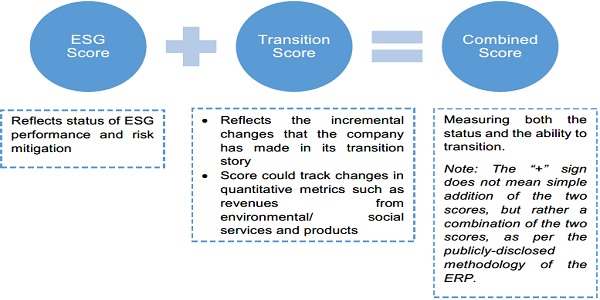

15. ESG Rating Agencies to track Transition Score

15.1 It is observed that various Indian companies may be rated on their current emission levels as they begin to align their strategies with India’s commitment of emissions intensity reduction to Net Zero by 2070, despite substantial reduction year on year.

15.2 Evaluating Indian corporates on an absolute yardstick without recognizing the efforts they make, and results they achieve, in transition may not lead to the appropriate incentives for transition finance.

15.3 Hence, rating agencies are advised to provide two additional ratings:

15.3.1 ESG transition/ Parivartan score: measuring the velocity of and investments in making the transition to Net Zero Goals/improving ESG risk management. In other terms, the transition or Parivartan score would reflect the incremental changes that the company has made in its transition story over recent years or concrete plans/targets to address the risk and opportunities involved in transitioning to more sustainable operations, rather than scoring them only on their current profile. This transition score could track changes in quantitative metrics in trend-lines or change in revenues from environmental/social services and products or any quantitative assessments, as per the model of the ERP.

15.3.2 Combined score: combining ESG rating and transition rating, i.e. measuring both the status and the ability to transition.

15.3.3 While transition scores could be measured using revenue earned from green activities, a more comprehensive framework that considers aspects beyond just revenue generation is recommended.

|

Views sought on: (i) Whether there should be additional regulatory guidelines on transition scores / combined scores for enhanced transparency? (ii) Whether the above structure is appropriate? (iii) Any other suggestions. |

16. Business Model

16.1 With regard to aforesaid reference to business models of ESG rating providers, it is proposed that either a issuer-pays or a subscriber-pays business model be allowed for ERPs in India.

16.2 However, hybrid business models shall not be allowed for ERPs. In other words, an ERP shall not be allowed to assign certain ESG rating based on issuer-pay model, while assigning another ESG rating based on a subscriber-pays business model.

16.3 The above proposal is to mitigate potential conflict of interests. An investor may rely on a certain ERP based on the assumption that the ERP assigns rating based on a subscriber-pays business model. However, the ERP might be assigning another ESG rating (or type of ESG rating) to the same company (or a group company) under an issuer-pays business model.

| Views sought on:

(i) Whether the above proposal on business model is appropriate? (ii) Any other suggestions. |

17. Public Comments

17.1 SEBI proposes an amendment in SEBI (Credit Rating Agencies) Regulations, 1999, a draft of which is placed at Annexure I to this consultation paper.

17.2 Considering the implications of the said matter on the market participants, public comments are invited on the consultation paper. The comments/ suggestions may be provided, separately for Part A and Part B of this consultation, as per the format below:

|

Name of the person proposing comments: |

|||||

| Name of the organization (if applicable): | |||||

| Contact details: | |||||

| Category: whether ERP, corporate, research analyst, CRA, or other market intermediary (mention type/category) or public (investor, academician, etc.) | |||||

| Part A | Pertains to which Regulation / Sub-Regulation |

Extract/ Brief of the Sub- Regulation | Whether you agree or disagree with the proposed regulation/ sub-regulation? | Suggested Amendment, If any | Rationale |

| Part B | Paragraph | Extract/ Brief of the Proposal | Whether you

agree or disagree with the proposal? |

Suggested

changes, if |

Rationale |

17.3 Comments as per aforesaid format may be sent to the following, and should reach SEBI latest by March 8, 2023, in any of the following manner:

17.3.1 Preferably by email to: deenar@sebi.gov.in and rohan@sebi.gov.in; or

17.3.2 By post to:

Deena Sarangadharan, GM / Rohan Shukla, Manager

Department of Debt and Hybrid Securities

Securities and Exchange Board of India,

SEBI Bhavan, C4-A, G-Block,

Bandra Kurla Complex, Bandra (East),

Mumbai – 400051

17.4 Kindly mention the subject of the communication as, “Comments on Consultation Paper on Regulatory Framework for ESG Rating Providers (ERPs) in Securities Market”.

Issued on: February 22, 2023

Annexure I

Draft Regulatory Framework for ESG Rating Providers in Securities Markets –Proposed Chapter in SEBI (CRA) Regulations, 1999

CHAPTER IVA

ESG RATING PROVIDERS

Applicability

28A. (1) This chapter shall be applicable to ESG rating providers registered with the Board or applicants desirous of registering with the Board as ESG rating providers.

(2) All the provisions of Chapter II2, III3 and IV4 of these regulations shall not apply to ESG rating providers.

(3) All the provisions of Chapter I5, V6, VI7 and VII8 of these regulations shall apply mutatis mutandis to ESG rating providers registered with the Board.

Definitions

28B. In this chapter, unless the context otherwise requires: –

(1) “Environmental, Social, and Governance ratings”, or “ESG ratings” refer to the broad spectrum of ratings products that are marketed as providing an opinion regarding an entity that is listed or proposed to be listed on a stock exchange recognized by the Board, or a security, that is listed or proposed to be listed on a stock exchange recognized by the Board, about its ESG profile or characteristics or exposure to ESG, governance risk, social risk, climatic or environmental risks or impact on society, climate and the environment, that are issued using a defined ranking system of rating categories, whether or not these are explicitly labelled as “ESG ratings”;

(2) “ESG rating provider or provider” means a body corporate which is engaged in, or proposes to be engaged in, the business of ESG ratings;

(3) “liquid asset” is an asset that can easily be converted into cash in a short amount of time, such as cash, money market instruments, Government Securities, T-bills and Repo on Government Securities.

(4) “liquid net worth” means net worth deployed in liquid assets which are unencumbered.

