The Reserve Bank of India announced a series of developmental and regulatory measures aimed at improving efficiency, easing compliance, and strengthening financial markets. Key proposals include removing the restriction on including quarterly profits in CRAR calculations linked to NPA provisioning deviations, and dispensing with the Investment Fluctuation Reserve requirement for certain banks to simplify prudential norms. The RBI also plans to rationalize board-level reporting requirements to enhance strategic focus and governance. On supervision, over 9,000 circulars have been consolidated into streamlined Master Directions, with further consolidation of supervisory instructions underway. To promote MSME participation, onboarding on TReDS platforms will be simplified by removing due diligence requirements. Additionally, the term money market will be expanded to include non-bank participants, improving liquidity and transmission. These measures collectively aim to enhance ease of doing business, regulatory clarity, and financial system resilience amid evolving global uncertainties.

Reserve Bank of India

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Regulations; (ii) Supervision; (iii) Payment Systems; and (iv) Financial Markets:

I. Regulations

1. Review of guidelines for inclusion of Quarterly Profits in Capital to Risk-weighted Assets Ratio (CRAR) computation – Commercial Banks

As per the extant guidelines, commercial banks (excluding Regional Rural Banks and Local Area Banks) are permitted to include quarterly net profits in the calculation of CRAR provided that the incremental provisions made for Non-Performing Assets (NPAs) at the end of any of the four quarters of the previous financial year, have not deviated more than 25 per cent of the average of the four quarters. On a review, it is proposed to dispense with this condition. The draft amendment directions in this regard will be issued for public comments shortly.

2. Review of Guidelines on Investment Fluctuation Reserve (IFR)

Banks currently maintain Investment Fluctuation Reserve (IFR) as an additional buffer against depreciation in the value of their investments, subject to mark-to-market (MTM) requirements. Currently, commercial banks (including Local Area Banks, but excluding Small Finance Banks, Payment Banks and Regional Rural Banks) already maintain capital charge for market risk and also follow revised norms on classification, valuation, and operation of investment portfolio. In consideration of these applicable prudential requirements, it is proposed to dispense with the IFR requirement for such commercial banks. The existing guidelines for other bank categories are also being revised to address the operational challenges encountered by such banks in complying with the regulatory thresholds on IFR and to harmonies instructions across bank categories, thereby enhancing regulatory clarity and consistency. Draft directions in this regard will be issued shortly for public consultation.

3. Review of matters placed before the Boards of the Banks

The matters to be placed before the Boards of banks, along with their periodicity, are determined by the Boards themselves, guided by the seven broad themes prescribed by the Reserve Bank of India. Meanwhile, the Reserve Bank has also mandated certain policies and matters to be placed before the Board for approval, review, or information. In an endeavor to enable Boards to utilize its time effectively, and to facilitate a more focused and qualitative engagement on strategy and risk governance, the Reserve Bank has undertaken comprehensive review and rationalization of all such instructions. Draft directions in this regard will be issued shortly for public consultation.

II. Supervision

4. Consolidation of Supervisory Instructions

The Reserve Bank has constantly endeavored to refine and strengthen its regulatory and supervisory framework while minimising compliance costs, through periodic evaluation of instructions for their continued relevance. In furtherance of this objective, Reserve Bank had undertaken a comprehensive consolidation exercise of the regulatory instructions, on an ‘as is’ basis, in 2025. The exercise involved consolidation of more than 9000 existing regulatory circular/ guidelines into 238 function-wise Master Directions (MDs), specific to each category of regulated entity. A similar exercise has now been carried out for the supervisory instructions. Accordingly, the Drafts of 64 consolidated Directions extant supervisory instructions on up to nine functional areas are being published today on RBI website for public comments.

III. Payment Systems

5. Simplifying the onboarding process of MSMEs in Trade Receivables Discounting System (TReDS)

With a view to facilitating timely access to working capital for MSMEs, guidelines for Trade Receivables Discounting System (TReDS) were issued in 2014 and subsequently updated in 2018. The scope of TReDS was further expanded in 2023 with the inclusion of insurance companies as the fourth participant. In order to promote ease of doing business for MSMEs and to encourage their greater participation on TReDS, it is proposed to dispense with the requirement of due diligence of MSMEs while onboarding on TReDS platforms. A comprehensive review of other extant instructions has also been undertaken, and draft directions will be issued shortly for public consultation.

