Reserve Bank of India (RBI) on October 1, 2025, kept the repo rate unchanged at 5.5%, maintaining a neutral stance, while unveiling a wide set of regulatory, forex, and consumer protection measures aimed at strengthening financial stability and supporting growth.

MPC Keeps Repo Rate Steady

The Monetary Policy Committee (MPC) voted unanimously to hold the repo rate, citing a sharp fall in inflation to 2.6% for FY 2025-26, aided by food price correction and GST rationalisation. GDP growth for the year was projected at 6.8%, supported by rural demand and reform momentum, though external trade headwinds remain.

RBI Governor Shaktikanta Das said the central bank is adopting a wait-and-watch approach, balancing inflation control with growth needs. “Price stability is our priority, but financial sector resilience and credit support remain equally important,” he noted.

Regulatory and Developmental Measures

Alongside the policy stance, the RBI announced several measures:

-

Introduction of an Expected Credit Loss (ECL) provisioning framework to enhance risk recognition.

-

Risk-based deposit insurance premiums to strengthen the safety net for depositors.

-

Liberalised rules for capital market exposures by banks and NBFCs.

-

Revised ECB and FEMA guidelines to simplify overseas borrowing and trade.

-

Draft guidelines for urban co-operative bank licensing.

Forex and Market Reforms

-

Longer timelines for exporters’ forex accounts.

-

Relaxed rules for merchanting trade and small exporters/importers.

-

Broader SRVA (Special Rupee Vostro Account) investment options to promote INR use in global trade.

-

Expanded set of forex reference rates to aid market transparency.

Consumer Protection Enhancements

-

Review of Basic Savings Bank Deposit (BSBD) accounts to improve accessibility.

-

Strengthened role of Internal Ombudsman and extension of the RBI Ombudsman Scheme to rural cooperative banks.

Outlook

With inflation under control, comfortable liquidity, and banking sector resilience, the RBI signalled room for calibrated reforms. However, it highlighted risks from global trade disruptions and geopolitical uncertainty.

Key Takeaway: RBI’s October 2025 policy signals a pause on rates while pushing ahead with structural reforms in regulation, forex, and consumer protection — with a long-term goal of internationalising the rupee and fortifying India’s financial system.

Reserve Bank of India

Statement on Developmental and Regulatory Policies

Date : Oct 01, 2025

This Statement sets out various developmental and regulatory policy measures relating to (i) Regulations; (ii) Foreign Exchange Management; (iii) Consumer Protection and (iv) Financial Markets.

I. Regulations

1. Expected Credit Loss (ECL) framework for provisioning

With a view to strengthen the resilience of the banking sector, it is proposed to issue the draft Reserve Bank (Asset Classification, Provisioning and Income Recognition) Directions, 2025 for Scheduled Commercial Banks (excluding Small Finance Banks, Payments Banks and Regional Rural Banks) and All India Financial Institutions. The draft directions inter alia, propose to replace the extant framework based on incurred loss with an Expected Credit Loss (ECL) approach, subject to a prudential floor, while retaining the existing asset classification norms. The guidelines are expected to enhance credit risk management practices, promote better comparability of reported financials across institutions. The framework is designed to be implemented in a non-disruptive manner with a suitable glide-path.

2. Basel III Guidelines on Capital Charge for Credit Risk – Standardised Approach

As a part of the broader objective of improving the resilience of the banking sector and aligning the regulatory framework with the best international practices, it is proposed to issue the draft guidelines on implementation of the revised Basel framework on Standardised Approach for Credit Risk for Scheduled Commercial Banks (excluding Small Finance Banks, Payments Banks, and Regional Rural Banks).The revised framework aims to improve the robustness, granularity and risk sensitivity of the standardized approach for calculating the capital charge for credit risk. The draft guidelines shall be issued shortly.

3. Forms of Business and Prudential Regulation for Investments

The draft guidelines on forms of business and investment for banks which was issued in October 2024 has been finalised and shall be issued shortly. Based on feedback and review, the proposed bar on overlap in the businesses undertaken by a bank and its group entity is being removed. The circular envisages to streamline the activities being undertaken by banks and their group entities while providing more operational freedom to the banks and NOFHCs for equity investments and setting up group entities respectively.

4. Introduction of Risk Based Premium Framework for Deposit Insurance in India

Deposit Insurance and Credit Guarantee Corporation (DICGC), under the DICGC Act, 1961 has been operating the deposit insurance scheme since 1962 on a flat rate premium basis. At present, the banks are charged a premium of 12 paise per ₹100 of assessable deposits. While the existing system is simple to understand and administer, it does not differentiate between banks based on their soundness. It is, therefore, proposed to introduce a Risk Based Premium model which will help banks that are more sound to save significantly on the premium paid. Detailed notification will be issued shortly, which will be effective from the next financial year.

5. Review of Capital Market Exposures Guidelines for banks

Capital market exposures (CME) of the regulated entities (REs) which include, inter alia, lending against securities to individuals and lending to capital market intermediaries, have been subject to prudential regulations relating to sectoral exposure limits, single borrower limits, margin requirements, etc. Further, bank finance for acquisition of shares has been generally disallowed.

There has been significant growth and development in the capital market structure, along with strengthening of the banking system in recent years. With the objective of rationalising the extant guidelines and broadening the scope for capital market lending by banks and other regulated entities, it is proposed to inter alia:

- provide an enabling framework for banks to finance acquisitions by Indian corporates;

- enhance the limit for lending by banks against shares, units of REITs, units of InvITs while removing the regulatory ceiling altogether on lending against listed debt securities; and

- put in place a more principle-based framework for lending to capital market intermediaries.