(5) “Net Worth” means the aggregate value of the paid up equity capital and free reserves (excluding reserves created out of revaluation), reduced by the aggregate value of accumulated losses and deferred expenditure not written off, including miscellaneous expenses not written of;

Provided that net worth shall be in the form of positive liquid net worth.

Provided further that the net worth can be drawn down in terms of the business plan submitted at the time of application for certificate of registration, subject to compliance with these regulations;

(6) “promoter” shall have the meaning as per Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations 2018;

| Views sought on:

(i) Whether the above definition of ESG ratings is appropriate? The same is broadly based on IOSCO recommendations. (ii) Whether any of the above definitions require any change(s)? |

Application for grant of certificate of registration for ESG rating provider 28C. (1) On and from the commencement of these regulations, no one shall act as an ESG rating provider in India unless it has obtained a certificate of registration from the Board:

Provided that an existing entity falling within the definition of ESG rating provider which is not registered with the Board may continue to operate for a period of three months from commencement of these regulations, or if it has made an application for registration under sub-regulation (4) within the said period of three months, till the disposal of such application.

(2) Any entity referred to in sub-regulation (1) who fails to make an application for grant of a certificate of registration within the period specified therein shall cease to carry on any activity as an ESG rating provider.

(3) ESG rating provider shall seek registration in one of the categories9 mentioned hereunder:

(a) “Category I ESG Rating Provider”,

(b) “Category II ESG Rating Provider”;

(4) An application for the grant of a certificate under sub-regulation (1) shall be made for any of the categories as specified in sub-regulation (3) to the Board in Form A of the Fourth Schedule to these regulations and shall be accompanied by a non–refundable application fee, as specified in Part A of the Fifth Schedule to these regulations, to be paid in the manner specified in Part B thereof.

(5) The Board shall take into account requirements as specified in these regulations for the purpose of considering grant of registration.

(6) Without prejudice to the powers of the Board to take any action under the Act or regulations made there under, the certificate of registration shall be valid till the ESG rating provider is wound up.

|

Views sought on: (i) What criteria should be adopted to categorize ERPs? For instance, the source of information obtained for ESG rating, net worth criteria, nature of services offered, size of the balance sheet, assets under managements of users of ESG rating providers, etc. The intent of categorization is inter-alia to encourage start-ups / new entrants to join the ESG rating industry. For ease of reference, a tabular comparison of Cat-I and Cat-II ERPs is provided at Annexure II. (iii) What further differences could be considered for Cat-I and Cat-II ERPs? For instance, it is proposed that only Cat-I ERPs may provide third-party certification for green debt securities. (ii) Whether the above requirements for ERPs (including those in the aforementioned Schedules) are appropriate? |

Consideration of application for ESG rating provider

28D. For the purpose of the grant of certificate of registration to an applicant, the Board shall consider the following conditions for eligibility, namely, —

(1) the applicant is set up and registered as a company under the Companies Act, 2013 (18 of 2013) and is incorporated in India;

(2) the applicant has specified ESG rating activity as the main objects in its Memorandum of Association;

(3) the applicant has submitted its business plan limited to ESG ratings of securities or entities that are listed, or proposed to be listed, at a stock exchange recognized by the Board;

Provided further that the applicant shall also furnish, along with the business plan, the following information for ESG rating of listed, or proposed to be listed, securities or entities:

(i) a target breakeven date, and

(ii) target revenue and number of clients, within two years of obtaining a certificate of registration as an ESG rating provider

(iii) cumulative cash losses that the applicant projects to incur until the target breakeven date, along with the activities or areas wherein such losses shall be incurred;

(4) the applicant submits a declaration to not undertake any activity or offer any product or service to anyone, except the following:

(i) ESG rating of an entity, that is listed or proposed to be listed on a stock exchange recognized by the Board, or

(ii) ESG rating of a security, that is listed or proposed to be listed on a stock exchange recognized by the Board, or

(iii) Any other product, service or activity as may be specified by the Board, or

(iv) ESG rating of any other product, service or activity as may be required by another financial sector regulator or authority, as may be specified by the Board, under the guidelines of such regulator or authority;

[Additionally, basis suggestions on the differences in categorization of Cat-I and Cat-II ERPs, restrictions / prohibitions shall be specified for Cat-II ERPs, for example Cat-II ERPs shall not undertake certification of green debt securities.]

(5) In case of “Category I ESG rating provider”, the applicant

(a) is a subsidiary of an intermediary registered with the Board, or is a subsidiary of a foreign ESG rating provider incorporated in a Financial Action Task Force (FATF) member jurisdiction and recognized under their law, having a minimum experience of five years in ESG rating of securities or companies;

(b) is promoted by a person belonging to any of the following categories, namely:

(i) an entity regulated by financial sector regulator viz. the Board, the Reserve Bank of India, the Insurance Regulatory and Development Authority, or Pension Fund Regulatory and Development Authority, subject to receipt of requisite approval from the concerned regulator or authority;

(ii) a foreign ESG rating provider incorporated in a Financial Action Task Force (FATF) member jurisdiction and recognized under their law, having a minimum experience of five years in ESG rating of securities or companies;

(iii) a credit rating agency registered with the Board; or

(iv) an entity having continuous net worth of minimum rupees one hundred crores as per its audited annual accounts for the previous five years prior to filing of the application with the Board for the grant of certificate under these regulations.

Provided further that the promoter shall maintain a minimum shareholding of 26% in the ESG rating provider for a minimum period of five years from the date of grant of registration by the Board.

(c) shall maintain minimum net worth is not less than ₹ 5 crore at all points in time.

Provided that at the time of making application, the minimum net worth of the “Category I ESG rating provider” shall not be less than the higher of, ₹10 crore, or addition of ₹10 crore and the cumulative cash losses target made by the applicant under Regulation 28D(3);

(d) has necessary infrastructure like adequate office space, technology or equipment, manpower, to enable it to provide ESG rating services in accordance with the provisions of the Act and these regulations;

(e) shall have at least ten employees specialised in the following areas, at all points of time, with at least one specialist in each of the following areas:

i. governance,

ii. sustainability,

iii. social impact or social responsibility,

iv. data analytics,

v. finance,

vi. information technology,

vii. law

Provided that any person shall be considered as specialised in an area if the person–

(i) has relevant work experience of not less than five years in the specified area; or

(ii) has professional qualification in the specified area from a university or an institution recognized by the Central Government or any State Government or a foreign university, or a CFA charter from the CFA institute , or

(iii) has any other qualification as may be specified by the Board.