IV. Financial Markets

6. Development of Term Money Market

An active-term money market, apart from providing an alternative funding avenue to the market participants, also helps in enhancing monetary policy transmission by creating a link between the overnight money market and longer-term interest rates. At present, only banks and standalone primary dealers are eligible to participate in the term money market, with certain prudential limits. With a view to further enhance the depth of participation and liquidity in the term money market segment, it has been decided to (a) expand the participant base in the term money market segment to include non-bank participants viz., AIFIs, NBFCs, including housing finance companies, companies, etc.; and (b) enhance the borrowing limit in the term money market for standalone primary dealers. The revised directions are being issued separately.

(Brij Raj)

Chief General Manager

Press Release: 2026-2027/38

Reserve Bank of India

Governor’s Statement: April 08, 2026

Good morning and Namaskar. Let me welcome you all to the first policy of 202627 at a time when the global economy is facing unprecedented challenges from heightened geo-political tensions, the conflict in West Asia and the disruption in global supply chains.

2. Before the outbreak of the conflict, India’s macroeconomic fundamentals exuded confidence with buoyant growth and low inflation. Conditions turned adverse in March with the widening of the conflict zone and its intensification. The fundamentals of the Indian economy are on a stronger footing at the current juncture than in previous crisis episodes as well as relative to many other economies, providing it with greater resilience to withstand shocks.

3. Global growth faces increasing downside risks as the sharp rise in energy prices and shortages of inputs for various industries have stoked inflation fears and pushed up the geopolitical risk premium in oil markets. Heightened uncertainty precipitated by the ongoing conflict is weighing on the outlook. Safe-haven flows have exerted depreciation pressure on currencies of major economies as the US dollar has strengthened. While commodity prices, such as of metal and gold, have moderated, financial markets have become more volatile. Equities registered a broad-based correction. Sovereign bond yields, already elevated due to long-run fiscal sustainability concerns, driven by inflation fears, have hardened across major economies.

Decisions of the Monetary Policy Committee (MPC)

4. The Monetary Policy Committee (MPC) met on the 6th, 7th and 8th of April to deliberate and decide on the policy repo rate. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent; consequently, the standing deposit facility (SDF) rate remains at 5.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 5.50 per cent. The MPC also decided to continue with the neutral stance.

5. I shall now briefly set out the rationale for these decisions.

6. The MPC noted that since the last policy meeting, geopolitical uncertainties have heightened significantly. Headline inflation remains contained and below the target. However, upside risks to the inflation outlook, driven by increased energy price pressures and probable weather disturbances affecting food prices, have increased.

Core inflation pressures remain muted, although supply chain dislocations and the risk of second-round effects render the future inflation trajectory uncertain.

7. The MPC further noted that high frequency indicators till February, 2026 suggest the continuation of strong momentum in economic activity. Growth impulses continue to be supported by robust private consumption and investment demand. However, the West Asia conflict is likely to impede growth. Higher input costs associated with increase in energy prices and international freight and insurance costs along with supply-chain disruptions that would constrain availability of key inputs for downstream sectors, would impair growth. The Government has taken several measures targeted at supporting exports and protecting supply chains. This should mitigate the adverse impact of the conflict.

8. The MPC opined that the intensity and the duration of the conflict and the resultant damage to the energy and other infrastructure add risk to the inflation and growth outlooks. However, the fundamentals of the Indian economy are on a stronger footing, providing it with greater resilience to withstand shocks now than in the past. The economy is confronted with a supply shock. It is prudent to wait and watch the changing circumstances and the evolving growth-inflation outlook. Accordingly, the MPC voted to keep the policy rate unchanged even as it remains vigilant, closely monitoring incoming information and assessing the balance of risks. The MPC also decided to continue with the neutral stance, retaining the flexibility to respond judiciously to incoming information.

Assessment of Growth and Inflation

Impact of the West Asia Conflict on the Indian Economy

9. Before I provide an assessment of growth and inflation, let me briefly elucidate on the channels of transmission through which the Indian economy may get impacted by the ongoing conflict. First, elevated crude oil prices could increase imported inflation and widen the current account deficit. Second, disruptions in energy markets, fertilisers and other commodities may adversely impact industry, agriculture and services, reducing domestic output. Third, heightened uncertainty, increased risk aversion and safe haven demand could impact domestic liquidity conditions, economic activity, consumption and investment. Fourth, weaker global growth prospects may dampen external demand and reduce remittance flows. Finally, adverse spillovers from global financial markets could tighten domestic financial conditions and raise the cost of borrowing. Overall, the initial supply shock can potentially transform into a demand shock over the medium term if the restoration of supply chains is delayed.

Growth

10. As per the new GDP series (base year 2022-23), real GDP growth for 2025-261 is estimated at 7.6 per cent. This corroborates the underlying strong momentum in economic activity, supported by robust consumption and investment2, amidst supportive policy measures, ongoing structural reforms, and favourable financial conditions.

