The Securities and Exchange Board of India (SEBI) has released a consultation paper to propose changes to the ICDR Regulations, 2018, aiming to improve the process for Initial Public Offerings (IPOs). The proposals address three key areas. First, SEBI plans to revise the rules for anchor investor allocation, suggesting an increase in the number of permitted investors for larger IPOs to accommodate multiple funds from a single Foreign Portfolio Investor (FPI). Second, it proposes to include life insurance companies and pension funds in the reserved anchor portion, increasing the total reserved allocation for these long-term institutional investors from 33% to 40%, with a specific 7% reservation for insurance and pension funds. Third, for large IPOs exceeding ₹5,000 crore, SEBI suggests adjusting the retail investor portion from 35% down to 25% and increasing the Qualified Institutional Buyer (QIB) share to a maximum of 60%. Additionally, the reservation for mutual funds within the non-anchor QIB category would increase from 5% to 15%. These changes are intended to align with market trends, reduce potential undersubscription in large retail categories, and attract a broader base of long-term institutional investors. Public comments on these proposals are invited until August 21, 2025.

Securities and Exchange Board of India

Consultation Paper on Facilitating Ease of Doing Business relating to Anchor Investor Allocation, Long-Term Institutional Participation and Retail Quota in Initial Public Offerings (IPO) under ICDR Regulations 2018

1. Objective:

1.1. This consultation paper seeks comments / suggestions from the public on the following proposals relating to amendments to SEBI (ICDR) Regulations, 2018, (“ICDR Regulations”) with the objective of facilitating ease of doing business and addressing practical challenges in the current framework relating to:

1.1.1. Discretionary allotment under Anchor portion in Initial Public Offer (IPO)

1.1.2. Reservation for Allocation for Life Insurance Companies registered with IRDAI and Pension Funds registered with PFRDA along with Domestic Mutual Funds in the Anchor Book

1.1.3. Flexibility in sizing the retail portion in large IPOs

1.2. The proposals relating to above provisions are discussed in the separate sections which are as under:

1.2.1. Section I: Discretionary allotment under Anchor portion in IPO

1.2.2. Section II: Reservation for Allocation for Life Insurance Companies registered with IRDAI and Pension Funds registered with PFRDA along with Domestic Mutual Funds in the Anchor Book

1.2.3. Section III: Flexibility in sizing the retail portion in large IPOs

Issued on: July 31, 2025

Section – I

1. Discretionary allotment under Anchor portion in IPO:

1.1. Existing provisions:

1.1.1. In terms of the regulation 32(3) of ICDR Regulation, in an issue made through the book building process, the issuer may allocate up to sixty per cent. of the portion available for allocation to qualified institutional buyers to anchor investors in accordance with the conditions specified in this regard in Schedule XIII of ICDR.

1.1.2. In terms of the Schedule XIII, the allocation to anchor investors in case of public issue on the main board, through the book building process, shall be on discretionary basis and subject to the following:

| Category | Anchor Allocation Size ( ₹crore) | No. of Permitted Investors | Minimum Allotment per

Investor ( ₹ crore) |

| I | Up to 10 | Maximum 2 | 5 |

| II | Above 10 and up to 250 | Minimum 2 and Maximum 15 | 5 |

| III | Above 250 | Minimum 5 and Maximum 15 for first ₹250 crore, plus 10 additional investors for every additional ₹250 crore or part thereof | 5 |

1.1.3. Further, one-third of the anchor investor portion shall be reserved for domestic mutual funds.

1.2. Need for review:

1.2.1. Representation has been received from stakeholders to review the limit of maximum Anchor investors allowed for allocations based on size of Anchor portion as prescribed in the current framework mentioned above. The need for such review arises as each FPI fund investing in the Anchor portion is considered separate application for allocation in the Anchor portion despite having the same beneficial owner (due to each FPI fund having a different PAN and PAN being the identifier for each investor) thereby limiting the ability of different FPI funds (with the same beneficial ownership) to invest in the Anchor portion or leading to an exhaustion of the available investor limits, in certain situations.

1.2.2. This may put FPI at a disadvantage compared to Mutual Funds where schemes of a Mutual Fund are considered as a single application for allotment, given Mutual Fund has one PAN.

1.2.3. Moreover, FPIs are active participants in IPOs; however, the current cap on the discretionary (Anchor) portion poses challenges in attracting certain investor classes—such as large FPIs and global investment funds,—who typically have diverse investment horizons and prefer large, assured allocations. Many of these global funds also follow a minimum investment size criterion, which becomes difficult to meet under the existing framework.