(6) In case of “Category II ESG rating provider”, the applicant

(a) Shall maintain minimum net worth of not less than ₹ 10 lakh at all points in time.

Provided that at the time of making application, the minimum net worth of the “Category II ESG rating provider” shall not be less than the higher of, ₹ 20 lakh, or addition of ₹ 20 lakh and the cumulative cash losses target made by the applicant under Regulation 28D(3);

(b) has necessary infrastructure like adequate office space, technology or equipment, manpower, to enable it to provide ESG rating services in accordance with the provisions of the Act and these regulations; Provided that in case the Category II ESG Rating Provider intends to offer remote work environment, that is, work from home, the requirement for an office space shall not be applicable, subject to declaration to that effect by the Provider.

(c) shall have at least five employees specialised in the following areas, at all points of time, with at least one specialist in each of the following areas:

i. governance,

ii. sustainability,

iii. social impact or social responsibility,

iv. data analytics

Provided that any person shall be considered as specialised in an area if the person–

(i) has relevant work experience of not less than five years in the specified area; or

(ii) has professional qualification in the specified area from a university or an institution recognized by the Central Government or any State Government or a foreign university, or

(iii) has any other qualification as may be specified by the Board.

(7) The applicant is not a credit rating agency or any intermediary registered with the Board;

(8) the applicant has appointed a compliance officer;

(9) the applicant has professional competence, financial soundness and general reputation of fairness and integrity in business transactions, to the satisfaction of the Board;

(10) the applicant has, in its employment, persons having adequate professional and other relevant experience to the satisfaction of the Board;

(11) the applicant, and its promoter, is a fit and proper person, as per Schedule II of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008;

(12) neither the applicant, nor any of its promoter or director, is involved in any legal proceeding connected with the securities market, which may have an adverse impact on the interests of the investors;

(13) the applicant, in the past three years from the date of application, has not been –

(a) refused by the Board a certificate of registration under these regulations, or

(b) deemed not fit and proper by the Board, or

(c) subject to any proceedings for a contravention of the Act or of any rules or regulations made under the Act.

(14) the grant of certificate of registration to the applicant is in the interest of investors;

(15) Any other condition as may be specified by the Board from time to time.

|

Views sought on: (i) Whether the above net worth and manpower requirements for Cat-I and Cat-II ERPs appropriate? (ii) Is it appropriate, in order for all ERPs having a level playing field, to require CRAs to set up a subsidiary to conduct ERP rather than do so divisionally or departmentally within the CRA? (iii) Whether the breakeven/revenue/client-based target is appropriate? The provision is intended to protect the interest of investors in securities markets, and prevent ERPs from resorting to malpractice such as indicative ESG ratings or incentivising rating shopping to attract clients. It may be noted that all three targets are based on self-declaration by ERP at the time of registration with SEBI. (iv) Whether the above conditions of registration appropriate? |

Criteria for fit and proper person

28E. For the purposes of determining whether an applicant or ESG rating provider is a fit and proper person, the Board may take into account the criteria specified in Schedule II of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008.

Furnishing of further information, clarification and personal representation

28F. (1) The Board may require the applicant to furnish any such further information or clarification regarding the activities of the ESG rating provider or any such matter connected thereto to consider the application for grant of a certificate or after registration thereon.

(2) If required by the Board, the applicant shall appear before the Board for personal representation.

Procedure for grant of certificate as an ESG rating provider

28G. (1) The Board may grant certificate under any specific category of ESG rating provider, if it is satisfied that the applicant fulfils the requirements as specified in these regulations.

(2) The Board, on being satisfied that the applicant is eligible, shall grant a certificate of registration in Form B of Fourth Schedule and shall send an intimation to the applicant.

(3) The certificate of registration granted under sub-regulation (1) shall be valid unless it is suspended or cancelled by the Board, or surrendered by the ESG rating provider.

(4) The grant of a certificate of registration shall be subject to payment of the registration fees as specified under Part A of Fifth Schedule, in the manner prescribed in Part B thereof.

Conditions of certificate

28H. The certificate of registration shall be subject to the following conditions:

(1) the ESG rating provider shall comply with the provisions of the Act, the regulations made there under and the guidelines, directives, circulars and instructions issued by the Board from time to time;

(2) the ESG rating provider shall forthwith inform the Board in writing if any information or particulars furnished to the Board by the ESG rating provider:

(a) is found to be false or misleading in any material particular; or

(b) has undergone change subsequently to its furnishing at the time of the application for a certificate.

(3) Where the ESG rating provider proposes change in control, it shall obtain prior approval of the Board for continuing to act as such after the change.

(4) the ESG rating provider shall at all times maintain a minimum net worth as specified in this Chapter.

(5) the ESG rating provider shall pay the fees for registration in the manner provided in these regulations;

(6) the ESG rating provider shall meet the targets specified by it under regulation 28D(3) under the specified time frames.

Provided that the above shall not include the projections on cumulative cash losses;

(7) the ESG rating provider only offers products, services, or undertakes activities as permitted under this Chapter and as declared by the provider at the time of application of registration with the Board;

|

Views sought on: (i) Whether the limitations on product/service offerings of ERPs, as prescribed above, appropriate? (ii) Whether the above conditions of certificate of registration require any changes? |

Procedure where certificate is not granted

28l. (1) If, after considering an application made under this Chapter, the Board is of the opinion that a certificate of registration should not be granted, it may, after giving the applicant a reasonable opportunity of being heard, reject the application.

(2) The decision of the Board, not to grant certificate of registration, as the case may be, under sub-regulation (1) shall be communicated by the Board to the applicant within a period of thirty days of such decision, stating the grounds of the decision.

Code of Conduct

28J. Every ESG rating provider shall abide by the Code of Conduct contained in the Sixth Schedule.

Transparency

28K. Every ESG rating provider shall:

(1) Make adequate levels of public disclosure and transparency a priority for its ESG ratings products, including its methodologies and processes.

