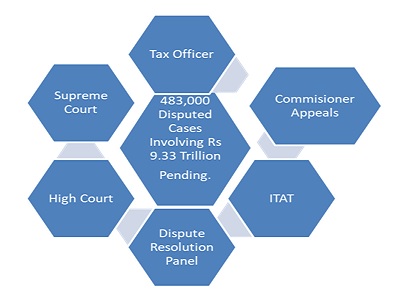

Recently there was an outreach by the Income Tax Department to the practicing CA’s to impress upon their clients to opt for the Vivadh se Vishwas scheme which will shortly conclude on 31-12-2020, though there is a likely hood of the scheme being further extended following the Luke warm response to the said scheme as announced by the Finance Minister Mrs Nirmala Sitharaman In March 2020, but the good intentions of the Government needs a thorough overall to convert Paper Tax Collection in to Actual Collections. Let Us have a look at the Tax Dispute Hierarchy structure to have a Bird’s eye view of the overall Disputed Major Tax Problems.

What is Vivad se Vishwas scheme ?

The Direct Tax Vivad se Vishwas Bill, 2020 has been introduced by the Government of India to settle pending direct tax litigations for litigants, and enable the government to collect revenues locked up in litigation.

The Direct Tax Vivad se Vishwas bill, 2020 was tabled on 5 February 2020, in the Lok Sabha, to provide a resolution for pending income-tax disputes. Thereafter, official amendments to the bill were proposed for accommodating the representation received from key stakeholders. However, several aspects of the scheme required clarifications, which the government provided in the form of an amended bill, passed by the Lok Sabha on 4 March, and by way of a circular issued by the Central Board of Direct Taxes (CBDT). The amended bill was passed by the Rajya Sabha on 13 March 2020. The President of India provided his assent to the bill on 17 March 2020, thus enacting the “Direct Tax Vivad se Vishwas Act, 2020“.

What need to be done to make it a Hit scheme

Issues pertaining to Transfer pricing, Global M&A ,GAAR need to be quickly resolved because majority of the disputes have risen over the interpretation of Law & Inadmissibility of expenses which have created a difference between the AO & Tax Payer, in majority of the cases the Tax Payer wins the case because the actions of AO are not substantiated at the higher jurisdictions, it can be case of wrong interpretation of the IT act or genuine expenses of the Tax Payer not approved by the AO since he is the first source of the contact in the entire Tax Litigation Process.

Also the law needs a clarity, in Developed countries only the tax payer can appeal to higher courts pertaining to the tax claims made by the taxation authorities however in India it’s a different ball game, In India, one wing (Assessment) of the Tax administration is empowered to Appeal to the Tax tribunal (ITAT) against the order of the Appeals Wing [CIT(A)] of the same Tax administration.

Under Vivadh Se Vishwas scheme, 45,855 cases have been filed in Form No 1 up to 17/11/2020, an amount of Rs72,480 Crores have been paid and disputes amounting to Rs 131,929 Crores have been settled says a communique form IT Department.

Author Bio