1.2.4. Further, over the past five years, the average IPO size on the main board has been approximately above ₹3000 crore, with even the smallest IPOs typically exceeding ₹300–₹500 crore. In light of this, the use of Category I under Schedule XIII of SEBI ICDR Regulations, which permits anchor allocation of up to ₹10 crore to a maximum of two investors, has become virtually redundant.

1.3.Proposals and Rationale:

Proposal 1

1.3.1. In order to address the above issue, it is proposed to increase the number of permissible Anchor Investor allottees for allocations above ₹250 crore. Specifically, a minimum of 5 and a maximum of 15 investors shall be allowed for allocations up to ₹250 crore. For every additional ₹250 crore or part thereof, an additional 15 investors instead of 10 may be permitted, subject to a minimum allotment of ₹5 crore per investor.

1.3.2. The proposal aims to ease participation for large FPIs operating multiple funds with distinct PANs, which currently face allocation limits due to line caps. By increasing the number of permissible anchor lines, the framework would accommodate such investors, enabling larger, more diversified anchor books and attracting global funds with minimum size criteria.

1.3.3. As a result of the above proposal, the number of applications where the size of the Anchor portion is between Rs. 250 crore and Rs. 500 crore, will increase by 5 allottees from the existing 25 to 30. Moreover, the impact analysis at different Anchor portion sizes is given below, and demonstrates the increase in the number of lines pursuant to the suggested change:

| IPO Size (Rs. crore) | Anchor Size (Assuming 30%) (Rs. crore) | Max No. of application as per Current Regulations | Max No. of application as per Proposal |

| 250 | 75 | 15 | 15 |

| 500 | 150 | 15 | 15 |

| 833 | 250 | 15 | 15 |

| 835 | 251 | 25 | 30 |

| 1,000 | 300 | 25 | 30 |

| 1,500 | 450 | 25 | 30 |

| 2,500 | 750 | 35 | 45 |

| 5,000 | 1,500 | 65 | 90 |

| 10,000 | 3,000 | 125 | 180 |

| 15,000 | 4,500 | 185 | 370 |

| 25,000 | 7,500 | 365 | 450 |

| 30,000 | 9,000 | 365 | 540 |

Proposal 2:

1.3.4. In view of the para 1.2.4 , it is proposed to Merge Category I with Category II, such that for any anchor investor allocation up to ₹250 crore, the following norms shall apply:

1.3.4.1. Minimum of two anchor investors

1.3.4.2. Maximum of fifteen anchor investors

1.3.4.3. Minimum allotment of ₹5 crore per anchor investor

1.3.5. Given the prevailing deal sizes, most issuances fall within the threshold of Category II or higher, which prescribes participation by a larger pool of anchor investors with a higher minimum allocation. Hence, Category I has limited practical relevance in the current market context and may be reconsidered or rationalized to reflect the evolved IPO landscape.

1.4. Amendment to ICDR Regulations:

1.4.1. The proposed amendments to Schedule XIII of ICDR Regulations are placed at Annexure I.

1.5. Public comments:

1.5.1. Public comments / suggestions are invited on the following:

Proposal 1: Whether the increase in the number of permissible Anchor Investor allottees for allocations above ₹250 crore as proposed above is required?

Proposal 2: Whether the merger of category I with category II under Anchor Investor allocations as proposed above poses any challenge to Issuer?

Section – II

1. Reservation for Allocation for Life Insurance Companies registered with IRDAI (‘Insurance Companies’) and Pension Funds registered with PFRDA (‘Pension Funds’) along with Domestic Mutual Funds (‘Mutual Funds’) in the Anchor Book

1.1. Existing Provision:

1.1.1. As per Schedule XIII of ICDR Regulations, one third of the anchor portion is reserved for MFs (subject to demand). Moreover, as per Regulation 32 of ICDR, there is also a reservation of up to 5% for Mutual Funds in the non-anchor qualified institutional buyers book. Currently there is no reservation for Insurance Companies or Pension Funds in the anchor portion.

1.2. Need for review:

1.2.1. In the context of source of funds, while Mutual Funds are retail and institutional driven products, Insurance Companies draw their funds from 2 sources:

1.2.1.1. Policyholder corpus and Shareholder corpus (built up with the profits/ surplus accrued)

1.2.1.2. ULIPs which are equity linked products

1.2.2. Insurance Companies typically have stable source of funds as insurance products are viewed more as safety products than yield products.