(2) Disclose its rating methodology for all its products on its websites, while maintaining a balance with respect to proprietary or confidential aspects of the methodologies and include category-wise weightages of environmental, social, and governance factors in ESG ratings, as well as the weightage of high-level themes or key issues in each of the three factors;

(3) Disclose the category of provider to which it belongs in all its website disclosures related to ESG ratings;

(4) Use proper terminologies for the products offered and, if an associate or subsidiary of a credit rating agency, prominently display that ESG ratings are different from credit ratings through website and ESG rating reports;

(5) Disclose any change in ESG rating methodology and consequential change in ESG ratings on its website;

(6) Disclose the extent to which a change in ESG rating is due to a change in the provider’s ESG rating methodology;

(7) Maintain and disclose archives of earlier ESG rating methodologies and ESG ratings on its website;

(8) Disclose ESG rating, type of ESG rating (whether risk-based or impact-based or otherwise), and scores on environmental, social and governance parameters, and any other parameter forming a part of overall ESG rating, on their websites for public access and provide a hyperlink to the methodology placed on website;

(9) Publish, on an annual basis, an evaluation of their ESG-rating methodologies against the outputs which they have been used to produce, in a manner specified by the Board;

(10) Publish their average one-year ESG rating transition rate over a 5-year period, on their respective websites, in a manner as may be specified by the Board;

(11) Disclose, on their website, the general nature of compensation arrangements with clients and whether the ESG ratings assigned were solicited or unsolicited;

(12) Take any other measure that the Board may consider material for a true and fair understanding of the ESG rating.

|

Views sought on: (i) Whether the above prescribed code of conduct for ERPs appropriate (please refer Sixth Schedule below)? (ii) Whether disclosure of ESG rating methodologies by ERPs, as proposed above, appropriate? (iii) Whether ERPs will be able to disclose the extent to which a change in ESG rating is due to a change in the ESG rating methodology? (iv) Whether ERPs be required to publish an annual evaluation of their ESG rating methodologies? The same is in line with IOSCO recommendations and is aimed at periodic analysis (and necessary revisions) of ESG rating methodologies, in view of steep rating migrations in ESG ratings, if any. (As an illustration, steep drop in ESG ratings of companies such as Pacific Gas & Electric – arguably, the first case of a climate-change bankruptcy, despite high ESG ratings by certain providers). (v) Whether the ESG rating transition rates will be an adequate proxy to measure performance of an ERP? This is akin to disclosures by CRAs on credit rating transitions. (vi) Whether the above transparency measures adequate and appropriate? |

Governance and conflict of interest

28L. An ESG rating provider shall:

(1) Identify, avoid, or appropriately manage, mitigate, and disclose potential conflicts of interest.

(2) Formulate policies and internal codes for dealing with the conflict of interest, which shall also be prominently disclosed on its website.

(3) Identify, disclose and, to the extent possible, mitigate potential conflict of interest that may arise between ESG rating provider and its clients or client groups, or among multiple clients, or between the rated entity and clients or client groups, or any other sources.

(4) Take steps to ensure the ESG ratings would not be affected by the existence of, or potential for, a business relationship between the ESG rating provider or their affiliates and any entity for which it provides ESG ratings, or associates of such entity.

(5) Structure reporting lines for their staff and their compensation arrangements to eliminate or appropriately manage actual and potential conflicts of interest related to their ESG ratings.

(6) Not provide consulting or advisory on ESG ratings or areas related to ESG.

(7) adopt and implement written policies and procedures designed to ensure that its decisions are independent, free from any form of undue interference or influence, and appropriately address potential conflicts of interest.

|

Views sought on: Whether the above measures on conflict of interests are appropriate and adequate? If not, please provide any further suggestions to prevent conflict of interest. |

Rating Process

28M. (1) Every ESG rating provider shall have appropriate resources within its group to assign an ESG rating.

(2) Every ESG rating provider shall inform the Board and the general public about new ESG rating instruments or symbols introduced by it.

(3) Every ESG rating provider shall ensure that the ESG rating suitably incorporates the environmental, social and governance aspects that are contextual to the Indian market, in a manner specified by the Board from time to time;

Provided that nothing contained above shall preclude the provider from offering additional ESG rating products or services.

(4) ESG rating definition, as well as the structure for a particular ESG rating product, shall not be changed by an ESG rating provider, without prior information to the Board.

(5) A provider shall disclose to the stock exchange(s) where the rated entity is listed, as well as through press release and websites for general investors, the ESG rating assigned to such entity or its securities, after periodic review, including changes in ESG rating/ reviews, if any.

(6) An ESG rating provider shall have written policies, procedures and internal controls designed to ensure the processes and methodologies are rigorous, systematic, and applied consistently and periodically reviewed and updated.

(7) An ESG rating provider shall have efficient systems to keep track of material ESG-related developments to ensure timely and accurate ESG ratings.

(8) A provider shall attempt to continually improve information gathering process with entities / securities covered by its products.

(9) A provider shall respond to, and address issues flagged by entities covered by its ESG rating products while maintaining the objectivity of these products.

(10) A provider shall share a draft of the ESG rating report with the rated entity before publication of the same. The provider shall also grant such entity an opportunity of appeal and representation before the provider.

|

Views sought on: Whether the above proposed measures on ESG rating process are adequate and appropriate? |

Monitoring of ESG rating

28N. (1) An ESG rating provider shall continuously monitor the rating of a client, unless the rating is withdrawn.

(2) An ESG rating provider shall disseminate information regarding the newly assigned ESG ratings, and changes in ESG earlier rating promptly through press releases and websites.

Procedure for review of ESG rating

28O. (1) An ESG rating provider shall carry out annual periodic reviews of all published ESG ratings, unless the ESG rating is withdrawn, subject to the provisions of sub-regulation (2) of these regulations.

(2) An ESG rating provider shall withdraw an ESG rating as per its documented policies, which shall also be disclosed on its website.

(3) If the listed entity does not co-operate with the ESG rating provider so as to enable the provider to comply with its obligations under this Chapter, despite being under a contractual obligation to do so, the provider shall carry out the review on the basis of the best available information, in the manner as specified by the Board from time to time.

Provided that if owing to such lack of co-operation, an ESG rating has been based on the best available information, the provider shall disclose to the investors the fact that the ESG rating is so based.

