Reserve Bank of India

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (October 9, 2020) decided to:

♦ keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

♦ The MPC also decided to continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. Incoming data point to a recovery in global economic activity in Q3 of 2020 in sequential terms, although downside risks have risen with the renewed surge in infections in many countries. Global trade is expected to be subdued. The rebound could turn out to be stronger among advanced economies (AEs) than in emerging market economies (EMEs). Global financial markets remain supported by highly accommodative monetary and liquidity conditions. Soft fuel prices and weak aggregate demand have kept inflation below target in AEs, although in some EMEs, supply disruptions have imparted upward price pressures.

Domestic Economy

3. On the domestic front, high frequency indicators suggest that economic activity is stabilising in Q2:2020-21 after the 23.9 per cent year-on-year (y-o-y) decline in real GDP in Q1 (April-June). Cushioned by government spending and rural demand, manufacturing – especially consumer non-durables – and some categories of services, such as passenger vehicles and railway freight, have gradually recovered in Q2. The outlook for agriculture is robust. With merchandise exports slowly catching up to pre-COVID levels and some moderation in the pace of contraction of imports, the trade deficit widened marginally sequentially in Q2.

4. Headline CPI inflation increased to 6.7 per cent during July-August 2020 as pressures accentuated across food, fuel and core constituents on account of supply disruptions, higher margins and taxes. One year ahead inflation expectations of households suggest some softening in inflation from three months ahead levels. Selling prices of firms remain muted, reflecting the weak demand conditions.

5. Domestic financial conditions have eased substantially, with systemic liquidity remaining in large surplus. Reserve money increased by 13.5 per cent on a year-on-year basis (as on October 2, 2020), driven by a surge in currency demand (21.5 per cent). Growth in money supply (M3), however, was contained at 12.2 per cent as on September 25, 2020. Banks’ non-food credit growth remains subdued. India’s foreign exchange reserves stood at US$ 545.6 billion on October 2, 2020.

Outlook

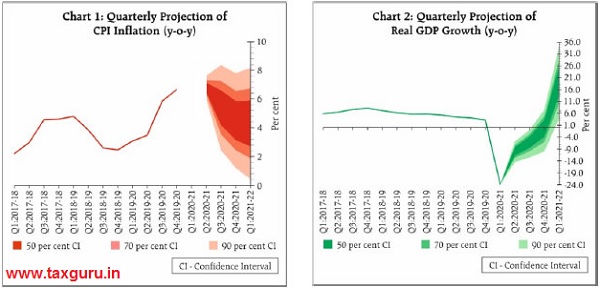

6. Turning to the outlook for inflation, kharif sowing portends well for food prices. Pressures on prices of key vegetables like tomatoes, onions and potatoes should also ebb by Q3 with kharif arrivals. On the other hand, prices of pulses and oilseeds are likely to remain firm due to elevated import duties. International crude oil prices have traded with a softening bias in September on a weak demand outlook, but domestic pump prices may remain elevated in the absence of any roll back of taxes. Pricing power of firms remains weak in the face of subdued demand. COVID-19-related supply disruptions, including labour shortages and high transportation costs, could continue to impose cost-push pressures, but these risks are getting mitigated by progressive easing of lockdowns and removal of restrictions on inter-state movements. Taking into consideration all these factors, CPI inflation is projected at 6.8 per cent for Q2:2020-21, at 5.4-4.5 per cent for H2:2020-21 and 4.3 per cent for Q1:2021-22, with risks broadly balanced (Chart 1).

7. Turning to the growth outlook, the recovery in the rural economy is expected to strengthen further, while the turnaround in urban demand is likely to be lagged in view of social distancing norms and the elevated number of COVID-19 infections. While the contact-intensive services sector will take time to regain pre-COVID levels, manufacturing firms expect capacity utilisation to recover in Q3:2020-21 and activity to gain some traction from Q4 onwards. Both private investment and exports are likely to be subdued, especially as external demand is still anaemic. Taking into consideration the above factors and the uncertain COVID-19 trajectory, real GDP growth in 2020-21 is expected to be negative at (-)9.5 per cent, with risks tilted to the downside: (-)9.8 per cent in Q2:2020-21; (-)5.6 per cent in Q3; and 0.5 per cent in Q4. Real GDP growth for Q1:2021-22 is placed at 20.6 per cent (Chart 2).

8. The MPC is of the view that revival of the economy from an unprecedented COVID-19 pandemic assumes the highest priority in the conduct of monetary policy. While inflation has been above the tolerance band for several months, the MPC judges that the underlying factors are essentially supply shocks which should dissipate over the ensuing months as the economy unlocks, supply chains are restored, and activity normalises. Accordingly, they can be looked through at this juncture while setting the stance of monetary policy. Taking into account all these factors, the MPC decides to maintain status quo on the policy rate in this meeting and await the easing of inflationary pressures to use the space available for supporting growth further.

9. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted for keeping the policy repo rate unchanged and continue with the accommodative stance as long as necessary to revive growth on a durable basis and mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to continue with this accommodative stance at least during the current financial year and into the next financial year, with Prof. Jayanth R. Varma voting against this formulation.

10. The minutes of the MPC’s meeting will be published by October 23, 2020.

(Yogesh Dayal)

Chief General Manager

Press Release: 2020-2021/453

Statement on Developmental and Regulatory Policies

Even as the threat of COVID-19 is yet to abate, with the gradual lifting of restrictions on movement of people and opening of business establishments across the country, a resumption of economic activities is well underway. The role of the financial sector during this phase of recovery will continue to remain important in facilitating businesses to reach the pre-COVID levels of economic activity. The focus of the Reserve Bank’s regulatory actions over the past few months was to first, provide an immediate relief to the borrowers from the impact of COVID-19, through extension of moratorium and other measures, and then to facilitate resolutions through the Resolution Framework for COVID-19 related Stress. Concomitantly, the lending institutions will need to start focusing on revival of activity and their core activity of lending. Accordingly, the measures are intended to (i) enhance liquidity support for financial markets so as to revive activity in targeted sectors of the economy with linkages to other sectors; (ii) provide a boost to exports; (iii) regulatory support to improve the flow of credit to specific sectors within the ambit of the norms for credit discipline; (iv) deepen financial inclusion; and (v) facilitate ease of doing business by upgrading payment system services so as to improve customer satisfaction, while supporting growth.

I. Liquidity Measures and Financial Markets

1. On Tap TLTRO

The focus of liquidity measures by the RBI will now include revival of activity in specific sectors that have both backward and forward linkages, and multiplier effects on growth. Accordingly, it has been decided to conduct on tap TLTRO with tenors of up to three years for a total amount of up to ₹1,00,000 crore at a floating rate linked to the policy repo rate. The scheme will be available up to March 31, 2021 with flexibility with regard to enhancement of the amount and period after a review of the response to the scheme. Liquidity availed by banks under the scheme has to be deployed in corporate bonds, commercial papers, and non-convertible debentures issued by the entities in specific sectors over and above the outstanding level of their investments in such instruments as on September 30, 2020. The liquidity availed under the scheme can also be used to extend bank loans and advances to these sectors. Investments made by banks under this facility will be classified as held to maturity (HTM) even in excess of 25 percent of total investment permitted to be included in the HTM portfolio. All exposures under this facility will also be exempted from reckoning under the large exposure framework (LEF). Moreover, banks that had availed of funds earlier under targeted long-term repo operations (TLTRO and TLTRO 2.0) will be given the option of reversing these transactions before maturity. In view of the borrowing requirements of the centre and states in the second half of 2020-21 and the likely pick-up in demand for credit as the recovery gathers strength, on tap TLTROs are intended to enable banks to conduct their operations smoothly and seamlessly without being hindered by illiquidity frictions. The objective is to ensure that liquidity in the system remains comfortable. The details of the scheme would be announced separately.

2. SLR Holdings in Held to Maturity (HTM) category

To engender orderly market conditions and ensure congenial financing costs, the Reserve Bank on September 1, 2020, increased the limits under Held to Maturity (HTM) category from 19.5 per cent to 22 percent of NDTL, in respect of SLR securities acquired on or after September 1, 2020, up to March 31, 2021. To give more certainty to the markets about the status of these investments in SLR securities after March 31, 2021, it has been decided to extend the dispensation of enhanced HTM limits of 22 percent up to March 31, 2022 for securities acquired between September 1, 2020 and March 31, 2021. The HTM limits would be restored from 22 per cent to 19.5 percent in a phased manner starting from the quarter ending June 30, 2022. It is expected that banks will be able to plan their investments in SLR securities in an optimal manner with a clear glide path for restoration of HTM limits.

3. Open Market operations (OMOs) in State Developments Loans (SDLs).

At present, SDLs are eligible collateral for Liquidity Adjustment Facility (LAF) along with T-bills, dated government securities and oil bonds. To improve liquidity and facilitate efficient pricing, it has been decided to conduct open market operations (OMOs) in SDLs as a special case during the current financial year. The OMOs would be conducted for a basket of SDLs comprising securities issued by states.

II. Support to Exports

4. Automatic Caution Listing of Exporters – Review

As part of automation of Export Data Processing and Monitoring System (EDPMS), the ‘Caution / De-caution Listing’ of exporters was automated in 2016. Accordingly, the exporters were to be caution-listed automatically, if any shipping bill against them remained outstanding for more than 2 years in EDPMS and no extension was granted for realisation of export proceeds against the outstanding shipping bill. Additionally, the normal system of caution-listing based on the recommendations of the Authorised Dealer (AD) bank before the expiry of 2 years in certain cases continued. In order to make the system more exporter friendly and equitable, it has been decided to discontinue the Automatic Caution-listing. The Reserve Bank will continue with caution-listing based on the case-specific recommendations of the AD bank. Related instructions in this regard will be issued shortly.