The draft guidelines shall be issued shortly.

- Guidelines on Enhancing Credit Supply for Large Borrowers through Market Mechanism – Withdrawal

The Guidelines on Enhancing Credit Supply for Large Borrowers through Market Mechanism were introduced in August 2016 with an objective to address the concentration risk arising from the aggregate credit exposure of the banking system to a single large corporate and encourage such large corporates to diversify their sources of funding. Upon review, considering, inter-alia, the changes evident in the profile of bank funding to corporate sector since the introduction of the Guidelines, it is proposed to withdraw the guidelines. While the Large Exposures Framework since put in place for banks addresses concentration risk at an individual bank-level, concentration risk at the banking system level, as and when considered as a risk, will be managed through specific macroprudential tools. The draft circular to withdraw these guidelines shall be issued shortly for public comments.

7. Risk Weights on infrastructure lending by NBFCs

Infrastructure projects that have commenced operations typically exhibit lower risk compared to those under construction. Recognizing this risk differential, the existing capital adequacy norms permit NBFCs to assign a lower risk weight to operational projects under Public-Private Partnerships (PPPs). With a view to further rationalise the risk weights for infrastructure lending by NBFCs in line with the nuanced risk-profile of operational projects, it has been decided to introduce a principle-based framework. The framework aims to align risk weights with the actual risk characteristics of operational infrastructure projects, promoting better risk assessment and capital allocation. Draft regulations in this regard shall be issued shortly for public consultation.

8. Discussion Paper on Licensing Framework for new Urban Co-operative Banks (UCBs)

Since 2004, issuance of fresh license for UCBs had been paused following weak financial health of the UCB Sector. Considering that more than two decades have passed since then and the positive developments in the sector, a discussion paper on licensing of new Urban Co-operative Banks (UCBs) will be issued shortly.

9. Consolidation of Regulatory Instructions

The evolution of regulatory framework administered by the Reserve Bank has resulted in proliferation of several circulars and directions. In order to provide ease of access and reduce the compliance cost faced by the regulated entities, the Reserve Bank has undertaken an exercise of consolidating the regulatory instructions administered by the Department of Regulation of the Reserve Bank into a set of Master Directions on an ‘as is’ basis The drafts of about 250 Master Directions consolidating extant instructions on up to 30 areas for 11 types of regulated entities shall be placed on the website shortly for comments on their completeness and accuracy.

10. Review of Restrictions on Transaction Accounts

With the objective of enforcing credit discipline among borrowers as well as to facilitate better monitoring by lenders, certain restrictions were placed on the operation of Current Accounts (CA), Cash Credit Accounts (CC) and Overdraft Accounts (OD) (“Transaction Accounts”) offered by banks vide various circulars issued from time to time. Based on the experience gained and feedback received, these instructions have been reviewed and it is proposed to ease some of the stipulations and provide greater flexibility to the banks in this regard, particularly in case of borrowers being entities regulated by a financial sector regulator. The draft guidelines shall be issued shortly.

II. Foreign Exchange Management

11. Foreign Currency accounts by Indian exporters- extension of time period for repatriation from accounts held in IFSC in India

In January 2025, RBI had permitted Indian exporters to open foreign currency accounts with a bank outside India for realisation of export proceeds. Funds in these accounts can be used for making import payment or have to be repatriated by the end of next month from the date of receipt of the funds. It has now been decided to extend the time period for repatriation, from one month to three months, in case of such foreign currency accounts maintained in IFSC in India. This will encourage Indian exporters to open accounts with IFSC Banking Units and also increase forex liquidity in IFSC. The amendments to regulations will be notified shortly.

12. Merchanting Trade Transactions (MTT)

Global uncertainties in trade are resulting in supply chain disruptions, making it challenging for Indian merchants to meet their contractual obligations in time. In terms of extant guidelines on MTT, outlay of foreign exchange is allowed upto four months. It has now been decided to increase the period for the forex outlay from four months to six months, in case of MTT. This relaxation is expected to help Indian merchants overcome the challenges they face in completing their business transactions efficiently while maintaining profitability. The amendments to regulations will be notified shortly.

13. Relaxation in compliance requirements for Small Value Exporters/Importers

With a view to ease compliance for exporters/importers, especially of small value goods and services, it has been decided to simplify the process of reconciliation in Export Data Processing and Monitoring System (EDPMS) and Import Data Processing and Monitoring System (IDPMS).

As per the revised guidelines, bills can be reconciled and closed by an AD bank in EDPMS or IDPMS, based on a declaration by the concerned exporter or importer, as the case may be, that the amount has been realised, for a shipping bill, or paid against a Bill of Entry, for entries (including outstanding entries) in EDPMS/IDPMS of value equivalent to INR 10 lakh per bill, or less.

The revised procedure will also enable reduction in the realisable value of bills by AD banks based on such declaration. This measure is expected to reduce compliance burden on small value exporters and importers and enhance ease of doing business. The directions will be issued shortly.

14. Review of External Commercial Borrowing Framework

With an objective to rationalise and simplify the regulations governing External Commercial Borrowings (ECB), the Reserve Bank of India has undertaken a review of the existing provisions under the Foreign Exchange Management (Borrowing and Lending) Regulations, 2018.

Based on the review, a revised framework that provides for expansion of eligible borrower and recognized lender base, rationalization of borrowing limits, rationalization of restrictions on average maturity period, removal of restrictions on the cost of borrowing for ECBs, review of end-use restrictions and simplification of reporting requirements, is proposed to be introduced. The draft Framework will be issued shortly.