Views sought on:

| Whether the proposed measures on monitoring of ESG ratings, withdrawal of ESG ratings and non-cooperation by issuers (under an issuer-pays business model) adequate and appropriate? |

Internal procedures to be framed

28P. (1) An ESG rating provider shall frame appropriate procedures and systems for monitoring the trading of securities by its employees in the securities of its clients, in order to prevent contravention of –

(a) the Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 2015;

(b) the Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices relating to the Securities Market) Regulations, 2003; and

(c) other laws relevant to trading of securities.

(2) An ESG rating provider shall adopt and implement written policies and procedures designed to help ensure the issuance of high quality ESG ratings based on publicly disclosed data sources where possible and other information sources where necessary, using transparent and defined methodologies.

Disclosure of ESG rating definitions and rationale

28Q. An ESG rating provider, while disclosing ESG ratings, shall:

(1) make public the definitions of the concerned ESG rating, along with the symbols;

(2) explicitly state that the ESG ratings do not constitute recommendations to buy, hold or sell any securities;

Submission of information to the Board

28R. (1) The ESG rating provider shall furnish such information as may be called for, by the Board including any report relating to its action within such period as may be specified.

(2) Every ESG rating provider shall, at the close of each accounting period, furnish to the Board copies of its financial statements.

Compliance with circulars etc., issued by the Board

28S. An ESG rating provider shall comply with such guidelines, directives, circulars and instructions as may be issued by the Board from time to time.

Appointment of Compliance Officer

28T. (1) An ESG rating provider shall appoint a compliance officer who shall be responsible for monitoring the compliance of all the applicable laws.

(2) The compliance officer shall immediately and independently report to the Board any non-compliance observed by her or him.

Maintenance of Books of Accounts records, etc.

28U. (1) Every ESG rating provider shall keep and maintain, for a minimum period of five years, the following books of accounts, records and documents, as applicable, namely:

(a) copy of its financial statements as on the end of each accounting period;

(b) a copy of the auditor’s report on its accounts for each accounting period.

(c) a copy of the agreement entered into with each client;

(d) information supplied by each of the client or rated entities;

(e) correspondence with each client or rated entities;

(f) ESG ratings assigned to various entities or securities including up gradation and down gradation (if any) of the ratings so assigned.

(g) ESG rating notes and/or any document outlining the rationale of assigning a particular ESG rating considered at the time of rating;

(h) record of decisions of the ESG rating process;

(i) letter or reports or website press release assigning ESG rating;

(j) particulars of fees charged for ESG rating and such other records as the Board may specify from time to time.

(2) Every ESG rating provider shall intimate to the Board the place where the books of account, records and documents required to be maintained under these regulations are being maintained.

Steps on auditor’s report

28V. Every ESG rating provider shall, within two months from the date of the report of the auditor, take steps to rectify the deficiencies if any, made out in such report, in so far as they relate to the activity of ESG rating.

| Views sought on:

Whether the above proposed measures on internal procedures, rating definitions, maintenance of books, etc. are adequate and appropriate? |

Confidentiality

28W. (1) Every provider shall treat, as confidential, information supplied to it by the rated entities and no provider shall disclose the same to any other person, except where such disclosure is required or permitted by or under any law for the time being in force, or unless explicit consent in writing has been obtained from the rated entities.

(2) Private or confidential information or data shared by any client for purpose other than ESG ratings shall not be used by the ESG rating provider for undertaking ESG ratings, unless explicit consent in writing has been obtained for the same from the said client. No private or confidential information or data shall be obtained from any other entity.

(3) Every provider shall adopt and implement written policies and procedures designed to address and protect all non-public information received related to their ESG rating products.

|

Views sought on: Whether the above proposed measures on confidentiality of information are adequate and appropriate? |

Shareholding in an ESG rating provider

28X. (1) ESG rating provider shall not:

(a) directly or indirectly, hold 10 per cent or more shareholding and/ or voting rights in any other ESG rating provider, or

(b) have representation on the Board of any other ESG rating provider:

Provided that an ESG rating provider may, with the prior approval of the Board, in the interest of investors, market integrity and stability, acquire shares and/ or voting rights exceeding 10 per cent in any other ESG rating provider, if such acquisition results in change in control in the ESG rating provider whose shares are being acquired.

(2) A shareholder holding 10 per cent or more shares and/ or voting rights in a ESG rating provider shall not hold 10 per cent or more shares and/ or voting rights, directly or indirectly, in any other ESG rating provider:

Provided that the said restriction shall not apply to holdings by Pension Funds, Insurance Schemes and Mutual Fund Schemes.

Explanation – For the purpose of these regulations, a “ESG rating provider” means a ESG rating provider registered with the Board.

|

Views sought on: Whether the above proposed measures preventing cross-shareholding among SEBI- registered ERPs appropriate? The same is modelled along the lines of CRAs. |

CHAPTER IV

RESTRICTION ON ESG RATING OF CERTAIN ENTITIES

Definitions

28Y. (1) In this Chapter, unless the context otherwise requires –

(a) “associate”, in relation to a promoter, includes a body corporate in which the promoter holds ten percent or more, of the share capital;

(b) “promoter” means a person who holds ten percent or more, of the shares of the ESG rating provider.

Entities connected with a promoter or a rating agency not to be rated

28Z. (1) No ESG rating provider shall, rate an entity or securities of such entity, which is; –

(a) a borrower of its promoter; or

(b) a subsidiary of its promoter; or

(c) an associate of its promoter, if

i. there are common Chairperson, Directors between ESG rating provider and these entities.

ii. there are common employees.

(2) An ESG rating provider shall not assign ESG rating to an entity promoted by it or its associates, nor shall it rate securities of such entities.

(3) No ESG rating provider shall rate an entity, or securities of such entity, if the ESG rating provider has a Chairperson, director or employee who is also a Chairperson, director or employee of any such entity:

Provided that the ESG rating provider may, subject to the provisions of sub-regulation (1) rate an entity having a common independent director with it if, –

(a) such an independent director does not participate in the discussion on ESG rating decisions, and

(b) the ESG rating provider makes a disclosure in the ESG rating announcement of such associate (about the existence of common independent director) on its Board, and that the common independent director did not participate in the rating process or in the meeting of its Board of Directors, when the rating of such associate was discussed.