1.2.3. Further, IRDAI has certain conditions on Insurance Companies investing in IPOs including size limits, good performance record, dividend track record, actively traded within 3 months of listing, etc.

1.2.4. The following trend is seen in case of subscription by Insurance Companies in the anchor portion of recent large issues: Allocation to Insurance Companies have been ~3-11%, with an average of ~6%. In fact, it is only recently in the last 1 year that the Insurance Companies interest in IPOs/ anchor portion has increased.

| S. No. | Issuer | Issue Size (Rs. crore) |

% allocation to Insurance Companies in the Anchor Portion |

| 1 | HDB Financial Services | 12,500 | 11.00% |

| 2 | Vishal Mega Mart | 8,000 | 5.63% |

| 3 | Hexaware Technologies | 8,750 | 3.23% |

| 4 | Hyundai Motors | 27,850 | 9.32% |

| 5 | Bajaj Housing | 6,560 | 11.08% |

| 6 | LIC India | 20,557 | 5.5% |

| 7 | Zomato | 9,375 | 0.7% |

| 8 | Star Health | 6,019 | 6.7% |

| Average | 6.65% |

1.2.5. While Pension Funds are allowed to invest in IPOs, they have certain restrictions. Additionally, Pension Fund Regulatory and Development Authority (PFRDA) has permitted pension funds to invest in IPOs of companies that are part of the top 200 companies by market cap listed on the BSE and NSE.

1.3. Proposals and Rationale:

Proposal 1

1.3.1. It is proposed to include Insurance Companies and Pension Funds in the reserved category of Anchor Portion along with Mutual Funds.

Proposal 2

1.3.2. It is also proposed to increase the reservation from existing thirty three per cent to forty per cent of the anchor investor portion for Life insurance companies registered with IRDAI, pension funds registered with PFRDA and domestic mutual funds.

Provided that one-third of the anchor investor portion shall be reserved for domestic mutual funds, and the remaining 7% shall be reserved for Insurance companies and Pension Funds. In case of undersubscription by Insurance Companies / Pension Funds in the 7% reservation for them, the unsubscribed portion of such reservation shall be available to domestic Mutual Funds.

1.3.3. With growing interest from insurance companies and pension funds in IPOs, the proposed increase in anchor reservation to 40% will ensures their participation. It would diversify the long-term investor base while retaining the existing one-third reservation for mutual funds, enhancing the depth and stability of anchor investments.

1.4. Amendment to ICDR Regulations:

1.4.1. The proposed amendments to Schedule XIII of ICDR Regulations are placed at Annexure I.

1.5. Public comments:

1.5.1. Public comments / suggestions are invited on the following:

Proposal 1: Whether the increase in the reservation limit available under the anchor allotment for specified institutions as proposed above is required?

Proposal 2: Whether the inclusion of Insurance Companies and Pension Funds under the reservation category exists in Anchor allotment as proposed above appropriate?

Section – III

1. Flexibility in sizing the retail portion in large IPOs

1.1. Existing Provision: Regulation 32 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“SEBI ICDR Regulations”) prescribes the manner of allocation in the net offer to the public for the Retail Individual Investors (RIIs), Non-Institutional investors(NIIs) and Qualified institutional Buyers(QIBs). The existing issue structure for an IPO through the book building process is summarised below:

| Investor category | IPOs under ICDR Regulation 6(1)* | IPOs under ICDR Regulation 6(2) |

Allocation |

| a) Retail individual investors (Bid of upto Rs. 2 lac) | Not less than 35% | Not more than 10% | Proportionate subject to minimum bid lot ^ |

| a) Non-Institutional (NII) | |||

| Non-Institutional 1 (Bid Rs. 2 – 10 lacs) | Not less than 5% | Not more than 5% | Proportionate subject to minimum bid lot^ |

| Non-Institutional (Bid > Rs. 10 lacs) | Not less than 10% | Not more than 10% | Proportionate subject to minimum bid lot^ |

| b) QIBs | Not more than 50% |

Not less than 75% |

|

| Anchor portion | 60% of the QIB portion, with 33% reservation to mutual funds (MFs), subject to demand, with allocation on a discretionary basis | 60% of the QIB portion, with 33% reservation to MFs, subject to demand, with allocation on a discretionary basis | Discretionary |

| Main Book QIB (Non-Anchor) |

40% of the QIB portion, of which atleast 5% allocated to MFs | 40% of the QIB portion, of which atleast 5% allocated to MFs | Proportionate |

| *Unsubscribed portion in Retail and NII portions may be allocated to applicants in any other portion.

