Valuation Made Easier

Introduction

Recently I made a small Thanksgiving trip to Hilltop temple Anegudde where you have the famous Lord Ganapathi temple , while driving across NH 66, you come across the landmark & iconic circular Glass Building HQ of Robosoft Technologies, what I liked was usually I used to see the name of the company in English and Kannada and this time I saw the name in the Japanese language too, it so because of the new owners Japanese technology-focused staffing and services firm TechnoPro Holdings which had bought earlier Udupi-based digital transformation solutions provider Robosoft Technologies for an estimated Rs 805 crore. The deal was structured in two tranches. TechnoPro will purchase an 80% stake in Robosoft in the first tranche for around Rs 580 crore, and buy the remaining by July next year and all the transactions or deal done is based on valuation. Now the question arises as to what is valuation and how to arrive at the figures.

Valuation is an interesting subject, during the course of my corporate career in the UAE I had the unique opportunity to work on the valuation part of 2 companies, the first being the parent company and the second being the highly profitable subsidiary company and we took the help of FAS of Big 4 for the parent company and one top management consulting firm of Abu Dhabi for the subsidiary and I was common to the valuation of both the companies and they adopted the similar basis of valuation beginning with 5 years of Past financials. Basically, valuation quite resembles the extrapolation of data which we had studied in Statistics with links to the past data and certain assumptions of growth with 3 sets of values under 3 different scenarios with some overlapping figures and leave it to the top management keeping in mind the present market conditions to adopt one set of valuation figures along with the valuation figures.

Importance of Valuation

A valuation is an estimate of how much a business, property, antique, or asset is worth. If you have a business and seek funding from investors, they will need to know how much your enterprise is worth. This is achieved through a valuation – an estimate of your company’s overall worth. A business valuation can be done for the following types of industries starting from

♦ Startup companies

♦ Growing companies

♦ High-growth companies

♦ Mature companies

♦ Falling or declining companies

Only last year that is 2021, Nearly 22 companies in India joined the unique unicorn club which is a mighty achievement on the basis of valuation which is commendable, valuation plays an important part in the formation of a unicorn, Between the years 2018-2022, almost 105 startups attained the status of Unicorns but at present, the number stands at 84.

What is a Unicorn?

“Unicorn” is a term used in the venture capital industry to describe a privately held startup company with a value of over $1 billion (Rs 8200 Crores). The term was first popularized by venture capitalist Aileen Lee, founder of Cowboy Ventures, a seed-stage venture capital fund based in Palo Alto, California.

Many different techniques may be used to determine something’s value. An expert who is making a valuation of a company will look at its management, its capital structure, the market value of its assets, and its outlook (the prospect of future earnings), there are certain basic requirements in the process of valuation and there are certain skills associated with it and they can be broadly classified as

√ Nature of the business

√ Economic Outlook

√ Book value

√ Earning capacity

√ Dividend paying capacity

√ Goodwill or other intangible assets

√ Market capitalization.

In the world of business and finance, items that are typically valued are financial assets, such as stocks, options, commercial enterprises, patents, or trademarks. Valuations may also be carried out on liabilities, such as the bonds issued by a company, having said there are many reasons and scope for valuation under different circumstances and they could be for the following reasons.

√ Valuation of the fresh issue of shares (IPOs) can be done by using the discounted cash flow method or net asset value method

√ Valuation for transfer of shares for both quoted and unquoted shares for 3 different scenarios like a valuation for capital gains purpose / Transfer Pricing? indirect transfer of assets.

√ Valuation for buyback was fancied earlier but these days it lost its charm/sheen due to tax liability of 20 % plus surcharges this scheme was very popular till recently.

√ Valuation for the purpose of mergers is usually based on the Fair Market Value of the merging companies to determine the swap ratio.

√ Valuation for sweat equity, what is sweat equity

√ Sweat equity is a non-monetary benefit that a company’s stakeholders give in labor and time, rather than a monetary contribution, that benefits the company. Sweat equity is rewarded in the form of sweat equity shares. These are shares given out by a company in exchange for labor and time rather than a monetary amount, the best example was the formation of Kochi tuskers Kerala IPL team with the blessings of the colorful MP from Kerala which later got terminated due to nonpayment of 10 % Bank guarantee.

√ Valuation of Employee stock option scheme or ESOP

An ESOP (Employee stock ownership plan) refers to an employee benefit plan which offers employees an ownership interest in the organization. There are defined rules and regulations laid out in the Companies Rules which employers need to follow for granting Employee stock ownership plans to their employees

> Valuation for Financial Reporting

India originally intended to converge with IFRSs in a phased approach beginning in 2011, but the transition to Ind AS was postponed. In January 2015, the Indian Ministry of Corporate Affairs (MCA) released a revised roadmap that reflects that, in essence, companies with a net worth of Rs. 500 crores or more will have to mandatorily follow Indian Accounting Standards (Ind AS), which are largely converged with International Financial Reporting Standards (IFRSs), from 1 April 2016. Corporates having a net worth of less than Rs. 500 crores but are listed, or in the process of getting listed, and companies with a net worth of Rs. 250 crores or more will have to follow the new norms from 1 April 2017. For banking, insurance, and non-banking finance companies, which were exempt from the general roadmap, a separate one was drawn up in January 2016 that will see a phased approach with Ind AS adoption beginning from 1 April 2018. This was later deferred to 1 April 2019l2019