11. Going forward, elevated energy and other commodity prices, as also shocks to availability of inputs due to disruptions in the Strait of Hormuz are likely to impact growth in 2026-27. The Government has, however, been proactive in ensuring supply of inputs across critical sectors to minimise the impact of supply chain disruptions.3 On the other hand, sustained momentum in services sector, persisting impact of GST rationalisation, and healthy balance sheets of financial institutions and corporates should continue to support economic activity. The agricultural sector’s prospects are supported by healthy reservoir levels.4 Business expectations remain optimistic,5 and leading indicators point towards continued resilience in manufacturing and services sectors.6 Moreover, the Government’s focus on scaling up domestic manufacturing in several strategic and frontier sectors augurs well for India’s ensuing growth trajectory.

12. On the demand side, private consumption in 2026–27 is expected to be supported by discretionary spending. Rural demand remains robust.7 It should gain further traction on the back of favourable agricultural conditions and a healthy labour market.8 Urban consumption is likely to strengthen further, aided by the beneficial impact of GST rationalisation and buoyant services sector activity. While the government’s thrust on infrastructure spending continues,9 the revival in private sector investment is expected to sustain on the back of high capacity utilisation,10 strong credit growth11 and benign financial conditions. On the external front, merchandise exports could be adversely impacted from disruptions to key shipping routes, the concomitant rise in freight and insurance costs and lower global demand on account of the conflict. However, merchandise exports may benefit from the recent trade agreements, while services exports12 are expected to remain resilient.

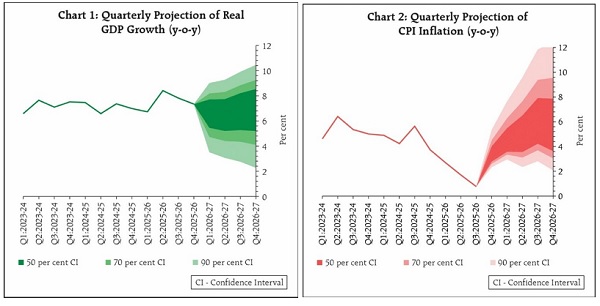

13. Taking all these factors into consideration, real GDP growth for 2026-27 is projected at 6.9 per cent, with Q1 at 6.8 per cent; Q2 at 6.7 per cent; Q3 at 7.0 per cent; and Q4 at 7.2 per cent. Further escalation and wider spread of the conflict, heightened volatility in global financial markets and weather-related events, however, and gross fixed capital formation (GFCF) posted a growth of 7.7 per cent and 7.1 per cent, respectively. Government final consumption expenditure (GFCE) increased by 6.6 per cent over the previous year.

weigh on the domestic growth outlook. Risks to the baseline projections are tilted to the downside, with uncertainty remaining elevated due to the ongoing West Asia conflict.

Inflation

14. In January-February, headline inflation continued to remain below target (2.7 per cent and 3.2 per cent, respectively), with food group recording inflation13 vis a vis a deflation in the previous four months14. Inflation in fuel items15 was modest. Core inflation was at 3.7 per cent16 and the underlying price pressures benign, as evident from the much lower core inflation excluding precious metals at 2.1 per cent.

15. Turning to the inflation outlook, recent spikes in energy prices due to the conflict have emerged as a risk. Although retail prices of petrol and diesel have remained unchanged so far, the pass-through of higher global energy prices has resulted in some price increases in a few other fuel items.17 Food price outlook remains comfortable in the near term with robust rabi production, adequate reservoir levels and comfortable buffer stocks of foodgrains18. The likely emergence of El Niño conditions could pose a risk.19 Considering all these factors, CPI inflation for 2026-27 is projected at 4.6 per cent with Q1 at 4.0 per cent; Q2 at 4.4 per cent; Q3 at 5.2 per cent; and Q4 at 4.7 per cent. Core inflation is projected at 4.4 per cent. Excluding precious metals, core inflation is even lower indicating that underlying inflation pressures are expected to remain contained. The risks are on the upside.