^ Minimum bid lot: Rs. 12,000 – 15,000 in the Retail portion and >Rs. 2 lac In the NII portion. Note 1: Reservation for MFs in the QIB category is subject to demand. Note 2: The percentages mentioned in (a), (b) and (c) above are allocations in the net offer to the public (being the total offer to the public excluding any IPO reservations). |

|||

1.2. Need for review:

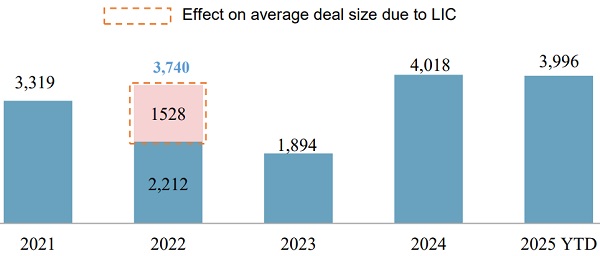

1.2.1. The average IPO size has been on the rise, and for IPOs > Rs. 1,000 crore, average issue size has been ~Rs. 4,000 crore in CY2024, likely to increase further in CY2025 and 2026. This reflects the maturity and growing confidence in the Indian capital markets.

1.2.2. Despite market fluctuations, Retail investors have continued to invest in the capital markets through MFs. While direct participation by Retail investors has remained flat over the last 3 years, their participation through MFs has seen a secular uptick.

1.2.3. The Indian mutual fund industry has crossed Rs. 70 lakh crore in AUM in May 2025, reaching new highs, driven by robust Retail participation and consistent SIP inflows. The growth of SIPs is particularly encouraging, indicating a shift towards disciplined, long-term investment. Monthly SIP contributions stood at a record Rs. 26,688 crore in May 2025, which also marked the industry’s 51st consecutive month of positive equity inflows.

| Year | Total SIP Flows (Rs. crore) | Monthly Avg SIP Flows (Rs. crore) |

| 2025 YTD | 131,645 | 26,329 |

| 2024 | 268,323 | 22,360 |

| 2023 | 183,741 | 15,312 |

| 2022 | 149,437 | 12,453 |

| 2021 | 114,016 | 9,501 |

1.2.4. For large sized IPOs, Retail and NII subscription has remained muted. While conglomerate and popular PSU IPOs like Bajaj Housing Finance, Tata Tech, LIC, Bharti Hexacom etc., saw robust response from Retail/ NII, other issuers coming to the equity market with large sized IPOs saw an undersubscription in both categories.