III. Regulatory Measures

5. Regulatory Retail Portfolio – Revised Limit for Risk Weight

As per the present RBI instructions, the exposures included in the regulatory retail portfolio of banks are assigned a risk weight of 75 per cent. For this purpose, the qualifying exposures need to meet certain specified criteria, including low value of individual exposures. In terms of the value of exposures, it has been prescribed that the maximum aggregated retail exposure to one counterparty should not exceed the absolute threshold limit of ₹5 crore. In order to reduce the cost of credit for this segment consisting of individuals and small businesses (i.e. with turnover of upto ₹50 crore), and in harmonisation with the Basel guidelines, it has been decided to increase this threshold to ₹7.5 crore in respect of all fresh as well as incremental qualifying exposures. This measure is expected to increase the much needed credit flow to the small business segment.

6. Individual Housing Loans – Rationalisation of Risk Weights

In terms of the extant regulations on capital charge for credit risk of individual housing loans by banks, differential risk weights are applicable based on the size of the loan as well as the loan to value ratio (LTV). Recognising the criticality of real estate sector in the economic recovery, given its role in employment generation and the interlinkages with other industries, it has been decided, as a countercyclical measure, to rationalise the risk weights by linking them only with LTV ratios for all new housing loans sanctioned up to March 31, 2022. Such loans shall attract a risk weight of 35 per cent where LTV is less than or equal to 80 per cent, and a risk weight of 50 per cent where LTV is more than 80 per cent but less than or equal to 90 percent. This measure is expected to give a fillip to bank lending to the real estate sector.

IV. Financial Inclusion

7. Review of the Co-origination Model

The Reserve Bank had, in 2018, put in place a framework for co-origination of loans by banks and a category of Non Banking Financial Companies (NBFCs) for lending to the priority sector subject to certain conditions. The arrangement entailed joint contribution of credit at the facility level, by both the lenders as also sharing of risks and rewards between them for ensuring appropriate alignment of respective business objectives. Based on the feedback received from the stakeholders, to better leverage the respective comparative advantages of the banks and NBFCs in a collaborative effort, and to improve the flow of credit to the unserved and underserved sector of the economy, it has been decided to extend the scheme to all the NBFCs (including HFCs), to make all priority sector loans eligible for the scheme and give greater operational flexibility to the lending institutions, while requiring them to conform to the regulatory guidelines on outsourcing, KYC, etc. The proposed framework will be called as “Co-Lending Model”. The revised guidelines will be issued by end of October 2020.

V. Payment and Settlement Systems

8. Round-the-Clock availability of Real Time Gross Settlement System (RTGS)

In December 2019, the National Electronic Funds Transfer (NEFT) system was made available on a 24x7x365 basis and the system has been operating smoothly since then. The large-value RTGS system is currently available for customers from 7.00 am to 6.00 pm on all working days of a week (except 2nd and 4th Saturdays of the month). To support the ongoing efforts aimed at global integration of Indian financial markets, facilitate India’s efforts to develop international financial centers and to provide wider payment flexibility to domestic corporates and institutions, it has been decided to make available the RTGS system round the clock on all days. With this, India will be one of the very few countries globally with a 24x7x365 large value real time payment system. This facility will be made effective from December 2020.

9. Perpetual Validity for Certificate of Authorisation (CoA) issued to Payment System Operators (PSOs)

Currently, the Reserve Bank issues “on-tap’ authorisation under the Payment and Settlement Systems Act, 2007 to non-banks issuing Prepaid Payment Instruments (PPIs), operating White Label ATMs (WLAs) or the Trade Receivables Discounting Systems (TReDS), or participating as Bharat Bill Payment Operating Units (BBPOUs). Authorisation (including renewal of authorisation) of such PSOs has been largely for specified periods up to five years. While such limited period licences were necessitated in the initial period of evolution of the payment system, it can lead to business uncertainty for the PSOs and involves avoidable use of regulatory resources in the process of renewal. Furthermore, the Reserve Bank’s oversight framework has gradually developed into a more mature and comprehensive system, which clearly lays out its oversight expectations and the methodologies adopted for oversight of PSOs. To reduce licensing uncertainties and enable PSOs to focus on their business and optimise utilisation of scarce regulatory resources, it has been decided to grant authorisation for all PSOs (both new applicants as well as existing PSOs) on a perpetual basis, subject to certain conditions. Detailed instructions will be issued separately.

(Yogesh Dayal)

Chief General Manager

Press Release: 2020-2021/454

Source :-

https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=50480

https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=50479