External Sector

16. Global trade is expected to witness a slowdown in growth during 2026 as compared to 2025, due to the lingering tariff related uncertainties, ongoing West Asia conflict and elevated energy prices.20 India’s merchandise exports contracted by 0.2 per cent during January-February 2026 on a year-on-year (y-o-y) basis, impacted by export contraction in key markets21. Merchandise imports recorded a double-digit growth of 22.2 per cent, largely driven by higher gold imports22, resulting in a widening of the trade deficit.23 Expected robustness in services exports24 and inward remittance receipts25 during Q4:2025-26 should keep India’s current account deficit moderate and within the sustainable level in 2025-26. Rising global uncertainties and elevated prices of key energy commodities pose some upside risks to India’s current account deficit in 2026-27. The recent bilateral and regional trade agreements with major trading partners are expected to boost India’s trade and investment opportunities, widen and diversify its trading partners and integrate India into global value chains.26

17. On the external financing front, gross foreign direct investment (FDI) witnessed strong growth, while net FDI showed improvement.27 India remains an attractive destination for greenfield FDI projects.28 Foreign portfolio investment (FPI) to India, driven by outflows in the equity segment, recorded net outflows of US$ 16.5 billion in 2025-26, followed by outflows of US$ 5.4 billion in 2026-27 (till April 6).29 Flows under external commercial borrowings and non-resident deposits moderated as compared to 2024-25.30 As on April 3, 2026, India’s foreign exchange reserves stood at US$ 697.1 billion. These are adequate in terms of the standard metrics of reserve adequacy including import cover (about 11 months) and external debt (91.1 per cent). Overall, India’s external sector indicators remain favourable.31 Nevertheless, elevated global geopolitical, trade and investment uncertainties require continuous vigil of the evolving developments.

18. Despite stronger macroeconomic fundamentals, the Indian rupee in 2025-26 depreciated more than the average in the previous years. In this regard, let me reiterate that our exchange rate policy remains unchanged. Specifically, intervention in the foreign exchange market is aimed at smoothening excessive and disruptive volatility without targeting any specific level or band for the exchange rate. This is consistent with our long-standing policy of the exchange rates being market-determined. The RBI stands committed to this policy and would judiciously contain excessive or disruptive volatility to ensure that self-fulfilling expectations do not exacerbate currency movements beyond what is warranted by fundamentals.

Liquidity and Financial Market Conditions

19. System liquidity, as measured by the net position under the Liquidity Adjustment Facility (LAF), stood at an average daily surplus of ₹2.3 lakh crore since the last MPC meeting.32 Since then, the weighted average call rate (WACR) traded in the lower half of the corridor except towards end-March33. Short term money market rates, especially those of commercial papers and certificates of deposit, remained elevated34. G-Sec yields remained largely rangebound with a softening bias in February but firmed up thereafter on account of the ongoing conflict, hardening global yields and the rise in energy prices35. Transmission in the credit market remained satisfactory.36

20. To ensure sufficient liquidity in the banking system, the Reserve Bank proactively undertook durable and transient liquidity measures37. Going ahead, we will continue to be proactive and pre-emptive in liquidity management and ensure sufficient liquidity in the banking system to meet the productive requirements of the economy.

Financial Stability

21. The system-level financial parameters related to capital adequacy, liquidity, asset quality and profitability of Scheduled Commercial Banks (SCBs) continue to remain healthy.38 Similarly, the system-level parameters of NBFCs too are sound, with adequate capital position and improved GNPA ratios39.

22. As per the latest available data, credit from all sources grew at 14.3 per cent (y-o-y) as compared to 11.7 per cent (y-o-y) a year ago40. Bank credit growth maintained its upward trajectory41, and remained broad-based.

Additional Measures

23. I shall now announce some measures related to Ease of Doing Business, capital adequacy, and market development.

Promoting ease of doing business

24. There are three measures proposed to promote ease of doing business.

25. First, to facilitate better utilisation of Bank Board’s time, after a comprehensive review of all our extant instructions, we propose to revise and rationalize the matters requiring its attention.

26. Second, you would recall that we had recently undertaken a detailed exercise, to consolidate over 9000 regulatory instructions into 238 Master Directions. A similar consolidation exercise has now been completed for all our supervisory instructions.

27. Third, to facilitate ease of doing business by MSMEs, we propose to dispense with the requirement of due diligence while onboarding them on TReDS platforms.

Supporting Capital Adequacy

28. There are two measures regarding capital adequacy of banks.

29. First, it is proposed to remove the condition regarding NPA provisioning for inclusion of quarterly profits in CRAR computation.

30. Second, in view of the developments in prudential framework over the years, it is proposed to dispense with the requirement to maintain an Investment Fluctuation Reserve (IFR) as an additional buffer to hedge against depreciation in the value of investments.

Development of Money Market

31. For further development of the term money market, we have decided to permit certain additional categories of non-bank entities in this market segment. At present, only banks and standalone primary dealers (SPDs) are eligible to participate in this market. We are also enhancing the borrowing limit of SPDs in the term money market.

Concluding Remarks

32. To conclude, global economic conditions and sentiments have soured after the outbreak of the West Asia conflict. These have adversely impacted the growth-inflation outlook. As reiterated before, we shall remain vigilant of the evolving situation and put in place policies that prioritise the best interest of the economy.