15. Rationalisation of regulations for Establishment in India of a Branch Office or a Liaison Office or a Project Office or any other place of business

The extant regulations for “Establishment in India of a Branch Office or a Liaison Office or a Project Office or any other place of business” were issued by the Reserve Bank in 2016. The regulations have been comprehensively reviewed. The revised regulations are principle driven and enable delegation of more powers to AD banks and reduction of compliance burden, thereby further enhancing the ease of doing business in India. The draft regulations will be issued shortly.

III. Consumer Protection

16. Review of instructions on Basic Savings Bank Deposit (BSBD) Account

BSBD Account is a savings bank account which was introduced with the objective of promoting financial inclusion. The extant instructions on BSBD account require banks to provide certain minimum facilities free of charge, without the requirement of minimum balance, to the holders of such accounts. The ongoing digitalization in the banking sector necessitates a BSBD account that is in sync with the customer’s changing requirements. Therefore, it has been decided to review the extant instructions on BSBD account to provide affordable banking facilities to the public and drive enhanced usage of BSBD accounts to deepen financial inclusion.

17. Measures for strengthening the Internal Ombudsman mechanism in REs

The Reserve Bank has institutionalized the Internal Ombudsman (IO) mechanism in select Regulated Entities (REs) which enables an independent apex level review of complaints that are being rejected by the RE. To further improve upon the efficacy of this mechanism, it is proposed that the IOs be equipped with compensation powers and be allowed access to the complainant, aligning the role of IOs more closely with that of the RBI Ombudsman. Additionally, a two-tiered structure may be introduced within REs for grievance redress prior to escalation to the IO. These measures aim to provide meaningful and timely resolution of customer grievances within the REs, thereby improving service standards and consumer confidence. A draft of the Master Direction, outlining these revisions, is being released shortly for public feedback.

18. Review of the Reserve Bank – Integrated Ombudsman Scheme, 2021

The Reserve Bank – Integrated Ombudsman Scheme (RB-IOS) (the Scheme), 2021 launched on November 12, 2021, provides customers of Regulated Entities (REs) a speedy, cost-effective and expeditious alternate grievance redress mechanism. The REs currently covered under the Scheme include Commercial Banks, Regional Rural Banks, Scheduled Primary (Urban) Co-operative Banks, Non-Scheduled Primary (Urban) Co-operative Banks with deposits size of ₹50 crore and above, select Non-Banking Financial Companies and Credit Information Companies.

To enable the customers of the rural co-operative banks to access the mechanism of RBI Ombudsman, it has been decided to bring State Co-operative Banks and District Central Cooperative Banks, hitherto with NABARD, within the scope of the RBI Ombudsman Scheme. Notification will be issued shortly in this regard.

Moreover, based on the operational experience, stakeholder feedback, and global best practices, the Reserve Bank has undertaken a comprehensive review of the Scheme. The review seeks to enhance clarity, simplify procedures and reduce timelines to further improve timely, fair, and effective redress. The draft Scheme shall be placed on the Reserve Bank’s website shortly for seeking feedback from stakeholders.

IV. Financial Markets

19. Lending in Indian Rupees (INR) by Authorised Dealer (AD) banks to Persons Resident Outside India

In order to promote the settlement of cross border transactions in INR and local currencies, the Reserve Bank of India has been progressively liberalising regulations under the Foreign Exchange Management Act. To take this initiative further, it is essential that INR liquidity is made available and accessible to residents of other countries. As a calibrated step in this direction, it has been decided that AD banks in India and their overseas branches may be permitted to lend in INR to persons resident in Bhutan, Nepal, and Sri Lanka, including a bank in these jurisdictions, to facilitate cross border trade transactions. The amendments to regulations will be notified shortly.

20. Additional Reference Rates to be published by Financial Benchmarks India Limited

Over the years, the development of forex market has facilitated the growing integration of the Indian economy with the rest of the world in terms of trade and capital flows. At present, Financial Benchmarks India Limited (FBIL) publishes reference rates for USD, EUR, GBP and JPY against INR. These rates are widely used for settlement of forex transactions including derivatives. It is now proposed to include select currencies of India’s major trading partners in the list of reference rates published by FBIL. This is expected to further deepen the onshore forex market and encourage banks to quote directly in a larger set of currency pairs, thus eliminating the need for multiple currency conversions and making trade more efficient. FBIL has been advised to publish the new reference rates in consultation with the market.

21. Expanding the bouquet of investments for Special Rupee Vostro Accounts (SRVA) holders

To promote exports from India and to support increasing interest of global trading community in INR, RBI had permitted Special Rupee Vostro Accounts (SRVA) in July 2022 to facilitate invoicing, payment, and settlement of exports / imports in INR. The arrangement permitted, inter alia, Rupee surplus balances in SRVA to be invested in government securities including treasury bills. To expand investment opportunities in India for SRVA holders, it has now been decided to permit balances of these accounts to be invested in corporate bonds and commercial papers. The revised regulations will be notified shortly.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/1218

***

Reserve Bank of India

Governor’s Statement: October 1, 2025

Namaskar. Greetings on the last day of Navaratri, and my best wishes for a Happy Dussehra and Gandhi Jayanti tomorrow.

2. Since the August policy meeting, significant developments on the domestic front amidst a fast-changing global economic landscape have altered the narrative on growth-inflation dynamics in India. Buoyed by a good monsoon, the Indian economy continues to exhibit strength by registering a higher growth in Q1:2025-26. At the same time, there has been a considerable moderation in headline inflation. The rationalisation of the goods and services tax (GST) rates is likely to have a sobering impact on inflation while stimulating consumption and growth. Tariffs on the other hand will moderate exports.