IPOs since 2022 with deal value >= Rs. 5,000cr |

Retail |

NII |

Overall |

||||||||

S. no. |

Company |

Period |

6(1)/6(2) |

Offer

|

PortionSize

|

Bids

|

Subs (x) |

Portion

|

Bids (Rs. cr) |

Subs

|

Subs

|

1 |

Hyundai Motor |

Oct-24 |

6(1) |

27,859 |

9,758 |

4,294 |

0.4 |

4,158 |

2,381 |

0.6 |

2.4 |

2 |

LIC |

May-22 |

6(1) |

20,557 |

6,270 |

10,094 |

1.6 |

2,814 |

6,686 |

2.4 |

3.0 |

3 |

HDB Financial |

Jun-25 |

6(1) |

12,500 |

3,931 |

5,851 |

1.5 |

1,685 |

17,780 |

10.6 |

17.6 |

4 |

Swiggy |

Nov-24 |

6(2) |

11,327 |

1,134 |

1,202 |

1.1 |

1,695 |

664 |

0.4 |

3.6 |

5 |

NTPC Green |

Nov-24 |

6(2) |

10,000 |

881 |

3,170 |

3.6 |

1,320 |

1,114 |

0.8 |

2.6 |

6 |

Hexaware Tech. |

Feb-25 |

6(1) |

8,750 |

3,156 |

316 |

0.1 |

1,299 |

274 |

0.2 |

2.8 |

7 |

Vishal Mega Mart |

Dec-24 |

6(1) |

8,000 |

2,804 |

6,842 |

2.4 |

1,200 |

17,948 |

15.0 |

28.8 |

8 |

Bajaj Housing |

Sep-24 |

6(1) |

6,560 |

2,050 |

15,459 |

7.5 |

879 |

37,664 |

42.8 |

67.4 |

9 |

Ola Electric |

Aug-24 |

6(2) |

6,146 |

613 |

2,368 |

3.9 |

921 |

2,028 |

2.2 |

4.5 |

10 |

Afcons Infra. |

Oct-24 |

6(1) |

5,430 |

1,899 |

1,785 |

0.9 |

811 |

4,241 |

5.2 |

2.8 |

11 |

Delhivery |

May-22 |

6(2) |

5,235 |

522 |

141 |

0.3 |

782 |

32 |

0.0 |

1.6 |

–

IPOs above Rs. 5,000 crs since 2022 |

|||||||||||

Issuer |

Issue

|

Offer Type |

Offer

|

Offer Price (Rs. per Share) |

Market Cap at Offer Price (Rs. crs) |

Offer

|

Listing Date |

Closing Price on Listing Date (Rs. per Share) |

Premium/ Discount(%) |

CMP

|

Premium/ Discount(%) |

HyundaiMotor |

15/10/2024 |

IPO |

27,870 |

1,960 |

1,59,258 |

17.50% |

22/10/ 2024 |

1,819.60 |

-7% |

2,135.80 |

9% |

LIC |

04/05/2022 |

IPO |

21,008 |

949 |

6,00,242 |

3.50% |

17/05/ 2022 |

875.25 |

-8% |

932.65 |

-2% |

HDBFinancial |

25/06/2025 |

IPO |

12,500 |

740 |

61,388 |

20.36% |

02/07 /2025 |

840.95 |

14% |

814.85 |

10% |

Swiggy |

06/11/2024 |

IPO |

11,329 |

390 |

87,300 |

12.98% |

13/11 /2024 |

456.00 |

17% |

389.85 |

0% |

NTPC Green |

19/11/2024 |

IPO |

10,010 |

108 |

91,010 |

11.00% |

27/11/ 2024 |

121.65 |

13% |

111.98 |

4% |

Hexaware Tech. |

12/02/2025 |

IPO |

8,759 |

708 |

43,025 |

20.36% |

19/02/ 2025 |

762.55 |

8% |

857.40 |

21% |

Vishal Mega Mart |

11/12/2024 |

IPO |

8,000 |

78 |

35,168 |

22.75% |

18/12/ 2024 |

111.93 |

44% |

137.63 |

76% |

BAJAJ HOUSING |

09/09/2024 |

IPO |

6,560 |

70 |

58,297 |

11.25% |

16/09/ 2024 |

165.00 |

136% |

123.36 |

76% |

OLAELECTRIC |

02/08/2024 |

IPO |

6,146 |

76 |

33,522 |

18.33% |

09/08/ 2024 |

91.20 |

20% |

42.29 |

-44% |

Afcons Infra. |

25/10/2024 |

IPO |

5,433 |

463 |

17,029 |

31.90% |

04/11/ 2024 |

474.20 |

2% |

419.45 |

-9% |

Delhivery |

11/05/2022 |

IPO |

5,236 |

487 |

35,284 |

14.84% |

24/05/ 2022 |

536.35 |

10% |

421.15 |

-14% |

1.2.5. In large IPOs, the Retail investor category is also large, especially under Reg 6(1) IPOs requiring 35% of the offer to Retail investors. Given the allocation methodology and experience in recent deals, these large Retail portions require lacs of Retail applicants for the Retail portion to be fully subscribed. For e.g. a Rs. 5,000 crore IPO depending upon the minimum retail application size would need about 7- 8 lac bidders and many more in larger offerings. Simply put, in case of large IPOs, the size of the Retail portion increases substantially and requiring significant Retail participation. This is specially challenging in tepid or uncertain markets. Due to global situations and conflicts in different parts of the world, equity markets have been volatile resulting in launch windows becoming narrower. While overflow of demand is permitted in IPOs from retail to QIB category, undersubscription has a negative impact on the sentiment for the IPO and also creates a negative perception.

1.2.6. Further, from data across over 280 IPOs since 2020, it is observed that, given the allocation methodology in retail portion, the average application size is approx. Rs. 20,000. This would translate into a need for at least 7-8 lac applications for an IPO of Rs 5000 cr and at least 17.50 lac applications for an IPO of Rs. 10,000 crore for one time subscription.

1.3. Proposal and Rationale:

Proposal 1

1.3.1. In light of the above, it is proposed to revise the issue structure for large IPOs (i.e., those exceeding ₹5,000 crore) under Regulation 6(1) of the SEBI (ICDR) Regulations. Specifically, the allocation to the Retail category may be reduced from the existing 35% to 25% in a graded manner, while the allocation to the QIB category may be increased from 50% to 60% (upto 8000 crore) in a graded manner.