33. Thank you. Namaskar and Jai Hind.

(Brij Raj)

Chief General Manager

Press Release: 2026-2027/37

Notes:

1Gross value added (GVA) at basic prices (y-o-y) is estimated to grow by 7.7 per cent. Agriculture and allied activities witnessed a deceleration with growth at 2.4 per cent in 2025-26 while industrial growth improved to 9.5 per cent and services grew by 8.7 per cent.

2 As per the Second Advance Estimates (SAE) released by National Statistics Office (NSO), GDP growth in 2025-26 is estimated at 7.6 per cent, higher than 7.1 per cent in 2024-25 and 7.2 per cent in 2023-24. Private final consumption expenditure (PFCE) and gross fixed capital formation (GFCF) posted a growth of 7.7 per cent and 7.1 per cent, respectively. Government final consumption expenditure (GFCE) increased by 6.6 per cent over the previous year.

3 In view of the closure of the Strait of Hormuz, steps have been taken to (i) ensure stable availability of petroleum products and LPG across the country and (ii) safeguard Indian vessels and seafarers operating in the region (PIB, March 22, 2026).

4 All-India water storage in 166 major reservoirs stands at 47 per cent of the total capacity as of April 02, 2026, as against 40 per cent a year ago and decadal average of 37 per cent. As per the second advance estimate (SAE) for 2025-26, total foodgrain production is estimated to grow by 3.0 per cent.

5 PMI manufacturing Future Output Index in March 2026 was placed at 67.3. Future Output Index has hovered above 56.3 since April 2025.

6 GST E-way bills increased by a robust 17.2 per cent in Q4:2025-26. Gross GST revenues rose by 7.1 per cent and motor vehicle sales (retail) expanded by 22.2 per cent in Q4. Steel consumption grew by 12.8 per cent and cement production increased by 9.3 per cent in February 2026. Petroleum consumption growth decelerated to 2.2 per cent in March from 5.5 per cent in February 2026. PMI services for March has moderated to 57.5 from 58.1 in February.

7 Two-wheeler and tractor retail sales registered double digit growth of 23.2 per cent and 28.5 per cent, respectively, in January-February 2026.

8 According to the monthly periodic labour force survey (PLFS), all-India unemployment rate remained low at 4.9 per cent in February. Demand for work under the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) declined by 21.0 per cent in Q4:2025-26.

9 The central government’s capex is budgeted to expand by 11.5 per cent in 2026-27. Effective capital expenditure (including grants-in-aid to state governments for capital expenditure) is budgeted to grow at 22.1 per cent.

10 As per the quarterly order books, inventories, and capacity utilisation (OBICUS) survey of the RBI, seasonally adjusted capacity utilisation (CU) of the manufacturing sector at 75.5 per cent in Q3:2025-26 was marginally above the long-term average of 73.9 per cent.

11 Bank credit to textiles, chemicals, base metals, gems and jewellery and engineering goods increased y-o-y by 8.2 per cent, 19.1 per cent, 15.2 per cent, 40.2 per cent and 36.0 per cent, respectively, in February 2026.

12 Services export expanded sharply by 9.8 per cent in January and 9.7 per cent in February 2026.

13 Food and beverages division recorded an inflation of 3.4 per cent in February, within which ‘Meat, fresh, chilled or frozen’, ‘fruits and nuts’, ‘oils and fats’, and ‘fish and other seafood’ classes have recorded an inflation of 9.7 per cent, 8.6 per cent, 7.4 per cent and 7.0 per cent, respectively.

14 During September-December 2025, CPI food and beverages group recorded a y-o-y deflation in the range of (-) 3.7 to (-) 1.4 per cent (as per the previous CPI (2012=100) series).

15 Fuel represents the group ‘Electricity, gas and other fuels’ and class ‘Fuels and lubricants for personal transport equipment’, both of which recorded a modest inflation of 0.1 per cent in February 2026.

16 This is significantly lower than 4.8 per cent recorded in the CPI-2012 series for the month of December 2025 on account of lower housing inflation and lower inflation in precious metals category, partly reflecting changes in specification of precious metals to include jewellery prices instead of bullion prices.

17As the West Asia conflict led to a sharp spike in energy prices, domestic LPG prices were increased by ₹60; commercial LPG prices were increased in two tranches first by ₹115 per cylinder and again by ₹195.5 per cylinder; prices of diesel for bulk buyers (industrial use) by about 25 per cent; and prices of some variants of premium petrol were increased by about ₹2 per litre since March 2026.

18 As on March 16, 2026, the rice and wheat stocks stood at 742 lakh tonnes (9.7 times the buffer norm) and 229 lakh tonnes (1.7 times the buffer norm), respectively.