3. As for the global economy, it has been more resilient than anticipated, with robust growth in the US and China. The outlook, however, remains clouded amidst elevated policy uncertainty. Inflation has remained above respective targets in some advanced economies, posing fresh challenges for central banks as they navigate the shifting growth–inflation dynamics. Financial markets have been volatile. The US dollar strengthened after the upward revision of US growth numbers for the second quarter, and treasury yields hardened recently as expectations of rate cuts by the Federal Reserve ebbed. Equities have remained buoyant across several advanced and emerging economies.

Decisions of the Monetary Policy Committee (MPC)

4. The Monetary Policy Committee (MPC) met on the 29th, 30th of September and 1st October to deliberate and decide on the policy repo rate. After a detailed assessment of the evolving macroeconomic conditions and the outlook, the MPC voted unanimously to keep the policy repo rate unchanged at 5.50 per cent; consequently, the standing deposit facility (SDF) rate remains at 5.25 per cent while the marginal standing facility (MSF) rate and the Bank Rate remain at 5.75 per cent. The MPC also decided to continue with the neutral stance.

5. I shall now briefly set out the rationale for these decisions. The MPC observed that the overall inflation outlook has turned even more benign in the last few months, due to a sharp decline in food prices and the rationalisation of GST rates. The average headline inflation for 2025-26 has been revised lower from 3.7 per cent projected in June and 3.1 per cent in August, to 2.6 per cent. Headline inflation for Q4:2025-26 and Q1:2026-27 too have been revised downwards and are broadly aligned with the target, despite unfavourable base effects. Core inflation for this year and Q1:2026-27 is also expected to remain contained.

6. The MPC also noted that growth outlook remains resilient supported by domestic drivers, despite weak external demand. It is likely to get further support from a favourable monsoon, lower inflation, monetary easing and the salubrious impact of recent GST reforms. However, growth continues to be below our aspirations. Even though the growth projection for the current financial year is being revised upwards, the forward-looking projections for Q3 and beyond are expected to be slightly lower than projected earlier, primarily due to trade related headwinds, despite being partially offset by the impetus provided by the rationalisation of GST rates.

7. Summarising, the MPC concluded that there has been a significant moderation in inflation. Moreover, the prevailing global uncertainties and tariff related developments are likely to decelerate growth in H2:2025-26 and beyond. The current macroeconomic conditions and the outlook has opened up policy space for further supporting growth. However, the MPC noted that the impact of the front-loaded monetary policy actions and the recent fiscal measures is still playing out. The trade related uncertainties are also unfolding. The MPC, therefore, considered it prudent to wait for the impact of policy actions to play out and greater clarity to emerge before charting the next course of action. Accordingly, the MPC unanimously voted to keep the policy repo rate unchanged at 5.5 per cent and decided to retain the stance at neutral.

Assessment of Growth and Inflation

Growth

8. Economic activity has remained resilient with growth of real gross domestic product (GDP) surprising on the upside at 7.8 per cent and gross value added (GVA) at 7.6 per cent for Q1: 2025-26.1As suggested by high frequency indicators available so far, domestic economic activity continues to sustain momentum in Q2:2025-26.2

9. Looking ahead, an above normal monsoon, good progress of kharifsowing and adequate reservoir levels have further brightened prospects of agriculture and rural demand. Buoyancy in services sector coupled with steady employment conditions are supportive of demand, which is expected to get a further boost from the rationalisation of GST. Rising capacity utilisation, conducive financial conditions, and improving domestic demand should continue to facilitate fixed investment. However, ongoing tariff and trade policy uncertainties will impact external demand. Prolonged geopolitical tensions and volatility in international financial markets caused by risk-off sentiments of investors pose downside risks to the growth outlook. The implementation of several growth-inducing structural reforms, including streamlining of GST are expected to offset some of the adverse effects of the external headwinds. Taking all these factors into account, real GDP growth for 2025-26 is now projected at 6.8 per cent, with Q2 at 7.0 per cent, Q3 at 6.4 per cent, and Q4 at 6.2 per cent. Real GDP growth for Q1:2026-27 is projected at 6.4 per cent. The risks are evenly balanced.

Inflation

10. Inflation conditions remained benign during 2025-26 so far with actual outcomes turning out to be significantly lower than projections.3Low inflation is primarily attributed to a sharp fall in food inflation,4aided by improved supply prospects and measures by the government to effectively manage the supply chain.5 Core inflation6 remained largely contained with the August reading at 4.2 per cent, despite continued price pressures on precious metals.7

11. Turning to the inflation outlook, the progress of the southwest monsoon has been satisfactory. Healthy kharif sowing8, adequate reservoir levels9and comfortable buffer stocks of food-grains10should keep food prices benign. The recently implemented GST rate rationalisation would lead to a reduction in prices of several items in the CPI basket. Overall, the inflation outcome is likely to be softer than what was projected in August, primarily on account of the GST rate cuts and benign food prices. Considering all these factors, CPI inflation for 2025-26 is now projected at 2.6 per cent with Q2 at 1.8 per cent; Q3 at 1.8 per cent; and Q4 at 4.0 per cent. CPI inflation for Q1:2026-27 is projected at 4.5 per cent The risks are evenly balanced.

External Sector

12. India’s current account deficit moderated to US$ 2.4 billion (0.2 per cent of GDP) in Q1:2025-26 as compared with US$ 8.6 billion (0.9 per cent of GDP) in Q1:2024-25 due to increased net services surplus and strong remittance receipts despite higher merchandise trade deficit.11During July-August 2025, merchandise trade deficit continued to remain elevated. Notwithstanding rising global trade uncertainties, India’s services exports, driven by software and business services, witnessed robust growth in July-August 2025.12Furthermore, robust services exports coupled with strong remittance receipts is expected to keep the current account deficit (CAD) sustainable during 2025-26.