> Valuation for IBC (Insolvency and Bankruptcy Board of India)

The Government of India introduced the IBC in 2016 to resolve claims involving insolvent companies. The bankruptcy code is a one-stop solution for resolving insolvencies, which previously was a long process that did not offer an economically viable arrangement. The code aims to protect the interests of small investors and make the process of doing business less cumbersome. The IBC has 255 sections and 11 Schedules. IBC was intended to tackle the bad loan problems that were affecting the banking system.

When carrying out a valuation of a business, there are several possible approaches:

1. The ‘Asset Approach’ looks at the company’s balance sheet and focuses on assets and liabilities.

2. The ‘Earning Valuation Approach’ looks at the economic benefits of owning the company – will the company be able to produce wealth in the future?

3. The ‘Market Approach’ focuses on the competition. How much are similar companies going for?

Valuations are required for several reasons, including merger and acquisition transactions (M &A), litigation, investment analyses, financial reporting, and capital budgeting.

Reasons for a business valuation

There are many reasons why somebody may decide to have a business valued:

- to improve the business’ real or perceived value

- to choose a good time to buy or sell the commercial enterprise

- to negotiate a better price – either as a seller or buyer

- to complete the purchase of the business more rapidly

- to raise equity capital

- to create an internal market for shares

- to motivate management – regular valuations can provide measurement and incentive for management performance and help management to focus on important issues.

Types of valuation

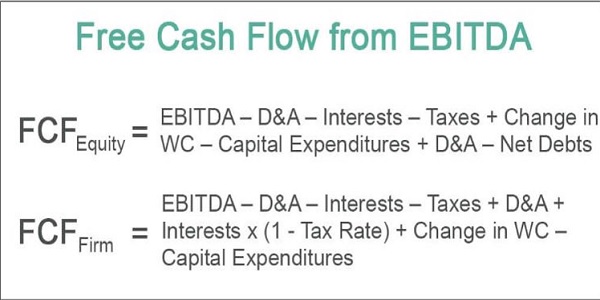

* DCF Valuation

* Free Cash Flow to Firm

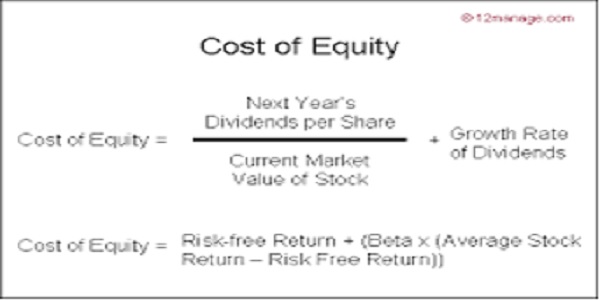

Cost Of Capital = Discount Rate – WACC

Cost of Equity Calculation = Discount Rate – Cost of Equity

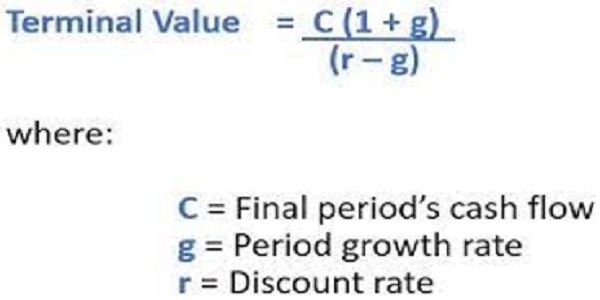

Terminal Calculation:

Comparable Companies Multiple (CCM) Method: –

Comparable Companies Multiple Method, also known as Guideline Public Company Method, involves valuing an asset based on market multiples derived from prices of market comparable traded on the active market.

Rule of Thumb Valuation

- A company’s value is mainly decided on multiples of its annual post-tax profit. A small unquoted business is generally worth, as far as potential buyers are concerned, between five and ten times its annual post-tax profit. Some IT businesses have been sold for considerably more, sometimes up to seventy times their annual net profit.

- When a potential buyer is valuing a company, he or she may also make anentry-cost valuation. Rather than purchase a business, how much would it cost to create a similar company from scratch? The estimated amount is the entry cost valuation.

- The worth of a company depends on how much profit a buyer can make from it, balanced by the perceived risks involved. Past profitability and current asset values are only some of the factors that are taken into account. Often, intangible factors such as intellectual property and goodwill provide the most value

- There is a saying in the venture capital industry: The value of a business is only what someone is willing to pay for it. In other words, the market, and your ability to attract investors and negotiate with them will determine the value or selling price.

Remember that many factors affect the value of your business. Seeking professional assistance can help you calculate an accurate value for your business because of the nature of the business which differs from a case-to-case basis and the valuation depends finally on the basis of adopting the method.

Author Bio