19 As per National Oceanic and Atmospheric Administration, United States, El Niño is likely to emerge (with a 62 per cent probability) during June-August 2026 and is expected to persist at least till December 2026.

20 According to WTO (March 2026), world goods and services trade volume growth is expected to moderate to 2.7 per cent in 2026 from 4.7 per cent in 2025.

21 Exports contracted in 7 destinations (38.5 per cent share in 2024-25) out of top 10 destinations covering 52.6 per cent of India’s exports in 2024-25. Among these 10 destinations, exports to the US contracted by 17.5 per cent, followed by the Netherlands (14.2 per cent) and the UK (6.3 per cent) during January-February 2026.

22 Rise in gold imports was driven by an increase in import volume as well as a rise in gold price. While gold import volume rose by 146.1 per cent during January-February 2026, gold price rose by 74.4 per cent during the same period.

23 As India’s merchandise imports grew faster than merchandise exports, trade deficit rose to US$ 61.8 billion in January-February 2026 from US$ 37.1 billion during January-February 2025.

24 India’s services exports grew by 9.7 per cent (y-o-y) during February 2026, while services imports grew by 16.2 per cent. Net services exports grew by 4.1 per cent in February 2026. For 2025-26 so far, i.e., April-February 2025-26, services exports rose by 8.9 per cent, while imports grew by 3.4 per cent, resulting in a growth of 14.6 per cent in services trade surplus.

25 India’s inward remittance receipts increased by 5.1 per cent y-o-y to US$ 37.8 billion in Q3:2025-26. For 2025-26 so far, i.e., April-December 2025-26, net remittance receipts rose by 11.3 per cent.

26 Trade deals with the UK and Oman have been signed; trade deal with the European Free Trade Association (EFTA) came into effect from October 1, 2025; trade deals with New Zealand and the European Union have been concluded; and the interim trade deal with the US has been announced.

27 Gross FDI flows to India grew by 18.1 per cent to US$ 88.3 billion in April-February 2025-26 from US$ 74.7 billion a year ago. Net FDI inflows stood higher at US$ 6.3 billion during April-February 2025-26 from US$ 1.5 billion a year ago.

28 As per fDi Markets data, during 2025-26 (April-January), greenfield project announcements to India were US$ 65 billion (US$ 73 billion during April-January 2024-25). Top 5 greenfield FDI project announcements in the fields of information technology and banking by Amazon, Microsoft, Google, General Catalyst and the MUFG Bank reflect investor optimism and a strong FDI pipeline.

29 During 2025-26, FPI to India recorded net outflows of US$ 18.6 billion from the equity segment, while debt segment registered net inflows of US$ 2.1 billion. During April 1-6, 2026, FPI to India recorded net outflows of US$ 4.0 billion and US$ 1.3 billion from the equity and debt segments, respectively.

30 Net inflows under external commercial borrowings to India moderated to US$ 11.9 billion during April-February 2025-26 from US$ 16.0 billion a year ago. Non-resident deposits recorded net inflows of US$ 11.0 billion in April-February 2025-26, lower than US$ 14.6 billion during April- February 2024-25.

26 Trade deals with the UK and Oman have been signed; trade deal with the European Free Trade Association (EFTA) came into effect from October 1, 2025; trade deals with New Zealand and the European Union have been concluded; and the interim trade deal with the US has been announced.

27 Gross FDI flows to India grew by 18.1 per cent to US$ 88.3 billion in April-February 2025-26 from US$ 74.7 billion a year ago. Net FDI inflows stood higher at US$ 6.3 billion during April-February 2025-26 from US$ 1.5 billion a year ago.

28 As per fDi Markets data, during 2025-26 (April-January), greenfield project announcements to India were US$ 65 billion (US$ 73 billion during April-January 2024-25). Top 5 greenfield FDI project announcements in the fields of information technology and banking by Amazon, Microsoft, Google, General Catalyst and the MUFG Bank reflect investor optimism and a strong FDI pipeline.

29 During 2025-26, FPI to India recorded net outflows of US$ 18.6 billion from the equity segment, while debt segment registered net inflows of US$ 2.1 billion. During April 1-6, 2026, FPI to India recorded net outflows of US$ 4.0 billion and US$ 1.3 billion from the equity and debt segments, respectively.

30 Net inflows under external commercial borrowings to India moderated to US$ 11.9 billion during April-February 2025-26 from US$ 16.0 billion a year ago. Non-resident deposits recorded net inflows of US$ 11.0 billion in April-February 2025-26, lower than US$ 14.6 billion during April- February 2024-25.