Explanation. ─ For the purposes of this sub-regulation the expression ‘independent director’ means a director who, apart from receiving remuneration as a director, does not have any other material pecuniary relationship or transactions with the company, its promoters, its management or its subsidiaries, which in the judgment of the board of the company, may affect the independence of the judgment of such director.

|

Views sought on: Whether the above proposed measures on entities that may not be rated by an ERP appropriate? The same is modelled along the lines of CRAs. |

FOURTH SCHEDULE

[See regulation 28C]

FORMS

FORM A

Application for grant of Certificate of Registration as an ESG rating provider

NAME OF APPLICANT:

NAME OF COMPLIANCE OFFICER:

MOBILE NO:

EMAIL ID:

INSTRUCTIONS FOR FILLING UP FORM –

1. Applicants must submit to the Board a completed application form together with appropriate supporting documents.

2. This application form should be filled in accordance with the regulations.

3. Application for registration will be considered, only if it is complete in all respects.

4. All answers must be typed.

5. Information which needs to be supplied in more detail may be given on separate sheets which should be attached to the application form.

6. All signatures on the application must be original.

7. Every page of the form as well as every additional sheet must be signed by the authorized signatory of the applicant.

8. Application must be accompanied by an application fee as specified in Schedule V to these regulations.

9. All mentions of ‘ratings’ in this Schedule shall be deemed to refer to ESG ratings, unless the context otherwise specifies.

1. PARTICULARS OF THE APPLICANT

1.1. Name, address of the registered office, address for correspondence, mobile number(s), email address of the Applicant. Address of branch offices, if any.

1.2. Name, mobile number and email address of the contact person.

1.3. Category of ESG rating provider to which the application is made.

1.4. If the application is for Category I ESG rating provider, please provide the following information, as applicable:

1.4.1. Details of the intermediary registered with the Board, of which the applicant is a subsidiary.

1.4.2. If promoted by a foreign ESG rating provider, please provide details of such promoter.

1.5. Please provide the following information regarding the applicant’s operations limited to ESG ratings of securities or entities that are listed, or proposed to be listed, at a stock exchange recognized by the Board:

1.5.1. business plan, and

1.5.2. a target breakeven date, and

1.5.3. target revenue and number of clients, within two years of obtaining a certificate of registration as an ESG rating provider, and

1.5.4. cumulative cash losses that the applicant projects to incur until the target breakeven date, along with the activities or areas wherein such losses shall be incurred;

1.6. Please provide a declaration that after being registered with SEBI, the ERP may draw down, from its liquid net worth, an amount equivalent to Para 1.5.4 above only on the areas specified under the business plan submitted at the time of application. Further, provide a declaration that this amount shall not be used in any other manner, except for incurring such expense or maintained as part of the liquid net worth.

1.7. Date of incorporation of the Applicant (enclose certificate of incorporation and memorandum and articles of association). Specify the following:

1.7.1. Objects (Main & Ancillary) of the Applicant company

1.7.2. Authorized, issued, subscribed and paid-up capital

1.8. Legal structure of the Applicant:

1.8.1. Limited company – Private/Public.

1.8.2. Unlimited company.

If listed, names of Stock Exchanges and latest share price to be given.

1.9. Whether the Applicant or its associates are registered with the Board or any other regulatory authority in any capacity, along with details of registration.

1.10. Whether the Applicant belongs to:

1.10.1. Company already in the business of undertaking ESG rating activities

1.10.2. Company proposing to undertake ESG rating activities for the first time.

2. ELIGIBILITY CRITERIA

2.1. Category to which the promoter(s) of the Applicant belong to (refer regulation 28D).

2.2. Name the promoters and indicate their shareholding in the company.

2.3. Enclose a Chartered Accountant’s certificate certifying the continuous net worth of the promoter referred to in regulation 28D(5), if applicable.

2.4. Net worth of the company as per the last audited accounts not earlier than three months from the date of application. Enclose a Chartered Accountant’s certificate certifying the same.

3. PARTICULARS OF DIRECTORS/KEY PERSONNEL

3.1. Particulars of Directors of the company, which shall include name, qualification, experience, shareholding in the company and directorship in other companies. (Enclose identity proof and address proof of the directors)

3.2. Particulars of Key Personnel of the company, which shall include name, designation in the company, qualification, and previous positions held, experience, date of appointment in the company and functional areas.

4. INFRASTRUCTURE

4.1. Details of infrastructure including computing facilities, office space, equipment, manpower, facilities for research and database available with the company and whether the existing infrastructure is adequate to carry on the rating activities proposed to be undertaken by the company.

4.2. Any further plan for additional/ improved infrastructure, and declaration of remote work environment, if any, to be indicated.

5. MAJOR SHAREHOLDERS

5.1. List of major shareholders (holding 5% and above of applicant directly or along with associates)

Shareholding as on:

| Name of shareholder | No. of Shares held | %age of total paid up capital of the company |

6. ASSOCIATE CONCERNS

6.1. Particulars of associate companies/concerns which shall include name, address, type of activity handled, nature of interest of the Applicant company in the associate, nature of interest of promoter(s) of the applicant in the associate.

6.2. Whether the Board has granted/ refused registration as ESG rating provider to any associate of the applicant. Give the details like date of application, date of refusal/registration, reasons for refusal etc.

7. BUSINESS INFORMATION OF THE COMPANY

7.1. History, major events and present activities. Details of Experience in Rating activities and other related activities

7.2. If the company is proposing to engage in ESG rating activities for the first time, business plan of the company with projected volume of activities and income for which registration is sought to be specifically given.

7.3. Rating activities handled during the last three years as per the table below:

| Name of Client | Size of issue | Year of Issue | Security/Instrument Rated | listed/unlisted |

7.4. Details of other rating activities undertaken during last three years

7.5. Any other information considered relevant to the nature of services rendered by the applicant.

8. FINANCIAL INFORMATION ABOUT THE APPLICANT

8.1. Net worth (Rs. In Lacs)

|

Items |

Year prior to the preceding year of the current year | Preceding year | Current year |

| (a) Paid-up equity capital |

|||

| (b) Free reserves (excluding reserves created out of revaluation) |

|||

| Total (a) + (b) | |||

| (c)Accumulated Losses |

|||

| (d) Deferred expenditure not writtenoff, including miscellaneous expenses not written off | |||

| Net worth (a) + (b) – (c) – (d) |

Please enclose audited annual accounts for the last three years. Where unaudited reports are submitted, give reasons. If minimum net worth Requirement has been met after last audited annual accounts, audited statement of accounts of a later date also be submitted.