1.3.2. It may be noted that in QIB there is reservation for MFs in both anchor and non-anchor portion which also represents Retail Individual Investors indirectly. Reducing the retail portion from 35% to 25% in a graded manner and increasing the QIB share to 60% in a graded manner better reflects market realities, ensures demand stability, and enhances issuer confidence in volatile or clustered market conditions.

1.3.3. The proposed change on the retail portion shall be as follow:

IPO

|

Current

|

PROPOSAL –

|

Retail

|

Retail as

|

Reduction in retail

|

Net QIB Portion (50% of IPO Size + Reduction in retail portion ) |

QIB as a % of

|

1000 |

350 |

35% of IPOsize |

350 |

35% |

500 |

50% |

|

2000 |

700 |

700 |

35% |

1000 |

50% |

||

4000 |

1,400 |

1,400 |

35% |

2000 |

50% |

||

4999 |

1,750 |

1,750 |

35% |

~2500 |

50% |

||

5000 |

1,750 |

1,750 |

35% |

2500 |

50% |

||

5001 |

1,750 |

35% of 5000

|

1,750 |

35% |

2500 |

50% |

|

6000 |

2,100 |

1,850 |

31% |

250 |

3250 |

54% |

|

7000 |

2,450 |

1,950 |

28% |

500 |

4000 |

57% |

|

8000 |

2,800 |

2,050 |

26% |

750 |

4750 |

59% |

Proposal 6:

1.3.4. Further, It is proposed to enhance reservations for MFs from the existing 5 % to 15% in the Non-Anchor QIB category.

1.3.5. Despite market fluctuations, Retail investors have continued to invest in the capital markets through MFs. While direct participation by Retail investors has remained flat over the last 3 years, their participation through MFs has seen a secular uptick. Thus, the lower allocation to the Retail portion would be compensated by the higher reservation for domestic MFs in the QIB portion as illustrated below at para 1.3.6.

Comparison between Existing and Proposed Scenario:

| Investor category |

IPOs under ICDR Regulation 6(1)* |

Proposed Scenario under Regulation 6(1) |

Allocation |

| d) Retail individual investors (Bid of upto Rs. 2 lac) | Not less than 35% | If Net offer < 5000 crore: Not

less than 35 % to RIIs If Net Offer > ₹5,000 crore:

|

Proportionate subject to minimum bid lot ^ |

| e) Non-Institutional (NII) | |||

| Non- Institutional 1 (Bid Rs. 2 – 10 lacs) | Not less than 5% | Not more than 5% | Proportionate subject to minimum bid lot^ |

| Non- Institutional (Bid > Rs. 10 lacs) | Not less than 10% | Not more than 10% | Proportionate subject to minimum bid lot^ |

| c) QIBs | Not more than 50% | Not more than 60% | |

| Anchor portion |

60% of the QIB portion, with 33% reservation to | 60% of the QIB portion, with ^^40% reservation to MFs/ICs/PFs, subject to | Discretionary |

| mutual funds (MFs), subject to demand, with allocation on a discretionary basis | demand, with allocation on a discretionary basis | ||

| Main Book | 40% of the QIB | 40% of the QIB portion, of which | Proportionate |

| QIB (Non- Anchor) | portion, of which atleast 5% allocated to MFs | atleast 15% allocated to MFs | |

| *Unsubscribed portion in Retail and NII portions may be allocated to applicants in any other portion. | |||

| ^ Minimum bid lot: Rs. 12,000 – 15,000 in the Retail portion and >Rs. 2 lac In the NII portion. | |||

| ^^ Out of 40%, 33% shall be reserved solely for MFs and 7% for Pension Funds & Life Insurance | |||

| Companies | |||

| Note 1: Reservation for MFs in the QIB category is subject to demand. | |||

| Note 2: The percentages mentioned in (a), (b) and (c) above are allocations in the net offer to the public (being | |||

| the total offer to the public excluding any IPO reservations). | |||

1.3.6. For instance, the proposed structure and its impact in case of large IPOs (assuming the size of IPO is Rs. 8000 crore) is shown as below:

Current and Proposed calculations:

| Current Scenario (Amount in Rs. crore) | Proposed Scenario (Amount in Rs. crore) | |||

| % | Amount | % | Amount | |

| QIB | 50% of IPO size | 4,000 | 59% of IPO Size | 4,750 |

| Anchor | 60% of QIB | 2,400 | 60% of QIB | 2,850 |

| – MF, ICs and PFs Reservation | ~33% of Anchor (this is solely reserved for MFs) |