32 The average daily net absorption under the liquidity adjustment facility (LAF) during December and January stood at ₹0.82 lakh crore and ₹0.79 lakh crore, respectively. In February 2026, average daily net absorption under the liquidity adjustment facility (LAF) increased to at ₹2.6 lakh crore. In March 2026, the average daily net absorption under the liquidity adjustment facility stood at ₹1.7 lakh crore and increased to ₹3.5 lakh crore in April (up to April 6, 2026).

33 The WACR on average traded 6 basis points below the policy repo rate.

34 The rates on 3-month treasury bill, 3-month certificates of deposit and 3-month commercial paper averaged 5.32 per cent, 7.18 per cent and 7.29 per cent respectively since February policy.

35 The 10-year G-sec yield hardened to 7.05 per cent as on April 06, 2026 from 6.66 per cent as on February 27, 2025.

36 During the current easing cycle February 2025-February 2026, the weighted average lending rate (WALR) of Scheduled Commercial Banks on fresh and outstanding rupee loans declined by 89 bps (decline of 92 bps was interest rate effect) and 87 bps, respectively. On the deposit side, the weighted average domestic term deposit rate (WADTDR) on fresh and outstanding deposits declined by 97 bps and 47 bps, respectively, over the same period.

37 The Reserve Bank conducted OMO purchase auctions amounting to ₹1,50,000 crore and long-term forex buy/sell swap auction of USD 10 billion in February and March 2026.

38 SCB Parameters: The system-level Capital to Risk Weighted Assets Ratio (CRAR) of 16.91 per cent in December 2025 was well above the regulatory minimum level. Ratio of non-performing loans improved further (GNPA ratio at 1.89 per cent in December 2025 vis-à-vis 2.42 per cent in December 2024, NNPA Ratio at 0.44 per cent in December 2025 vis-à-vis 0.55 per cent in December 2024). Liquidity buffers were robust, with an LCR of 125.85 per cent as of end December 2025. The annualised return on assets (RoA) and return on equity (RoE) stood at 1.32 per cent and 12.95 per cent, respectively, in December 2025. Net Interest Margin was 3.28 per cent in December 2025 (3.49 per cent in December 2024).

39 NBFC Parameters: Total CRAR of NBFCs was 25.59 per cent and Tier I CRAR was 23.71 per cent in December 2025, well above the minimum regulatory requirements. GNPA ratio has improved from 2.52 per cent in December 2024 to 2.14 per cent in December 2025, while NNPA ratio also improved from 1.10 per cent in December 2024 to 0.93 per cent in December 2025. RoA for the sector decreased slightly from 2.89 per cent in December 2024 to 2.71 per cent in December 2025. NIM has slightly decreased from 4.54 per cent in December 2024 to 4.43 per cent in December 2025.

40 The total flow of resources from bank and non-bank sources to the commercial sector stood higher at ₹40.4 lakh crore vis-à-vis ₹32.2 lakh crore in the corresponding period of the previous year. The increase in flows from non-food bank credit (₹6.9 lakh crore) and corporate bond issuances by non-financial entities (₹ 1.7 lakh crore) have been the major drivers of this growth.

41 Bank Credit recorded a growth (y-o-y) of 13.8 per cent as on the fortnight ended March 15, 2026, as compared to 11.0 per cent a year ago (based on fortnightly Section 42 return of RBI). Credit growth (y-o-y) has trended upward since May 2025.

Reserve Bank of India

Monetary Policy Statement, 2026-27

Resolution of the Monetary Policy Committee

April 6 to 8, 2026

Monetary Policy Decisions

The Monetary Policy Committee (MPC) held its 60th meeting from April 6 to 8, 2026, under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Poonam Gupta and Shri Indranil Bhattacharyya attended the meeting.

2. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent. Consequently, the standing deposit facility (SDF) rate remains at 5.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate remains at 5.50 per cent. The MPC also decided to continue with the neutral stance.

Growth and Inflation Outlook

Global Outlook

3. The outbreak of the conflict in West Asia has led to severe disruption of global supply chains. This poses an unprecedented challenge for the global economy – higher prices and lower global growth. In this environment, monetary policy faces a difficult trade-off – anchoring inflation expectations through policy tightening while minimising its impact on growth forgone. Sovereign bond yields, already high from long-run fiscal sustainability concerns across major economies, have further hardened, driven by inflation fears. Additionally, equity valuations have corrected. As a result of the turmoil in global financial markets, the US dollar has rallied, buoyed by safe-haven demand that has exerted pressure on currencies of major economies. Further intensification of the conflict, its prolongation and widening geographical spread remain the key downside risks to the global outlook.