13. On the external financing side, net foreign direct investment reached a 38-month high in July 2025, driven by increased gross foreign direct investment and a moderation in repatriation and outward foreign direct investment.13However, net FPI recorded outflows of US$ 3.9 billion in 2025-26 so far (April 01-September 29) due to outflows in both equity and debt segments.14As on September 26, 2025, India’s foreign exchange reserves stood at US$ 700.2 billion, sufficient to cover more than 11 months of merchandise imports.15 Overall, India’s external sector continues to be resilient, and we remain confident of meeting our external obligations comfortably.16

14. Notwithstanding the robust domestic macroeconomic fundamentals, the INR has witnessed some depreciation accompanied by phases of volatility. RBI is keeping a close watch on movements of the INR and will take appropriate steps, as warranted.

Liquidity and Financial Market Conditions

15. System liquidity, as measured by the net position under the Liquidity Adjustment Facility (LAF), stood at an average daily surplus of ₹2.1 lakh crore since the last MPC meeting in August 2025.17Going ahead, the drawdown of government cash balances and the remaining 75 basis points cut in the cash reserve ratio (CRR) during October-November will aid banking system liquidity in the near-term. Through our two-way operations, we will actively manage liquidity to anchor short-term rates.

16. Money market rates have remained relatively stable amidst comfortable liquidity conditions.18During February-August 2025, in response to the 100-basis points (bps) cut in the policy repo rate, the weighted average lending rate (WALR) of Scheduled Commercial Banks moderated by 58 bps for fresh rupee loans; 71 bps is on account of interest rate effect. The moderation for outstanding rupee loans is to the extent of 55 bps. On the deposit side, the weighted average domestic term deposit rate (WADTDR) on fresh deposits declined by 106 bps, while that on outstanding deposits softened by 22 bps over the same period. Transmission has been broad-based across sectors. Going forward, adequate liquidity in the system and the remaining CRR cuts will further facilitate monetary transmission.

Financial Stability

17. The system-level financial parameters related to capital adequacy, liquidity, asset quality and profitability of the Scheduled Commercial Banks (SCBs) continue to remain healthy.19Similarly, the system-level parameters of NBFCs too are sound, with adequate capital and improved GNPA ratios20.

18. Bank credit growth, despite being lower than last year, continues to be healthy and supportive of real economic activity.21I would like to emphasise here that, as other sources of funding are gradually but steadily increasing their footprint, it is the overall flow of financial resources to the economy that is more pertinent for assessing flow of funds to the productive sectors. The total flow of resources from non-bank sources to the commercial sector increased by ₹2.66 lakh crore in 2025-26 so far, more than offsetting the decline in non-food bank credit by ₹0.48 lakh crore).22

Additional Measures

19. I shall now announce a package of twenty two additional measures aimed at strengthening the resilience and competitiveness of the banking sector, improving the flow of credit, promoting ease of doing business, simplifying foreign exchange management, enhancing consumer satisfaction, and internationalization of Indian Rupee.

Strengthening the resilience and competitiveness of the banking sector

20. There are four measures for strengthening the resilience and competitiveness of the Indian banks.

21. The Expected Credit Loss (ECL) framework of provisioning with prudential floors is proposed to be made applicable to all Scheduled Commercial Banks (excluding Small Finance Banks (SFBs), Payment Banks (PBs), Regional Rural Banks(RRBs)) and All India Financial Institutions (AIFIs) with effect from 1st April 2027.

22. They will be given a glide path (till March 31, 2031) to smoothen the one-time impact of higher provisioning, if any, on their existing books.

23. Further, it is proposed to make the revised Basel III capital adequacy norms effective for commercial banks (excluding SFBs, PBs and RRBs) from 1st April 2027.

24. In furtherance of this, a draft of the Standardised Approach for Credit Risk shall be issued shortly. Under the revised approach, the proposed lower risk weights on certain segments are expected to reduce the overall capital requirements, particularly for MSMEs and residential real estate (including home loans).

25. It may be recalled that capital requirements for operational risk have already been finalised (in 2023) whereas the capital requirements for market risk are under finalisation after receipt of comments from the public.

26. These measures will help align our guidelines with international standards adapted to our national conditions and priorities, and strengthen the capital adequacy framework for banks and AIFIs.

27. A draft circular on Forms of Business and Prudential Regulation for Investments was issued in October, 2024. It has been finalised after public consultations and will be issued shortly. The proposed regulatory restriction on overlap in the businesses undertaken by a bank and its group entity(ies) is being removed from the final guidelines. The strategic allocation of business streams among group entities will be left to the wisdom of Bank Boards.

28. It is further proposed to introduce risk-based deposit insurance premium with the currently applicable flat rate of premium as the ceiling. This will incentivise sound risk management by banks and reduce premium to be paid by better rated banks.

Improving the flow of credit

29. I will announce five measures to improve flow of credit.

30. One, to expand the scope of capital market lending by banks, it is proposed to provide an enabling framework for Indian banks to finance acquisitions by Indian corporates.

31. Two, it is proposed to (a) remove the regulatory ceiling on lending against listed debt securities and (b) enhance limits for lending by banks against shares from Rs. 20 lakh to Rs. 1 crore and for IPO financing from Rs. 10 lakh to Rs. 25 lakh per person.

32. Three, it is proposed to withdraw the framework introduced in 2016 that disincentivized lending by banks to specified borrowers (with credit limit from banking system of Rs.10,000 crore and above).

33. While the Large Exposure Framework since put in place for banks addresses credit concentration risk to a particular entity or group at an individual bank-level, concentration risk at the banking system level, as and when considered necessary, will be managed through specific macroprudential tools.