800 | ~40% of Anchor (33% of anchor portion shall be reserved solely for MFs and 7% for Insurance companies and Pension funds) |

1,140 |

| Non-anchor QIBs | 40% of QIB | ,1600 | 40% of QIB | 1,900 |

| – MF Reservation | 5% of Non-anchor QIB | 80 | 15% of Non-anchor QIB | 285 |

| NII | 15% of IPO size | 1,200 | 15% of IPO Size | 1,200 |

| NIIs – A (>=10 lacs) | 10% of IPO size | 800 | 10% of IPO size | 800 |

| NIIs – B (b/w 2-10 lacs) | 5% of IPO size | 400 | 5% of IPO size | 400 |

| Retail | 35% of IPO size | 2,800 | ~26% of IPO size* | 2,050 |

| Effective Retail participation – direct and through MFs | ~46% of IPO size | 3,680

(800+80+2800) |

~44% of IPO size | 3,475

(1140+285+2050) |

1.4. Amendment to ICDR Regulations:

1.4.1. The proposed amendments to Schedule XIII of ICDR Regulations are placed at Annexure I.

1.5. Public comments:

1.5.1. Public comments / suggestions are invited on the following:

Proposal 1: Whether the revision in the existing issue structure for large IPOs (i.e., those exceeding ₹5,000 crore) under Regulation 6(1) of the SEBI (ICDR) Regulations as proposed above appropriate?

Proposal 2: Whether the increase in the reservation limit for Mutual funds from existing 5% to 15% under the non-anchor QIB category as proposed above is appropriate?

2. Public Comments:

2.1. In order to take into consideration, the views of various stakeholders, public comments are invited on Proposals mentioned in Section I, Section II and Section III at paragraphs 1.3, 1.3 and 1.3 respectively.

2.2. Need to amend provisions of SEBI (ICDR) Regulations as proposed at annexure I in order to resolve the existing challenges as mentioned in Section I, Section II and Section III at paragraphs 1.2, 1.2 and 1.2 respectively.

3. Submission of Public Comments:

3.1. Considering the implications of the aforementioned matters on the market participants, public comments are invited on the above-detailed proposals. The comments/ suggestions should be submitted latest by August 21, 2025, through the following link: https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPub licComments=yes

3.2. In case of any technical issue in submitting your comment through web based public comments form, you may send your comments through e-mail to consultationcfd@sebi.gov.in with the subject “Consultation Paper on Facilitating Ease of Doing Business relating to Anchor Investor Allocation, Long-Term Institutional Participation and Retail Quota in Initial Public Offerings (IPO) under ICDR Regulations 2018”.

***********

Annexure I

1.1. Proposed amendments to ICDR Regulations:

1.1.1. With respect to proposals of section I, following amendments be included to the relevant clause of Schedule XIII of the ICDR Regulations:

| Existing Provision | Proposed Recommendation |

| 2(1) (c) “anchor investor” means a qualified institutional buyer who makes an application for a value of at least ten crore rupees in a public issue on the main board made through the book building process in accordance with these regulations or makes an application for a value of at least two crore rupees for an issue made in accordance with Chapter IX of these regulations;

SCHEDULE XIII – BOOK BUILDING PROCESS (10) Anchor Investors a) An anchor investor shall make an application of a value of at least ten crore rupees in a public issue on the main board made through the book building process or an application for a value of at least two crore rupees in case of a public issue on the SME exchange made in accordance with Chapter IX of these regulations. b) Up to sixty per cent. of the portion available for allocation to qualified institutional buyers shall be available for allocation/allotment (“anchor investor portion”) to the anchor investor(s). c) Allocation to the anchor investors shall be on a discretionary basis, subject to the following: (I) In case of public issue on the main board, through the book building process: (i) maximum of 2 such investors shall be permitted for allocation up to ten crore rupees (ii) minimum of 2 and maximum of 15 such investors shall be permitted for allocation above ten crore rupees and up to two fifty crore rupees, subject to minimum allotment of five crore rupees per such investor; (iii) in case of allocation above two fifty crore rupees; a minimum of 5 such investors and a maximum of 15 such investors for allocation up to two fifty crore rupees and an additional 10 such investors for every additional two fifty crore rupees or part thereof, shall be permitted, subject to a minimum allotment of five crore rupees per such investor.