8.2. Provide a declaration that the net worth is in compliance of the applicant is in compliance with these regulations. Submit relevant documentation to support the same.

8.3. Name and Address of the Principal bankers of the Applicant Company.

8.4. Name and address of the Auditors.

9. OTHER INFORMATION

9.1. Details of all pending litigations against the applicant company, directors and employees:

Nature of dispute Name of the party Status

9.2. Indictment or involvement in any legal proceeding connected with the securities market by the applicant or any of its directors, or key managerial Personnel in the last three years;

9.3. Details of previous application to the Board as an ESG rating provider, if any.

9.4. If the applicant has, in the past, been deemed not ‘fit and proper’ by the Board, please provide relevant details of the same.

10. DECLARATION

10.1. Give the following declarations signed by two directors:

I/We hereby apply for registration.

I/We warrant that I/We have truthfully and fully answered the questions above and provided all the information which might reasonably be considered relevant for the purposes of my registration.

I/We declare that the information supplied in the application form is complete and correct.

For and on behalf of

| (Name of Applicant) | |

| Director

Name in Block Letters |

Director

Name in Block Letters |

| Date | Date |

FORM – B

[See regulation 28G]

Certificate of Registration as an ESG rating provider

I. In exercise of the powers conferred by sub-section (1) of section 12 of the Securities and Exchange Board of India Act, 1992 (15 of 1992), read with the rules and regulations made thereunder, the Board hereby grants a certificate of registration to ___________________ as an Environmental, Social, and Governance (ESG) rating provider, under Category-_________ , in accordance with and subject to the conditions in the regulations to carry out the activity of the ESG rating provider: –

II. The category of the ESG rating provider shall be –

III. Registration Code for the ESG rating provider is

IN/ERP/(Category)/_________ .

IV. This certificate of registration shall be valid till it is suspended or cancelled by the Board.

Place:

Date

By Order

Sd/-

For and on behalf of

Securities and Exchange Board of India

FIFTH SCHEDULE

[See regulations 28C and 28G]

FEES FOR ESG RATING PROVIDERS

PART A

Amount to be paid as Fees

| 1. | Application fee for grant of registration | ₹ 50,000 |

| 2. | Registration Fees

(a) Category I (b) Category II |

(a) ₹ 10,00,000

(b) ₹ 1,00,000 |

| 3. | Recurring registration fee

(For every three years) (a) Category I (b) Category II |

(a) ₹ 5,00,000

(b) ₹ 50,000 |

PART B

1. An ESG rating provider who has been granted certificate of registration under regulation 28G, shall pay fees, as specified under item 2 of Part A, within fifteen days from the date of receipt of intimation from the Board.

2. A provider who has been granted certificate of registration, to keep its registration in force, shall pay fee as specified under item 3 of Part A, for every three years from the sixth year of the date of grant of certificate of registration or of the date of grant of certificate of initial registration granted prior to the commencement of the Securities and Exchange Board of India.

3. The fee specified above shall be paid by way of direct credit in the bank account through online payment using SEBI payment gateway.

4. The (recurring) registration fee payable every three years as specified under item no. 3 of Part A, shall be paid by the ESG rating provider one month before the expiry of the block for which the fee has been paid.

SIXTH SCHEDULE

[See regulation 28J]

CODE OF CONDUCT FOR ESG RATING PROVIDERS

1. An ESG rating provider shall make all efforts to protect the interests of investors.

2. An ESG rating provider, in the conduct of its business, shall observe high standards of integrity, dignity and fairness in the conduct of its business.

3. An ESG rating provider shall fulfil its obligations in a prompt, ethical and professional manner.

4. An ESG rating provider shall, at all times, exercise due diligence, ensure proper care and exercise independent professional judgment in order to achieve and maintain objectivity and independence in the ESG rating process.

5. An ESG rating provider shall maintain records to support its decisions.

6. An ESG rating provider shall have in place a ESG rating process that reflects consistent rating standards.

7. An ESG rating provider shall not indulge in any unfair competition, nor shall it wean away the clients of any other ESG rating provider on assurance of higher or lower ESG rating.

8. An ESG rating provider shall keep track of all important changes relating to the entities or securities it rates and shall develop efficient and responsive systems to yield timely and accurate ratings. Further, an ESG rating provider shall also monitor closely all relevant factors that might affect the ESG characteristics of the rated entities or their securities.

9. An ESG rating provider shall, wherever necessary, disclose to the client, possible sources of conflict of duties and interests, which could impair its ability to make fair, objective and unbiased ratings. Further, it shall ensure that no conflict of interest exists between any member participating in the rating analysis, and that of its entity who is being rated or whose securities are being rated.

10. An ESG rating provider shall not make any exaggerated statement, whether oral or written, to the client either about its qualification or its capability to render certain services or its achievements with regard to the services rendered to other clients.

11. An ESG rating provider shall not make any untrue statement, suppress any material fact or make any misrepresentation in any documents, reports, papers or information furnished to the Board, stock exchange or public at large.

12. An ESG rating provider shall ensure that the Board is promptly informed about any action, legal proceedings etc., initiated against it alleging any material breach or non-compliance by it, of any law, rules, regulations and directions of the Board or of any other regulatory body.

13. An ESG rating provider shall maintain an appropriate level of knowledge and competence and abide by the provisions of the Act, regulations and circulars, which may be applicable and relevant to the activities carried on by the ESG rating provider. The ESG rating provider shall also comply with award of the Ombudsman passed under the Securities and Exchange Board of India (Ombudsman) Regulations, 2003.

14. An ESG rating provider shall ensure that there is no misuse of any privileged information including prior knowledge of ESG rating decisions or changes.

15. An ESG rating provider or any of its employees shall not render, directly or indirectly any investment advice about any security being rated or about any rated entity in the publicly accessible media.