34. Four, to reduce the cost of infrastructure financing by NBFCs, it is proposed to reduce the risk weights applicable to lending by NBFCs to operational, high quality infrastructure projects.

35. Five, since 2004, licensing for Urban Co-operative Banks (UCBs) had been paused. Considering the positive developments in the sector during the last two decades and in response to the growing demand from the stakeholders, we propose to publish a discussion paper on licensing of new UCBs.

Promoting Ease of Doing Business

36. I now come to measures related to EoDB. We have seven announcements including those related to FEMA.

37. First, a large number of circulars and directions totalling about 9000, have been consolidated, subject wise, across 11 types of regulated entities. Drafts of the same shall be issued shortly for public consultation.

38. Second, it is proposed to provide greater flexibility to banks for opening and maintaining transaction accounts of borrowers (viz. current accounts and CC/OD accounts). This will particularly help borrowers which are regulated by a financial sector regulator. Restrictions with respect to collection accounts are also proposed to be withdrawn.

39. The export sector is a vital part of India’s economy. To further strengthen the sector and enhance ease of doing business, we shall:

- a, extend the time period for repatriation from foreign currency accounts of Indian exporters in IFSC, from one month to three months.

- b, increase the period for forex outlay for Merchanting Trade transactions, from four months to six months; and

- c, simplify the process of reconciliation of outstanding entries related to exports and imports in the respective reporting portals (EDPMS/IDPMS).

Simplifying foreign exchange management

40. Sixth, key provisions relating to eligible borrowers, recognised lenders, limits on borrowing, cost of borrowing, end-use and reporting, etc. in ECB regulations, issued under FEMA, are proposed to be rationalised.

41. Seventh, it is proposed to rationalise FEMA regulations regarding non-residents establishing their business presence in India.

Enhancing consumer satisfaction

42. I shall now state three consumer centric proposals:

43. One, the bouquet of services offered to Basic Savings Bank Deposit account holders without levy of minimum balance charges is proposed to be expanded to, inter alia, include digital banking (mobile/internet banking) services.

44. Two, the Internal Ombudsman mechanism is proposed to be strengthened to make grievance redressal by regulated entities more effective.

45. Three, the RBI Ombudsman Scheme is also being revised for improved grievance redressal and rural cooperative banks are being included under the ambit of the Scheme.

Internationalising Indian Rupee

46. We have been making steady progress in the use of Indian Rupee for international trade. Three measures are proposed in this regard:

- First, permit AD banks to lend in Indian Rupees to non-residents from Bhutan, Nepal and Sri Lanka for cross border trade transactions.

- Second, establish transparent reference rates for currencies of India’s major trading partners to facilitate INR based transactions.

- Third, permit wider use of SRVA balances by making them eligible for investment in corporate bonds and commercial papers.

Concluding Remarks

47. Let me now conclude. Despite an external environment that has deteriorated since the August policy, the Indian economy remains poised to register high growth. The sobering of inflation has given greater leeway for monetary policy to support growth without compromising on the primary mandate of price stability. However, the MPC decided to wait for the cumulative impact of recent policy actions to play out before charting the next course of action.

48. As India strives towards achieving Viksit Bharat by the centenary year of its independence, it would need the coordinated support of fiscal, monetary, regulatory and other public policies to attain its goal. The recent rationalisation of GST rates by the Government is a major step in this direction. Our various policy announcements today will also support the achievement of this goal. In terms of monetary policy actions, we will remain vigilant of the incoming data and stay focussed on our objective of maintaining price stability while supporting growth. In pursuit of this objective, we will be proactive, objective and consistent in our communication while backing it up with credible actions.

Thank you. Namaskar and Jai Hind.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/1217

***

Reserve Bank of India

Monetary Policy Statement, 2025-26 Resolution of the Monetary Policy Committee September 29 to October 1, 2025

Monetary Policy Decisions

The Monetary Policy Committee (MPC) held its 57th meeting from September 29 to October 1, 2025, under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Poonam Gupta and Shri Indranil Bhattacharyya attended the meeting.

2. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.50 per cent; consequently, the standing deposit facility (SDF) rate remains at 5.25 per cent while the marginal standing facility (MSF) rate and the Bank Rate remains at 5.75 per cent. The MPC also decided to continue with the neutral stance.

Growth and Inflation Outlook

3. The global economy has been more resilient than anticipated in 2025, with robust growth in the US and China. The outlook, however, remains clouded amidst elevated policy uncertainty. Inflation has remained above their respective targets in some advanced economies, posing fresh challenges for central banks as they navigate the shifting growth-inflation dynamics. Financial markets have been volatile. The US dollar strengthened after the upward revision of US growth numbers for the second quarter, and treasury yields hardened recently tracking changes in policy rate expectations. Equities have remained buoyant across several advanced and emerging market economies.

4. In India, real gross domestic product (GDP), driven by strong private consumption and fixed investment, recorded a robust growth of 7.8 per cent in Q1:2025-26. On the supply side, growth in gross value added (GVA) at 7.6 per cent was led by a revival in manufacturing and steady expansion in services. Available high frequency indicators suggest that economic activity continues to remain resilient. Rural demand remains strong, riding on a good monsoon and robust agriculture activity, while urban demand is showing a gradual revival. Revenue expenditure of the Union and State Governments registered robust growth during the fiscal year so far (April-July). Investment activity, as suggested by healthy growth in construction indicators i.e., cement production and steel consumption in July-August, is holding up well even though production and import of capital goods witnessed some moderation. Recovery in manufacturing sector continues while services activity is sustaining its momentum.