Domestic Outlook

4. On the domestic front, the Indian economy remained resilient in 2025-26. Real gross domestic product (GDP) is estimated to grow by 7.6 per cent (y-o-y) during the year, as per the Second Advance Estimates (SAE) of the new GDP series (base year 2022-23). Private consumption and fixed investment contributed significantly to overall growth, while net external demand remained soft. On the supply side, estimated real GVA growth of 7.7 per cent was driven by buoyant services sector and robust manufacturing activity.

5. Looking ahead, elevated energy and other commodity prices coupled with supply shock due to disruptions in the Strait of Hormuz would act as a drag on domestic production in 2026-27. Heightened volatility in global financial markets with its spillover on domestic financial conditions would weigh on growth prospects. On the external front, merchandise exports may be adversely impacted from disruptions to key shipping routes and the concomitant rise in freight and insurance costs in case the conflict is long-drawn. On the other hand, sustained momentum in services sector, persisting impact of GST rationalisation, rising capacity utilisation in manufacturing, and healthy balance sheets of financial institutions and corporates should continue to support domestic demand. In this milieu, the Government’s focus on scaling up domestic manufacturing in several strategic and frontier sectors announced in the Union Budget 2026-27 bodes well for India’s ensuing growth trajectory. Taking all these factors into consideration and on the assumption that the adverse impact of the conflict would remain contained in the near term, real GDP growth for 2026-27 is projected at 6.9 per cent, with Q1 at 6.8 per cent; Q2 at 6.7 per cent; Q3 at 7.0 per cent; and Q4 at 7.2 per cent (Chart 1). Further escalation of the conflict, its continuation over a wider geographical spread and uncertainty regarding the damage to the energy infrastructure, apart from weather related events, pose downside risks to the domestic growth outlook.

6. As per the new CPI series (2024=100), headline inflation increased to 3.2 per cent in February 2026 from 2.7 per cent in January. The uptick was primarily driven by unfavourable base effects even as the momentum remained muted. While food inflation increased in February, core (excluding food and fuel) inflation remained unchanged. Excluding precious metals, core inflation remained moderate at 2.1 per cent in January and February, suggesting subdued underlying inflation pressures.

7. The ongoing conflict has led to large volatility in international energy and other commodity prices imparting considerable uncertainty to the near-term inflation outlook. The pass-through of higher global energy prices has resulted in price increases in select fuels such as premium petrol and LPG and diesel for industrial use. On the other hand, the near-term food supply prospects have been boosted by robust rabi crop providing some comfort. Considering all these factors, CPI inflation for 2026-27 is projected to be at 4.6 per cent with Q1 at 4.0 per cent; Q2 at 4.4 per cent; Q3 at 5.2 per cent; and Q4 at 4.7 per cent. Persistently elevated energy prices due to the West Asia conflict and possible El Niño conditions (which could have a negative impact on southwest monsoon) pose upside risks to inflation (Chart 2). Core inflation is projected at 4.4 per cent for 2026-27 and, excluding precious metals, it is even lower indicating that underlying inflation pressures are expected to remain contained.

Rationale for Monetary Policy Decisions

8. Since the last policy meeting, geopolitical uncertainties have heightened significantly. Headline inflation remains contained and below the target, but upside risks to the inflation outlook have increased, driven by increased energy price pressures and probable weather disturbances affecting food prices. Core inflation pressures remain muted, although supply chain dislocations and the risk of second-round effects render the future inflation trajectory uncertain.

9. High frequency indicators till February 2026 suggest the continuation of strong momentum in economic activity. Growth impulses continue to be supported by robust private consumption and investment demand. However, the West Asia conflict will adversely impact growth. Higher input costs associated with increase in energy prices and international freight and insurance costs along with supply-chain disruptions could constrain availability of key inputs for downstream sectors, thus impairing growth. The Government has taken several measures targeted at supporting exports and protecting supply chains, which should mitigate the adverse impact of the conflict.

10. The MPC noted that the intensity and the duration of the conflict in West Asia and the resultant damage to the energy and other infrastructure add risk to the inflation and growth outlooks. However, the fundamentals of the Indian economy are on a stronger footing, providing it with greater resilience to withstand shocks now than in the past. The economy is confronted with a supply shock. It is prudent to wait and watch the changing circumstances and the evolving growth-inflation outlook. Accordingly, the MPC voted to keep the policy rate unchanged even as it remains vigilant, closely monitoring incoming information and assessing the balance of risks. The MPC also decided to continue with the neutral stance, retaining the flexibility to respond judiciously to incoming information.

11. The minutes of the MPC’s meeting will be published on April 22, 2026.

12. The next meeting of the MPC is scheduled for June 3 to 5, 2026.

(Brij Raj)

Chief General Manager

Press Release: 2026-2027/36