16. An ESG rating provider shall ensure that any change in registration status/any penal action taken by the Board or any material change in financials which may adversely affect the interests of clients/investors is promptly informed to the clients and any business remaining outstanding is transferred to another registered person in accordance with any instructions of the affected clients/investors.

17. An ESG rating provider shall maintain an arm’s length relationship between its ESG rating activity and any other activity.

18. An ESG rating provider shall develop its own internal code of conduct for governing its internal operations and laying down its standards of appropriate conduct for its employees and officers in the carrying out of their duties within the ESG rating provider and as a part of the industry. Such a code may extend to the maintenance of professional excellence and standards, integrity, confidentiality, objectivity, avoidance of conflict of interests, disclosure of shareholdings and interests, etc. Such a code shall also provide for procedures and guidelines in relation to the establishment and conduct of the officers and employees serving in the rating process.

19. An ESG rating provider shall provide adequate freedom and powers to its Compliance officer for the effective discharge of his duties.

20. An ESG rating provider shall ensure that the senior management, particularly decision makers have access to all relevant information about the business on a timely basis.

21. An ESG rating provider shall ensure that good corporate policies and corporate governance are in place.

22. ESG rating provider shall not, generally and particularly in respect of entities or securities rated by it, be party to or instrumental for—

(a) creation of false market;

(b) price rigging or manipulation; or

(c) dissemination of any unpublished price sensitive information in respect of securities which are listed and proposed to be listed in any stock exchange, unless required, as part of rationale for the rating accorded.

********

|

Category I ESG Rating Provider |

Category II ESG Rating Provider | ||

| Services Offered |

(I) ESG rating of listed, or proposed to be listed, entities and/or securities; or

(II) Any other product, service or activity as may be specified by SEBI, or (III) ESG rating of any other product, service or activity as may be required by another financial sector regulator or authority (specified by SEBI) under the guidelines of such regulator or authority; |

||

| [Additionally, basis suggestions on the differences in categorization of Cat-I and Cat-II ERPs, restrictions / prohibitions shall be specified for Cat-II ERPs, for example, Cat-II ERPs shall not undertake certification of green debt securities.] | |||

| Net worth | Net worth of not less than ₹ 5 crores at all points in time. | Not worth of not less than ₹ 10 lakh | |

| Provided that at the time of making application, the minimum net worth of the “Category I ESG rating provider” shall not be less than the higher of, ₹10 crore, or addition of ₹10 crore and the cumulative cash losses projection made by the applicant under Regulation 28D(3); | at all points in time.

Provided that at the time of making application, the minimum net worth of the “Category II ESG rating provider” shall not be less than the higher of, ₹ 20 lakh, or addition of ₹ 20 lakh and the cumulative cash losses projection made by the applicant under Regulation 28D(3); |

||

· Net worth shall be in the form of positive liquid net worth, i.e., deployed in liquid assets which are unencumbered.

|

|||

| Entities Eligible |

Entity incorporated in India under Companies Act, 2013; CRAs or SEBI-registered intermediaries not eligible; | ||

| (i) Constituted as a subsidiary of an intermediary registered with the Board, or (ii) a subsidiary of a foreign ESG rating provider incorporated in a Financial Action Task Force (FATF) member jurisdiction and recognized under their law, having a minimum experience of five years in rating securities or companies; Provided that an ERP should not hold a certificate of registration with SEBI | (no such requirement for Cat-II) | ||

| Promoter Req. |

Promoter of the ERP must be a ‘fit and proper person’ as stated in Schedule II of SEBI (Intermediaries) Regulations, 2008 | ||

| Cat-I ERP must be promoted by one of the following:

(a) an entity regulated by financial sector regulator viz. SEBI, RBI, IRDAI, PFRDA, subject to receipt of requisite approval from the concerned regulator or authority; (b) a foreign ERP incorporated in a FATF member jurisdiction and recognized under their law, having a minimum experience of five years in ESG rating of securities or companies; (c) a CRA registered with SEBI; or (d) an entity having continuous net worth of minimum rupees 100 crores as per its audited annual accounts for the previous five years prior to filing of the ERP application with SEBI Provided further that the promoter shall maintain a minimum shareholding of 26% in the ESG rating provider for a minimum period of five years from the date of grant of registration by the Board. |

(no such requirement for Cat-II) | ||

| Manpower Req. | at least ten employees specialised in the following areas, at all points of time, with at least one specialist in each of the following areas:

(i) governance, (ii) sustainability, (iii) social impact or social responsibility, (iv) data analytics, (v) finance, (vi) information technology, (vii) law |

at least five employees specialised in the following areas, at all points of time, with at least one specialist in each of the following areas:

i. governance, ii. sustainability, iii. social impact or social iv. data analytics |

|

| Remote Work / WFH |

May be offered by Cat-I ERPs, but they are still required to have an ‘adequate office space’ | If desired so by Cat-II ERPs, then requirement for an ‘adequate office space’ shall not be applicable | |

| Business Plan-based Targets |

(i) a target revenue within two years of registration, and (ii) target number of clients within two years of registration, and (iii) target breakeven date. (iv) projected cumulative losses by breakeven date, and areas wherein the same may be incurred.

|

||

| Fees to SEBI |

Application Fee – 50,000 | ||

| Registration Fee – 10 Lakhs

Recurring Registration Fee (for every three years) – 5 Lakhs |

Registration Fee – 1 Lakh

Recurring Registration Fee (for every three years) – 50,000 |

||

Refer Part A of this Consultation

****************

Notes:-

1 Berg, Florian and Kölbel, Julian and Rigobon, Roberto, Aggregate Confusion: The Divergence of ESG Ratings (August 15, 2019). Forthcoming Review of Finance, Available at SSRN: https://ssrn.com/abstract=3438533 or http://dx.doi.org/10.2139/ssrn.3438533

2 Registration of CRAs

3 General Obligations of CRAs

4 Restriction on rating of securities issued by promoters or by certain other persons – these provisions have been provided separately for ERPs

5 “Preliminary” – Short title; definitions

6 Procedure for Inspection and Investigation

7 Procedure for action in case of default

8 Power to relax strict enforcement of the regulations

9 who shall undertake activities, or offer products or services, as specified in this Chapter