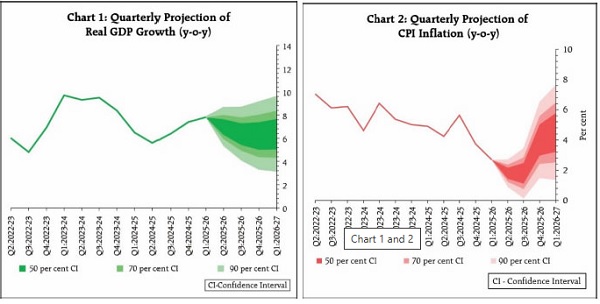

5. Looking ahead, an above normal monsoon, good progress of kharif sowing and adequate reservoir levels have further brightened prospects of agriculture and rural demand. Buoyancy in services sector coupled with steady employment conditions are supportive of demand, which is expected to get a further boost from the rationalisation of goods and services tax (GST) rates. Rising capacity utilisation, conducive financial conditions, and improving domestic demand should continue to facilitate fixed investment. However, ongoing tariff and trade policy uncertainties will impact external demand for goods and services. Prolonged geopolitical tensions and volatility in international financial markets caused by risk-off sentiments of investors also pose downside risks to the growth outlook. The implementation of several growth-inducing structural reforms, including streamlining of GST are expected to offset some of the adverse effects of the external headwinds. Taking all these factors into account, real GDP growth for 2025-26 is now projected at 6.8 per cent, with Q2 at 7.0 per cent, Q3 at 6.4 per cent, and Q4 at 6.2 per cent. Real GDP growth for Q1:2026-27 is projected at 6.4 per cent (Chart 1). The risks are evenly balanced.

6. Headline CPI inflation declined to its eight-year low of 1.6 per cent (y-o-y) in July 2025 before rising to 2.1 per cent in August – its first increase after nine months. Benign inflation conditions during 2025-26 so far have been primarily driven by a sharp decline in food inflation from its peak of October 2024. Inflation within the fuel group moved in a narrow range of 2.4-2.7 per cent during June-August. Core inflation remained largely contained at 4.2 per cent in August. Excluding precious metals, core inflation was at 3.0 per cent in August.

7. In terms of the inflation outlook for H2: 2025-26, healthy progress of the south-west monsoon, higher kharif sowing, adequate reservoir levels and comfortable buffer stock of foodgrains should keep food prices benign. The recently implemented GST rate rationalisation would lead to a reduction in prices of several items in the CPI basket. Overall, the inflation outcome is likely to be softer than what was projected in the August MPC resolution, primarily on account of the GST rate cuts and benign food prices. Despite the anticipation of moderate momentum during H2, large unfavourable base effects are likely to exert upward pressure on headline CPI inflation, especially in Q4. Considering all these factors, CPI inflation for 2025-26 is now projected at 2.6 per cent with Q2 at 1.8 per cent; Q3 at 1.8 per cent; and Q4 at 4.0 per cent. CPI inflation for Q1:2026-27 is projected at 4.5 per cent (Chart 2). The risks are evenly balanced.

Rationale for Monetary Policy Decisions

8. The MPC observed that the overall inflation outlook has turned even more benign in the last few months, due to the reasons discussed above. The average headline inflation for 2025-26 is now revised lower from 3.7 per cent and 3.1 per cent projected in June and August policy, respectively, to 2.6 per cent. Headline inflation for Q4:2025-26 and Q1:2026-27 too have been revised downwards and are broadly aligned with the target, despite unfavourable base effects. Core inflation for this year and Q1:2026-27 is also expected to remain contained.

9. Growth outlook remains resilient supported by domestic drivers, despite weak external demand. It is likely to get further support from a favourable monsoon, lower inflation, monetary easing and the salubrious impact of recent GST reforms. However, growth continues to be below our aspirations. Even though the growth projection for the financial year 2025-26 is being revised upwards, the forward-looking projections for Q3 and beyond are expected to be slightly lower than projected earlier, primarily due to tariff-related developments, despite being partially offset by the impetus provided by the rationalisation of GST rates.

10. To summarize, there has been a significant moderation in inflation. Moreover, the prevailing global uncertainties and tariff related developments are likely to decelerate growth in H2:2025-26 and beyond. The current macroeconomic conditions and the outlook has opened up policy space for further supporting growth. However, the MPC noted that the impact of the front-loaded monetary policy actions and the recent fiscal measures is still playing out. The trade related uncertainties are also unfolding. The MPC, therefore, considered it prudent to wait for the impact of policy actions to play out and greater clarity to emerge before charting the next course of action. Accordingly, the MPC unanimously voted to keep the policy repo rate unchanged at 5.5 per cent. The MPC also decided to retain the stance at neutral. However, two members – Dr. Nagesh Kumar and Prof. Ram Singh, were of the view that the stance be changed from neutral to accommodative.

11. The minutes of the MPC’s meeting will be published on October 15, 2025.

12. The next meeting of the MPC is scheduled during December 3 to 5, 2025.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/1216

Notes:

1 During Q1:2025-26, private final consumption, government consumption, and gross fixed capital formation (GFCF) grew by 7.0 per cent, 7.4 per cent, and 7.8 per cent, respectively. Real GVA of agriculture, manufacturing and services posted a growth of 3.7 per cent, 7.7 per cent and 9.0 per cent, respectively, in Q1.