|

2(1) (c) “anchor investor” means a qualified institutional buyer who makes an application for a value of at least ten crore rupees in a public issue on the main board made through the book building process in accordance with these regulations or makes an application for a value of at least two crore rupees for an issue made in accordance with Chapter IX of these regulations;

SCHEDULE XIII – BOOK BUILDING PROCESS … (10) Anchor Investors a) An anchor investor shall make an application of a value of at least ten crore rupees in a public issue on the main board made through the book building process or an application for a value of at least two crore rupees in case of a public issue on the SME exchange made in accordance with Chapter IX of these regulations. b) Up to sixty per cent. of the portion available for allocation to qualified institutional buyers shall be available for allocation/allotment (“anchor investor portion”) to the anchor investor(s). c) Allocation to the anchor investors shall be on a discretionary basis, subject to the following: (I) In case of public issue on the main board, through the book building process:

ii) minimum of 2 and maximum of 15 such investors shall be permitted for allocation up to two fifty crore rupees, subject to minimum allotment of five crore rupees per such investor; (iii) in case of allocation above two fifty crore rupees; a minimum of 5 such investors and a maximum of 15 such investors for allocation up to two fifty crore rupees and an additional 10 15 such investors for every additional two fifty crore rupees or part thereof, shall be permitted, subject to a minimum allotment of five crore rupees per such investor. |

1.1.2. With respect to proposals of section II, following amendment be included to the clause (10)(d) of Schedule XIII of the ICDR Regulations:

| Existing Provision | Proposed Recommendation |

| (d) One-third of the anchor investor portion shall be reserved for domestic mutual funds. | d) Of the anchor investor portion:

(i) thirty three per cent shall be reserved for domestic mutual funds; and (ii) seven per cent shall be reserved for life insurance companies and pension funds. Provided that the aggregate reservation under sub-clauses (i) and (ii) above shall be forty per cent of the anchor investor portion. Provided further that any under-subscription in reserved category specified in sub-clause (ii) above may be allocated to domestic mutual funds. Provided further that any under-subscription in any of the reserved categories specified in sub-clause (i) or sub-clause (ii) above may be met with oversubscription in the other reserved category. Explanation: For the purpose of this clause – A) “life insurance company” means an entity registered with the Insurance Regulatory and Development Authority of India; (B) “pension fund” means a fund registered with the Pension Fund Regulatory and Development Authority under the Pension Fund Regulatory and Development Authority Act, 2013, having a minimum corpus of twenty five crore rupees. |

1.1.3. With respect to proposals of section III, following amendments be included to the regulation 32 of ICDR Regulations in case of IPO under regulation 6(1).

| Existing Provision | Proposed Recommendation |

| Allocation in the net offer

32. (1) In an issue made through the book building process under sub-regulation (1) of regulation 6 the allocation in the net offer category shall be as follows: (a) not less than thirty five per cent. to retail individual investors (b) not less than fifteen per cent. to noninstitutional investors; (c) not more than fifty per cent. to qualified institutional buyers, five per cent. of which shall be allocated to mutual funds: Provided further that the unsubscribed portion in either of the categories specified in clauses (a) or (b) may be allocated to applicants in any other category: Provided that in addition to five per cent. allocation available in terms of clause (c), mutual funds shall be eligible for allocation under the balance available for qualified institutional buyers. |

Allocation in the net offer

32. (1) In an issue made through the book building process under sub-regulation (1) of regulation 6 the allocation in the net offer category shall be as follows: (a) not less than thirty five per cent. to retail individual investors (b) not less than fifteen per cent. to noninstitutional investors; (c) not more than fifty per cent. to qualified institutional buyers, fifteen per cent. of which shall be allocated to mutual funds: Provided that, where the size of the net offer exceeds five thousand crore rupees, allocation to retail individual investors shall be: (i) not less than thirty-five per cent of the portion of the net offer up to five thousand crore rupees; and (ii) then, not less than ten per cent of the portion of the net offer that exceeds five thousand crore rupees: Provided further that, in all cases in this proviso, the total allocation to retail individual investors shall not be less than twenty-five per cent of the net offer: Provided further that, if the total allocation to retail individual investors based on the first proviso above is less than thirty-five per cent of the net offer, which shall be added to the portion available for allocation under clause (c) above: Provided further that, any unsubscribed portion in either of the categories specified in clause (a) or clause (b) may be allocated to applicants in any other category, subject to compliance with applicable regulations: Provided further that, in addition to the allocation of fifteen per cent specified under clause (c), mutual funds shall also be eligible for allocation under the remaining portion available to the qualified institutional buyers. |