2 Tractor and two-wheelers sales grew robustly by 17.3 per cent and 7.9 per cent, respectively, during July-August 2025. According to NielsenIQ, FMCG sales volume increased by 8.3 per cent and 4.1 per cent, respectively, in rural and urban areas during July-August 2025. Domestic air passenger traffic contracted by 1.7 per cent during this period. Consumption of finished steel and production of cement increased by 8.7 per cent and 8.8 per cent, respectively in July-August 2025. Domestic production of capital goods expanded at 5.6 per cent in July-August 2025 following a strong growth during Q1:2025-26 at 9.8 per cent, while imports of capital gods expanded by 5.4 per cent during July-August. Manufacturing PMI surged to a 17.5-year high of 59.3 in August, along with strong business optimism. Services PMI reached a 15-year high of 62.9 in August 2025, led by rising new orders.

3 The actual outcomes for Q1 and projection for Q2 of 2025-26 turned out to be lower by 90 bps and 210 bps, respectively, that what was set out in April policy, primarily on account of the faster than expected decline in food inflation. Core inflation largely evolved as projected.

4 Food group registered a deflation of -0.8 per cent in July (lowest since January 2019), before closing with zero inflation in August 2025.

5 Within food group, deflation was observed in prices of vegetables (-15.9 per cent), pulses (-14.5 per cent), and spices (-3.2 per cent) in August. Decline in inflation within cereals sub-group to 2.7 per cent in August 2025 as compared with 7.3 per cent a year ago also contributed to the overall moderation in food inflation.

6 CPI headline excluding food and fuel.

7 Core excluding gold and silver recorded a y-o-y inflation on 3.0 per cent in August 2025.

8 As on September 19, 2025, the area sown under kharif crops stood at 11.2 crore hectares, 2.2 per cent over higher than the normal sowing area for the season.

9 As of September 25, 2025, reservoir levels stood at 90 per cent of total capacity, exceeding the levels recorded a year ago and the decadal average.

10 As on September 16, 2025, the Food Corporation of India’s wheat stocks were 1.2 times the buffer norms (highest in last 4 years) while rice stocks were 3.5 times the buffer norms.

11 In this context, it is pertinent to inform that we have reduced the time lag of releasing the quarterly balance of payments data and press release from 90 days to 60 days.

12 As per provisional figures, India’s services exports grew by 6.5 per cent during July-August 2025, while services imports increased by 1.5 per cent during this period. Net services exports grew by 12.2 per cent during July-August 2025.

13 Gross foreign direct investment (FDI) inflows grew by 33.2 per cent to US$ 37.7 billion in April-July 2025-26 from US$ 28.3 billion during the same period a year ago. Net FDI inflows increased by more than 200 per cent to US$ 10.8 billion in April-July 2025-26 from US$ 3.5 billion a year ago.

14 During April-September 2025 (till September 29), there were net outflows of US$ 3.3 billion and US$ 0.6 billion in equity and debt segments, respectively.

15 Based on actual merchandise imports (on a BoP basis) during the four quarters period (Q2:2024-25 to Q1:2025-26), sufficient to cover around nine months of imports of goods and services combined and around 94 per cent of total external debt as on end-June 2025.

16 India’s CAD/GDP ratio moderated to 0.6 per cent in 2024-25 from 0.7 per cent during 2023-24. India’s external debt to GDP ratio moderated to 18.9 per cent at end-June 2025 from 19.1 per cent at end-March 2025. The net International Investment position to GDP ratio improved to (-) 8.0 per cent from (-) 8.6 per cent during the same period.

17 The average daily net absorption under the liquidity adjustment facility (LAF) during June and July stood at ₹2.8 lakh crore and ₹3.1 lakh crore, respectively. The average daily net absorption under the LAF declined to ₹2.9 lakh crore in August 2025 and ₹1.6 lakh crore in September 2025 (up to 29th).

18 In response to the cumulative policy repo rate cut of 100 basis points (bps) in the current easing cycle (up to September 29), the WACR, the 3-month T-bill rate, the 3-month CP issued by NBFCs, and the 3-month CD rate declined by 92 bps, 105 bps, 118 bps, and 147 bps, respectively.

19 SCB Parameters: The outstanding credit and deposit increased by 10.4 per cent and 11.3 per cent on a y-o-y basis, respectively, between June-24 and June-25. The system-level Capital to Risk Weighted Assets Ratio (CRAR) of 17.54 per cent in June 2025 was well above the regulatory minimum level. Ratio of non-performing loans improved further (GNPA ratio at 2.22 per cent in June 2025 vis-à-vis 2.67 per cent in June 2024, NNPA Ratio at 0.51 per cent in June 2025 vis-à-vis 0.60 per cent in June 2024). Liquidity buffers were robust, with an LCR of 132.69 per cent as of end June 2025. The annualised return on assets (RoA) and return on equity (RoE) stood at 1.30 per cent and 13.02 per cent, respectively, in June 2025. Net Interest Margin was 3.25 per cent for June 2025 (3.54 per cent in June 2024).

20 NBFC Parameters: Total CRAR of NBFCs was 25.69 per cent and Tier I CRAR was 23.78 per cent in June 2025, well above the minimum regulatory requirements. GNPA ratio has improved from 2.54 per cent in June 2024 to 2.23 per cent in June 2025, while NNPA ratio also improved from 1.07 per cent in June 2024 to 0.98 per cent in June 2025. RoA for the sector decreased slightly from 2.66 per cent in June 2024 to 2.64 per cent in June 2025. NIM has slightly decreased from 4.85% in June 2024 to 4.50% in June 2025.

21 Non-food bank credit recorded a year-on-year (y-o-y) growth of 10.2 per cent as on September 5, 2025, compared to 13.3 per cent a year ago.

22 Among the non-bank sources, issuances of corporate bonds by non-financial entities increased by ₹1.66 lakh crore while net inward FDI increased by ₹0.93 lakh crore.